With all the numbers, laws, and regulations associated with the work financial and investment advisors do, it’s easy for them to make mistakes that could result in client lawsuits or regulatory actions. In many cases, the cost of a lawsuit and settlement could be in the six or seven figures. The expenses related to defending yourself in a regulatory dispute can be almost as much. A lawsuit or regulatory action can put a financial professional out of business and cause them to lose their home and forfeit their savings.

Errors and omissions (E&O) insurance, often referred to as professional liability insurance, can help prevent these losses.

In this article, we’ll reveal the top 5 errors and omissions insurers for financial and investment advisory businesses in the U.S. and explain what makes them the best. We’ll also provide you with the information you need to get the coverage that’s right for you.

- 5 top errors and omissions insurers for financial and investment advisory businesses in the United States

- What is the top risk faced by financial professionals?

- What does E&O insurance for financial and investment advisors cover?

- What does errors and omissions insurance pay for?

- What other types of insurance do investment and financial advisors get?

- What E&O insurance for financial firms doesn’t cover

- How much does professional liability insurance for financial advisors cost?

- Ways to save money on your errors and omissions insurance

- How to find cheap errors and omissions and other business coverage

5 top errors and omissions insurers for financial and investment advisory businesses in the United States

- CoverWallet: Best for financial and investment professionals who want to compare quotes quickly

- Hiscox: Best for financial businesses with unique E&O coverage needs

- Next: Ideal for financial and investment advisors who prefer to buy insurance online

- Insureon: Best overall online insurance buying experience

- Chubb: Best for advisors who prefer coverage from an established insurer

CoverWallet: Best for financial and investment professionals who want to compare quotes quickly

CoverWallet is a cutting-edge insurance provider. The firm has developed its own state-of-the-art platform, based on its own algorithms, to ensure it is able to connect small businesses with all the E&O and other business insurance they need, at the most reasonable price. The platform makes it quick and easy to get quotes from several providers at once, making it possible to compare premium prices from highly reputable insurers all on a single screen.

The firm’s experts have used their extensive experience to make sure you only have to input the information needed to generate quick and accurate quotes. The entire process should take ten minutes or less.

You can feel confident knowing that CoverWallet is a part of Aon, an established company that provides advice to businesses on things like risk, health, and retirement.

Once you get your quote, CoverWallet makes it easy to purchase E&O and other business insurance online or through an agent. When you get your policy through CoverWallet, it’s simple to manage your coverage online, including downloading a certificate of insurance, filing a claim, renewing your insurance, and more.

Hiscox: Best for financial businesses with unique E&O coverage needs

Hiscox offers a complete array of business coverages, including errors and omissions insurance, and is a leading insurer that specializes in small companies.

Hiscox makes it easy to purchase most types of business insurance online. You can also speak with experienced business insurance experts who can help you customize your coverage to meet the specific risks you and your employees face. The insurer is known for providing top tier service, delivering fast quotes, supplying instant coverage, and processing claims quickly.

If you choose Hiscox for your business coverage, you can feel confident knowing you’re entrusting your organization to a firm that’s been in operation since 1901. More than 400,000 companies have turned to Hiscox for their coverage.

Next: Ideal for financial and investment advisors who prefer to buy insurance online

Next is changing how businesses purchase E&O insurance and other coverage.

Their operation is focused on delivering the ultimate online insurance experience. Because of this, you’re able to purchase a policy, file a claim, or get a certificate of insurance any place, any time, 365 days a year. Even though Next is an online insurer, you can get expert help over the phone when you need it.

Even though Next is a relatively new and innovative company, you can rest assured knowing it has an excellent rating from A.M. Best, an insurance company rating agency. All the company’s policies are backed by MunichRe, an established insurance company and reinsurer. More than 10,000 business owners have turned to Next for their insurance needs. The firm has earned a solid 4.7 customer rating.

