Small business owners already know what commercial property insurance is: it protects the space you use for business and the contents within it. Even if you run your business from home, you should consider getting commercial property insurance, as your homeowners or renters insurance won’t cover your business.

What companies should you consider for commercial property insurance? These are our best 5 picks after comparing commercial property insurance quotes and policies from 10+ companies. Where we could, we entered that we were seeking commercial property insurance for a small bakery with two employees and $100,000 in revenue in Massachusetts to get a quote

- CoverWallet: Best for Comparing Quotes Online

- The Hartford: Best Commercial Property Insurance for Franchise Owners and Retailers

- Hiscox: Best Commercial Property Insurance for New Businesses

- Liberty Mutual: Best Commercial Property Insurance for Small Business Owners Who Prefer Working with An Agent

- Nationwide: Best Commercial Property Insurance for Contractors

- Travelers: Best Commercial Property Insurance for Property Owners with Multiple Properties

CoverWallet: Best for Comparing Quotes Online

Shopping commercial property insurance with one of the national digital commercial insurance broker will allow you to compare quotes online to select the best one for you. CoverWallet is one of the leading digital broker. Their quoting flow is very simple and fast. Just in less than 10 minutes, you will be able to compare 3-5 quotes from leading commercial insurance companies.

In addition to online quotes, if you are a new business owner and new to the world of commercial insurance, you might want to call their customer service to discuss your situation. Their customer service staff is very knowledgeable and will provide you with a lot of good information for your situation.

The Hartford: Best Commercial Property Insurance for Franchise Owners and Retailers

The Hartford offers a wide range of protections to help your business get back up and running in case of a fire, theft, or natural disaster. The Hartford offers flexible options so that you can tailor your policy to your business and make adjustments as needed.

The Hartford has a Risk Engineering team that was launched to help businesses determine their risks. They can help you avoid accidents, prevent potential losses, and make suggestions to improve workplace safety.

The Hartford has resources specifically for franchise owners, making it our top pick for such businesses.

The Hartford can offer you a commercial property insurance policy as a standalone policy, or they can combine it with general liability into a business owners policy (BOP). Prices are competitive and the customer reviews are pretty positive.

