There are actually many different types of jobs that fall under the heading of “independent contractor”. An independent contractor could actually be anything—a freelance writer, data entry specialist, computer consultant, tax accountant, or a writer, etc. They all need some sort of independent contractor insurance.

The pandemic caused many formerly employed people to strike out on their own and either start their own businesses or enter the gig economy as freelancers. One of the many questions you may have is what kind of insurance you need. Are you an independent contractor? Do you need liability insurance? Here’s what you need to know.

- The 6 Best Providers of Independent Contractor Insurance

- What Insurance do Independent Contractors Need?

- How Much does Independent Contractor Insurance Cost?

- How to Get Cheap Independent Contractor Insurance Quotes?

The 9 Best Providers of Independent Contractor Insurance

Many insurance companies offer some version of independent contractor insurance. Let’s take a look at nine of the top companies for small business insurance.

- CoverWallet: Best for providing guidance on the types of insurance independent contractors need

- Simply Business: Best for Comparing Quotes Online

- Hiscox: Best for a Fast Quote

- Contractor’s Edge Insurance Services: Best for Specializing in Construction Industry

- AIG – American International Group: Best for Independent Contractors with Large Projects

- Liberty Mutual: Best for offering independent contractors with the flexibility of working with an agent or digitally

- Zurich: Best for independent contractors with projects outside of the US

- Next Insurance: Best for independent contractors in the gig economy

- Nationwide: Best for independent contractors who want to combine their personal and business insurance

CoverWallet – Best for providing guidance on the type of insurance independent contractors need

If you’re confused about what kinds of insurance you might need as an independent contractor, CoverWallet offers a free insurance assessment so you can make sure your business is covered. While an independent contractor who does construction work might need general liability, builders’ risk, workers compensation, E&O and professional liability insurance, a freelance writer might just need E&O insurance.

You can get many types of business insurance from CoverWallet, including:

- General liability

- Workers compensation

- Business owners’ policies

- Umbrella

- E&O

- Product Liability

- Business interruption

We requested a quote for a contractor who builds homes in Massachusetts. It also recommended we get workers compensation and commercial auto policies.