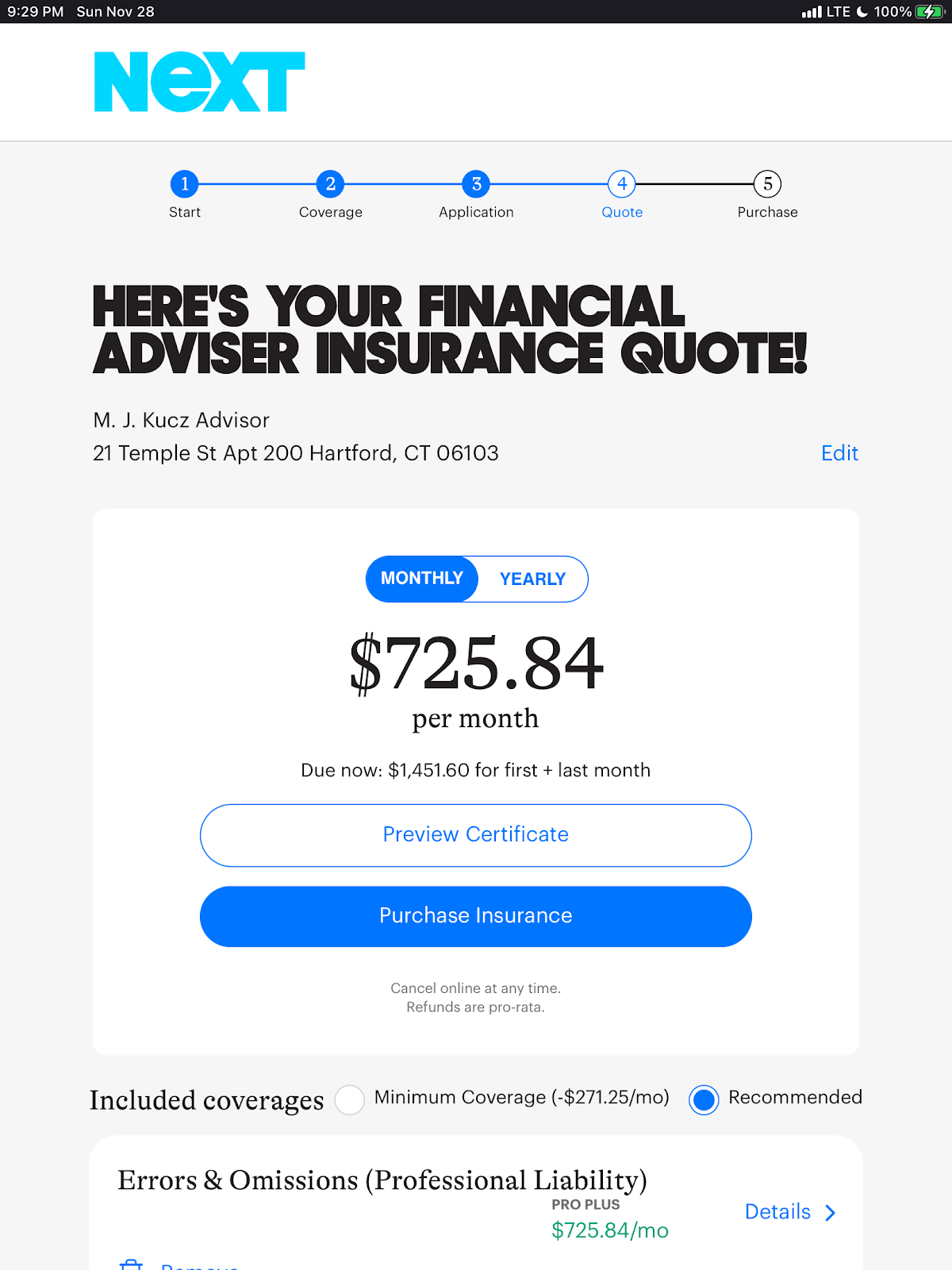

Here is a sample E&O quote fromNext.

Insureon: Best overall online insurance buying experience

Insureon is the number one independent online marketplace for small business insurance. The company’s platform makes it easy to apply for errors and omissions and other types of small business insurance coverage, buy policies, and manage your insurance all in one place. Plus, if you need help selecting your coverages, Insureon has experts who can answer your questions and provide advice over the phone.

Even though Insureon is a tech based company, you can rest assured knowing it has been in business for more than ten years. They’ve written more than one million policies and have provided insurance for more than 350,000 small businesses.

Chubb: Best for advisors who prefer coverage from an established insurer

Chubb is the largest publicly traded property and casualty insurance company in the world.

Chubb focuses on understanding the unique risks of businesses in different industries including all aspects of financial services. That means your business general liability coverage can be combined with other coverages (Chubb has more than 30 of them) to protect against the risks faced by almost any type of financial advisory or investment business

Because the experts at Chubb have such a deep understanding of the risks faced by businesses in many industries, they have programs — and are able to offer advice — on how to reduce risks in the workplace. Not only is lowering risk levels the right thing to do, it can help cut errors and omissions and other business insurance costs.

What is the top risk faced by financial professionals?

As a financial or investment advisor, your risk of lawsuits is relatively high, perhaps only slightly less than that for medical professionals and lawyers. When you provide financial or investment advice to clients, if they lose money based on what you tell them or forget to tell them, you could be sued for their losses, whether you are at fault or not. Professional liability insurance will help cover discovery, legal, and settlement costs if your business is sued because you or someone who works for you forgets to provide information or makes a mistake while offering financial or investment advice to them.

What does E&O insurance for financial and investment advisors cover?

Professional liability insurance typically covers:

- Breach of fiduciary duty. In this case, a client sues you if they believe you didn’t act in their best interest. For example, if you recommend a higher commission stock that’s not suitable for them rather than one that’s better aligned with their investment goals.

