The front end of most restaurants generally looks calm and under control. Behind the scenes, the picture is vastly different. It’s often frantic, fast paced, and a stress bomb ready to go off at any time. The crazy pace in the kitchen, storage spaces, and loading areas of restaurants fosters an environment where injuries happen all the time.

According to the U.S. Bureau of Labor Statistics, workers in full-service restaurants were involved in 93,800 nonfatal work related injuries and illnesses in 2019, the most recent year data is available. About one-third of these cases required at least one day away from work for recovery. The incidence rate of cases that required taking days away from work for full-service restaurants was just over 88 cases per 10,000 full-time workers. The rate in 2018 was just over 73. For all private industry workers, the rate was almost 87 in 2019 and 90 in 2018.

The most common employee injuries in restaurants include:

- Cuts from knives, kitchen equipment, and broken or chipped tableware

- Burns from hot liquids and oil, chemicals, plates, stoves, and ovens

- Slips and falls because of wet and slippery floors

- Strains from lifting and carrying things

- Food delivery and catering related auto accidents.

Injuries often leave restaurants short-staffed, which is a particularly big challenge at a time when it’s difficult to find servers and other employees. In addition to protecting restaurant owners from being sued by employees over workplace injuries, workers’ comp provides benefits that can get them back to work more quickly.

In this article, we’ll cover:

- 5 top workers compensation insurance companies for restaurants

- Do all restaurants need workers’ comp coverage?

- What does restaurant workers compensation insurance cover?

- How can restaurants prevent employee injuries?

- How much does workers compensation insurance cost?

- How to find cheap workers compensation insurance

5 top workers compensation insurance companies for restaurants

Here are our 5 best workers comp insurance companies for restaurants for different reasons:

- CoverWallet: Best for restaurant owners looking to compare quotes quickly and easily

- Cerity: Best for stand alone workers’ comp coverage for restaurants

- Employers: Best for restaurant workers’ comp coverage backed by experienced professionals

- biBerk: Best for low cost workers’ compensation coverage

- AmTrust Financial: Best for restaurants that need customized coverage

CoverWallet: Best for restaurant owners looking to compare quotes quickly and easily

CoverWallet is a next-generation, yet highly-experienced, insurance provider. The company has developed their own state-of-the-art platform, using algorithms generated by the people who work for it, to ensure it’s able to supply small businesses with the workers comp coverage they need at the best possible price. The platform makes it fast and simple to get quotes from several providers, allowing restaurant owners to compare quotes on a single screen.

More good news: You only have to answer the questions about your restaurant — and provide the information required — to generate quick and accurate quotes. You don’t have to waste time inputting things that don’t impact your premium cost. The entire process should take less than ten minutes from beginning to end. If your situation isn’t complicated, it could take less than five.

You can rest assured knowing that CoverWallet is a part of Aon, a well-known company that provides advice to businesses on things like risk, health and retirement.

Once you get your quote, it’s easy to purchase a policy online or through an agent. When you get your workers’ comp coverage through CoverWallet, it’s simple to manage your policies online, including doing things like downloading a certificate of insurance, filing a claim, renewing your policy, and more.

In addition to all this, you can get other types of coverage through CoverWallet, so you can secure and manage all your small business coverage through a single provider.

