As an insurance agent, you already know what errors and omissions (E&O) insurance is—it’s a policy that protects businesses against lawsuits claiming a business was negligent or in error. You may have even sold this insurance to some of your clients.

The question is, as an insurance agent, do you need errors and omission insurance? Let’s take a look at why you may want to get errors and omissions insurance for yourself.

- Top 5 Providers of E&O Insurance for Insurance Agents

- What is Errors and Omissions (E&O) Insurance?

- Why do Insurance Agents Need Errors & Omissions (E&O) Insurance?

- What does Errors and Omissions (E&O) Insurance Cover and not Cover?

- How Much does E&O Insurance for Insurance Agents Cost?

- How to Find Cheap E&O Insurance for Insurance Agents?

- Cheap E&O Insurance for Life & Health Insurance Agents

- Cheap E&O Insurance for P&C Insurance Agents

Top 5 Providers of E&O Insurance for Insurance Agents

After looking at price, customer service, digital experience, and convenience, we recommend the following five companies.

- CoverWallet: Best for Comparing Online Quotes

- CNA: Best for Personalized Policies

- Hiscox: Best for Claims Responsiveness

- Travelers: Best for Flexible Coverage

- BCS Insurance: Best for Individual Plans

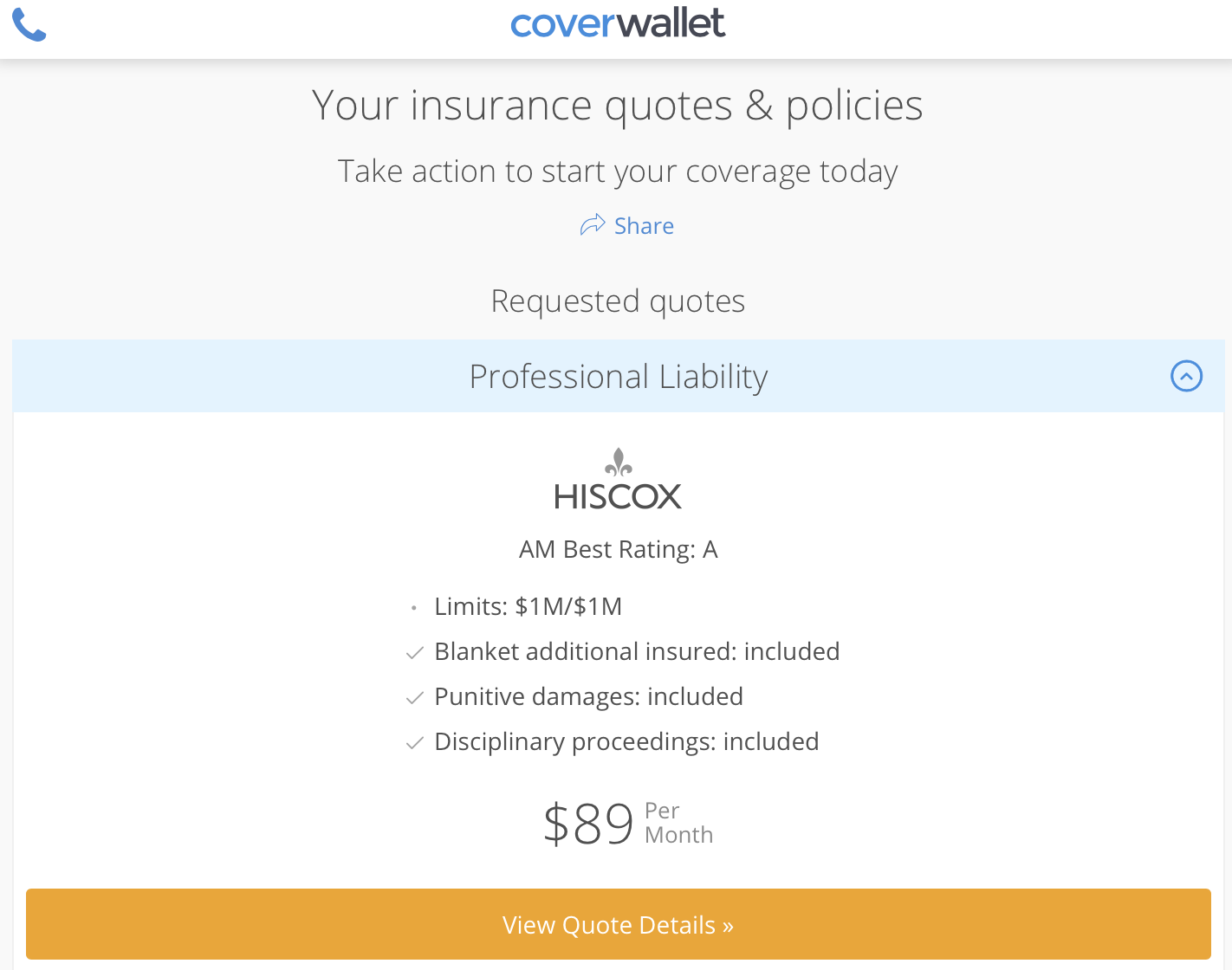

CoverWallet: Best for Comparing Online Quotes

CoverWallet’s easy online quote system make them a contender for anyone seeking insurance. Using a sophisticated system of AI and human intelligence, they can provide you will quotes from multiple insurance companies within minutes. If you prefer to talk to an agent, you can do that, too.

CNA: Best for Personalized Policies

CNA is the nation’s leading provider of errors and omissions insurance. If you are searching for E&O insurance online, they underwrite eoforless.com, NAPA (National Association of Professional Agents), and 360 Coverage Pros, and a few others. All of these are underwritten by CNA. They understand the risks you expose yourself to and can recommend policies to protect you.

CNA won’t give you a quote online, they prefer to match you to an agent to give you their price quotes. They do offer an estimate of what you’ll pay.

