If you run a restaurant, or are thinking of starting a restaurant business, liability is an issue you’re going to have to face, so you should look into restaurant insurance. A lot can go wrong while running a restaurant: an employee could burn themselves while using a deep fryer, a patron could slip on a wet floor or one of your foods could trigger an allergy attack in a customer. All of these situations could result in a lawsuit or needing to pay worker’s compensation benefits. So below we’ll look at restaurant insurance so you can remain protected when accidents and mistakes happen. We’ll cover what restaurant insurance is, how much it costs and where you can find it.

- The 6 best providers of restaurant insurance

- What insurance does a restaurant need?

- How much does restaurant insurance cost?

- How much does insurance cost per month for a typical restaurant?

- Compare restaurant insurance quotes

- Workers compensation insurance for restaurants

The 6 Best Providers of Restaurant Insurance

Insurance for restaurants is quite popular, so many, if not all, insurance companies have products available for restaurant owners. Here are the top 6 insurance providers to restaurants:

- Simply Business: Best for finding cheap coverage

- CoverWallet: Best for Comparing Online Quotes

- The Hartford: Best for comprehensive coverage from a top carrier

- NEXT: Best for a great digital experience and competitive rates

- Smart Financial: Best for experienced agents

- InsurePro: Best for short-term restaurant insurance

Simply Business: Best for finding cheap coverage

In less than 10 minutes, Simply Business’s online form enables restaurants of all sizes to get coverage options and rates from 20+ insurance providers. Simply Business specializes in partnering with carriers offering low-cost coverage so that they can help small businesses, and restaurants, find the cheapest coverage available.

Their website is an attractive option for people who like to compare rates side-by-side or who are uncertain about the sort of coverage they should have.

Pros

- Good option to compare and find low-cost coverage

- User-friendly platform

- Quotes generation takes about 10 minutes

- Partners with prominent insurance carriers

- Abundance of industry-specific information

Cons

- Customer support hotline hours are restricted and vary regularly

- Sometimes quotes are not available online, especially for restaurants with unique or high-risk operations

CoverWallet: Best for Comparing Online Quotes

CoverWallet is a digital commercial insurance broker. They work with several business insurance companies and are able to provide quotes of these companies for consumers to compare and choose. They provide business insurance quotes for a wide range of industries. Restaurants or food catering is one of the industries they cover.

If you are new to buying restaurant insurance, you should give them a call and discuss your specific restaurant situation with their agents, who are very knowledgeable about business insurance in general.

CoverWallet also offers 4 different packages of restaurant insurance that you can choose from: Basic, Standard, Pro, and Custom. The basic restaurant insurance policy costs $39/month and includes general liability insurance only. The pro restaurant insurance policy costs $189/month and includes general liability, commercial property, and Employment Practices Liability Insurance (or EPLI).