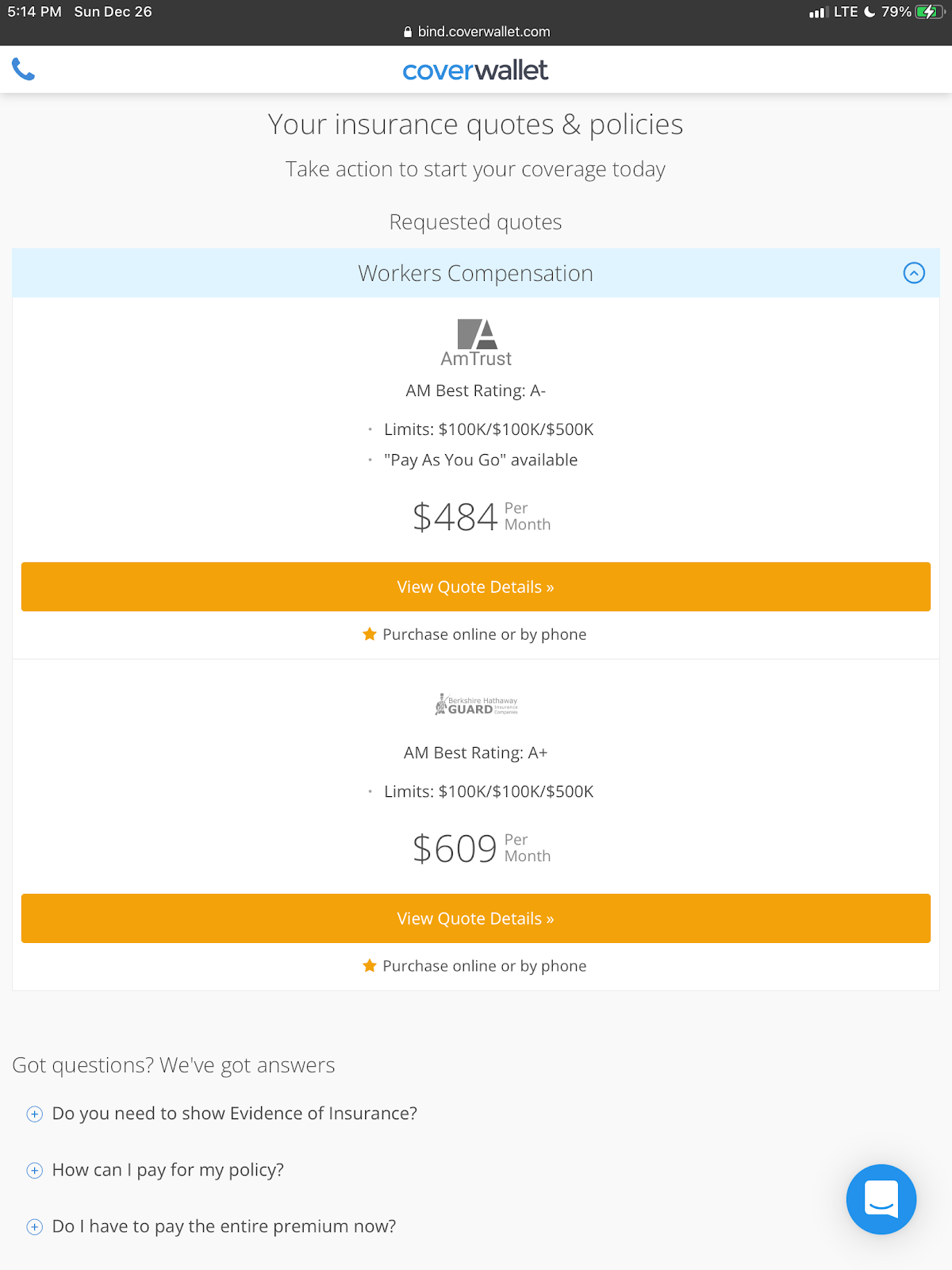

Where is a sample restaurant workers’ comp quote from CoverWallet

Cerity: Best for stand alone workers’ comp coverage for restaurants

Cerity makes our list of top workers’ compensation providers because it specializes in the coverage. It currently does not offer a Business Owners Policy or other types of insurance. It’s a relatively low cost provider, yet delivers a high level of service. Policies start as low as $25 per month and the company has fewer fees than most insurers. Cerity makes it fast and easy to get a quote online.

Cerity isn’t low cost because it cuts corners. It actually uses artificial intelligence to up its efficiency. However, everything at Cerity isn’t technology based. When you require help, you will have access to a team of licensed policy and claims experts. You can rest assured knowing Cerity has been in business for more than a century and is rated highly by their clients.

Employers: Best for restaurant workers’ comp coverage backed by experienced professionals

Employers has agents all over the United States that can connect you with the workers’ compensation insurance you need to cover your workforce. The company only offers workers’ compensation insurance targeted to the needs of independent small businesses, including restaurants. Employers dates back to 1913 and is known for its extensive experience in the workers’ comp space, financial stability, knowledge base, and resources.