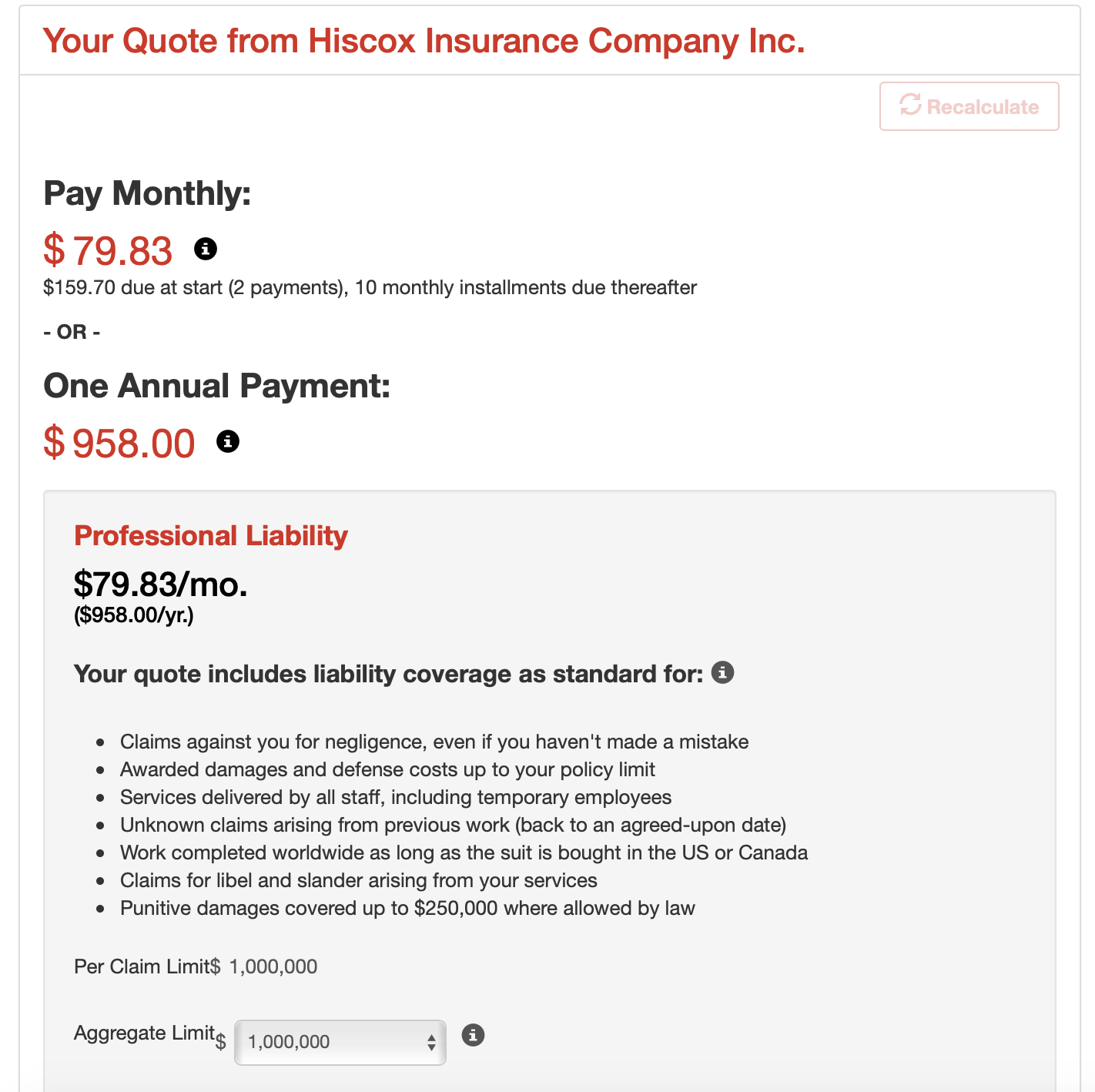

Hiscox: Best for Claims Responsiveness

Hiscox is also quick to provide online quotes, which simplifies the whole insurance buying experience. They are a specialty insurance company that devotes a lot of attention to the types of insurance they offer.

They are a carrier for Insurance Bee, so if you are interested in Insurance Bee, know that Hiscox might provide your insurance.

They have an A+ rating on BBB and almost no complaints. They pride themselves on immediately defending customers against claims and will even appoint a lawyer for you.

Travelers: Best for Flexible Coverage

Traveler’s has a specialty insurance program called Traveler’s Wrap+. It helps to protect you from a range of exposures and is non-cancelable by the insurer unless you neglect to pay your bill. They also have limits of up to $3 million dollars.

They don’t offer online quotes, but if you put in your zip code they will find an agent in your area.

BCS Insurance: Best for Individual Plans

BCS offers individual and company policies. They have errors and omissions insurance for specifically for insurance agents and they focus on protecting you from financial losses. They are backed by several different carriers, such as Chubb, Liberty Mutual and Beazley—it largely depends on what type of policy you want and what state you live in.

If you want a quote from BCS, you will have to submit a form. They will get back to you to discuss your options.

>>MORE: The 9 Best E&O Insurance Companies for Small Businesses