Pros

- Quotes, purchases, and policy management are made online

- You can monitor your policy online

- Guide to business insurance available

Cons

- It may take some time to produce a quote

- You can get quotes from carriers on their platform only

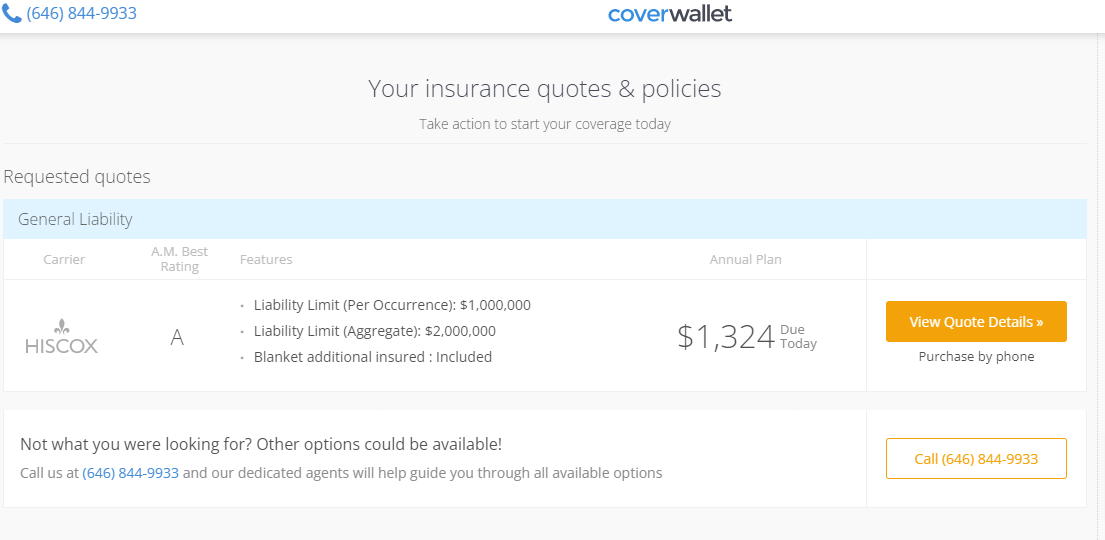

This is a sample quote generated from CoverWallet for restaurant general liability insurance.

The Hartford: Best for comprehensive coverage from a top carrier

As a major player in the business insurance world, this company has a page detailing what type of insurance you’d want for a restaurant business. It recommends getting a business owners policy, which can include general liability, commercial property, and business income. However, the online quote system does not reflect this bundled option. When we selected property, general liability, and worker’s compensation together, we got the following quote screen:

NEXT: Best for a great digital experience and competitive rates

NEXT is an insurtech firm that offers restaurant insurance. The company offers different policies, including general liability, commercial property, and other policies, depending on their location and company. Customers may save money by purchasing several insurance policies from NEXT. It also offers fast insurance coverage through its mobile app. Their rates, especially for general liability insurance, tend to be competitive and affordable.

