Bars and restaurants are places where people come to celebrate, socialize, and enjoy great food and drinks. But owning and operating a bar and/or a restaurant where alcohol is served can be a headache due to the risk of lawsuits. You need to protect yourself, your livelihood, and your employees with the best bar insurance you can find.

- The 4 best bar insurance companies

- What type of insurance does a bar/restaurant need?

- How much does restaurant/tavern/bar insurance cost?

- Five most common bar insurance claims

- Insurance for sports bars

- Insurance for nightclubs

- Insurance for juice bars

The 4 best bar insurance companies

We research more than 10 companies offering insurance for bars, nightclubs, and restaurants. Here are our recommendations of the 4 best providers.

- CoverWallet: Best for comparing online quotes

- Huckleberry: Best for a completely digital experience

- RMS Hospitality Group: Best for specializing in bar and nightclub insurance

- Next Insurance: Best for customized bar insurance policy

CoverWallet: Best for comparing online quotes

CoverWallet is a digital broker. They work with several leading business insurance providers. If you want to compare several quotes in one place to select the best and cheapest one for your company, you may want to start with CoverWallet.

After providing your company’s information, within minutes, CoverWallet will provide with several quotes in one place making it convenient for you to compare and select the best one for you.

CoverWallet focuses on making buying and managing business insurance policies easy and convenient for you. After buying a policy through CoverWallet, you will get access to their digital dashboard to manage all of your business insurance policies that you may buy from different providers in one place.

CoverWallet is now a part of Aon, one of the biggest insurance brokers in the world. Aon has an excellent financial strength (A) by AM Best. CoverWallet also earns the customer satisfaction rating of A by BBB.

Huckleberry: Best for a completely digital experience

Huckleberry is relatively new, founded in 2017, but they’re backed by insurance giants such as Chubb, Markel, and The Hartford. They are 100% online—you can get a quote, pay online and you’re done. They offer many types of business insurance, some of which may be of particular interest to bar owners:

- General liability

- Business interruption

- Commercial property

- Employment practices liability

- Restaurant endorsement

- Liquor liability

- Equipment breakdown

- Spoilage coverage

- Employee dishonesty coverage

Huckleberry could give us a quote, but only for workers compensation insurance policy. They said that that would contact us for other policies.

RMS Hospitality Group: Best for specializing in bar and nightclub insurance

RMS Hospitality Group specializes in bar, nightclub, and restaurant coverage. They offer:

- General liability

- Liquor liability

- Product liability insurance

- Products and completed operations

- Assault and battery

- Excess liability

They have over 20 years experience, and can make recommendations to increase the safety of your establishment, so you’ll be less subject to lawsuits. To get a quote, you can call them and speak to an insurance broker.

>>MORE: Restaurant Insurance: Cost and Best Companies

Next Insurance: Best for customized bar insurance policy

Next is one of the more popular insuretech startups. They modernize business insurance by providing a fully digital experience from getting quotes, buying a policy, and managing policies.

Next offers a customized policy for bars, nightclubs, and restaurants. Instead of getting different policies covering different aspects of operating a bar or a nightclub, a bar insurance from Next will cover several risks involving in running a bar, a nightclub, or a restaurant.

What type of insurance does a bar/restaurant need?

A bar/restaurant is a small business. You’ll need small business insurance, like:

General liability insurance: this coverage protects you against third-party bodily injury and third- party property damage. If a customer trips into a table and breaks a wrist, general liability will cover you. Restaurants and bars can be hazardous places, with spilled drinks and slippery floors leading to customer injuries.

General liability should also cover you if a customer gets food poisoning from having eaten something at your restaurant.

Many general liability policies exclude patrons who are intoxicated, which is why you’ll need liquor liability insurance.

Liquor liability insurance: If a patron has been drinking and then injures themselves or someone else, liquor liability insurance will protect you. Alcohol makes people less coordinated than usual, and if your establishment offers dancing or riding mechanical bulls, there is plenty of potential for injuries.

>>MORE: Liquor Liability Insurance: Cost and Best Providers

Commercial property insurance: Restaurants and bars often have expensive, professional equipment. Commercial property insurance will also cover the bar or restaurant itself, which is good because any restaurant with a kitchen could potentially catch fire. If you don’t own the building where the restaurant is, the owner could sue you for damages. If you have commercial property insurance, you should be covered.

Business Owners policy: You could combine general liability insurance and commercial property insurance and get a business owners policy or BOP.

Workers Compensation: Unless you’re running this restaurant/bar by yourself, you’ll probably need workers compensation insurance. Most states require it if you have four or more employees, and some require it if you have even one employee. Workers compensation protects you and your employees if one of them gets injured on the job. If one of your bouncers try to eject an unruly customer and then the bouncer gets punched in the face, workers compensation will cover the cost of his wages while he recovers.

