Did you know: When you hire a nanny, you’re considered a household employer? The same is true for other household staff you hire to work in your residence.

Many think that nannies can be paid in cash and treated like a babysitter. However, many states have requirements that need to be followed when bringing a nanny into your home. Workers’ compensation insurance, which is generally required for office jobs, retail stores, restaurants, factories and other businesses, may be needed to cover your nanny, as well.

In this article, we’ll cover:

- The 6 best nanny workers’ compensation insurance companies

- What’s workers’ compensation insurance and what does it cover?

- What’s the difference between workers’ comp insurance and homeowners insurance?

- State requirements for workers’ compensation for nannies

- Why is workers’ compensation insurance so important?

- How much does workers comp insurance for nannies cost?

- How to get workers’ comp coverage for your nanny

- Nanny workers’ comp coverage: The bottom line

The 6 best nanny workers’ compensation insurance companies

We researched the companies that offer nanny workers’ compensation insurance to come up with our top six for different reasons.

- CoverWallet: Best for comparing quotes online

- Workers Comp For Nannies: Best for getting nanny coverage fast and comparing several quotes

- HomeStaff Protect: Best overall provider of nanny workers’ comp coverage

- ADPIA: Best for parents who need guidance on buying workers comp coverage

- GTM: Best for covering nannies along with other household employees

- Golden Global Insurance: Best for high touch customer service

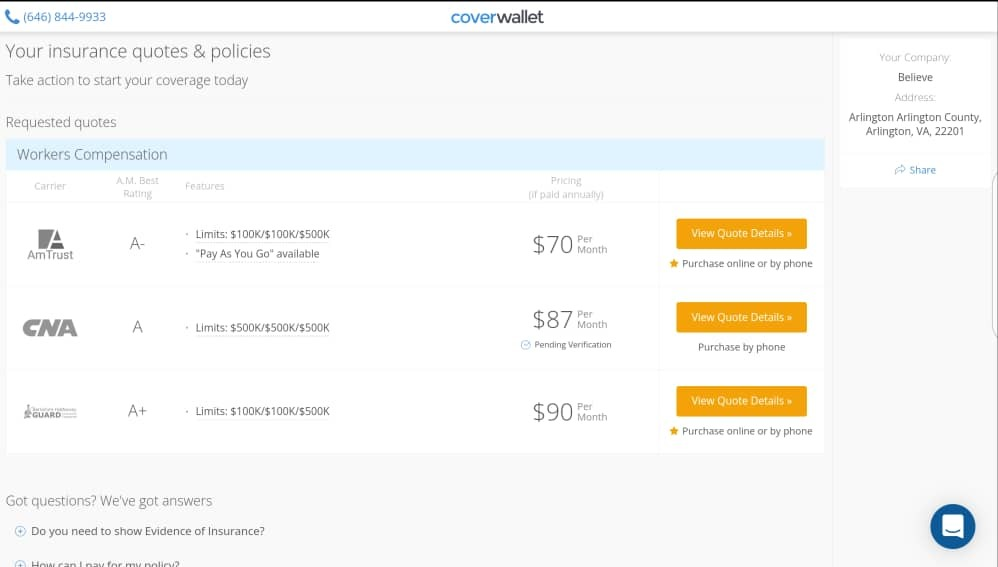

CoverWallet: Best for comparing several quotes online

CoverWallet is a leading digital broker. They work with several leading insurance companies. Workers comp insurance is one of their coverage focuses.

The advantage of working with a leading broker is that they can help you pull quotes from several companies to compare them in one place conveniently. Their quote form is very simple and straightforward. It shouldn’t take you more than 10 minutes to complete the quote form and see several quotes from the companies that they partner with. You can compare and buy a policy completely online.

After a buying a policy online with CoverWallet, it is also very easy to manage the policy using their digital dashboard.

CoverWallet is a digital-first broker. This means that if you want to talk to an expert, you can always give them a call to discuss your situation with an insurance expert on their staff. CoverWallet’s customer service team earn a good rating of A from BBB.

Below is an example of their quote result:

Workers Comp For Nannies: Best for getting nanny coverage fast and comparing several quotes

Have you hired a nanny and need workers’ comp coverage right away so she can start working immediately? Workers Comp for Nannies could be exactly what you need. The company is a broker specializing in providing workers comp insurance for nannies.