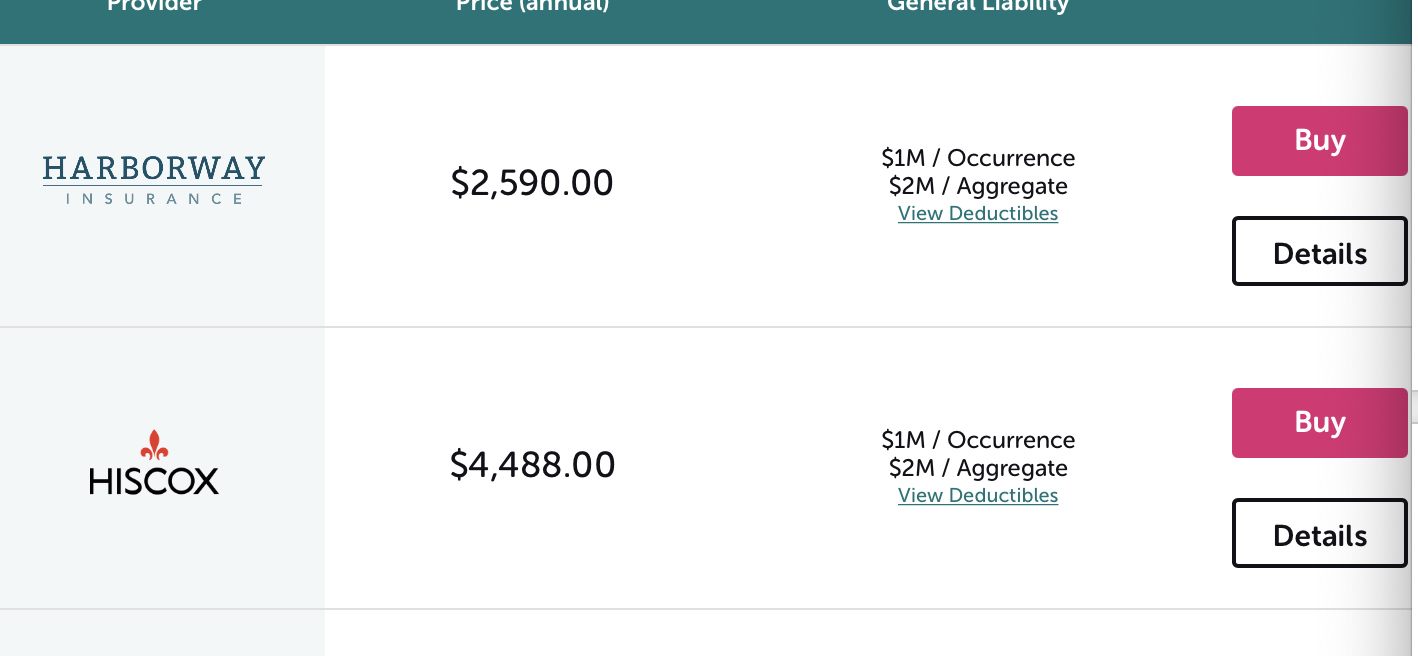

Simply Business: Best for Comparing Quotes Online

Simply Business is an insurance aggregator, culling quotes from different insurance companies so that you can compare. They work with 10 different companies, including Hiscox and Markel. They can also cover you no matter what sort of independent contractor you are, from photographers to construction workers to IT consultants.

They offer general liability, professional liability, E&O insurance, workers compensation and more. They can give you several quotes within just a few minutes.

This quote is for a handyperson living and working in Colorado.

Hiscox: Best for A Fast Quote

It’s easy to get a quote from Hiscox. When you enter your profession from the drop-down menu, they recommend business insurance you might need. For example, for a computer consultant in Connecticut, it recommended professional liability insurance, and then either general liability or a business owners policy.

The following a quote for a computer consultant from Connecticut.

Contractor’s Edge Insurance Services: Best for Specializing in Construction Industry

Contractor’s Edge is an insurance agency that specializes in the construction industry. They’re a relatively new start-up, springing up in 2014. They can offer you:

