When you are an event planner or vendor, you need to ensure that you have the appropriate insurance to cover your activities at the event. Some business insurance companies offer policies specifically tailored for single events, while others provide liability policies that protect your business. It’s essential to keep in mind that these policies cover your liability; they do not cover the event itself. Even if you are an event planner, the policies cover your activities, and the event itself will need a different kind of policy.

We researched companies that offer insurance for events or weddings. The following companies were the four best we found. We also attempted to get quotes from each of them to give you an idea of the cost of insurance related to events.

The quote-gathering process was similar for all four companies. It was a simple online questionnaire, and the company processed and returned the quotes in less than ten minutes after accessing the websites.

- 4 best vendor insurance companies for events and weddings

- Why do vendors at events and weddings need to have insurance?

- Vendor general liability insurance for events and weddings

- How much is vendor liability insurance cost for events and weddings?

- One-day vendor insurance

4 best vendor insurance companies for events and weddings

- Simply Business: Best for comparing quotes to find the cheapest rates

- NEXT: Best for quick coverage and reasonable rates

- InsurePro: Best for those who need short-term coverage

- Event Helper: Best for large events

Simply Business: Best for quote comparisons

A digital commercial insurance broker like Simply Business could be the way to go. They compare various quotes and return the best choices for your specific needs. You provide them with personal information as well as event information, and they provide you with quotes; often, the company returns multiple quotes based on one information form.

It typically takes less than 10 minutes to receive a quote from Simply Business. You also have the option of speaking to someone if you need something more complicated than their basic questionnaire covers.

Pros:

- Online quotes. Easy to compare to find the cheapest one

- Several coverages for different types of vendors and events

- You can buy policies online

- Multiple reference resources are available

- Great customer satisfaction rating on Trustpilot (4.7 out of 5, which is very very high for an insurance company)

Cons:

- Policies handled by third-party insurers

- Can’t file claims through Simply Business

Our attempt to collect a quote from Simply Business yielded a message that we needed to call to speak with an agent.

NEXT: Best for quick coverage and reasonable rates

NEXT is a business insurance company that specializes in selling policies to small businesses online. Insurance policies can be purchased in packages that are customized to specific industries, or you can purchase policies individually. NEXT customers can access their accounts to manage their claims online or access and share digital certificates of insurance.

If you need coverage fast, NEXT might be the company for you. The company was founded in 2016. Claims are handled in-house, and it has its own AM Best rating.

If you need specialized coverage, NEXT may not be the company for you.

Pros:

- Easy, complete in minutes online application

- Reasonable rates for small and micro businesses

- Can get discounts for bundled policies

- Access certificate of insurance online

- Share certificate of insurance digitally

Cons:

