Errors and omissions (E&O) insurance is one of the least understood business coverages. The truth is that what it covers is relatively simple: Lawsuits related to mistakes made by you and the people who work for you when providing services to your clients.

Even if you’re the absolute best at what you do and run a completely buttoned up operation, mistakes and unintentional errors happen. If a client or customer believes a mistake or error committed by you or an employee while providing services to them resulted in a financial loss or other harm, they can sue you. And these days, they often do.

Professional liability insurance helps cover you and your business if a client or customer sues because they aren’t happy with the service that your business provided to them. This coverage is also known as professional liability or indemnity insurance.

In this article, we’ll reveal the top four errors and omissions insurers in the U.S. and explain what makes them the best. We’ll also provide you with the information you need to get the coverage that’s right for you.

- What is errors and omissions (E&O) insurance?

- Who needs E&O coverage?

- What does E&O insurance cover?

- What errors and omissions insurance doesn’t cover

- Why errors and omissions coverage is important

- The cost of errors and omissions insurance

- Ways to save money on your errors and omission insurance

- How to find cheap errors and omissions insurance

- 5 top errors and omissions insurers in the United States

What is errors and omissions (E&O) insurance?

Errors and omissions insurance, also commonly known as E&O insurance and professional liability or indemnity insurance, protects you and the people who work for you against lawsuits claiming someone made a mistake when providing professional services. This insurance can cover legal and court related costs, along with settlements. These things can be very costly for a business to pay for, especially those in particularly risky professions like healthcare and law.

Who needs E&O coverage?

Businesses that provide services to customers should purchase errors and omissions insurance. This includes:

- Insurance agents who could be sued if your clients believe that they are getting the coverage that they didn’t. See more in the best E&O insurance for insurance agents

- Real estate agents who can be held responsible for failing to disclose defects in a property, misfiling paperwork, or breach of contract. See more in the best real estate E&O insurance

- Notary that could be taken to court if they fail to verify the signing person is who they say they are. Learn more in the best notary E&O insurance

- Home inspectors that can be used by either home sellers or home buyers if they believe that the home inspector is negligent in doing in their job. Learn more in the best E&O insurance for home inspectors

- Appraisers who can be held liable legally responsible for making a mistake in their real estate appraisers causing their clients financial loss. See more in the best E&O insurance for appraisers

- Accountants who could be sued if they make a calculation error that ends up costing a client money. See more in the best E&O insurance for accountants and CPAs

- Engineers and engineering firms that could be held liable if they misinterpret architectural plans and make a construction error that prevents a building from being approved for use. See more in the best professional liability insurance for engineers

- Advertising and marketing firms that could be taken to court if they develop an ad or website that includes an error that costs the client money

- Educators that could be sued because students think they shared incorrect information. See more in the best professional liability insurance for teachers

- Florists and wedding planners who could be held legally responsible for not delivering on contractually required event services. See more in the best event planner insurance

- Consulting companies who could be sued if the recommendations they make to clients cause harm to their business. See more in the best professional liability insurance for consultants

- Lawyers and legal firms that can be held liable if they provide advice to a client that’s wrong or makes their legal situation worse. It is usually called as legal malpractice insurance. See more in the best legal malpractice insurance

- Printing and publishing companies can be sued for things like making a mistake in a book they publish or forgetting to print invitations on time

- Doctors and medical professionals are often sued for malpractice if a healthcare service they provide does not help a patient or makes their condition worse. It is usually called medical malpractice insurance. See more in the best medical malpractice insurance

- Veterinarians, similar to doctors, can be sued for providing care to animals that doesn’t help or makes what they’re suffering from worse

- Hair stylists are often sued if they cut, burn or otherwise harm a customer while providing hair care services. See more in the best barber and hair stylist insurance

This list makes it clear that even the most careful, by the book business, can be sued for making simple mistakes. It’s the reason it is a smart move for businesses that provide services to people to get errors and omissions coverage.

What does E&O insurance cover?