- General liability

- Commercial umbrella

- Workers’ compensation

- Commercial auto

- Inland marine/tool coverage

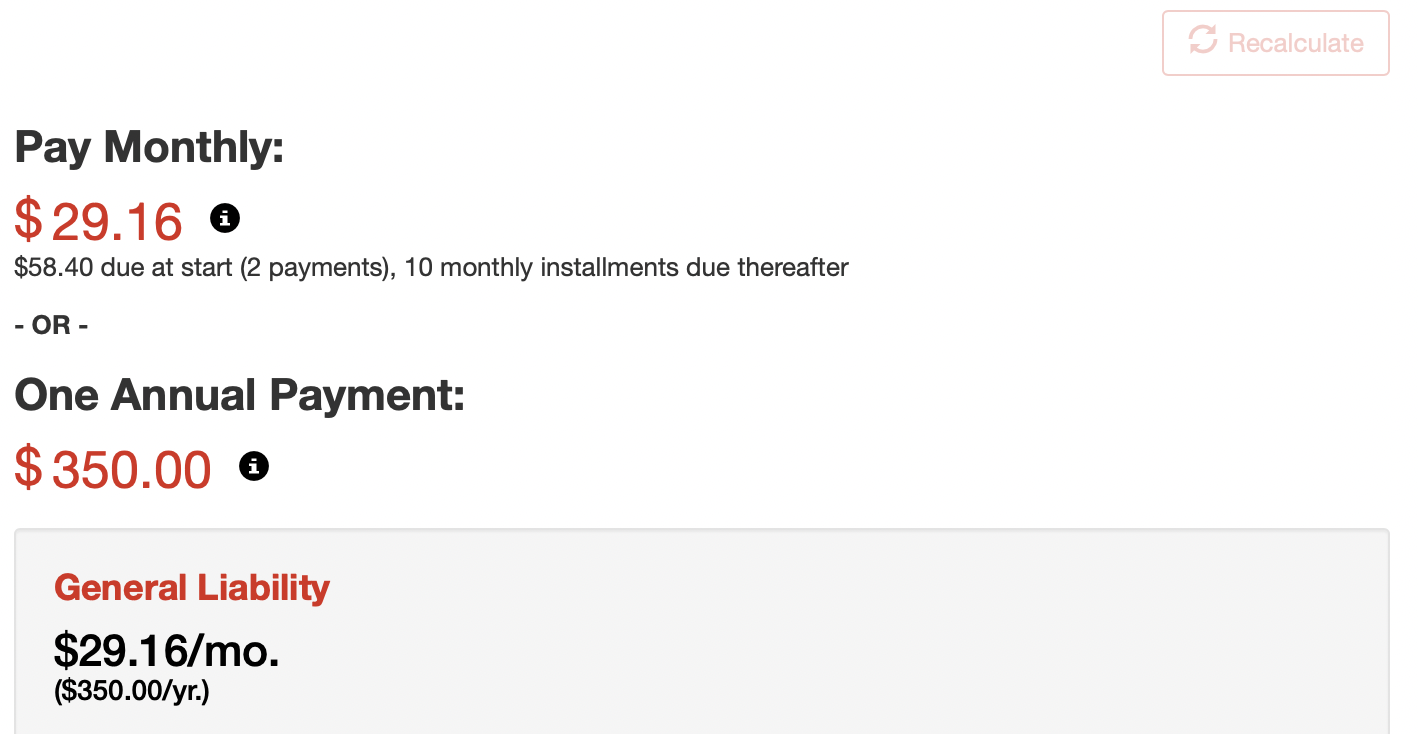

Contractor’s Edge was able to offer us a quote of $174 down, and $53 a month for the next 10 months for a $2,000,000 general liability insurance policy. If you pay in full, the cost is $656.

Most online reviews are positive, mentioning how fast and responsive they are. They are not accredited by the BBB. However, since they only serve contractors and construction industry professionals, they should be familiar with your needs. And it’s easy to get a quote.

AIG – American International Group: Best for Independent Contractors with Big Projects

AIG has been in business for a hundred years (established in 1919). They have a lengthy list of the types of insurance they can offer you, including general liability and commercial property insurance. They also have specialty policies such as cybersecurity insurance and management liability insurance. Whatever you need, chances are AIG can accommodate you.

AIG business insurance can be purchased through brokers or agents. How much you pay depends on the nature of your business, how much risk is involved, how many employees you have, and how much revenue you think you’ll earn.

They’ve been given an A- rating by the BBB, but they are not accredited by the BBB. If the BBB accredits a company, it means the company has agreed to abide by the ethical standards set forth by the BBB.

AIG is rated an “A” by A.M. Best for financial strength, so they do have the financial backing to follow up on claims.

AIG offers property casualty insurance, as well as Inland Marine, Surety, alternative risk and pollution liability insurance. Whatever your insurance needs, AIG has a policy for you.