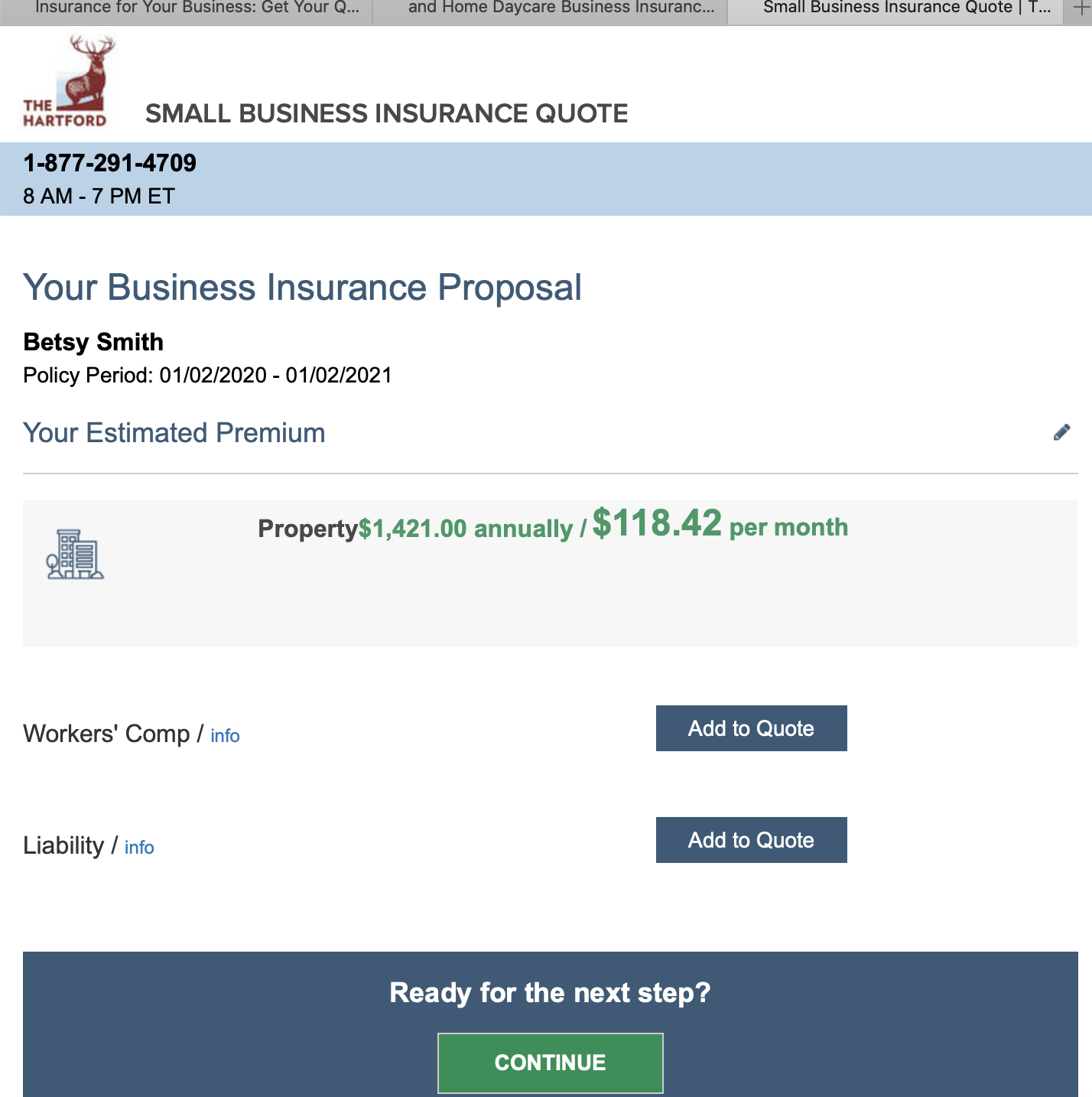

The Hartford asked a lot of questions before they would give us a quote for our hypothetical bakery. They wanted to know:

- What year the building was built (1952 is what we said)

- Is the building constructed with wood framed exterior walls?

- Does the building have wood joists/rafters in the roof?

- Are the exterior walls constructed of solid masonry materials?

- Is the building rated as “fire resistive”?

- Number of floors

- Have the building’s roof, electrical, HVAC, and plumbing all been updated?

- Year they were modernized?

They quoted us a rate of $1421.00 annually, or $118.42 a month for commercial property insurance.

>>MORE: Full Review of the Hartford Small Business Insurance

Hiscox: Best Commercial Property Insurance for New Businesses

Hiscox is a new but growing small business insurance provider. Their commercial property policy covers some things that other policies do not, such as:

- Tenant improvements

- Lost business income and extra expenses

- Forgery

- Accounts receivable

- Interruption of computer operations

They have policies that are customizable and flexible. You can buy their insurance either online or through an agent. They have a 14-day money back guarantee, which not many insurance companies offer. They also have online resources for the new business owner, as well as a fairly straightforward process for getting a policy, making them our pick for new owners.

>>MORE: Full Review of Hiscox Small Business Insurance

Liberty Mutual: Best Commercial Property Insurance for Small Business Owners Who Prefer Working with An Agent

Liberty Mutual has several features that make it an appealing option for small business owners.

They have local agents, so they have a personal relationship with you and your business. Since they are local, they have a better understanding of your needs and your community.

They have a flexible range of coverages, so you be sure your business is protected. Regardless of size or industry, Liberty Mutual has coverage that will work for you.

If you live in the Northwest, companies with similar business needs can join together and get reduced policy rates from Liberty Mutual.

Liberty Mutual doesn’t even have an online quote system for business insurance. You are asked to call and speak to an agent and they will help you.

>>MORE: Full Review of Liberty Mutual of Small Business Insurance

Nationwide: Best Commercial Property Insurance for Contractors

Nationwide is a fortune 500 company with over eighty years of experience serving the needs of small businesses.

They have a number of PDF articles for small contractors, which are excellent references. They also have every type of insurance a small contractor might need.

Agents are available 24/7 to answer questions or help you file a claim. They have prevention and loss tools to help prevent claims from happening in the first place.

They received the highest score for overall customer satisfaction in J.D. Power’s commercial insurance study for 2019.

We entered our information for Nationwide and got a message saying we should call so they could help us find a policy.

>>MORE: Full Review of Nationwide Small Business Review

Travelers: Best Commercial Property Insurance for Property Owners with Multiple Properties

Travelers is a huge company that strives to be there for small business owners. They offer flexibility in what coverages you add on, and you can add riders for more comprehensive coverage.

If you are someone who manages property, you know that claims can happen any time of the day or night. Travelers has a 24/7 claims center. They also have one of the largest risk control departments in the industry, so you take them to all of your properties to see where you can lower your risk.

One product they offer is the green building coverage. This is an extension that will pay to meet green standards for your building after you suffer a loss.

MyTravelers for Business in their online app where you can pay your bill, get a copy of your documents, and request certificates.