Employers goes above and beyond by offering 24 / 7 claims service, solid fraud prevention and loss control services, managed care support, a pay-as-you-go program, and an industry-leading return to work program.

If you decide to work with Employers, you can rest assured knowing you’ll have a good experience.

biBerk: Best for low cost workers’ compensation coverage

biBERK is Berkshire Hathaway’s low-cost workers’ comp insurance provider. Even though you’re saving money on your coverage with biBerk, you can rest assured knowing you are still getting quality protection for your employees. biBERK is able to lower workers’ comp insurance costs by approximately 20 percent because it insures small businesses directly, without the added costs of having to work through a middleman or insurance broker.

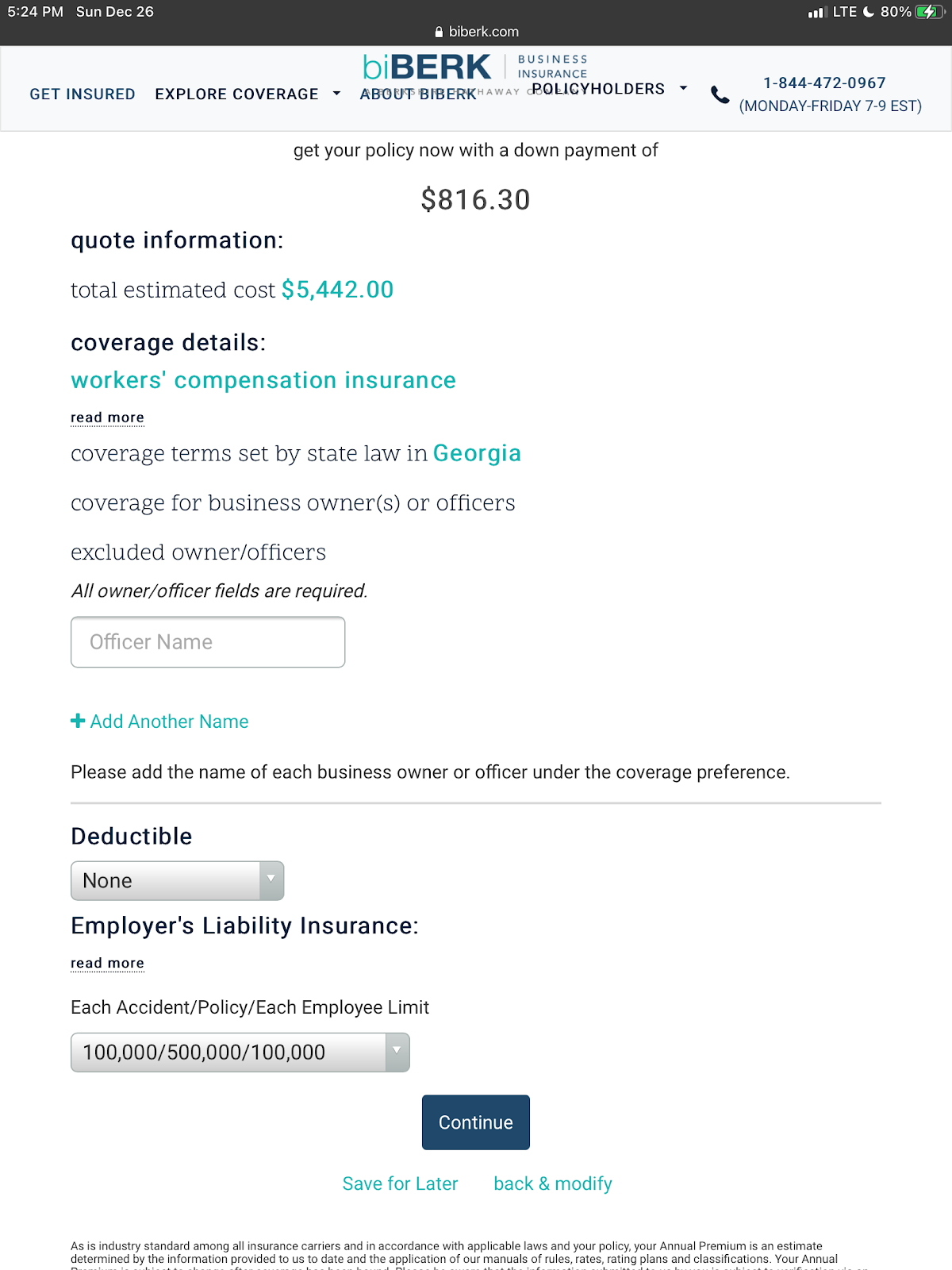

Here is a sample restaurant workers’ comp quote from biBerk.

AmTrust Financial: Best for restaurants that need customized coverage

AmTrust is an insurance provider that specializes in small business and workers’ comp coverage. It is known for its high level of service and willingness to work with businesses to help them get the coverage they need.

AmTrust and their agents make it possible for small businesses to customize their coverage based on their individual requirements, something many insurers are unable to do. The firm works closely with their agents to design the individual insurance packages businesses need.

AmTrust has excellent customers service ratings and their coverage is surprisingly affordable especially when you consider the level of customization they offer.

Do all restaurants need workers’ comp coverage?

Owning and running a restaurant without providing workers’ compensation insurance coverage is illegal in all states except Texas. Visit your state’s workers’ compensation agency or bureau website to learn about your requirements for coverage.

If you don’t have coverage when it’s required, it could result in severe penalties, ranging from significant fines to stop work orders all the way up to prison terms.

Regardless of the state government requirement to secure coverage, having workers’ compensation insurance is always a smart business move. It protects restaurant owners from potentially costly employee lawsuits and settlements. As an added benefit, restaurant owners can usually deduct their workers’ compensation premiums from their federal taxes.

What does restaurant workers compensation insurance cover?