>>MORE: Full Review of AIG Small Business Insurance

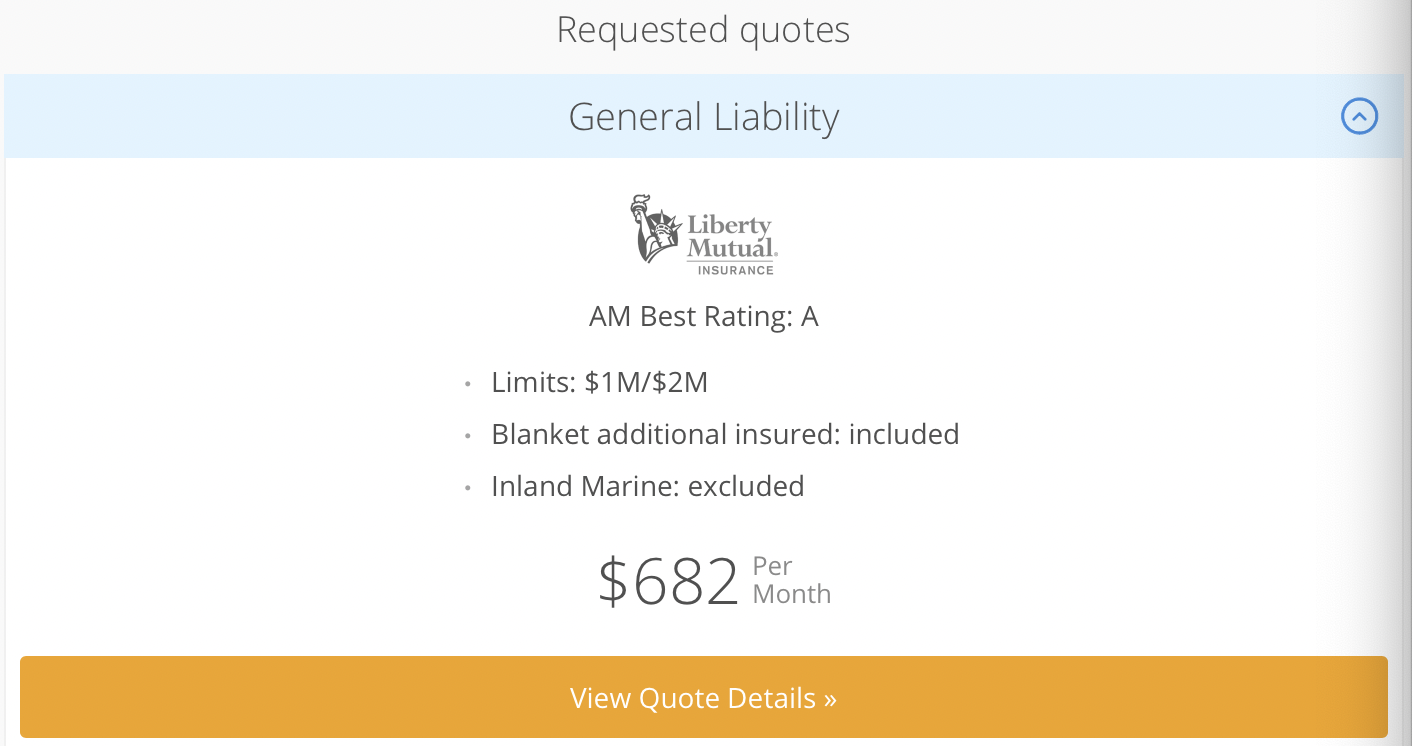

Liberty Mutual: Best for offering independent contractors the flexibility of working with an agent or completely digitally

Liberty Mutual offers insurance for whatever business you’re in, whether you’re in construction, healthcare, restaurants, or manufacturing. They have a network of independent agents, brokers and benefit consultants. Their goal is to know your business as well as you do, so that they can provide you with the business insurance you need.

You enter your information, and Liberty Mutual will create a list of 25 agencies or so that can provide a quote for you. Some people may find it helpful to speak with a live person about their insurance, as opposed to an app. If you prefer doing everything digitally, Liberty Mutual also offers a great digital experience from getting quotes online, buying and binding a policy, getting certificate of insurance, and managing your policy going forward.

Liberty Mutual has been in business for 107 years. They get an “A” rating from the BBB and are accredited. They also earn a score of A (Excellent) by A.M. Best. However, if you read the customer reviews on the BBB site, some of them report difficulty filing a claim.

Liberty Mutual offers many types of insurance policies, such as:

- Inland marine insurance

- Project-specific coverage

- Surety bonds

- Terrorism and sabotage

They do offer an online mobile app, which allows you to file a claim, pay your bill, and request roadside assistance (if you have regular or commercial auto insurance).

>>MORE: Full Review of Liberty Mutual Small Business Insurance

Zurich: Best for Independent Contractors Having Projects Outside of the US

As you might guess from the name, Zurich was founded in Switzerland in 1872. Zurich has been paying claims for 146 years and says they pay 99% of the claims filed. They have 500 claim experts in the United States alone, with an additional 400 of them located around the world. They offer:

- Commercial auto

- General liability

- Workers’ compensation

- Commercial Property

They also offer:

- Office contents insurance

- Business interruption insurance

- Equipment insurance

- Cybersecurity insurance

- Environmental insurance

They can’t offer you a quote, due to how many variables there are in formulating a quote, but you can go online and put in your information. Since they have an extensive international presence, be sure you are entering information for the country you reside in.

They only insure small business owners—no individual policies, so they should be able to meet your small business needs, especially if you do any business internationally. Their customer service reviews are mixed.