What is Errors and Omissions (E&O) Insurance?

Errors and Omissions (E&O) insurance is also called professional liability insurance—for a more thorough explanation, see “What is Professional Liability Insurance? And Its Cost?”

The amount of errors and omissions lawsuits brought against insurance agents seems to be increasing, according to a 2018 case law study. If a client feels you recommended inadequate insurance coverage and suffers financial losses because of that, they could turn around and sue you. Errors and Omissions (E&O) insurance is basically malpractice insurance.

Even if they have a frivolous lawsuit, you will still potentially have to go to court. Just one costly lawsuit could bankrupt you. Errors and Omissions (E&O) insurance would protect you.

>>MORE: Best Professional Liability Insurance Companies for Small Businesses

Why do Insurance Agents Need Errors & Omissions (E&O) Insurance?

Mistakes happen. Sometimes it’s something you overlook, sometimes it’s a typo when you enter information into the computer. Sometimes it’s a misunderstanding, for example, the client thought they were getting coverage that they weren’t.

Many insurance companies employ independent insurance agents. This may have the benefit of giving you more autonomy and earning potential, but it also holds you responsible if any claims are brought against you.

As an insurance agent, you’re an independent contractor. As an independent contractor, you could be sued personally if a client is dissatisfied with something.

What does Errors and Omissions (E&O) Insurance Cover?

