Hair salon insurance is an important investment for any salon owner. It helps protect you in various situations, including providing necessary coverage in the event of an accident at your hair salon.

For a hair salon owner, it’s critical to understand the differences between the various types of business insurance coverage. It’s also critical to understand the various coverage types you require to safeguard your company, clients, investments, and employees. This guide will teach you everything you need to know about salon insurance.

- 5 best hair salon and hair stylist insurance companies

- What kinds of insurance does a hair salon need?

- What does hair salon business insurance cover?

- How much does hair salon insurance cost?

- How to find cheap hair salon insurance?

- Who needs hair salon insurance?

5 best hair salon and hair stylist insurance companies

- InsurePro: Best for cheap on-demand insurance

- Simply Business: Best for new salon owners and new stylist

- CoverWallet: Best for comparing several quotes online

- Thimble: Best for flexible short-term coverage

- NEXT: Best for a great digital experience and affordable rates

Insurepro: Best for cheap on-demand insurance

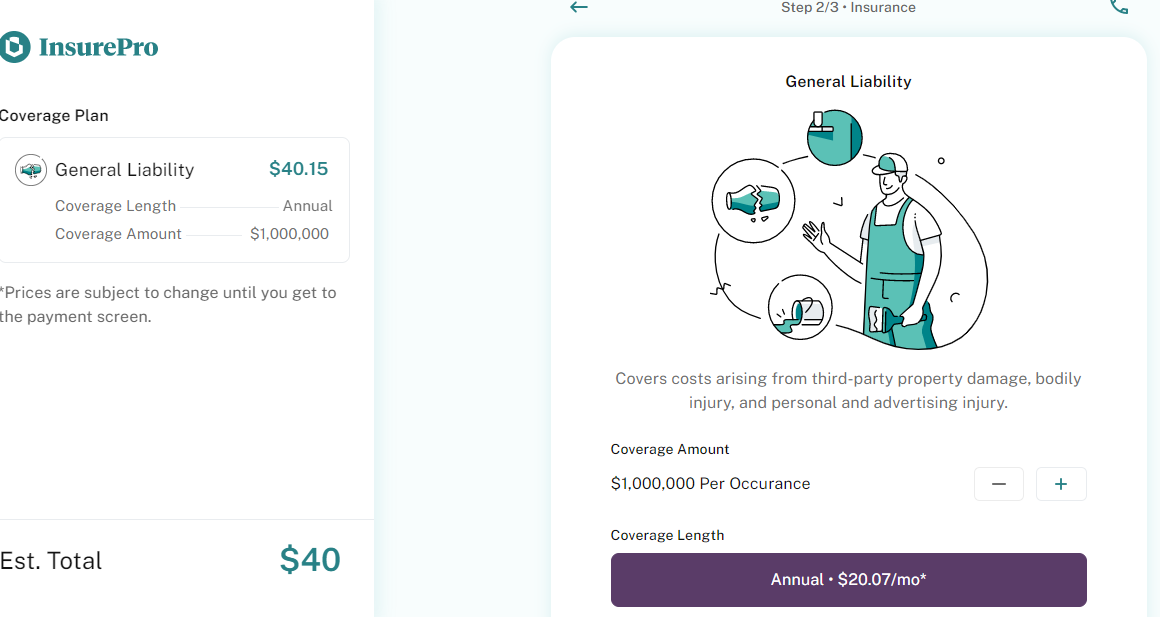

Insurepro offers insurance on demand for hair salon owners in the US. That means, with the company, hair salon owners can buy policies to protect their businesses only when needed. The company works with over 20 partners to help clients find the best policy. You may find your quotes in 5 minutes or less using their website. Even though they are new, the company has offered their top-notch service.

The following is a sample quote for a hair salon in Georgia from Insure Pro.

Pros

- Makes it easy to shop for insurance

- Quotes are available when you need it

- Access to over 20 insurance partners

Cons

- Relatively new company

Simply Business: Best for new salon owners and new stylists

Simply Business is a digital insurance broker that works with top insurers to provide quotes for small businesses nationwide. Their system and operations are small business-friendly, especially for new buyers.

They also have a team of agents that educate small business owners about insurance coverages and other important insurance related-topics. They will recommend the cheapest policy for your salon when you use their service. Plus, their service is available to almost all small businesses.

Pros

- The process for obtaining a quote is fast and easy

- To assist you, licenced agents are available.

- You have the option of selecting from several reputable insurance companies.

Cons

- Their customer service helpline’s opening hours are inconsistent.