Travelers doesn’t offer commercial property insurance in all 50 states, however, so if you live in one of the states they don’t insure, you’ll have to look elsewhere.

Traveler’s would also like you to call to get a quote from them.

>>MORE: Full Review of Travelers Small Business Insurance

What is commercial property insurance?

Commercial property insurance protects your business from loss due to fire, theft, vandalism and natural disasters. You’ve invested your hard-earned money in this business, and you want to protect yourself. Furthermore, if you rent or lease space, the landlord will require it.

>>MORE: Commercial Property Insurance: What It Covers & Who Needs It

What does commercial property insurance cover?

Commercial property insurance covers the space where you do business and the items inside and around it. It includes:

- Computers

- Furniture

- Equipment

- Exterior signs, fencing, etc.

- Important documents

- Business inventory

- Building

- Tools

- Loss of income due to property damage

The last one is important. If there’s a fire in the building where you rent space and you can’t use it for two weeks while it’s being repaired, commercial property insurance will cover you for the loss of income.

What doesn’t it cover?

Generally, commercial property insurance will not cover damage from floods or earthquakes, unless you purchase it as an extra protection. If you’re a landlord who rents space to businesses, you can require your tenants purchase commercial property insurance.

Who needs commercial property insurance?

Anyone who runs a business should consider commercial property insurance. You know you need to protect your business, but what you may not know is that if you run a business from home your homeowners insurance may not adequately cover your office space or your business inventory. Furthermore, if you run a business from your home and your insurance company isn’t aware of it, they could deny you a claim.

The cost of commercial property insurance varies according to the following:

- Location

- Construction of the building

- What kind of business

- Occupancy

- Fire and theft protection: if you have a security system in place, sprinklers, etc.

- Value of your business

When you look into commercial property insurance, you’ll need to decide between actual cash value coverage (ACV) and Replacement Cost (RC) coverage. ACV means you’ll be reimbursed for the current fair market value of the property that was damaged. RC means you’ll get cash to buy new equipment. ACV is less expensive, but if buying all new equipment in case of a loss will bankrupt you, you should consider RC coverage.

Let’s say you run a bakery. There’s a fire and your ovens and equipment is a total loss. You purchased the equipment five years ago for $50,000. If you have ACV coverage, you might get $30,000 because of depreciation whereas if you had RC insurance, they might give you $60,000 to cover the cost to buy replacement equipment.

You will also need to decide if you want “all perils” coverage or “named perils” coverage. All perils covers your property for every type of damage that the policy doesn’t specifically exclude, and named perils only covers the ones you list on the policy. All-perils coverage is more expensive because it offers broader coverage.

What is commercial landlord insurance?

If you make money by renting out apartments to others, you’ll want commercial landlord insurance. This is a little different than commercial property insurance, as you need to protect your property from damage from the tenants, and you’ll also need to protect yourself against lawsuits from tenants who fall down the stairs or slip on an icy sidewalk.

What is additional insured on a commercial property policy? How does it work?

An additional insured is a third party that has a liability exposure in a business relationship. For example, if you have a cleaning business in a commercial building, you could ask to be named as an additional insured on the owner of the building’s policy. That way if someone falls on the floor you just cleaned, you’ll be protected by the owner’s general liability policy or business owner’s policy. You should get your own general liability insurance, though, just in case.

>>MORE: The 5 Best Providers of Cleaning Business Insurance

Vacant commercial property insurance

Vacant buildings are often targets of vandals and thieves. They can also sustain damage from fire and other natural disasters. A property is considered vacant if it’s less than 31% occupied for an extended period of time. This can happen because of renovations or repairs. Vacant commercial property insurance protects the owner of the building from losses due to fire, vandalism, flood, etc.

How to get cheap commercial property insurance?

Commercial property insurance is often bundled with general liability insurance, in what’s called a business owner’s policy. That way, both your property is covered in case of damages due to fire or natural disasters, and you’re also covered if someone injures themselves on your property.

