Any general contractor has a never-ending list of items on their to-do list. One thing you should never overlook is buying general liability insurance. General liability insurance protects you and your business. Without general liability insurance, you would incur the costs of any lawsuits brought against your business. We recommend the top 7 companies providing general liability insurance for contractors to inform your selection.

- The 7 best general liability insurance providers for contractors

- What is general liability insurance?

- What does general liability insurance cover?

- Why do contractors need general liability insurance?

- Should contractors add their clients as an additional insured to their general liability insurance policy?

- How much general liability insurance do contractors need?

- How much does general liability insurance for contractors cost?

- How can contractors get cheap general liability insurance?

The 7 best general liability insurance providers for contractors

Here are our recommendations of the 11 best general liability insurance companies for contractors, both general and independent contractors.

- CoverWallet: Best for comparing online quotes and knowledgeable agents

- The Hartford – Best Overall

- Simply Business: Best broker for a fast online quote

- State Farm: Best for combining personal and business insurance

- Chubb – Best for small businesses with international clients

- Hiscox – Best for small businesses operating out of a home office

- Next Insurance – Best Overall for Small Independent Contractors

CoverWallet: Best for comparing online quotes and knowledgeable agents

CoverWallet is a national digital commercial insurance broker. They work with several business insurance companies and help you compare quotes from these companies.

If you have questions about what type of insurance you need, CoverWallet can do an insurance assessment for you. If you’re a general contractor, you’ll definitely need general liability insurance, but you might need property insurance or workers compensation insurance as well.