Pros

- You can get insurance in less than 5 minutes,

- You can get an insurance certificate online

- Online insurance prices, coverage, and management

- Online live assistance

- Competitive and affordable rates

Cons

- NEXT does not cover restaurant in all states yet

- Quotes for other coverages may not be available online

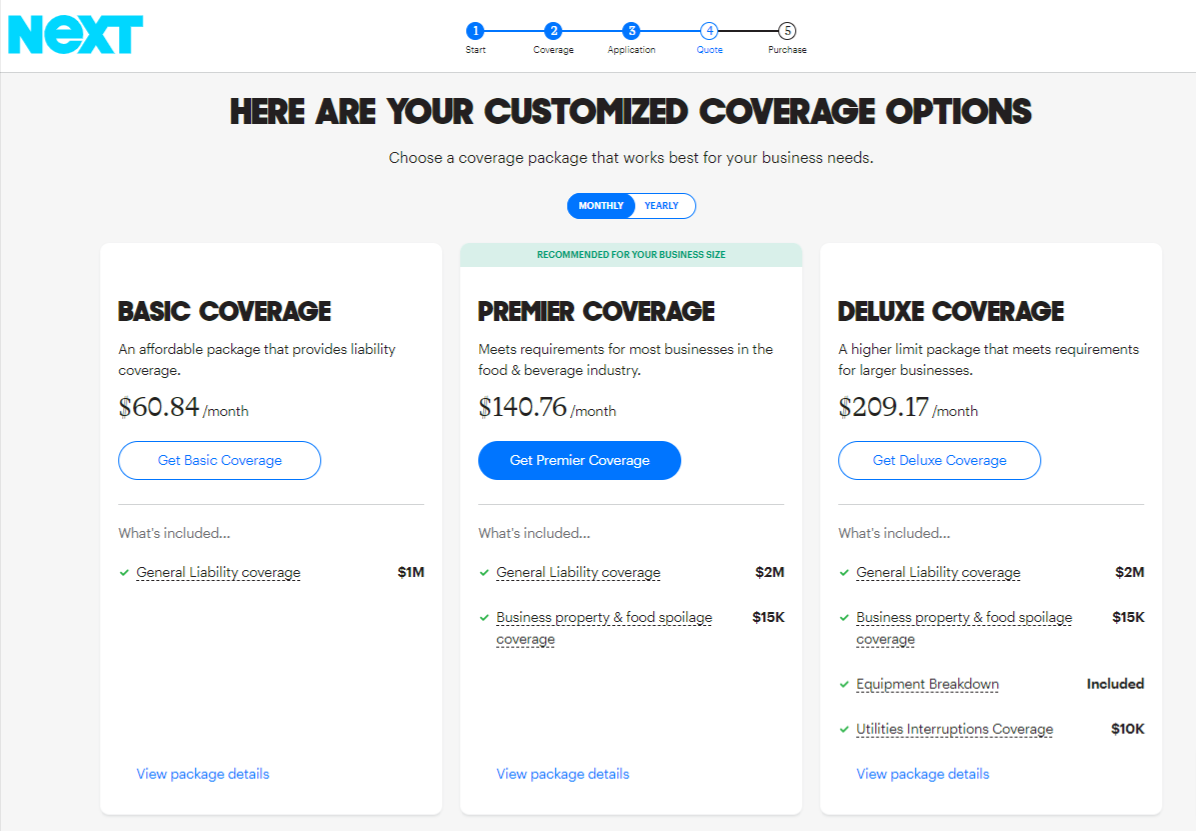

This is a sample quote generated from Next insurance for restaurant liability insurance.

Smart Financial: Best for experienced agents

Restaurant insurance is actually quite complicated with different types of coverage and each coverage may have several nuances for different types of restaurants, different restaurant classes with different food types, alcohol, and services such as valet parking, etc. It is often advisable that restaurant owners should work with an experienced agent to help identify the right coverage and find the best rates.

If you prefer working with an experienced agent, you may want to consider Smart Financial. They are a brokerage firm with hundreds of experienced agents. They will match you with the most knowledgeable agent in their network in your restaurant niche.

Pros:

- Experienced and knowledgeable agents who have decades of experience working with restaurants of all sizes and in all operational niches

- Partner with 30+ carriers so that their agents can help you compare several quotes to find the cheapest one

- Customer service available 24/7

Cons:

- Limited digital capabilities

- You have to work with an agent. If you prefer doing everything online, this may not for you

InsurePro: Best for short-term restaurant insurance

InsurePro is an insurance broker specializing in serving small and micro businesses. Their unique product is on-demand short-term general liability insurance, which can provide coverage for small businesses for just one day, or a few days, or a few weeks. If small businesses don’t need a traditional permanent and long-term insurance policy, this is a great option for them to save money on their coverage.

Pros

- On-demand short-term liability coverage for just one day or a few days

- Compare different prices beginning at $10/month.

- Coverage starts within 24 hours

- Getting quotes online takes a few minutes

Cons

- Some policies are state-specific

- Claims must be filed directly with the provider.

>>MORE: Best Business Insurance for Bars

What is restaurant insurance?

Restaurant insurance is a catch-all phrase that includes the types of insurance that restaurants typically need in order to remain protected from claims and lawsuits. When running a restaurant, you typically need a full range of coverage, from protecting against lawsuits if someone slips on your floor to covering the wait staff in case of a workplace injury or if someone sues you for having over sold alcohol for customers who cause accidents after leaving your restaurants.

What Insurance Does a Restaurant Need?

As mentioned above, restaurants would need several insurance coverages to protect operations and business. The Insurance Information Institute lists several types of insurance that a restaurant should consider:

- Commercial property insurance

- General liability insurance

- Liquor liability insurance

- Commercial auto insurance

- Workers compensation insurance

- Employment practices liability insurance

- Business Owners Policy (or BOP)

Commercial property insurance

Commercial property insurance protects your tools and equipment from loss to fire, explosions, burst pipes, vandalism, storms, and theft. Earthquakes and floods aren’t usually covered, but if you live in an area prone to floods or earthquakes, you can add them to your policy.

For restaurant owners, whether you rent or own your restaurant space, you definitely need this insurance policy to protect your physical space and the equipment stored in it.

>>MORE: Best Commercial Property Insurance Companies

General liability insurance

General liability insurance will cover you if a client slips and falls and injures themselves in your shop. It covers third party bodily injury and property damage, plus advertising injury.