- Doesn’t offer some specialized policies

- Those who prefer paper records may not like the digital processes

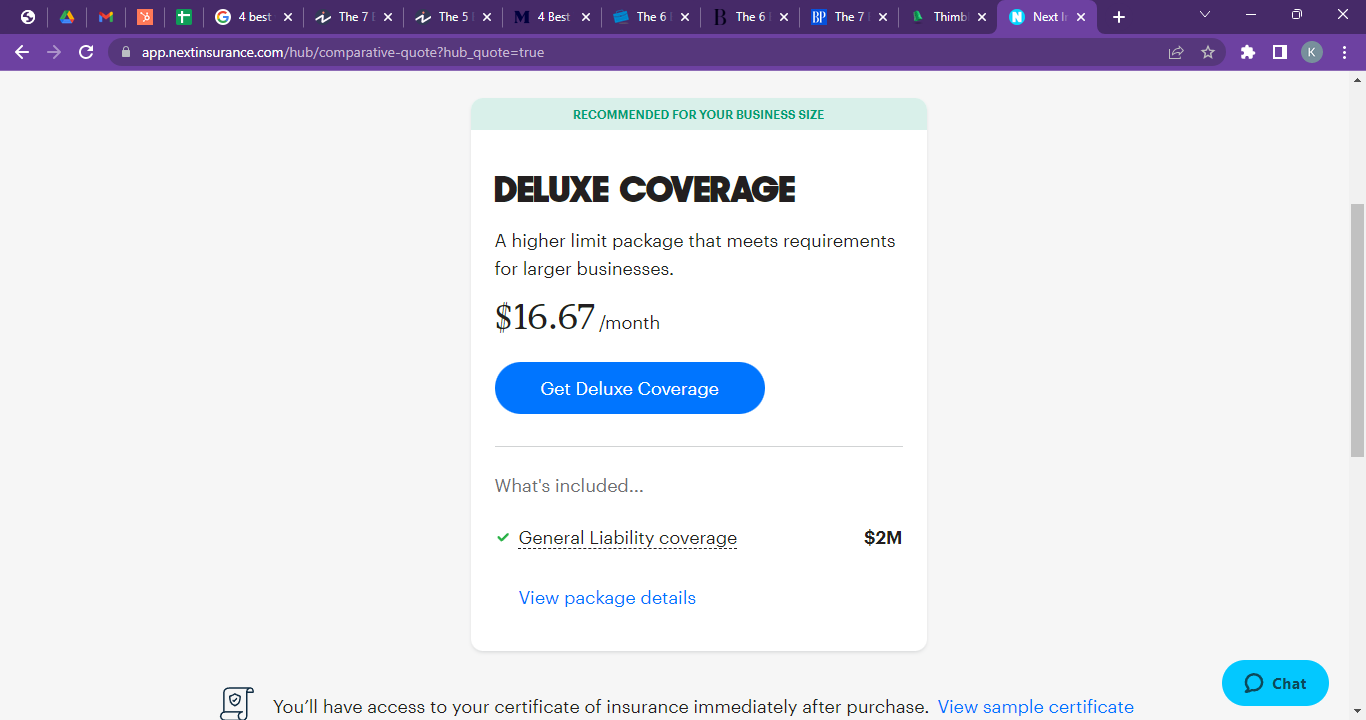

We requested a quote from NEXT for an event planner in Hartselle, Alabama, and this is the monthly premium for that policy.

InsurePro: Best for short-term coverage

InsurePro offers short and long-term insurance coverages for businesses. The company sells coverage for as little as an hour. The policies are underwritten by other companies.

If a business needs coverage quickly or temporarily, InsurePro is a convenient choice. The company also offers policies to business owners who hire contractors. A feature of InsurePro is that it allows you to determine the kind of insurance requirements you have for your contractors, and they can buy a policy specific to your requirements through InsurePro.

InsurePro submits claims to insurance companies that underwrite your policy for you. Thimble only offers customer support online. If you prefer to communicate with your insurance agent via the telephone, InsurePro is likely not the company for you because everything they do is online.

Pros:

- Receive a quote and purchase your policy online in minutes

- Use the Certificate Manager to verify the insurance complies with the contract

- Hourly, daily, and monthly coverage is available

Cons:

- Not available in all states yet

- Only offer online customer support

Event Helper: Best for large events

Event Helper has been in the insurance business since 2009. This company is an event specialist with the capability to cover events that host up to 5,000 guests. They offer liquor liability, and you can add more insureds for multiple venues within their basic liability policies.

Event Helper’s service is ideal for those who want to save money. You also have the ability to go through your personal agent or online.

Pros:

- Instant confirmation of insurance

- Money-back guarantee based on the venue accepting coverage

- Covers large events, up to 5,000 guests

- Liability ranging from $2,000,000 to $3,000,000

- Can purchase a policy over the phone or online

- No-fault coverage for medical expenses

Cons:

- Coverage only in the US

- No payment options

- No 24/7 claims service

- Charge by the day

- Don’t offer coverage for some music genres (heavy metal, punk rock, etc.)