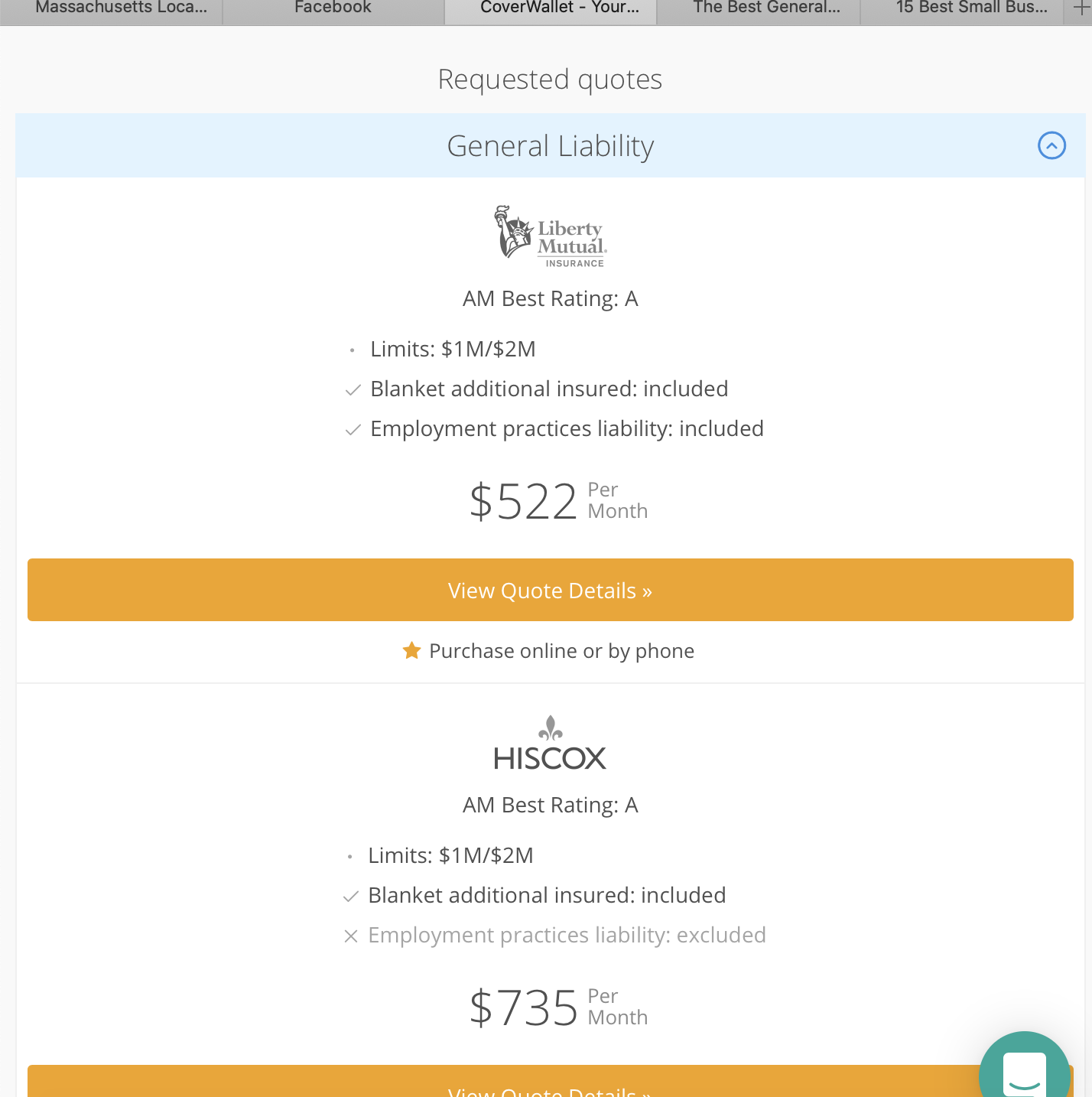

To get a quote, you’ll answer questions about your business, such as how much experience you have in your industry, what your yearly revenue is, and what sort of work you do. Then CoverWallet will come up with a quote.

The following quote is for a general contractor in New Jersey with $1 million in revenue a year.

The Hartford – Best Overall

The Hartford offers a number of business policies, including general liability insurance, commercial property insurance, and workers compensation insurance. They also offer:

- Data breach insurance

- Professional liability insurance

- Commercial auto insurance

They earn an A+ score from the Better Business Bureau. Their customer service and claims servicing are rated very highly (97% of respondents would recommend them to a friend). The Hartford was the first insurer to create a small business division 35 years ago, so they’re experienced with meeting small business owners’ needs.

Historically, the Hartford sells business insurance through their agent network only. However, they have recently improved their digital capabilities significantly. Small businesses can get quotes, buy and bind policies, and manage their business insurance policies, including filing a claim, completely digitally through their website or mobile app.

The Hartford also distributes their business insurance products to several insuretech commercial insurance broker such as CoverWallet, Simply Business, Embroker, etc. making it easier for small business to compare their quotes with others’.

>>MORE: Full Review of the Hartford Small Business Insurance

Simply Business: Best for easy online quotes

Simply Business works with ten different insurance companies to provide you with several quotes. They have a 4.3 out of 5 score on Trustpilot. Most people praise how quick and easy it was to get insurance, although about 15% rate them as “bad” and cite lack of communication and the fact that they feel they were misled.

State Farm: Best to combine personal and business insurance

State Farm offers many different types of personal and business insurance, including general liability. They also offer the following essential insurance that contractors may need:

- Commercial liability umbrella

- Professional liability

- Errors and Omissions

- Employment Practices Liability Insurance (insurance against lawsuits from former employees)

- Business Owners Policies

They cover industries such as HVAC contractors, plumbers, painters, electricians, both independent and general contractors. If you want to combine and manage all of your personal and business insurance policies with the same carrier, State Farm is a perfect option for you.

To get a quote, you enter your zip code, and an agent will contact you.

Chubb – Best for small businesses with international clients

Chubb is a good choice if your business operates internationally, as they have on-the-ground resources in 54 countries. They have 130 years of experience and the largest market share of general liability insurance for small businesses. They offer almost every insurance policy a small business could possibly want, so if you find yourself in need of additional insurance at some point down the road, Chubb can accommodate you. If your business grows, Chubb can supply whatever insurance you need.