For example, if your client slips and falls in your restaurants, they are injured and have to be hospitalized for some time and decide to sue you, a general liability insurance policy will pay for their medical bills and lost wages as a result of the injury. This is actually one of the most common lawsuits against small businesses, especially among restaurants.

You can also add liquor liability endorsement to your general liability insurance policy to cover your liabilities if you serve alcohol to someone who already has had too much and that person ends up in an accident after leaving your restaurant.

However, if your restaurant is a fine dining one, with a lot of liquor consumption, you may want to consider a separate liquor liability insurance policy. (see more below)

>>MORE: Best General Liability Insurance Companies

Liquor liability insurance

Liquor liability insurance: If your restaurant serves alcohol, you will need to obtain liquor insurance as well. Liquor liability insurance is defined as coverage for bodily injury or property damage that an intoxicated person causes after being served alcohol by a policy holder. The coverage on a liquor liability policy varies quite a bit from state to state because each state interprets who is legally liable for damages or injuries differently.

In many states, liquor liability insurance is required when you apply for a liquor license, so make sure to obtain it before applying for a liquor license.

Commercial auto insurance

If you use a vehicle for work, including delivering food to your customers or getting groceries from supermarkets to your restaurant, you will need a commercial auto insurance policy. It is legally required in all 50 states

Your personal auto insurance policy doesn’t cover you if you drive your vehicle for work. The personal auto insurance company will refuse your claims. Even worse, they might drop you off altogether when they find out. Commercial auto insurance is usually a bit more expensive than personal auto policy. However, it is not worth it skipping it.

>>MORE: Best Commercial Auto Insurance Companies

Workers compensation insurance

If you have employees, workers’ compensation insurance is a must since it is legally required. This will cover the costs of employees work-related injuries or illnesses, including medical cost and lost wages. If you are running your restaurants by yourself and/or your family members, you are a self-employed independent contractor, you still need workers comp insurance coverage to protect yourself (and your family members) when you get injured at work.

Working in a restaurants is actually one of the most risky jobs, especially for those who work in the kitchen. The likelihood of getting injured in a commercial kitchen is relatively high. Make sure you have workers comp insurance coverage to protect yourself and your employees.

Even more importantly, with COVID, your waiters and waitresses are now at risk to contracting COVID from your customers. Although more and more restaurants require vaccination proof from customers for entry, the risk is still there.

Having workers comp insurance will also make it easier for you to hire employees. Your employees will feel safe and protected. Most restaurants are short of staff due to COVID. Potential employees wouldn’t even consider you if you don’t provide workers comp insurance coverage for them.

Here are the best workers comp insurance companies for restaurants.

>>MORE: Best Workers Comp Insurance Companies

Employment Practices Liability Insurance (EPLI)

This is to protect restaurant owners from claims and law suits of claims of harassment, discrimination, wrongful termination, and wage discrimination.

You will be surprised to learn that harassment and wage discrimination is the second most popular lawsuits among restaurants. Protect yourself and your restaurant business to obtain EPLI coverage. Learn more at the best employment practices liability insurance (EPLI) companies.

Business Owners Policy (BOP)

Some of these policies can be combined into a convenient business owners policy (BOP), which often bundles property, general liability coverage, and business (income) interruption insurance. If your restaurant generates less than $10M in annual revenue and/or employ less than 100 people, which most restaurants do, you might want to consider a BOP policy, instead of three separate policies: general liability, commercial property, and business income interruption.

However, if your restaurant generates more than $10M in annual revenue or employs more than 100 people, you are not eligible for BOP policy. You need to get three separate policies.

BOP makes it simple and more cost efficient for you to get coverage to protect your restaurant business.

Garage keepers insurance

Restaurants may need garage keepers insurance if they offer valet parking services or if they have a parking lot for customers to use. This type of insurance provides coverage for damage to vehicles that are parked on the restaurant’s property, including those that are being valet parked.

