Your friend is getting married. He’s booked a lovely venue for the reception. You did some bartending back in college, so when he asks you to be the bartender at his wedding, you enthusiastically say yes.

But not so fast. Being an independent and private bartender—that is, one not attached to a restaurant or bar—carries some responsibilities with it that you’ll need to be aware of. If you serve someone one drink too many and then they injure someone in an accident on the way home, could you be held liable? That’s where bartender insurance comes in.

- Best 3 Providers of Bartender Insurance

- What is Bartender Insurance?

- What does Bartender Insurance Cover?

- Bartender Insurance for Wedding: What do you need to know?

- How Much does Bartender Insurance Cost?

Best 3 Providers of Bartender Insurance

The first rule of thumb is always comparing quotes from a few companies. Digital commercial insurance brokers like CoverWallet or Simply Business make it easy for us to compare quotes from leading companies.

- Food Liquor Liability Program (FLIP): Best for Bartenders Who Need General Liability and Liquor Liability Policies

- Coverwallet – Best for Mobile Bartenders with Repeat Business and Comparing Quotes

- AP Intego: Best for Comparing Quotes by Agents

1. Food Liquor Liability Program (FLIP) – Best for Bartenders Who Need General Liability and Liquor Liability Policies

FLIP specializes in providing insurance to those in the food and beverage industry. They offer estimates on what you’ll pay for a policy before you enter any information. Prices vary quite a bit by state (states with stricter laws have higher insurance rates).

If you’re searching for a one-day policy for a mobile bartending business, almost every website referred us back to FLIP.

Also, if you live in any of the following states, FLIP won’t be able to insure you: AL, VT, DC, AK. HI. IA, KY, NH, PA, or WV.