Their liability insurance is divided into two basic categories:

- Premises and operations liability

- Products and completed operations liability

Their customer reviews are positive, and they specialize in quick processing of claims.

If you’re only interested in general liability insurance, you can get an online quote from Chubb but for most other types of insurance, you’ll have to contact a broker or an agent.

Learn more about Chubb’s general liability insurance for US companies.

Hiscox – Best for small businesses operating out of a home office

Hiscox gets top marks for the breadth of their policy offerings (they insure everyone from civil engineers to hot dog cart vendors). They earn an A+ rating from the Better Business Bureau, and they have mostly positive reviews from customers. They are particularly adept at working with people who operate a business out of their home.

Regarding costs, Hiscox says that general liability insurance typically costs $30 a month, based on a survey they took of 50,000 small business owners. They also offer flexible payment options at no additional charge.

Next Insurance: Best overall for small independent contractors

Next Insurance is a newcomer in the general liability insurance business, having been established in 2015. They offer a range of insurance products for small businesses, including general liability, commercial auto, and professional liability. They are not available in every state, though they have plans to go national. They have an easy online quote system. All you have to do is answer about ten questions and they’ll give you a quote. For a general contractor in MA (as an example) they quoted $62.50 a month.

What is General Liability Insurance?

Basic general liability insurance covers anything that can happen to other people or property during the course of your doing business. It does not protect you, your employees, or your equipment from damage or injury.

Imagine you’re remodeling a kitchen for a client. You set your drill down on the floor. Your client, Mr. Client, trips over it and injures his hip. Then he sues you for negligence. General liability insurance will protect you.

You’re building a new basement in another client’s house. You accidentally gouge a hole in their expensive parquet floor. General liability insurance will protect you in this case as well.

Even if you are the most careful contractor in the world, accidents can and will happen. General liability insurance is a small price that you will be happy you paid when an accident occurs.

Some states will require a general contractor to have general liability insurance, but even if you live in a state that doesn’t require it, customers may ask if you have it, and they may be more likely to hire you if you do.

For small businesses with less than $1 million annual revenue, general liability insurance policy is usually purchased in Business Owners Policy (BOP) package, which also includes property coverage and business interruption insurance and can be customized with other less popular policies too.

>>MORE: Contractor Insurance: What; How Much; And Where to Get It?

What does General Liability Insurance Cover?

- Bodily injury to someone or property damage due to business

- Product liability if someone sues you for a defective product

- Libel, slander and copyright infringement

>>MORE: How Much does General Liability Insurance Cost?

>>MORE: Insurance for General Contractors: Coverage, Cost, and Providers

What doesn’t General Liability Insurance Cover?

- Damage to your equipment

- Employee on-the-job injuries

- Malpractice

- Employee discrimination suits

- Intentional injury or fraud

- Failure to protect information

Basically, general liability insurance covers anything that happens to customers or property while you’re on the job.

>>MORE: Best General Liability Insurance for Small Businesses

What type of contractors need general liability insurance?

Almost every type of contractor, both general contractors and independent contractors, needs general liability insurance. General liability insurance protects your business from being sued for damaging property, causing bodily harm, or advertising injury. If you work with the public at all, you should have general liability insurance.

Why do contractors need general liability insurance?

Because it is the most essential liability insurance to protect contractors from being sued in an unfortunate event.

Another reason to get general liability insurance is that many clients prefer to work with contractors who have it. Otherwise, they could be held responsible and no one wants that.

A third reason why you need general liability insurance is that your state may require it. State laws differ, but many states require general contractors to carry general liability insurance. Check with your state, but even if they don’t require it, it’s certainly advantageous to have.

Should contractors add their clients as an additional insured to their general liability insurance policy?

Contractors often work with subcontractors, clients, designers, and project owners. Sometimes the project owner will ask to be listed as an additional insured on the contractor’s general liability policy. This ensures that the client is covered against bodily injury, property damage, and the legal costs resulting from these hazards.