Insurance agents are typically sued for things like:

- Mistakes

- Failure to maintain appropriate coverage

- Failure to explain coverage

- Failure to share or explain policy changes

- Failure to send accurate information to the insurer

- Failure to disclose exclusions

Errors and omissions insurance covers:

- Legal defense costs

- Judgements

- settlements

What doesn’t It Cover?

- White collar crime. In other words, if you set out to defraud your clients and your goal is to steal their money, you’re not covered.

- Discrimination

- Acts that pollute.

How Much does E&O Insurance for Insurance Agents Cost?

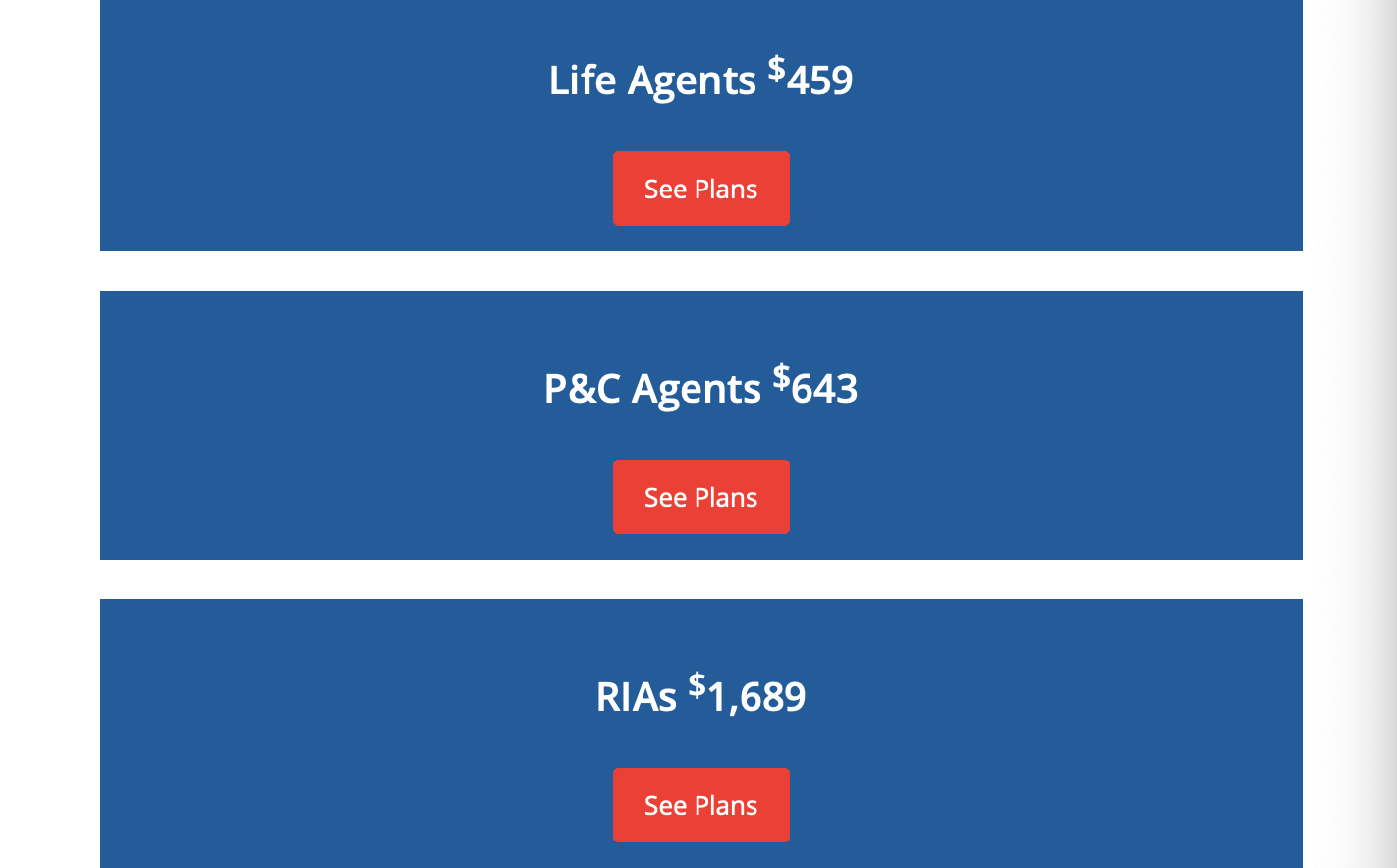

The median annual cost of an errors and omissions policy for insurance agents is $710 a year, or about $60 a month.