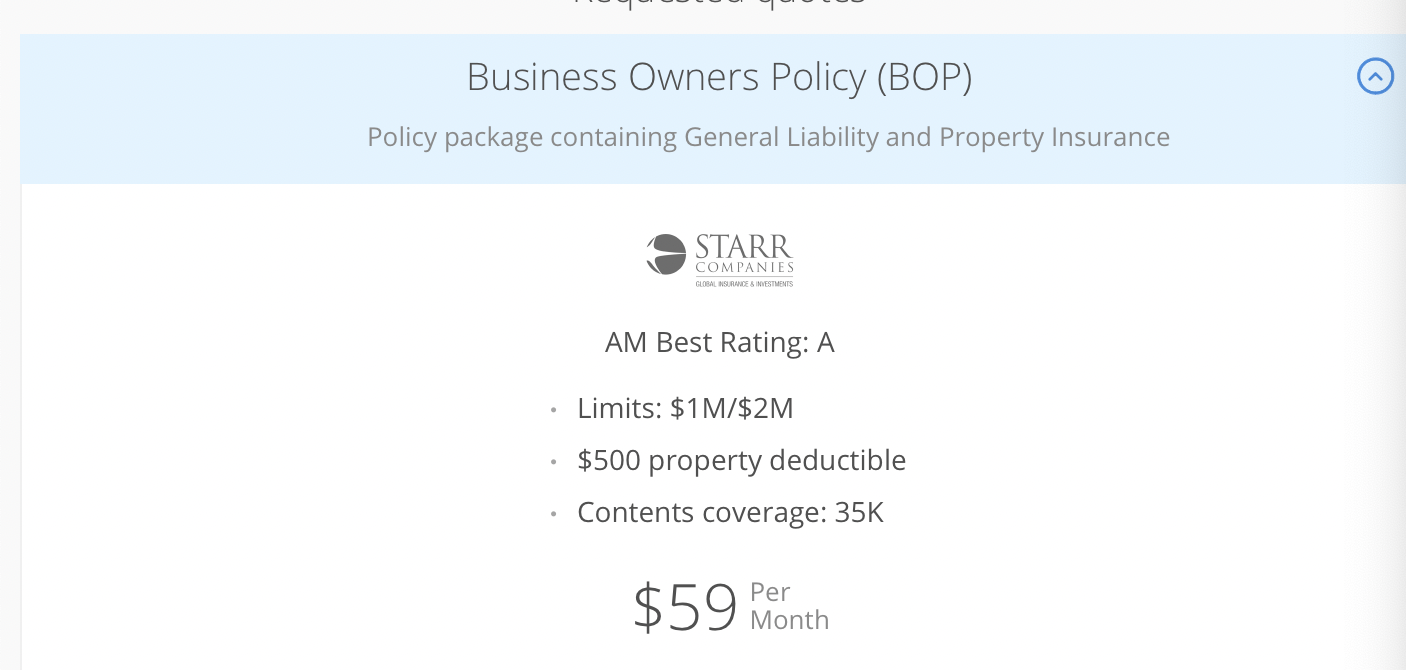

The following quote is from Coverwallet. They wouldn’t give us a quote for just commercial property insurance, they insisted we needed a business owner’s policy (which is true). We asked for a quote for a small bakery with one owner, two full time employees and one part-time employee and $100,000 in revenue per year.

Keep in mind that you can deduct the cost of commercial property insurance on your taxes because it’s a business expense.

To save some money on commercial property insurance, make sure the building is new, or has been updated. If your building is older than fifty years old, make sure the plumbing, electrical, HVAC and roof have been updated. You can also invest in a security system and fire safety equipment. Also keep excellent records (which every business should do anyway) in case of a claim.

Final Thoughts

Each company has its own specifications about their properties. Each insurance company has its specific benefits and weaknesses in its commercial property insurance policies. They also specialize in specific industries. You should shop around and compare quotes from at least 3-5 companies to choose the best policy for your business.

>>MORE: How Much does Commercial Property Insurance Cost?

Below are a few FAQs about Commercial Property Insurance

1. Should I combine commercial property insurance with general liability insurance?

If you can, you should. This is called a Business Owners Policy and it offers the protection of both types of insurance at a rate lower than if you were to buy the policies separately.

2. How can I reduce the costs of commercial property insurance?

Insurance companies like to see a building newer than fifty years. If your building is older than this, you can make sure the roof, the HVAC, plumbing and electrical systems have all been updated. Having fire safety equipment and a security system will also save you money. Some insurance companies will go over your business with you and make recommendations on how you can make your office space safer.

3. Is commercial property insurance required by law?

No, but if you lease or rent a space from a landlord, the landlord may require you to have it. Read your lease carefully.

4. What is business interruption insurance? And do I still need it in addition to commercial property insurance?

In the event some catastrophe happens and your business is forced to close temporarily, business interruption insurance will help reimburse you for lost income and get you back on your feet.

Commercial Property Insurance and Business Interruption Insurance are complimenting each other. For example, if your business is closed due to fire. Commercial Property Insurance will cover the damages of the building and other equipment caused by the fire whereas Business Interruption Insurance will cover the lost income during the period when your business is closed. That’s the reason why for small businesses of annual income of less than $1 million, commercial property insurance, general liability insurance, and business interruption insurance are combined into one single policy, called Business Owners Policy (BOP).