Garage keepers insurance can protect the restaurant from financial loss in case of damage or theft of vehicles that are in their care, custody, or control. It can also protect against third-party claims for loss or damage to vehicles, which is important for the restaurant’s reputation. Without this coverage, a restaurant could be held liable for any damages that occur to a vehicle while it is on their property.

Some of the specific risks that garage keepers insurance can protect against include fire, theft, vandalism, and collisions. It can also provide coverage for the cost of defending against a lawsuit if a customer or other third party files a claim against the restaurant for damages of their vehicles while parking at the restaurant’s parking lot.

What is restaurant liability insurance?

Restaurant liability insurance is a comprehensive insurance policy that protects a restaurant from financial losses caused by general third-party claims of bodily injury or property damage. It is also known as comprehensive general liability insurance, which includes other liability coverage such as product liability and liquor liability in a general liability insurance policy:

Some of the things that restaurant liability insurance typically covers include:

- Slip and fall accidents: If a customer slips and falls in your restaurant, this insurance can help cover the costs of their medical bills and other expenses.

- Food poisoning: If a customer becomes ill from food served at your restaurant, this insurance can help cover the costs of their medical treatment and any legal expenses.

- Property damage: If a customer damages property while in your restaurant, this insurance can help cover the costs of repairs.

- Advertising injury: If your restaurant is accused of infringing on a third party’s trademark, copyright or other intellectual property rights, this insurance can help cover the cost of any legal action.

- Medical payments: If a customer is injured while in your restaurant, this insurance can help cover the costs of their medical treatment, regardless of who is at fault.

- Liquor liability is typically included as part of a restaurant liability insurance policy, but it can also be purchased as a separate coverage.

- Liquor liability insurance is designed to protect a restaurant from financial losses that may occur as a result of customers becoming injured or causing damage while under the influence of alcohol served at the restaurant. It covers claims resulting from “dram shop” laws which hold servers, sellers, or providers of alcohol liable for injuries or damages caused by an intoxicated person.

- This type of insurance can help cover the costs of legal expenses, medical bills, and other expenses related to injuries or damages caused by a customer who has consumed alcohol at your restaurant. It’s particularly important for restaurants, bars, and other establishments that serve alcohol as they may face unique legal liabilities.

- It’s worth noting that some states have specific laws regarding liquor liability insurance and may require certain types of coverage for licensed establishments that serve alcohol. Therefore, it’s important to check the laws in your state and consult with a professional insurance agent or broker to ensure that you have the right coverage to meet your needs and comply with state regulations.

It’s important to note that restaurant liability insurance typically does not cover all types of risks, such as worker’s compensation, employee dishonesty, or loss of income due to a closure. For those types of risks, other specific insurance policies such as worker’s compensation, crime insurance, and business interruption insurance are usually required.

Who needs restaurant insurance?

Many types of food-serving businesses need some types of restaurant insurance. Below are a few of them:

- Casual restaurants

- Fast food restaurants

- Diners

- Fine dining

- Bars – learn more about bar insurance in one of our articles

- Pubs

- Cafes

- Food delivery services

- Catering services – learn more about catering insurance in one of our articles

- Coffee shops

- Juice bars

- Ice cream shops

- Bakeries

- Pizzerias

How Much Does Restaurant Insurance Cost?

Tabak Insurance Agency, with specializes in the food industry, averages a business owners policy, worker’s compensation, and liquor liability insurance at $4,300 annually. Though the agency states that restaurant insurance costs for a business owners policy (BOP) can range widely from $1,100 to $10,500 annually.

Many factors can affect how expensive restaurant insurance is, like the size of your business, how many employees you have, whether you sell liquor and the location of your business, to name a few conditions.

Learn more at how much restaurant insurance costs

How Much Does Restaurant Insurance Cost Per Month?

On average, a typical small restaurant with about $1 million in annual revenue would pay about $600 in restaurant insurance a month, or $7,200 a year, all necessary policies included.