CoverWallet: Best for comparing several quotes online

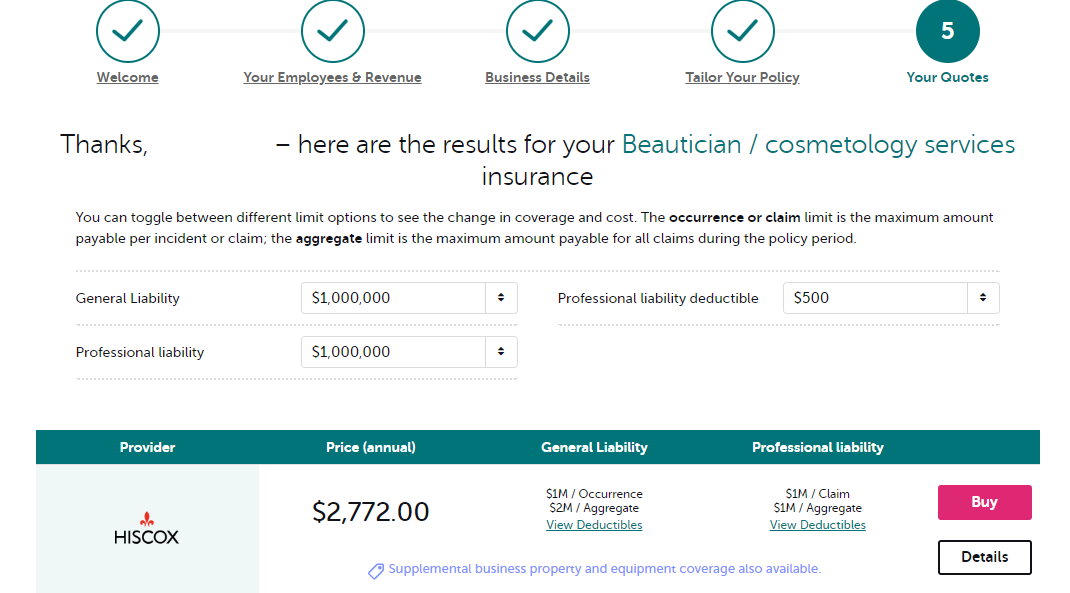

Because it acts as an online broker, CoverWallet can generate multiple quotes from various highly accredited carriers at once, making it a viable alternative to traditional insurance companies. Hair salon owners can shop and buy all lines of standard and specialized coverages based solely on coverage and premiums available on the market, thanks to the impartiality and volume of insurance company partnerships that CoverWallet has.

Pros

- Simple to use

- Quotes are available for no cost.

- Insurers from a wide range of companies are compared.

Cons

- Customer service is slow.

- Quotes don’t always appear right away.

- Only partners can provide insurance.

Here is the quote we receive from CoverWallet for a hair salon located in Miami, Florida. As you can see, CoverWallet provide several quotes from their carrier partners, making it easy for us to compare them in one place.

Thimble: Best for flexible short-term coverage

Even though Thimble is relatively new in the industry, they are the pioneer of flexible, short-term insurance coverage. Small hair salons with one stylist can buy coverage from Thimble for a few days to start or even buy their policies when they need it.

This is useful for salons open a few days a week and can save you a lot of money. One policy can cover your salon’s essentials. General, professional, and equipment liability are covered.

Pros

- In minutes, you can get a quote and buy insurance online.

- Coverage is available on a monthly, daily, and even hourly basis.

- Reliable customer services

Cons

- You must submit claims to the insurance company that underwrites the policy via email or phone.

NEXT: Best for a great digital experience and affordable rates

NEXT is a newer insurance company, or an insuretech. Unlike other established insurance companies, NEXT is digitally savvy. They built an excellent digital experience. Working with NEXT means that you are buying and managing your insurance policies just like you are buying stuff from Amazon. Everything is online, fast, and simple. Because of that, NEXT decreases their cost of operations and is able to reduce their prices, making their rates more affordable.

Pros

- Fast, simple, and affordable quotes

- Buying and managing the policy completely online

- Coverage available for both the hair salon owner and hair stylists

- A.M. Best gave it an A (Excellent) rating.

Cons

- In some states, key policies are not available.

- Online quotes are only available for BOP, general liability, and professional liability.

What is hair salon business insurance?

Hair salon owners must protect themselves, their employees, and their customers from liability, accidents, and damage by ensuring their salon. Many things can go wrong in your salon, so it’s critical to safeguard against potential losses.

What kind of insurance does a hair salon need?

Commercial Property Insurance, General Liability Insurance, Professional Liability Insurance, and Workers’ Compensation Insurance are all required for a typical salon. Some insurers may offer a Business Owner Policy, a package of insurance policies designed specifically for business owners and a more cost-effective option.

The following is an explanation of the popular coverages under this policy

Hair salon business property insurance

This policy is designed to protect the property that hair salons own and use daily. Commercial insurance covers the structure and the tools and equipment you use to provide services. If you rent your salon, your landlord will require this coverage.

Learn more at commercial property insurance cost and the best commercial property insurance companies

Business owners’ policy (BOP) for hair salon business

This is a package that includes both general liability and property insurance. It protects you from various perils and threats, such as damage to personal property, equipment, and employee theft. Getting a BOP, instead of two separate policies, will save you money.

Learn more at BOP insurance cost and the best BOP insurance companies

Professional liability insurance for hair salon businesses & hair stylists

Hair salons will be covered by professional liability insurance if one of their employees makes a mistake that causes a client or customer to suffer losses or damages. You won’t have to worry about covering for claims made by a client if they are injured while having their hair styled if you are insured in this way.

This coverage is necessary for both hair salon owners and hair stylists. If you work at a hair salon and the owner doesn’t provide this coverage. As a hair stylist, you need to get this coverage for yourself.