2. Coverwallet – Best for Mobile Bartenders with Repeat Business and Comparing Quotes

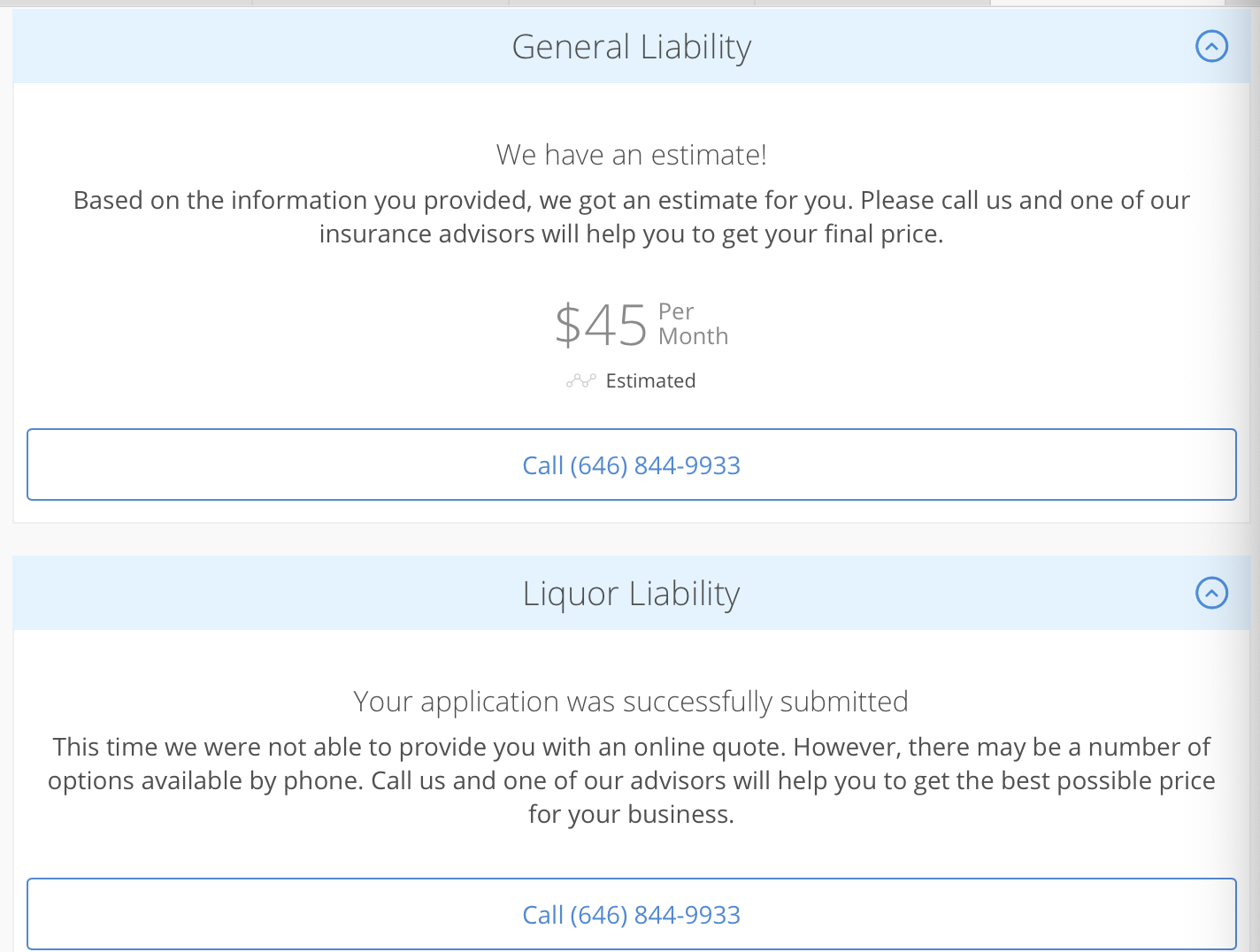

Coverwallet works with insurance companies to provide you with the best quotes possible. They wouldn’t give us a quote for a one-day bartender, but if you’re a mobile bartender who frequently serves alcohol at weddings and corporate events, Coverwallet can offer you a general liability policy for about $45 a month. However, for the liquor liability insurance, they gave us a message telling us to call.

3. AP Intego: Best for Comparing Quotes by Agents

AP Intego will take your information and search for insurance providers for you. If they find any that will offer you liquor liability coverage, they will email you.

Bars and restaurants will find this helpful. They might find you insurance if you’re a mobile bartender, depending on the state you live in.

What is Bartender Insurance?

Technically, there isn’t a specific bartender insurance. If you work at a restaurant or in a club, their insurance should cover you in case of injuries or property damage. However, if you are a mobile or private bartender, you’ll want to look into liquor liability insurance and general liability insurance as well.

What does Bartender Insurance Cover?

There are two types of insurance you should consider—liquor liability insurance and general liability insurance. If you only go with one, it should be liquor liability insurance.

Liquor liability insurance covers:

- Legal fees

- Settlements

- Medical costs

- Injuries caused by intoxicated patrons

General liability covers:

- Third-party injury

- Third-party property damage

- Advertising injury

Laws vary quite a bit from state to state. However, as a general rule, liquor liability should fall on the hosts of an event or the people providing the alcohol. In other words, for that wedding you said you would bartend for, it’s probably the hosts responsibility to get special event insurance.

Below are the three circumstances you would need liquor liability coverage:

- You are in the business of selling and distributing alcohol

- You are the host and are providing alcohol to your guests. In this case, you would need host liquor liability insurance which is a bit different from the liquor liability insurance.

- You are bartending at a special event where liquor in not sold, such as a wedding, but a liquor license is required

Sometimes a venue will require a mobile bartender to have insurance. Again, laws vary considerably from state to state, so be sure to investigate the laws in the state where you’ll be serving.

However, bartenders have been sued before and even been held liable for over-serving someone, depending on state laws. In many states, something called Dram Shop laws hold a bartender legally responsible if they serve someone too much alcohol. Other states don’t allow these lawsuits because they feel the drinking person should have known better. Check with the laws of the state you’ll be serving in.