Worker’s comp helps cover:

- Accidents and injuries: Workers’ compensation pays medical costs if an employee gets injured on the job

- Illness: If a worker is exposed to harmful chemicals or allergens in the workplace that cause an illness, their medical care is covered by workers’ comp

- Lost wages: A work-related injury or illness often forces employees to take time off. Workers’ comp helps replace the lost wages of injured or sick employees while they’re recovering

- Ongoing care: If a workplace injury or illness requires an employee to get ongoing care, such as physical therapy, workers’ compensation will pay for the treatment

- Funeral costs: If an employee passes away because of a work-related incident, workers’ comp pays funeral costs up to a certain limit

- Repetitive injury: If a worker is injured because of ongoing repetitive job related strain, such as carpal tunnel syndrome, workers’ comp will pay for therapy

- Disability benefits: If an injury is so severe an employee never returns to work, or doesn’t for a long time, workers’ comp will pay medical costs and some lost wages over the long term.

What doesn’t workers compensation insurance cover?

Workers’ compensation insurance does not cover things like:

- Injuries to independent contractors, clients, or customers

- Employees who are intoxicated or high when they’re injured

- Wages for temporary employees while recovering from a work-related injury

- OSHA fines

- Injuries that occur after an employee has left work

- Vandalism or intentional injuries.

How is workers compensation insurance different than general liability insurance?

Workers comp only covers people who work for you. If a client, customer, or random person is injured at your workplace or job site, general liability insurance will cover it. General liability covers bodily injury and damage caused by you or an employee to someone else’s property.

How can restaurants prevent employee injuries?

Of course, it’s necessary to do everything possible to prevent restaurant accidents from happening in the first place. It’s the reason most workers’ comp insurance providers offer loss control services to help restaurant owners limit risk, build a safety culture, and create safer work environments by:

- Evaluating restaurant operations and making recommendations to control hazards

- Providing management, supervisory, and employee education programs to help support sound health and safety practices.