Errors and omissions coverage helps protect your business from claims related to:

- Negligence, or gross irresponsibility in providing professional services

- Errors in services provided, including common mistakes and human error

- Omissions, including forgetting to communicate important things or leaving out critical information

- Misrepresentation, or representing something that’s untrue as true

- Violation of good faith and fair dealing, or providing a level of service that’s outside the profession’s norms

- Inaccurate advice, or providing recommendations that are factually wrong.

If someone sues your business for making a mistake related to the professional services you provide, errors and omissions insurance helps cover your:

- Legal fees, which can easily reach six figures even in a frivolous lawsuit

- Court costs, such as reserving a courtroom or paying for expert witnesses

- Administrative costs to build a defense, including paying court reporters

- Settlements and judgments, which typically cost thousands to millions of dollars.

A business insurance specialist can explain what your E&O policy covers.

What errors and omissions insurance doesn’t cover

E&O insurance doesn’t cover claims from events that happened before your policy’s retroactive date (the first date that an issue can be covered). It also doesn’t help your business with claims filed after your policy’s extended reporting period (the period, usually three or six months after a policy ends when a business is allowed to report an incident that took place during the time when the policy was in effect).

Also, errors and omissions coverage won’t help your business with claims related to:

- Illegal acts and purposeful wrongdoing, such as intentionally breaking the law or lying to your customers or clients.

- Bodily injury or property damage that’s cause by your business. A general liability policy will cover these types of issues.

- Employee injuries or illnesses that happen because of work-related reasons. A workers’ compensation policy will cover medical care and provide benefits to employees who are injured or get sick on the job. Be aware that most states require this coverage if you have employees.

- Discrimination or harassment in the workplace that employees sue you over. Employment practices liability insurance could help cover these types of claims.

Why errors and omissions coverage is important

Think about it, would your business be able to pay legal and other related costs if you or someone who works for you makes a mistake in providing professional services and your business is sued? The answer for most organizations is NO, because these costs can rise into the millions of dollars. A lawsuit, even a frivolous one or one that’s dropped, often forces businesses to close down.

The cost and likelihood of lawsuits today are the primary reasons professional services businesses need errors and omissions coverage.

How much is the cost of errors and omissions insurance

Perhaps more than any other type of insurance, the price of errors and omissions coverage varies significantly. It will cost less for florists, where the risk of a costly lawsuit is lower than for doctors who frequently conduct difficult brain operations.

Each professional services business has unique needs and faces different risks, so it’s impossible to benchmark the typical cost of coverage. Your errors and omissions insurance premium amount will be specific to your company. However, no matter how much it costs, it’s a smart investment in the long term security of your business.

Different factors impact your E&O insurance cost, including:

- Business risk: If you’re in a higher risk industry, you’ll likely pay more for your coverage

- Coverage limits: Higher policy limits usually lead to higher premiums

- Claims history: Typically, you’ll pay more for your E&O coverage if you have a history of professional liability claims against your business

- Location: Rates are typically higher in larger cities.

Get quotes from multiple providers to ensure you’re getting adequate errors and omissions coverage at a fair price.

>>MORE: E&O Insurance Cost for Different Professionals

Ways to save money on your errors and omissions (E&O) insurance

You may be able to keep your E&O insurance premium down by:

- Providing your employees with ongoing professional services training focused on best practices. Of course, you should take advantage of the training, as well

- Hiring the best people

- Communicating with customers regularly to make sure they’re satisfied and don’t have doubts about the services you provide to them.

How to find cheap errors and omissions insurance

E&O coverage is important and you shouldn’t skimp on it. However, there are some ways to help you find the coverage you need at a fair price:

- Shop around for the best value. Get quotes from a few companies and compare coverages and costs to find the best combination of the two.

- Don’t stop shopping around. Make sure you get new quotes when it comes time to renew your policy.

- Take advantage of discounts. If they’re not offered to you when getting a quote, ask about them, whether you’re buying online or through an agent.