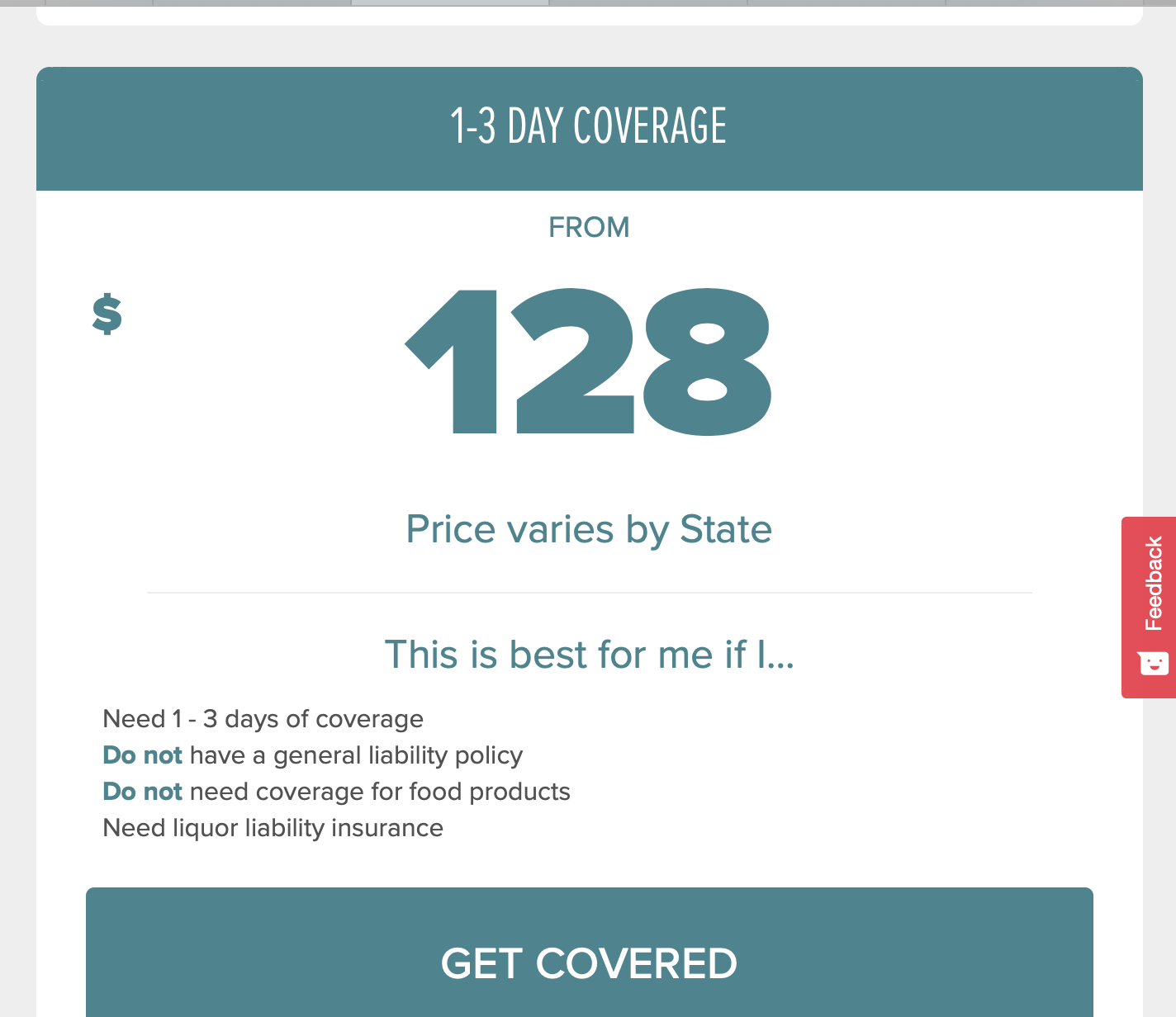

If you do decide to purchase your own insurance, you can get a one-to-three day policy that will cover you in the event someone requires it.

What doesn’t Bartender Insurance Cover?

Liquor liability insurance laws vary, but generally liquor liability won’t cover:

- Any event where the insured is promoting or sponsoring any entertainment

- Any risk that allows consumption of alcohol by employees during hours of employment

- Any event that goes past 2:00 a.m.

- Any event that allows or encourages drinking games, drink incentives, all-you-can-drink specials, complimentary drinks, BYOB service or self-service.

- Underage drinking (if you knowingly serve someone underage)

>>MORE: Liquor Liability Insurance: Coverage, Cost, and the Best 4 Providers:

Bartender Insurance for Wedding: What do you need to know?

If you are a private bartender and invited to bartend for a wedding. Even it is the wedding of your best friend or a family member and it is just one-day event, be sure to get a bartender insurance policy, which should combine both general liability and liquor liability. If you want to get one policy only to save money, you definitely need to get a liquor liability insurance policy.

However, since it is just a one-day event, you can simply ask for a one-day bartender insurance policy, which will be cheaper. It usually comes in 1-3 day policy.