Learn more at professional liability insurance cost and the best professional liability insurance companies

Hair salon business workers’ compensation

Workers’ compensation is intended to protect your hair salon’s employees, as the name implies. Workers’ compensation covers claims made by injured or ill employees who require time off from work.

Hair salon owners are not required by law to provide this coverage to their stylists if their hair stylists are independent contractors. However, hair stylists can still get this coverage on their own to protect them from accidents and injuries at work. Learn more at the best workers comp insurance for independent contractors.

Business income insurance for hair salon businesses & hair stylists

This type of commercial insurance will cover you if your business’s income levels drop or your financial situation is harmed as a result of things like crimes or natural disasters, such as an earthquake that disrupts your operations.

Learn more at workers comp insurance cost and the best workers comp insurance companies

What does hair salon business insurance cover?

To understand what a salon business insurance covers, consider the following situations:

- In your hair salon, a customer trips and falls at the shampoo station, breaking his ankle.

- As part of your spa package, you provide professional advice that causes a client injury.

- During treatment, one of your hair stylists destroys your client’s expensive shoes.

- In your hair salon, an employee was hurt.

You’ll agree that things like this can happen at any time. You must ensure that your salon, employees, and clients are safe from the effects of such events.

How much does hair salon insurance cost?

The average cost of hair salon general liability insurance ranges is $36 per month, or $432 per year. Small hair salon owners pay between $24 to $300 per month, depending on several factors. And this is the cost for a general liability policy only. If hair salon owners add more coverage, they’ll pay more. Below are the average costs for different policies:

| Hair salon insurance coverage | Average costs |

| General liability insurance | $36 per month |

| Professional liability insurance | $42 per month (per stylist) |

| Commercial property insurance | $127 per month |

| Workers comp insurance | $82 per month |

| Business interruption insurance | $25 per month |

Keep in mind that these are just the averages that thousands of hair salon owners pay for their insurance policies. Your rates will be different. Be sure to shop around with a few companies or work with a top broker like Simply Business, InsurePro, or CoverWallet to compare several quotes to find the cheapest one for your hair salon.

What factors affect hair salon business insurance cost?

The following are some factors that may affect the cost of hair salon business insurance.

Coverage amount

If you require more coverage, you will typically be required to pay a higher monthly or annual premium.

Revenue

Because they have more to lose, salon businesses that generate much revenue usually have to pay higher premiums.

Services

The types of services you provide can impact the premiums you must pay, as some services are considered riskier and more likely to result in claims. For instance, companies that do tanning may pay more for their insurance.

Employees

s maaThe number of employees you have and the types of employees can affect your premium. More employees mean more risk and also equals higher premiums. However, if your staff are well trained, you may reduce your premiums.

Location of business

Salon owners’ costs may be influenced by their location. Some areas, for example, have high crime rates, resulting in higher premiums. Alternatively, renting an older building may be higher due to the risk of structural damage.

Type of business

Different types of businesses have different prices. If you need insurance for your home salon, the costs might be lower than if you had a full-service salon with many employees.

How to find cheap hair salon insurance?

While it is important to have insurance, some salon owners may feel the cost is too high. The following steps will ensure that you don’t overpay for your coverage and get insurance at the best price.

Check for the best price in the market:

One thing about insurance like you saw above is that price varies from one company to another. So, to ensure you are getting the best value, you need to check as many companies as possible. Even after you have gotten a company, it is important that you still check for better prices every year when you renew your policy. You may even ask other salon owners around you to see if their insurer gives good prices.

Discounts

Most insurers offer discounts for their products. Depending on the company or the insurance package, the discount could be 10 and 20%. So, when you buy any insurance package, ask if you qualify for any discount.

Commit to safe working conditions

Safety is one critical factor that determines your insurance premiums. Salons that pay attention to safety tend to pay less. You can encourage safety in your salon by providing “injury-free” incentives to workers, train staff and managers to recognize signs of pain in their employees, and coach them on ergonomic self-care.

Who needs hair salon insurance?

Hair salon insurance is a must if you own a small hair salon because you can be sued as a business owner even if you have done nothing wrong. A client may hold you liable as a salon owner for a bad haircut that causes serious injury to the client’s scalp or even slips and fall injuries to your customers. Hair salon insurance is the best way to safeguard yourself.

Salon owners that provide facial, hair, nail and body treatments, as well as a variety of other spa services, should consider this policy.

What is not covered by hair salon insurance?

The insurer decides what they will cover and what is not covered. Therefore, you must read the terms of your policy before purchasing. However, most standard policies will not cover the following:

- Services for tanning

- Services for airbrushing

- Electrolysis

- Hair transplantation and implanting

- Services for eyelash dyeing or colouring

- Services of a massage therapist

- Services for red light therapy

Insurance for hair stylists renting a chair in a hair salon

If you are a hair stylist or hair dresser renting a chair in a hair salon, you will definitely need insurance to protect yourselves. Actually, most hair salon owners require you to have insurance before agreeing to rent a chair to you. Your insurance needs are different from hair stylists working for the salon. Learn more about your insurance needs and where to get the insurance for yourself.