You simply provide the information required in an online form or over the phone and the service combs its database of nanny workers’ comp insurance providers in your state, and comes back with the best options for you. You can also compare several quotes from the carriers in their network to find the cheapest one. They are uniquely able to allow you to compare several quotes and supply same day insurance coverage thanks to a large carrier network that they work with.

You can rest assured knowing Workers Comp for Nannies is powered by The Insurance Shop, a national insurance agency licensed in all 50 states.

Similar to Workers Comp for Nannies, you can also consider other digital brokers to compare quotes such as CoverWallet, Simply Business, Commercialinsurance.com, or ez.insure

HomeStaff Protect: Best overall provider of nanny workers’ comp coverage

All Risks, Ltd. offers HomeStaff Protect, a specialized workers’ compensation insurance plan developed specifically for families with nannies. They have partnered with the Care.com HomePay payroll service and a highly rated insurance carrier to provide this vital protection for nannies and the families that employ them.

HomeStaff Protect makes it easy to get a quote. They have a simple online application process and are known for their expert claim support. If you’re looking for a company that specializes in workers’ comp coverage for nannies, HomeStaff Protect could be the right insurer for you.

Here’s an example of a premium quote from HomeStaff Protect.

ADPIA: Best for parents who need guidance on buying workers comp coverage

Automatic Data Processing Insurance Agency is an affiliate of ADP, the well-known payroll service provider. If you get your nanny workers’ comp coverage through ADPIA, you can expect to get help and guidance from experienced, licensed insurance agents, which can be reassuring to parents who don’t understand the ins and outs of the coverage.

You can also expect reliable service from experienced professionals whenever you need it. You’ll also have convenient access to your certificate of insurance 24 hours a day, 7 days a week and it’s possible to get same day coverage. Plus, you’ll have the option to pay your nanny through the ADP payroll service. The firm prides itself on helping hundreds of households secure the nanny workers’ comp coverage they need.

GTM: Best for covering nannies along with other household employees

GTM is another payroll service that offers workers’ compensation coverage for nannies and other household workers. Because the company is exclusively focused on this segment, it’s certified and licensed experts are able to provide the advice you need for your nanny and other household workers in your employ.

If you decide to partner with GTM, you’ll be able to take advantage of their payroll, accounting and tax services, developed exclusively for nannies and other household employees. Plus, experts are available to provide you with a complimentary, in-depth consultation about your family’s situation.

Golden Global Insurance: Best for high touch customer service

Golden Global Insurance prides itself on offering its customers knowledgeable advice and top level customer service. The firm makes it a point to be respectful of the customers they serve and to take time to understand their individual needs. What Golden Global Insurance lacks in size, it makes up for in personalized service.

If your main goal is to get the cheapest workers comp insurance policy for your nanny, be sure to shop around with a few companies or a digital broker like CoverWallet, Simply Business, ez.insure, or commercialinsurance.net to compare several quotes:

What’s workers’ compensation insurance and what does it cover?

Workers’ comp insurance typically helps protect businesses and their employees from financial losses when an employee is injured on the job or gets sick because of a work-related cause. For example, if a worker falls down while on the job and breaks a leg, a workers’ compensation policy will typically cover the injured employee’s medical bills along with a portion of their missed wages if they can’t go to work because of the injury. In the case of your nanny, he or she could trip and break an arm while out on a walk with your kids, get a dog bite while watching your dog or be injured in a car accident while out running errands for you. In these cases, nanny workers’ comp could cover medical care required because of the incidents, missed wages and other things.

Nanny workers compensation insurance protects the caregiver and the homeowner / employer from the expenses and liabilities associated with a work-related accident. A single incident could leave the homeowner liable for thousands of dollars or more in medical bills.

Did you know: Workers’ compensation insurance provides you with legal protection because when an employee accepts benefits from you, he or she generally forfeits their right to sue you?

What’s the difference between workers’ comp insurance and homeowners insurance?

Because a nanny works out of a home, many people believe that a homeowners policy would cover injuries or accidents that happen to them while at work, in the same way that it covers visitors and guests that are injured on the property.

However, while homeowners insurance covers injuries, it usually applies to people who don’t work for you that are on your property, whether it’s a visitor, salesperson or passerby. Because a nanny is considered to be your employee, homeowners insurance usually won’t cover any injuries he or she experiences while working at your home.