Zurich gets an A+ from the BBB and was accredited in 2017. They also get an A + from A.M. Best.

Next Insurance: Best for Small Independent Contractors in the Gig Economy

Unlike most companies on this list, if you put in the type of work you do and the state you do it in, Next Insurance will immediately spit out a quote. Example: Independent contractor, Massachusetts, $62.50 a month for general liability insurance. It’s probably only a ballpark estimate, but it’s still nice to have numbers. If you go through the whole survey, they will come back with three quotes for you to choose from.

They get an A + rating on the BBB website, and their reviews are positive. Customers praise how easy and fast it is to get insurance with Next, and they are happy with how affordable they are. Although they were launched in 2015, they have earned an A (Excellent) from A.M. Best.

Next offers general liability insurance, professional liability insurance, commercial auto insurance and workers’ compensation insurance. These are the basics. If your company needs specialized insurance, Next won’t be able to help you. Also, not every insurance they have is available in every state, so you’ll have to look into that.

Next is perfect for small independent contractors that earn less than $150,000 dollars in revenue each year and don’t need a lot of bells and whistles.

Nationwide: Best for Independent Contractors Who Want to Combine Personal And Business Insurance

Nationwide’s website is straightforward and easy to navigate. They offer all types of insurance, including home, auto, business, pet, renters, motorcycle and condo insurance. You could conceivably have Nationwide cover all of your personal and business insurance needs. As far as the business insurance end goes, they offer:

- General liability

- Commercial auto

- Professional liability

- Workers’ compensation

- Employment practices liability insurance

Nationwide ranks highest in overall customer satisfaction among small commercial insurance and performs highest in policy offerings, price and claims. (J.D. Power) It doesn’t do nearly as well with large commercial insurance. But if you’re a small business owner or independent contractor and you want to combine your personal insurance with business insurance in the same company, they might be perfect for you.

They also have a lot of online articles and guides to help you sort through what your insurance needs are. The online mobile app allows you to access your account from your phone, make a payment, or file a claim.

- What is an independent contractor? How does it differ from an employee?

- General Liability Insurance for Independent Contractors

- Workers’ Compensation Insurance for Independent Contractors

- Professional Liability Insurance or E&O Insurance for Independent Contractors

- Health insurance for independent contractors

- Unemployment insurance for independent contractors

- Disability insurance for independent contractors

- Do independent contractors need personal auto insurance or commercial auto insurance?

What is an independent contractor? How does it differ from an employee?

If you’re an independent contractor, you’re self-employed. According to the IRS, “an individual is an independent contractor if the payer has the right to control or direct only the result of the work and not what will be done and how it will be done. You are not an independent contractor if you perform services that can be controlled by your employer.”

As an independent contractor, you are responsible for your own Social Security and Medicare taxes, plus provide your own health insurance. You’ll also need to report all of your income to the IRS and submit self-employment taxes.

Almost anyone can be considered an independent contractor: doctors, dentists, contractors, subcontractors, actors, musicians, software engineers…the list goes on and on. Basically, if you work for yourself but supply goods or services to customers, you can consider yourself an independent contractor. Another word for it is freelancer.

If you are an independent contractor working in the construction field, you may also be called a subcontractor. You are also likely to work in the following fields:

- Handyman – The 5 Best Providers of Handyman Insurance

- Carpentry – 4 Best Providers of Business Insurance for Carpenters;

- Painting; Roofing — Four Best Roofing Insurance Companies;

- Plumbing; HVAC; Electrical wiring; Masonry; Concrete construction; Lawn caring; Appliance technician; etc.

How is an independent contractor different from a general contractor?

A general contractor outsources certain jobs to other entities (subcontractors) to perform certain jobs. For there to be a general contractor, there must be three parties involved: the customer, the general contractor and the subcontractor. For example, if you’re a general contractor, you work in construction. You are responsible for the coordination and supervision of the project, but you might hire subcontractors to do the plumbing and electrical wiring. If something goes wrong, it’s the general contractor’s job to fix it.

An independent contractor can work in any industry, as long as they are self-employed and work for themselves.

>>MORE: The 5 Best General Contractor Insurance Companies for 2021

What insurance does an independent contractor need?