In the 5 top companies offering this insurance for insurance agents that we are able to get quotes, the costs range from $40 to $80 a month.

You should always compare quotes from 2-4 companies to select the best one. Shopping with a digital broker like CoverWallet or Simply Business is an easy way to compare quotes from several companies.

>>MORE: Errors and Omissions (E&O) Insurance Costs by Professions

>>MORE: Where to Get No Down Payment Errors and Omissions (E&O) Insurance?

How to Find Cheap E&O Insurance for Insurance Agents?

It is essential to maintain your E&O insurance policy while working as an insurance agent. Maintaining your policy consistently will help reduce the cost of your policy when you renew. Don’t let your policy lapse. Otherwise, you may see an increase in premium when you renew.

The longer you work as an insurance agent with a clean track record, the more affordable your E&O insurance policy will be. On the other hand, the more claims and lawsuits you have from your clients, the more expensive your E&O policy will be.

Last but not least, in order to get a cheap E&O insurance policy, be sure to shop around with a few companies or with a digital broker like CoverWallet or SimplyBusiness so that you can compare several quotes before selecting the final one for you. Comparing quotes is the only way to make sure you get the cheapest one.

Cheap E&O Insurance for Life & Health Insurance Agents

Life & Health insurance agents are required to have E&O insurance before they can work. Most brokerage firms and agencies require life & health insurance agents to show their E&O insurance proof, or certificate of insurance, before allocating new business opportunities to them.

Compared to property & casualty or P&C insurance agents, life & health insurance agents usually pay less for their E&O insurance policies.

When buying E&O insurance, life & health insurance agents should be clear about their coverage scope, ie. insurance lines that they sell, to make sure they can get the cheapest price. For example, if a life & health insurance agents only focus on selling medicare insurance only, he needs to make it clear so that he can get the cheapest E&O insurance policy.

The cost of E&O insurance for life & health insurance agents increases when they add more insurance lines to their portfolio: medicare only, and then medicare and life and health insurance. If they add annuities to their portfolio, the cost will increase; and the most expensive premiums are for agents who also sell mutual funds and variable policies. So, even if your licenses allow you to sell mutual funds and variable life insurance policies, but you don’t actively sell these policies, you shouldn’t take it out of your portfolio when buying an E&O policy so that it costs you less.

Lastly, the only way to make sure you get the cheapest E&O insurance is to compare quotes from a few companies or working with a digital broker like CoverWallet or Commercialinsurance.net to compare several quotes from their partners.

Cheap E&O Insurance for P&C Insurance Agents

Similar to Life & Health Insurance agents, P&C insurance agents are also required to show their E&O insurance proof before they can sell P&C insurance policies.

The coverage scope of P&C insurance agents, ie. the number of product lines they sell, affects the cost of their E&O insurance policy. To get a cheap E&O insurance policy, P&C insurance agents need to limit the insurance coverage scope to the only insurance lines that they are actively selling.

The E&O insurance cost will increase if a P&C insurance agent sells both personal and commercial lines. P&C insurance agents who sell personal and commercial and surplus lines will pay the most for their E&O insurance.

Lastly new agents, ie. having had their licensed for less than 2 years, will pay more for their E&O insurance than experienced agents.

Don’t forget to compare several quotes to choose the cheapest one for you. Working with a digital broker like CoverWallet or commercialinsurance.net is a good option. They are able to provide several quotes from their partners.

What should I Consider When Purchasing E&O Insurance?

Coverwallet says that the standard errors and omissions policy is $1,000,000 in coverage per claim. If you or your company earns more than $1,000,000 a year, you should get a higher limit.

Be sure to read your policy and know what is covered. You don’t want to be sued and then discover your limits are lower than you thought.

Last Thoughts

Insurance agents excel at providing coverage for their clients. Don’t forget to insure yourself as well. After all, mistakes can and do happen. They don’t even have to happen to you—your client could be in error and blame you for it. Errors and Omissions insurance will cover your legal costs if someone sues so you can focus on your clients.