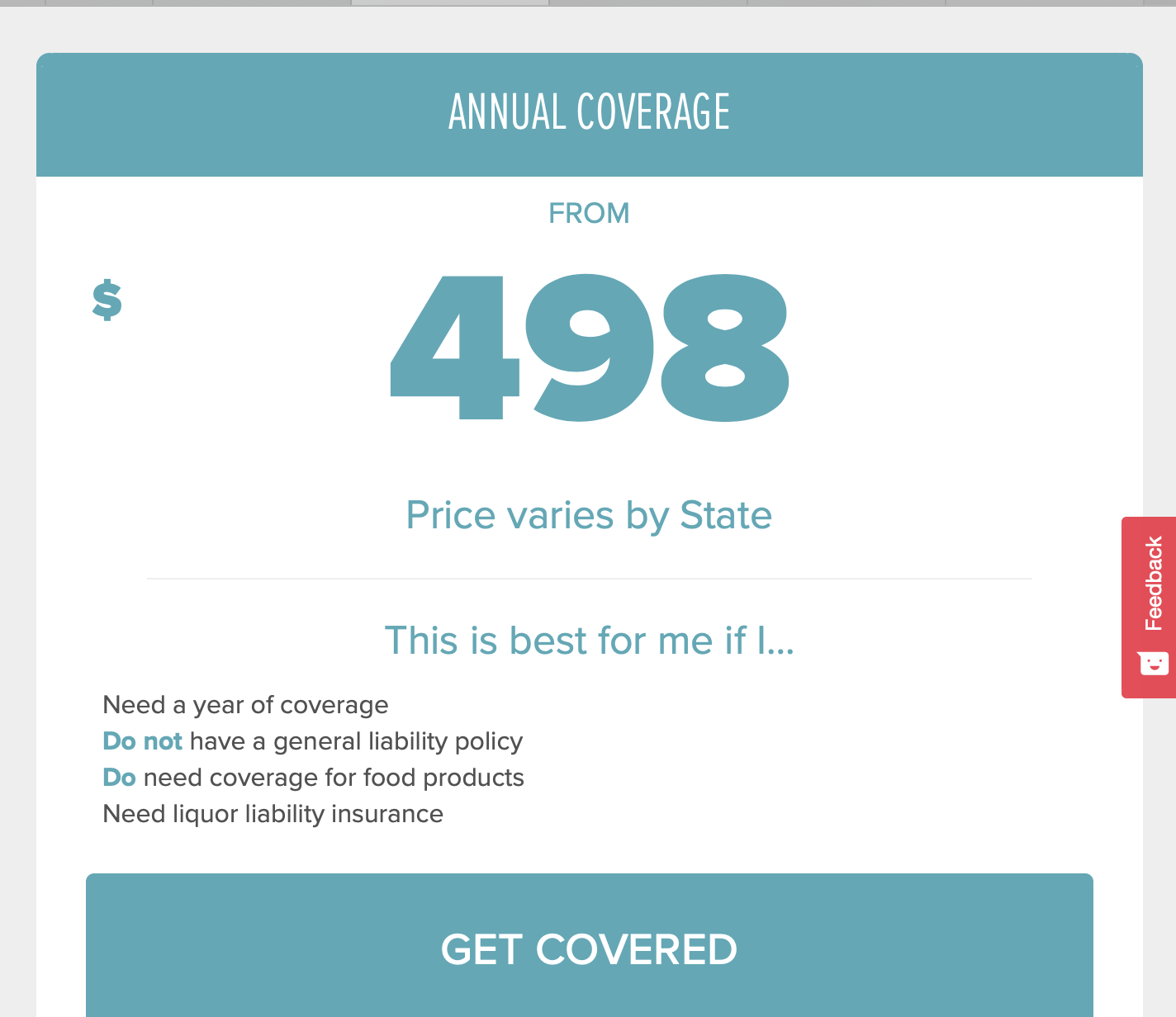

How Much does Bartender Insurance Cost?

According to FLIP (Food Liability Insurance Program) you can buy a one-to-three day event liquor liability insurance policy for about $99, or, if you bartend for events all the time, you can purchase a combination of liquor liability and general liability for about $299 annually.

As always, comparing quotes from several companies will help you find the cheapest one for your situation. Commercial insurance brokers like CoverWallet and Simply Business make it easier for you to compare several quotes in one place.

What Benefits Should You Consider Before You Purchase Bartender Insurance?

You’ll want to determine how much liability you want. Coverage limits range for $100,000 per occurrence with a $300,000 aggregate to a $1 million dollar policy with a $2 million dollar aggregate.

What can I Do To Limit My Risk?

Besides having liquor liability insurance, you can do some things to limit your risks, such as:

- Identify designated drivers at the event

- Provide water and non-alcoholic beverages

- Offer to call an Uber or a Lyft for any patron who appears intoxicated

- Be prepared to stop serving anyone who appears noticeably drunk

Final Thoughts

If you’re a mobile and private bartender, you’ll need some insurance. You can get a general liability policy almost anywhere, but a liquor liability policy that will cover bartending is harder to find. Make sure you familiarize yourself with the laws in your state, as they vary quite a bit. However, bartenders have been held liable for over-serving customers, so make sure you’re protected.