Taking these steps will help ensure you’re not paying too much for your E&O and other business coverage.

5 top errors and omissions insurers in the United States

- CoverWallet: Best for comparing several quotes online

- biBerk: Best for low-cost errors and omissions coverage

- Hiscox: Best for small businesses with unique E&O coverage needs

- Liberty Mutual: Best for companies that are growing and changing

- The Hartford: Best for businesses looking for a sound and ethical insurer

CoverWallet: Best for comparing several quotes online

If your goal is to compare several quotes online to get the best and the cheapest one for you, you may want to start with CoverWallet. They are a digital broker, specializing in small business insurance. They work with several leading companies and are able to pull quotes from these companies for you to compare and select the best and the cheapest one.

Once you buy a policy through CoverWallet, you can manage all of your business insurance policies through its digital dashboard. The dashboard offers several useful features such as downloading the certificate of insurance, renewing a policy, or filing a claim.

CoverWallet also earns a good consumer rating (A) on BBB.

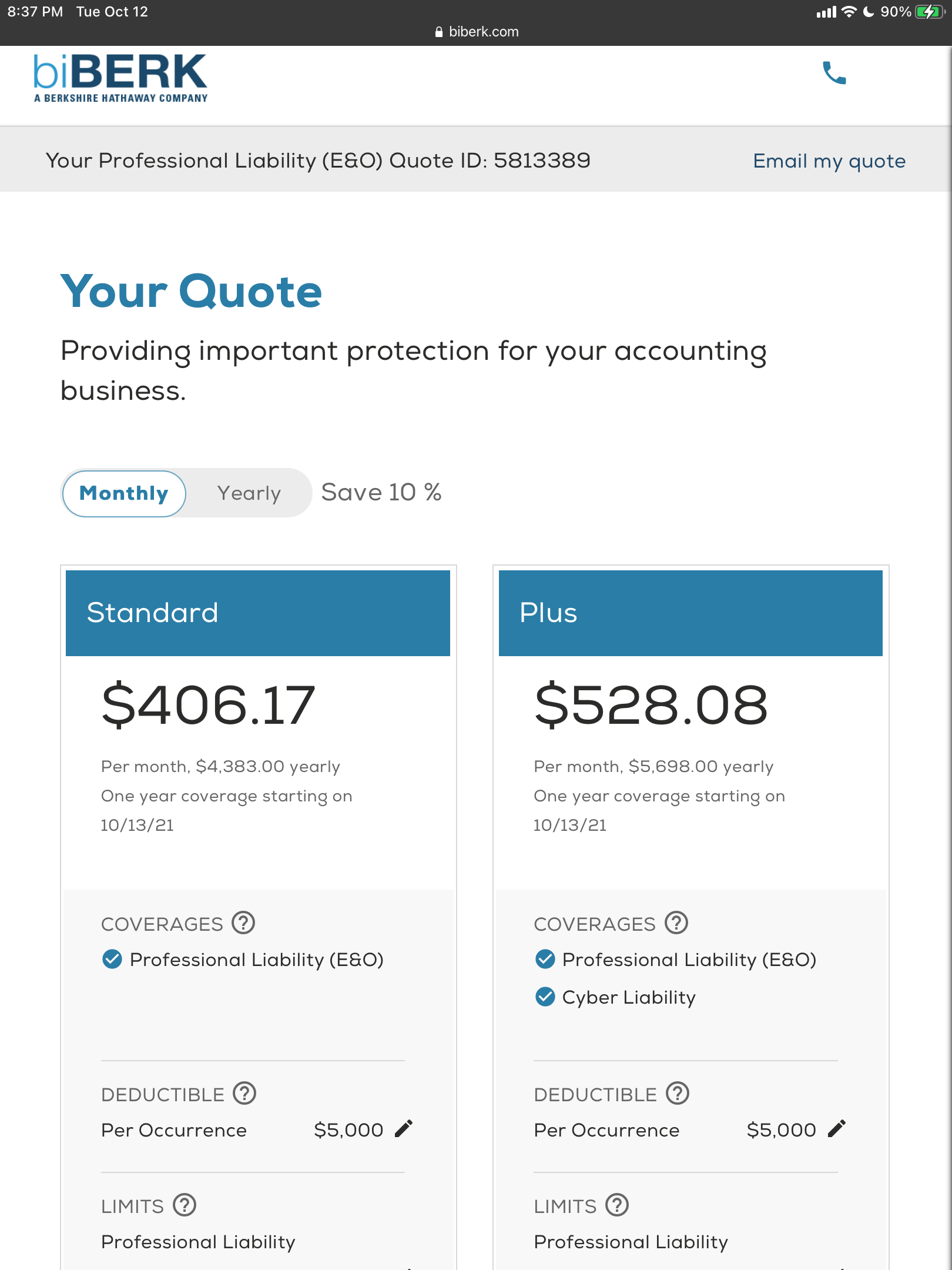

biBerk: Best for low-cost errors and omissions coverage

biBerk makes it simple to get an E&O quote online in less than five minutes. Getting coverage only takes a few minutes more.

biBerk is a low-cost business insurance provider. Despite saving money on your E&O insurance and other business coverage, you can rest assured knowing you’re still getting quality protection for your business. biBERK is able to lower insurance costs by almost 20 percent because it insures small businesses direct, without the added costs of having to work through a middleman or insurance broker.

You can rest assured knowing biBerk is a part of Berkshire Hathaway, a highly reputable company headed by well-known investor Warren Buffett. It’s a firm that has millions of satisfied customers that’s been insuring people and businesses for more than 75 years.