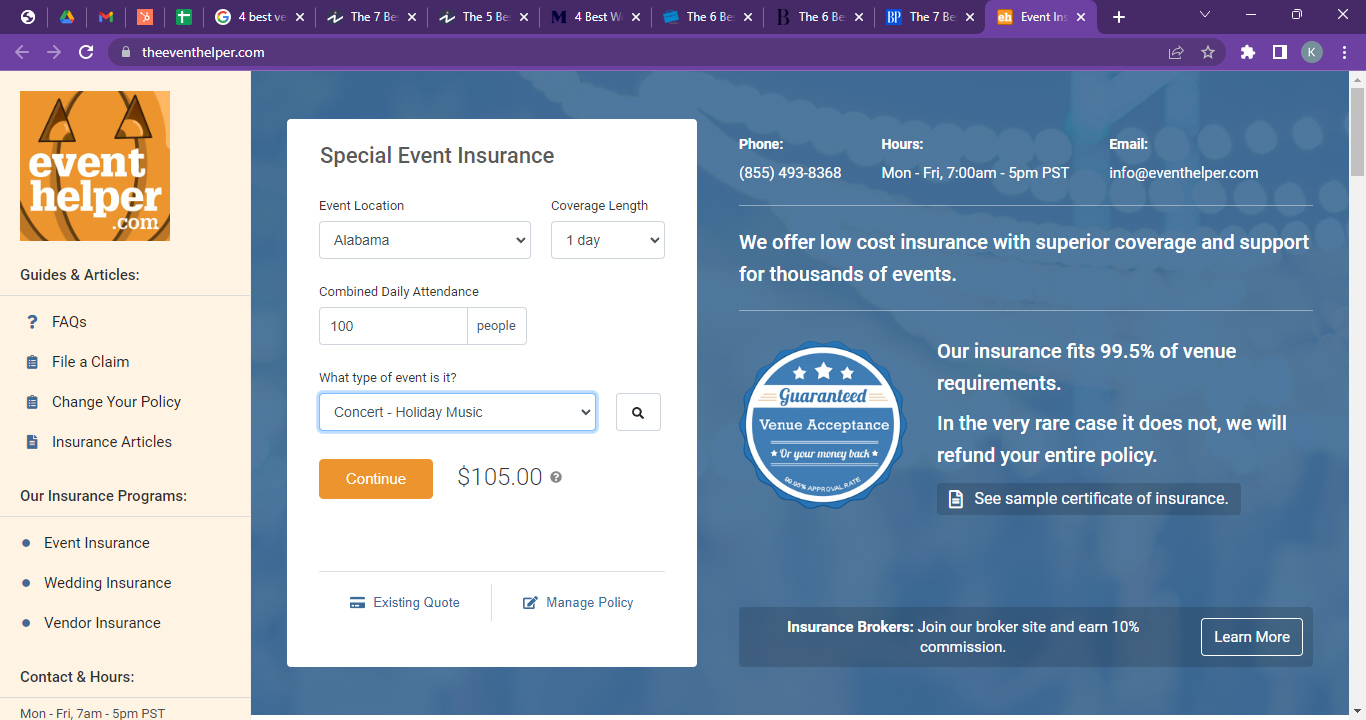

The following quote is for a one-day holiday music concert in Alabama with 100 attendees.

Why do vendors at events and weddings need to have insurance?

Typically when a vendor attends an event or a wedding to provide their services, they are asked to have proper insurance coverage to protect themselves. Also, vendor insurance is to protect the event manager in case the vendor causes some injury and damage at the event and wedding but they don’t have proper insurance coverage. In such cases, the injured may sue the event manager.

So if you are running a vending business and about to attend an event or a wedding, you should have vendor insurance. The event manager will require it. In some cases, the event manager will require all vendors to have vendor liability insurance. Vendor liability insurance may be in several policies, the most common ones are general liability, public liability, product liability, professional liability, and liquor liability.

Vendor general liability insurance for events and weddings

If you are a vendor at an event or wedding, you need general liability insurance coverage. This type of insurance protects you in the event that someone is injured or their property is damaged as a result of your actions. It can help to protect you from costly legal fees and damages.

For example, if someone trips over your table and gets injured, your general liability insurance would cover the costs of any medical bills or lawsuits. Additionally, general liability insurance also protects vendors from any property damage that may occur at the event. For example, if your tent blows over in a storm and damages someone’s car, your insurance would cover the costs of repairing or replacing the damaged property.