Restaurant owners can proactively:

- Identify potential hazards. Prevent slips and falls by making sure floors are clean and clear of liquids and grease. Require employees to wear closed-toe shoes with slip-resistant soles. Avoid burns by enforcing the use of personal protective equipment (PPE), including safety gloves, mitts, and aprons. Reduce knife injuries by making sure kitchen staff understands safe knife handling techniques, always use sharp knives, and wear cut-resistant safety gloves. Mandate that cleaning staff members wear PPE when handling dangerous cleaners and disinfectants. Encourage employees to use proper lifting techniques to avoid back injuries.

- Provide ongoing training for all employees. Everyone — no exceptions — should receive training on how to handle equipment safely and prevent injuries to themselves and others.

- Keep all facilities clean and organized. Keeping the restaurant clean and clutter free is the best way to help reduce the chance of workplace accidents, such as slips, trips, and falls.

- Maintain equipment. Dishwashers, refrigerators, ovens, slicers, blenders, and coffee makers must be regularly checked, well-maintained, and have guards in place. It’s a sure way to prevent employee injuries.

Fostering safe restaurant working conditions can help prevent employee injuries and lower your workers’ compensation insurance premiums.

How much does workers compensation insurance cost?

The only way to know for certain is to contact insurance agents or workers’ compensation insurance carriers who will review the business and its location(s) so they can come up with a premium for coverage.

The cost of your workers’ comp premium is based on a number of factors, including your:

- Number of employees and size of payroll

- Type of restaurant

- Workplace risks

- Restaurant claims history

- Business location

- Business age or years in operation.

Taken together, all these things will determine your ultimate premium cost. Learn more about the cost and how to calculate workers comp insurance.

How to find cheap workers compensation insurance

In most states, except for Ohio, Wyoming, Washington, and North Dakota which require that businesses purchase workers’ comp through a state fund, restaurant owners are able to choose their own workers’ comp insurance provider. You owe it to yourself to compare coverage and costs from several insurers. They have different ways of calculating premiums and you will likely find a range of prices. You can select one that offers you the coverage you need at the best possible cost.

>>MORE: The Cheapest Workers Comp Insurance Companies

How do restaurant file workers’ comp claims?

When a restaurant worker gets injured on the job, he or she must inform the restaurant owner (if possible) and the restaurant’s workers’ compensation insurance provider about the injury and file a claim. If it’s a serious of life threatening injury, the employer should seek immediate emergency medical care for the employee. For less serious injuries, the worker should review the workers’ compensation poster displayed in the workplace which will explain how to file a claim and receive medical care if needed. Some states regulate the amount of time after an injury that the worker must seek medical attention, and whether treatment must be received from an approved doctor or facility.

If a claim is denied by the insurer, most states allow employees to make their case before a state workers’ comp or agency. Information about doing this will be available through their website.

Other insurance coverages that restaurants need

In addition to workers comp insurance, restaurants might need other business insurance coverages. Learn more about restaurant insurance in general. And below are the main coverages that restaurant might need:

- General liability insurance: which helps protect your business from claims of bodily injury and property damage that happen in your home while conducting business or while you and anyone employed by you is working. This includes things like client injuries that result from a slip and fall in your home when they’re visiting for business reasons or property damage that happens because of a work-related accident in a client’s home. Learn more at the best general liability insurance companies; and the cheapest general liability insurance companies.

- Commercial property insurance: which covers losses in your home workspace resulting from things like weather damage, fire, theft, or vandalism. Learn more at the best commercial property insurance companies

- Business Owners Policy: which bundles general liability and commercial property coverages in one single policy to make it simple for small businesses to manage their insurance needs. It also helps save money by bundling several coverages in one policy. Learn more at the best BOP insurance companies.

- Employment practices liability insurance: or also called EPLI protects employers against claims made by their employees for things like discrimination, sexual, and other types of harassment, or wrongful termination. It is getting more and more popular among restaurants to have claims and lawsuits from their employees for these matters.

- Commercial auto insurance: which pays for damage to vehicles and the cost of medical care if you or an employee is involved in an accident while driving for work related reasons. Similar to a homeowners policy, your personal auto insurance will not cover accidents that happen while conducting business. Learn more why small businesses need commercial auto insurance; the best commercial auto insurance companies; and how to find cheap commercial auto insurance.