Here’s a sample E&O quote for an accounting business from biBerk:

Hiscox: Best for small businesses with unique E&O coverage needs

Hiscox offers a complete array of business coverages and is a leading insurer that specializes in small business insurance.

Hiscox makes it easy to purchase most types of business insurance online, but we found that because of the complexity of errors and omission coverage, you may need to make a phone call to complete an E&O quote started online with Hiscox. You can also speak with experienced business insurance experts who can help you customize your coverage to meet the specific risks you and your employees face. The insurer is known for its top tier service, providing fast quotes, supplying instant coverage and processing claims quickly.

If you choose Hiscox for your business coverage, you can feel confident knowing you’re entrusting your organization to a firm that’s been in operation since 1901. More than 400,000 companies have turned to Hiscox for their coverage.

Liberty Mutual: Best for companies that are growing and changing

Small businesses change over time, and their insurance needs evolve, as well. Liberty Mutual is uniquely able to serve their changing insurance needs. This is especially important when it comes to errors and omissions coverage. It’s not enough to secure coverage once, you need to keep up with it and get more and different coverage as your risks increase and evolve.

In addition to E&O protection, Liberty Mutual offers one of the most comprehensive ranges of business coverages of any insurer. They are able to customize policies to meet the needs of virtually any business. In addition to this, their experts are always looking ahead to identify new business risks and find efficient ways to cover them.

In addition to its flexibility, Liberty Mutual is a Fortune 100 company and one of the largest insurance firms in the United States and across the globe. You can feel confident knowing that Liberty Mutual will have the funds to cover any claim you make.