It depends on what sort of work you do. If you do some accounting work from your home, you’ll probably be okay with E&O insurance, unless you have clients who come over. Then you might want a general liability policy in case someone trips down the stairs on the way to your office.

For most independent contractors, a general liability policy and E&O insurance would be the bare minimum. E&O insurance protects you if you make a mistake in a professional capacity. For example, if our accountant miscalculates someone’s taxes and they wind up owning money in penalties, they could (and probably will) sue you. E&O insurance would cover you for that. Also, keep in mind that people can sue you even if you didn’t make any mistakes: they can sue you if they think you made a mistake.

If you have even one employee, you probably need workers compensation insurance. And if you use your car for business, you might need commercial auto insurance.

A business owners policy might be a good idea: this bundles general liability with property insurance and business interruption insurance. Get quotes from multiple insurance companies, as rates vary.

A business will suffer a ransomware attack every 11 seconds. If you do business online (and who doesn’t?) you might want to consider cyber security insurance. This will protect you in a lawsuit if there is a data breach or your business is hacked.

In addition, you might need health insurance, unemployment insurance, disability insurance, or commercial auto insurance. Let’s look at these one by one.

General Liability Insurance for Independent Contractors

This covers you in case of an injury to your customers or damage to their property. It also protects you in case of a defective product. It does not cover either your property or your employees. If you get only one kind of insurance, make it general liability insurance.

Workers’ Compensation Insurance for Independent Contractors

This is the type of insurance you need to protect your employees from work injuries, lost wages, or funeral costs if the worst happens. Workers’ compensation insurance is required in most states but not all: check this list at NFIB to find out what the laws are in your state.

Commercial Auto Insurance for Independent Contractors

If you have a company vehicle, or if your employees drive company vehicles for work, you’ll want commercial auto insurance. It protects you and your employees from financial responsibility if someone driving the vehicle gets into an accident. It also protects the vehicles from vandalism, theft and collisions.

Professional Liability Insurance or E&O Insurance for Independent Contractors

This is designed to fill any gaps left by general liability insurance. If you make a mistake on a job and your client sues, professional liability insurance or errors and omissions (E&O) insurance can help cover your legal expenses and payouts if a judge rules in favor of your clients. This is probably the most common insurance that an independent contractor needs.

- >>MORE: Best Professional Liability Insurance Companies for Small Businesses

- >>MORE: Professional Liability vs. Malpractice vs. E&O Insurance: How Are They Different?

Contractors’ Pollution Insurance

As a contractor, you know there are environmental laws that you have to adhere to. This insurance protects your business in case of a violation (or if someone thinks there is a violation).

Builders’ Risk Insurance

This usually falls under general liability insurance—be sure to ask if this is included. It covers your equipment and materials in case they are lost or stolen from a job site. If you have a lot of valuable equipment, this is worth looking into.

Roofers’ Insurance

This is also a kind of general liability insurance that protects roofers from physical injury or property damage. If you do any roofing at all, consider adding roofers’ insurance.

These are the most common types of insurance for contractors. Talk to an agent or broker about what insurance your business needs—general liability is the most important, and others can be added on depending on your needs.

Health insurance for independent contractors

If you’re self-employed, you may be wondering what to do about health insurance. Usually, your employer provides this, or at least subsidizes it. And of course, healthcare costs are astronomical, so you don’t want to go without.

If you’re self-employed, you can go to healthcare.gov and enroll in the Individual Health Insurance Marketplace. When you fill out an application, you’ll find out if you qualify for tax credits or other savings. You will also find out if you qualify for Medicaid or CHIP programs, depending on your income and the state you live in.

You can choose from four tiers of coverage, bronze, silver, gold, or platinum depending on your health care needs. Bronze costs the least but you incur higher out-of-pocket costs, and platinum charges the highest monthly premium but your deductible and out-of-pocket costs are very low.

You can also explore self-employed health insurance. Many insurance companies offer these plans. Another option is to look into COBRA coverage if you’ve just left a full-time job. This will allow you to continue on your employer’s group health insurance for up to 36 months. However, now that the Affordable Care Act offers health plans, you will probably find a better deal there.