Vendor public liability insurance for events and weddings

Vendor public liability insurance is similar to vendor general liability insurance. It also covers third-party’s bodily injury and property damage caused by your operations. However, public liability policy is more standardized and less flexible than general liability policy. While you can add more coverages to your general liability such as food liability and liquor liability, you can’t do that to your public liability policy. As a result, public liability insurance policies tend to be cheaper for the same coverage limits.

Vendor professional liability insurance for events and weddings

Professional liability insurance is important for vendors at events and weddings because it can cover the cost of any legal damages that may be incurred when a vendor is sued because your customers or clients believe that the damage was the result of your negligence, mistakes, or omissions, even when you are actually not. This coverage can be important for vendors who are providing services and advice at an event or wedding, as it can help protect them from any potential liabilities that may arise from their services and advice.

There are many types of vendors at events and weddings that need professional liability insurance. Some of the most common types of vendors that need professional liability insurance include caterers, photographers, and DJs. It is important to note that not all businesses that provide services at events and weddings need this type of insurance. For example, a florist who only provides flowers does not need professional liability insurance. However, if that florist also provides delivery or set-up services, then they would need to have this type of coverage.

Vendor product liability insurance for events and weddings

There are several types of vendors at events and weddings who need product liability insurance. Caterers, for example, need to be covered against any accidents that may occur as a result of the food they are serving. If someone gets sick from the food, the caterer would be held responsible. Similarly, florists need to be covered in case one of their arrangements falls apart and injures someone. And finally, any vendor who is giving away or selling products at an event needs to have product liability insurance in case someone is injured by one of their products.

Product liability insurance covers the cost of defending and settling any product liability lawsuits brought against the vendors. It also covers the costs associated with a product defect. This includes the cost of damages, settlements, and defense costs.

Vendor liquor liability insurance for events and weddings

If you are providing or selling liquor at an event or a wedding, you’ll need vendor liquor liability coverage. One reason why vendors at events and weddings need liquor liability insurance is that it covers them in the event that someone gets sick or injured as a result of drinking alcohol. Liquor liability insurance can also help protect vendors in the event that they are sued for serving alcohol to minors or adults who are already intoxicated.

How much is vendor liability insurance cost for events and weddings?

As you can see vendor liability insurance costs vary significantly depending on several factors. The main drivers are the types of events, coverage types, coverage limits, etc.

The average cost of a $1M general liability insurance for vendors at events and weddings is $55 per month, or $660 per year. This is for a permanent long-term policy.

For the costs of a policy of different types coverage, different coverage periods, and different event types, learn more at the how much does vendor insurance cost

Vendor liability insurance companies

Tens, if not hundreds, of insurance companies, offer vendor liability insurance. It is the most popular insurance policy for vendors working at several event types. It can be overwhelming for you to find the best companies for you. We have done the homework and help you take the guesswork out of this process. Here are our recommendations for the best vendor liability insurance companies for your consideration.

Learn more at the best vendor liability insurance companies

One-day vendor insurance

In many cases, vendors may need a one-day insurance policy only, not wasting their money on a standard and long-term policy. That is because many event managers and wedding planners require one-day coverage for the event date.

The good news is that many insurance companies offer vendor one-day insurance policies. This policy is typically a liability policy, it protects vendors from any liability they may cause during the date of the event. A one-day vendor liability insurance policy is usually with $100K coverage limit. You may want to double-check with the event manager if they require a higher coverage limit.

Learn more at the best one-day vendor insurance companies

Closing thoughts

If you’re working an event in any capacity, you need to consider obtaining appropriate liability insurance. The policies that we found covered vendors or event planners with general liability insurance. However, they didn’t cover the actual event.

Some companies, like Thimble, offer policies that are only in effect for the actual event. You can choose whether to purchase insurance for an hour, a day, or longer. Additionally, if you need coverage for your business beyond the upcoming event, you can purchase those policies as well.

Contact your insurance company or broker if you are unsure what kind of insurance you need for an upcoming event. The professionals with the company of your choice can help you determine what coverage you need for your business or event.