- General liability insurance costs $69 a month

- Food contamination insurance costs $49 a month

- Commercial property insurance costs $139 a month

- Liquor liability insurance costs $89 a month

- Commercial auto insurance costs $215 a month

- Workers compensation insurance costs $75 a month (with 4 full-time employees)

Each restaurant is unique with its own features. Each restaurant will also have different quotes from different insurance companies. The only way to get the best quote is to shop around with 3-5 companies and compare their quotes. Working with a digital broker like CoverWallet or Simply Business is a good way to compare quotes from several leading companies in one place.

What is a restaurant insurance quotes and where to get them?

A restaurant insurance quote is an estimate of the cost of an insurance policy for a restaurant. The quote is typically based on factors such as the size and location of the restaurant, the type of cuisine served, and the number of employees. To get a quote, you can contact an insurance agent or broker who specializes in insuring restaurants, or you can use an online insurance comparison tool to get quotes from multiple insurance companies.

Pros and cons of getting restaurant insurance quotes from brokerage firms

There are pros and cons of getting restaurant insurance quotes from brokerage firms or carriers. In general, we believe restaurant owners should work with a good brokerage firm to get the right insurance quotes for their restaurants at the cheapest rates:

Pros:

- Expertise: Brokerage firms specialize in insuring restaurants and have a deep understanding of the specific risks and exposures that restaurants face. They can provide tailored coverage options that meet the unique needs of your restaurant.

- Access to multiple insurance companies: Brokerage firms work with multiple insurance companies, which gives you more options to choose from and increases the chances of finding a policy that meets your needs and budget.

- Personalized service: Brokerage firms provide personal service and can help you navigate the complex process of buying insurance. They can answer your questions, explain different coverage options, and help you find the right policy for your restaurant.

Cons:

- Dependence on the broker: You need to be aware of your broker’s expertise, reputation, and track record. Not all brokers are created equal.

- Carrier preference limitation: If you prefer a specific carrier that the brokerage firm doesn’t work with, you need to look elsewhere.

Overall, getting a restaurant insurance quote from a brokerage firm can be a good option for restaurants looking for personalized service and access to multiple insurance companies. However, it’s important to compare quotes from multiple sources, including direct from insurance companies, to ensure that you are getting the best coverage at the best price.

Compare restaurant insurance quotes

In order to try to compare restaurant insurance quotes online, we put in a business owners policy through CoverWallet, since many insurers recommend this as an option for restaurants. We entered a full-service restaurant with three part-time employees that’s three years old. We got the following screen with one quote:

Restaurant Insurance in New Jersey

Restaurant owners in New Jersey need to obtain sufficient business insurance coverage to protect their restaurant business operations. In addition to the standard restaurant coverage such as workers comp, general liability insurance, and commercial auto insurance, restaurant owners in New Jersey will need to have liquor liability insurance. New Jersey is popular with its dram shop laws, which holds restaurant owners liable for serving alcohol to minors and for harm caused by the individuals that have been over-served by the restaurants even after they have left the restaurants.

Restaurant owners in New Jersey may also need to consider hurricane and flood insurance. They can obtain these coverages separately or add the coverage as endorsements to their commercial property policy.

Restaurant Insurance in New York

A restaurant in New York state should have the same set of business insurance policies as in other states. However, it is likely to be a lot more expensive in New York than in other states, especially for commercial property, liquor liability, and commercial auto insurance. New York state is in the top 3 most expensive states for these insurance policies.

Don’t skip restaurant insurance because it is expensive. It is a lot costlier without restaurant insurance in New York when bad luck happens. Make sure you shop around, compare quotes with digital brokers like CoverWallet and Simply Business to get the best quote for your restaurant.

Final Thoughts

- Restaurant insurance is an umbrella term that covers the different types of insurance a restaurant business should carry. These typically include general liability insurance, property insurance, professional liability insurance, worker’s compensation and commercial auto insurance.

- The cost can vary depending on how much coverage you want, benefits like limits and the size of your business, as a few examples. It typically ranges all around the thousands of dollars annually.

- Some of the top five companies to look into include Next Insurance, The Hartford, Nationwide, Farmer’s and Liberty Mutual.

- CoverWallet is a good source for restaurant insurance quotes, since it allows you to pick insurance types by industry recommendations.