Keep in mind that adding a client to your general liability policy could max out your policy, if the additional insured seeks coverage under your policy. You don’t want to leave yourself underinsured. Also, there have been documented cases of such agreements being interpreted by the courts to mean the client is covered whether the general contractor was negligent or not. On the other hand, some clients may refuse to work with a contractor that won’t add them to their policy. So, it’s a risk you’ll have to weigh.

If you decide to add on an additional insured, merely contact your agent or your insurance company to make this request.

Compare general liability insurance for general contractors vs. independent contractors

Since a general contractor supervises and manages construction projects, they incur higher risks. A worker could fall off of a roof, a customer could trip over some construction debris, or a client’s furniture could be damaged during a remodel. These incidents may be caused by a general contractor’s employee or an independent contractor.

While a general contractor is an independent contractor, not all independent contractors are general contractors. The term general contractor refers to someone who oversees a construction project, entering into a contract with a property owner. An independent contractor is simply someone who is self-employed. They could work in any industry, such as:

- Musicians

- Photographers

- Hair stylists

- Dance instructors

- Accounting

- IT consulting

- Construction

According to the IRS, you are an independent contractor if you perform work that is not controlled by your employer. For example, a doctor with a small practice who sees patients in an office is an independent contractor. A doctor who sees patients in a hospital and is responsible for working a certain number of hours is an employee.

>>MORE: The 9 Best Independent Contractor Insurance Companies

While independent contractors may or may not need general liability insurance, depending on what kind of work you do, a general contractor always need general liability insurance. If you as an independent contractor provide IT services and a client trips over an old desktop computer, you could be sued. If you never deal with the public, for example, you do freelance writing from home, you could probably skip general liability insurance.

On the other hand, general contractors, are those who usually deals with customers or clients. They definitely should should have it. In fact, many clients will not work with general contractors if they don’t have proof of sufficient general liability coverage.

>>MORE: The 5 Best General Contractor Insurance Companies

How much general liability insurance do contractors need?