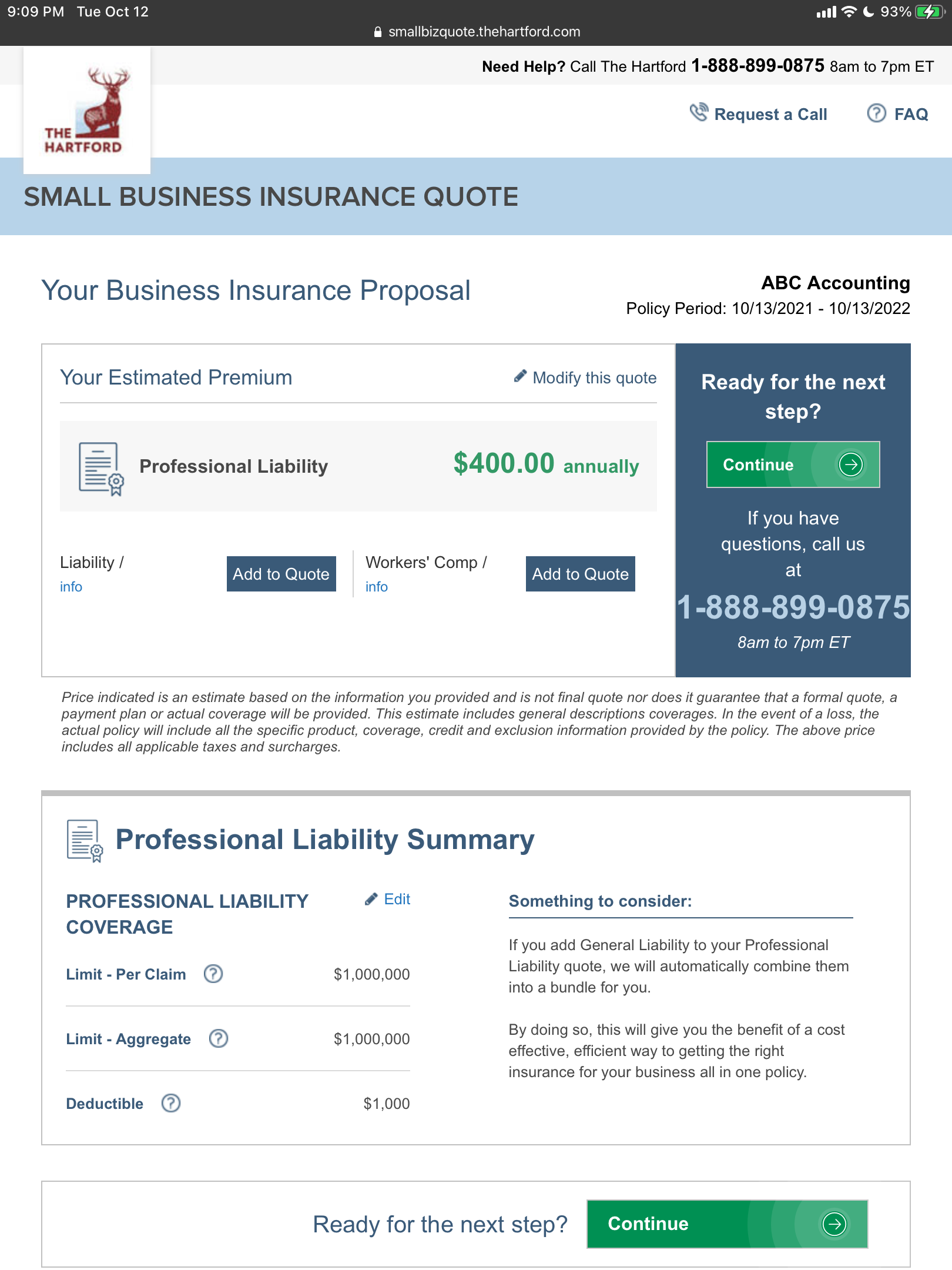

The Hartford: Best for businesses looking for a sound and ethical insurer

The Hartford is one of the oldest companies of any kind in the United States. It’s been offering insurance solutions for more than 200 years and has helped one million plus businesses with their insurance needs. The Hartford has been named a World’s Most Ethical Company by the Ethisphere Institute twelve times. The Hartford’s longevity and focus on ethical business practices makes it a company that you can feel good about getting your E&O and other business coverage from.

The Hartford’s dedicated and highly experienced small business team is available to help company owners explore their E&O and other commercial insurance options. If you decide to purchase insurance from The Hartford, you can rest assured knowing you’re entrusting your business to a strong, stable, knowledgeable and ethical provider.

Here is a sample E&O quote from The Hartford for a small accounting firm:

>>MORE: Best E&O Insurance Companies