- Failing to comply with regulations. You’re covered if you have to defend yourself because you fail to comply with financial industry or government regulations.

- Omissions or mistakes in providing advice to clients. If you, or someone who works for you, fails to provide complete information or good advice to a client and it leads to financial losses for them, you could be covered for discovery, legal, and settlement costs.

Even if you’re found to be not guilty in a regulatory or legal matter, professional liability insurance will still cover your defense expenses.

>>MORE: The Best Professional Liability Insurance Companies

What does errors and omissions insurance pay for?

If someone sues your business for making a mistake related to the financial or investment advisory services you provide — or you fail to meet regulatory requirements — errors and omissions insurance helps cover your:

- Legal fees, which can easily reach six figures even in frivolous lawsuits

- Court costs, such as reserving a courtroom

- Administrative costs to build a defense

- Settlements and judgments, which typically cost thousands to millions of dollars.

A business insurance specialist with experience in working with financial and investment advisors can explain what an E&O policy covers.

Tip: Even if you don’t make a mistake, your client can sue you. Your errors and omissions insurance will still cover your legal and other related costs.

>>MORE: The Best E&O Insurance Companies

What other types of insurance do investment and financial advisors get?

It all depends on your operation, but some common coverages purchased by financial businesses include:

A Business Owners Policy (BOP). It provides many of the core coverages you need to protect your investment or financial advisory business, including:

- General liability insurance covers you and your business if someone is injured while visiting your office. It will also cover claims of libel and slander. Example: A client slips and falls in your lobby and breaks a hip. General liability insurance will pay for their medical care. Learn more at the best general liability insurance companies.

- Business property insurance protects your financial office space, whether you rent or own it. The coverage will pay for repairs from damage caused by things like fire or wind storms and other weather events. It will also pay for damage to — or theft of — office equipment. Learn more at the best commercial property insurance companies.

- Business income insurance will pay lost income if you cannot open your office and meet with clients because of a reason covered by your business property insurance, such as fire damage or theft. Learn more at the best business income interruption insurance companies.

A BOP makes it easy to purchase the other coverages your financial firm needs, including errors and omissions, and add them to your policy. Learn more at the best BOP insurance companies.

Tip: If you run your investment or financial advisory business out of your home, it’s critical that you get a BOP. Your homeowners insurance policy will not cover client injuries that happen at your home or work property losses.

Some other coverages to consider include:

- Employment practices liability insurance. This covers you if an employee sues you or your business over things like discrimination or sexual harassment.

- Cyber (data breach) insurance. Financial advisory firms store a lot of confidential client data on their computers and servers. This insurance will pay costs related to a data hack or theft — or a ransomware attack. Learn more at the best cyber insurance companies and the best data breach insurance companies.

- Valuable papers and records coverage. This will pay to replace or restore client files or financial records that get damaged, are lost, or stolen.

- Computers and media coverage. Financial firms are highly dependent on computers. This insurance protects you if your computer equipment is damaged by a malicious virus.

- Commercial vehicle insurance. Many financial professionals drive their personal cars to clients’ homes and offices. If you or someone who works for you has an accident while driving for business, their personal auto policy won’t cover the damages. That’s why it’s important to be protected by a business auto policy. Learn more at the best commercial auto insurance companies.

What E&O insurance for financial firms doesn’t cover

E&O insurance doesn’t cover claims from events that happened before your policy’s retroactive date (the first date that an issue can be covered). It also doesn’t help your business with claims filed after your policy’s extended reporting period (the timeframe, usually three or six months after a policy ends). It also doesn’t cover illegal acts and purposeful wrongdoing, such as intentionally breaking the law or outright lying to your clients.

How much does professional liability insurance for financial advisors cost?

On average, a financial or investment advisor can expect to pay approximately $1,500 per year for this coverage. Of course, many factors go into calculating your premium costs including the size of your financial firm, number of employees, assets under management, prior claims history, and more. What’s important is that you get quotes from multiple insurers to makes certain you get the coverage you need at the best possible price.

Ways to save money on your errors and omissions insurance

You may be able to keep your E&O and other business insurance costs down by:

- Providing your employees with ongoing regulatory training focused on best practices. Of course, you should take advantage of the training, as well

- Hiring the best people

- Communicating with customers regularly to make sure they’re satisfied and don’t have doubts about the advisory services you or the people who work for you provide to them.

How to find cheap errors and omissions and other business coverage

There are a few ways to find the coverage you need at a fair price:

- Shop around for the best value. Get quotes from a few companies and compare coverages and costs to find the best combination of the two.

- Don’t stop shopping around. Make sure you get new quotes when it comes time to renew your policy.

- Take advantage of discounts. If they’re not offered to you when getting a quote, ask about them, whether you’re buying online or through an agent.

Taking these steps will help ensure you’re not paying too much for your E&O and other business coverage.