Assault and Battery coverage: If several patrons get into a bar fight, assault and battery coverage will cover you if one or both of them holds the bar responsible. A bar that serves patrons past the point of intoxication could be held liable for sustained injuries. This will also cover you if a bouncer accidentally injures a customer when stopping a fight. This type of coverage can also protect you from sexual harassment claims.

You might also consider cyber liability and employment practices liability insurance.

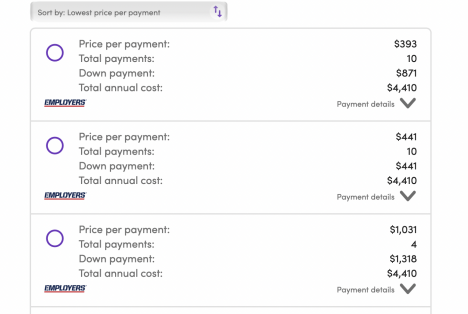

How much does bar insurance cost ?

Bar insurance cost is similar to restaurant or tavern insurance cost. It depends. There are so many variations of what makes up a bar, a restaurant, or a tavern. You could have a huge, multi-floor nightclub featuring dancing and live bands, or you could have a small, mom-and-pop diner that’s only open for breakfast. There are other factors that affect how much you’ll pay as well:

- What type of bar/restaurant you own

- Location

- How many years of experience you have

- Annual sales and revenue

- Claims history

- Live entertainment

- Number of customers

- Type of building

- Coverage limits

The average cost of restaurant/bar insurance is between $3,000 and $8,000 a year, depending on your business.

Be sure to shop around with a few insurance companies or a digital broker like CoverWallet to compare several quotes to select the cheapest one for your company.

Five most common bar insurance claims

There are so many moving parts to running a bar, but statistically, these are the most common claims:

- Fire damage

- Customer or employee injuries

- Spoiled food

- Theft

- Credit card fraud

Basically, the lesson here is that restaurant and bar insurance is complex and is highly dependent on what type of bar/restaurant you own.

Insurance for sports bars

Sports bars feature a convivial atmosphere as everyone roots for their favorite team on one of the many large screen TV’s. Burgers and brews flow freely. Sports bar don’t have to contend with dancing or live music, but they do have to be on the alert for bar fights among members of opposing teams. As such, you’ll want at least these types of policies:

- General liability insurance

- Liquor liability insurance

- Assault and battery

- Property insurance (or a business owners policy)

- Workers’ compensation

Get quotes from at least three companies, but be aware you may need to call. In addition to CoverWallet and Huckleberry, RMS Hospitality Group and Next offer specialty insurance for sports bars and other types of restaurants.

Insurance for nightclubs

Pulsating music, flashing lights and a crowded dance floor come to mind when you think of nightclubs. Unfortunately, dance floors tend to be both crowded and filled with drunk people, which is a recipe for injury. In addition, nightclubs frequently have live music, a cover charge and bouncers/security at the door. You will need:

- General liability

- Liquor liability

- Assault and battery

- Bouncer liability

- Event liability

- Workers compensation

In addition, there is nightclub coverage, which gives you additional protection against liabilities that are specific to nightclubs. They can be a combination of commercial property insurance, liquor liability, food contamination coverage, equipment breakdown coverage, and product liability coverage (in case someone claims they got food poisoning from you).

Restaurant and bar insurance

Restaurants don’t usually have live music or bouncers, but they do prepare food in kitchens. Kitchens can and do catch fire, so you’ll need to protect yourself with commercial property insurance. If you lease your space and your establishment causes a fire, the owner of the building could sue you for damages. You will also need:

- General liability

- Workers’ compensation

- Product liability insurance

- Assault and battery

- Business interruption

- Cyber security

When purchasing business interruption insurance, read the fine print carefully. The pandemic of 2020 infuriated many business owners when they realized that business interruption insurance does not (usually) cover pandemics. It does cover things like:

- Theft

- Fire

- Wind

- Falling objects

- Lightning strikes

In these cases, business interruption insurance will replace your income if your business needs to close.

Cyber liability insurance is increasingly important. If someone steals a customer’s credit card information and drains their account, you could be held liable. If someone hacks into your database and steals all of your customers’ information, cyber liability insurance should cover your legal costs.

Insurance for juice bars

Juice bars don’t have nearly as many risks as, say, a nightclub. Juice bars don’t serve alcohol, offer live entertainment or dancing. Still, accidents can happen. At the very least, you should get.

business owners policy and workers compensation insurance. The business owners policy combines general liability insurance and commercial property insurance, and you’ll need workers compensation insurance if you have even one employee in many states. The good news is that insurance for a juice bar is less expensive than insurance for a bar or a restaurant. Most juice bar owners pay less than $2,000 a year for all policies combined.

Last Thoughts

You’ve put a lot of hard work into your restaurant or bar business. Make sure you protect yourself from lawsuits by getting the right kind of insurance. After all, it can take only one accident to devastate your business.