If you’re under the age of 26, you can stay on your parents’ health insurance, and if you’re married of course you can get insured through their plan.

Health insurance averages somewhere between $300 and $500 a month, depending on where you live. It’s a huge expense for self-employed workers and independent contractors.

Unemployment insurance for independent contractors

Historically, self-employed people were unable to collect unemployment benefits. Then the pandemic happened, and the Pandemic Unemployment Assistance program (PUA) made it possible for independent contractors to collect some benefits. You can even receive benefits if your work has been significantly reduced than your normal level. Unemployment provisions have been extended until September 6, 2021.

Once the PUA benefit period ends, freelancers and those staffing the gig economy will no longer be eligible for unemployment benefits. However, the definition of an independent contractor can be a bit tricky. Federal agencies depend on the “economics realities test” which means if a person gains a large portion of their income from one business, you’re an employee no matter what your employer calls you.

Disability insurance for independent contractors

If you pay Social Security and Medicare taxes, you might qualify for SSDI, or disability benefits. If you haven’t earned enough money to qualify for SSDI, you may still qualify for SSI. SSI is not dependent on how much you make. You only need to have worked the equivalent of ten years or have earned 40 work credits to qualify for disability.

People with a disability are more likely to be self-employed than people without a disability, according to the Bureau of Labor Statistics. They’re also more likely to work part-time instead of full-time.

If you’d rather, there are companies that can offer you either short-term disability insurance or long-term disability insurance. Some companies that offer disability insurance are:

- State Farm

- MassMutual

- Northwestern Mutual

- Assurity

If you choose to go this route, be sure to get at least three quotes and shop around for the best price.

Do independent contractors need personal auto insurance or commercial auto insurance?

If you use your car in the act of providing your business services, you probably need commercial auto insurance. That’s because business use of your personal vehicle isn’t covered by your personal auto insurance policy, so if you get into an accident while working, your insurance company can deny the claim.

If you occasionally use your personal car in the scope of your business, your personal auto insurance should cover it. If you use your car on a regular basis, you should have commercial auto insurance.

Most commercial auto policies run between $100 and $200 a month. Just like your personal auto insurance, the minimum liability insurance covers the cost of bodily injury and property damage to the other party. Laws vary from state to state, with different states requiring differing amounts of liability coverage. If you want to cover damages to your car, you’ll need comprehensive insurance. And just like personal auto insurance, if you have a loan on the car, your insurance company will require you to carry collision and comprehensive insurance.

How much does independent contractor insurance cost?

It depends on many factors. What your business actually does and how risky an insurance company deem it to be is the most important factor in determining how much you pay for insurance. For example, “contractor” could mean you work in residential construction, commercial construction, flooring, roofing, swimming pools—the list is endless.

Also affecting your rates will be where your business is located, how your business is set up, if you operate your business out of your home or if you have an office. This is why most companies won’t give you a quote, although some will. Coverhound, for example, said they couldn’t provide a quote, but estimated $80 a month for general liability insurance.

Consider a business owners policy. This combines business property and general liability insurance into one policy, which saves you some money over buying the policies separately.

>>MORE: Insurance for General Contractors: Coverage, Cost, and Providers

How to get cheap independent contractor insurance quotes?

The most important thing is to shop around. Get quotes from many different companies. There are fintech companies that specialize in small business insurance, including:

- CoverWallet

- Simply Business

- Embroker

- Next

- Biberk

- Huckleberry

- Hiscox

- Thimble

These companies vary a bit in who they insure, but any one of them is worth a look. Almost all of them offer online quotes.

The amount of risk your business is exposed to will dictate how much you pay for insurance. Someone who works in construction will pay higher rates than someone who works in an office. Higher limits will also result in higher premiums (although sometimes those higher limits are necessary). The state where you’re located will also play a role.

To save money on your insurance, you can:

- Shop around to get the best price

- Buy only the amount of coverage you need

- Bundle your policies

- Raise your deductible

- Review your insurance annually

- Maintain a safe work environment

Insurance can be expensive, but it’s necessary. Don’t skip it and hope for the best.

Last thoughts

Being an independent contractor is great in some ways, but not so great in others. Stack the deck in your favor by purchasing the right amount of independent contractor insurance for your business.