State requirements for workers’ compensation insurance for nannies

Similar to payroll and tax related issues, workers’ comp requirements for nannies vary by state. Most states require that you have coverage if you have an employee, even if it is a nanny. The same is true of senior caregivers and housekeepers. If your state does not require the coverage, if could still be a good idea to have it as a safety net for you and your nanny.

Based on our research, the following states require nanny workers’ comp coverage only for full time employees:

- Colorado: Regularly working 40 hours per week

- Illinois: Regularly working 40 hours per week

- Michigan: Regularly working 35 or more hours per week

- New York: Regularly working 40 hours per week and for live-in workers, no matter how many hours they work

- Utah: Regularly working 40 hours per week.

The following states require coverage for both full and part time employees:

- Alaska

- California: Working 52 or more hours per quarter.

- Connecticut: Regularly working 26 or more hours per week

- Delaware: Earning $750 or more per quarter

- District of Columbia: Working 240 hours or more per quarter

- Hawaii: Earning $225 per quarter

- Florida: Required if 4 or more full or part time household employees

- Georgia: Required if 3 or more full or part time household employees

- Iowa: Earning $1,500 per year

- Kansas: Total gross wages for all employees of $20,000 or more per year

- Kentucky: Required if 2 or more full or part time household employees

- Maryland

- Massachusetts: Regularly working 16 or more hours per week

- Minnesota

- Mississippi: Required if 5 or more full or part time household employees

- New Hampshire

- New Jersey

- Ohio: Pays wages of $160 or more per quarter

- Oklahoma: Pays wages of $10,000 or more per year

- South Carolina: Required if 4 or more full or part time household employees

- South Dakota: Employed more than 20 hours per week for 6 or more weeks

- Virginia: Required if 3 or more full or part time household employees

- Washington: Required if 2 or more full or part time household employees

Coverage is voluntary in the following states:

- Alabama

- Arizona

- Arkansas

- Idaho

- Indiana

- Louisiana

- Maine

- Missouri

- Montana

- Nebraska

- Nevada

- New Mexico

- North Carolina

- North Dakota

- Oregon

- Pennsylvania

- Rhode Island

- Tennessee

- Texas

- Vermont

- West Virginia

- Wisconsin

- Wyoming

Check with your state and insurance provider to see if you need workers’ comp for your nanny. State laws change all the time and you’ll want to ensure you base your decision on the most current information.

Why is workers’ compensation insurance for nannies so important?

Families that don’t have workers’ compensation insurance coverage for their nanny take on significant risk if there is ever an on the job injury. They may have to pay out-of-pocket for the nanny’s medical expenses and lost wages if they are unable to work.

How much does nanny workers comp insurance cost?

The cost of workers comp insurance for nannies varies, depending on several factors such as your location, your nanny’s age, your nanny’s years of experience, how long your nanny has been with you, etc.

On average, nanny workers comp insurance costs $70 to $120 a month, or $840 to $1,440 a year.

Different insurance companies have different quotes. If you want to get the cheapest one, be sure to shop around with a few companies or a digital broker such as CoverWallet, Simply Business, ez.insure, or commercialinsurance.net, etc. to get compare several quotes:

>>MORE: How Much does Workers Comp Insurance Cost?

How to get workers’ comp coverage for your nanny

The easiest way to get coverage is through the company that provides your homeowners and auto coverage. Check with them to see if they offer workers’ comp coverage for nannies and other home-based employees. If they do, you may find that you qualify for a discount for bundling your coverage.

You can also check out the specialized services we rated earlier in this article. Three of them are affiliated with payroll, tax and accounting services for nannies and other household employees. It might be better and cheaper for you to get these services bundled together along with the workers’ comp coverage.

If you’re already working with a payroll service, check with them to see if they can provide you with coverage.

If you’re finding it impossible to secure nanny workers’ comp insurance and if your state has a state fund for workers’ compensation, you maybe able to obtain coverage from it, although it may be more expensive than through an insurer.

>>MORE: The Cheapest Workers Comp Insurance Companies

Nanny workers’ comp coverage: The bottom line

Hiring nannies and other household employees isn’t as easy as many people think.

The most important thing to keep in mind is that you are considered an employer when you hire a nanny or other household help. It’s critical that you protect your nanny and your family in the same way other employers protect their employees and businesses. Workers’ compensation is a win-win for all parties involved because you’ll be covered should an accident happen, and your employee can rest assured knowing they are protected, as well.