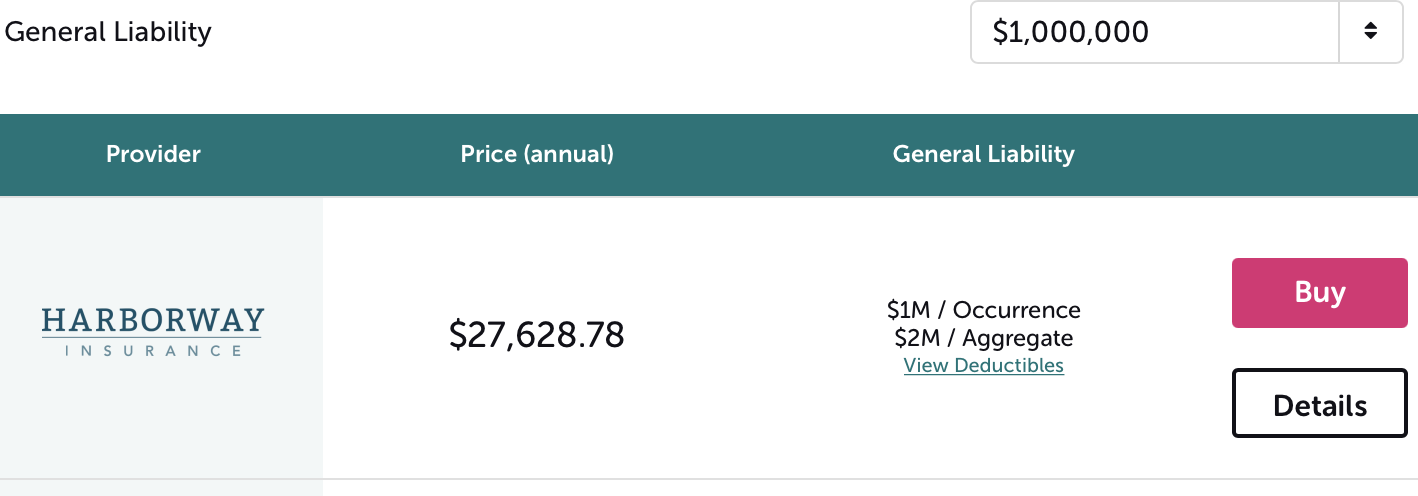

Most small business owners choose $1 million occurrence limit and a $2 million dollar aggregate limit, according to small business insurance digital broker Insureon. Insureon also estimates that the median annual cost of general liability insurance for a general contractor is about $825 a year. However, there are so many variables that go into how much you pay for liability insurance that it’s almost impossible for a company to give an estimate. These are the variables that go into how much you’ll pay for general liability insurance:

- If you’re a sole proprietor, LLC, partnership, association, corporation, or joint venture

- How many years you’ve been in business

- How much experience you have in the industry

- How many employees you have and if they are full-time or part-time

- Expected payroll for said employees

- If you subcontract work

- If you use day laborers

- What your projected revenue is for the coming year

- If you have international clients

- Amount of risk involved in your business (roofers pay a higher rate)

- Where you usually perform work

- What licenses you have

Depending on where your quote is from, there could be even more questions. With all of these variables, it’s challenging to get estimates from any insurance company. Other factors include how much insurance you need and how high you want your deductible. In choosing our five top companies for general liability insurance, we had to go by reputation, customer satisfaction, and types of coverage offered.

How much does general liability insurance for contractors cost?

According to insureon, the median cost of general liability insurance for general contractors is about $90 a month. However, it varies quite a bit according to things like:

- Policy limits

- Deductible

- Level of risk

- Size of the projects you typically do

It should come as no surprise that roofers pay the most for general liability insurance, averaging $3,590 a year. Locksmiths pay the least, at about $406 a year.

Another factor that will affect what you pay is your claims history. If you’ve ever filed a claim in the past, your rates will be higher than someone with a clean history.

How can contractors get cheap general liability insurance?

There’re a few things you can do to try to lower your costs.

- Shop around. Even if you have a general liability insurance policy already, you should review it every 2-3 years and see if someone can give you a lower rate. Companies often give lower rates to new customers and then raise them over time.

- Bundle your policies. The odds are, if you’re a general contractor, that you also need workers comp insurance, professional liability insurance, E&O insurance…the list goes on. Getting all of your policies from the same company should earn you a discount.

- Raise your deductible. Usually, the default deductible on a general liability quote is $500. If you raise it to $1,000 or more, you’ll save money on premiums. Just make sure you have enough money set aside just in case.

- Only get as big a policy as you need. If you’re barely scraping by, you don’t need $2 million in liability insurance. Be realistic. If you have no idea how much insurance you need, that might be a good time to talk to an agent.

- Manage risks. These days, there are many software programs that will point out areas where you could improve your risk and increase workflow. Just a few are Salus Pro, SiteDocs, and TradeTapp.

>>MORE: Cheapest General Liability Insurance for General Contractors

Does contractors need professional liability insurance?

If contractors want to get one business insurance policy only, that should be general liability policy. If they want to get another layer of protection for their contracting work, they may want to consider contractors professional liability insurance. This coverage protects them when their clients sue them believing that they make mistakes or omissions in their work and that causes their clients damages or financial loss. For example, if a building doesn’t stand well in a storm and rain penetrates into a wall causing damages to the building and the client believes that this was caused due to an error in your structural design of the building. They will use the architect and/or the construction contractors. This is out of the coverage of the general liability insurance policy. Contractors professional liability insurance policy or endorsement will cover and pay for this lawsuit.

Learn more about this and how and where to get the best contractors professional liability insurance companies.

Last thoughts

Although no one enjoys shopping for insurance policies, it’s worth getting general liability insurance if you’re a contractor. Some states require it for contractors, and some clients insist on it. Plus, it protects you from lawsuits. Don’t put it off.