There are several benefits to being a vendor and running a vending business. First, vending is a great way to make money. Vendors can typically charge higher prices for their products than those in traditional retail stores, and they do not have to pay rent or other overhead costs. Second, vending is a very flexible business. Vendors can work part-time or full-time, depending on their needs. They are essentially your own boss. They can also choose to vend at various locations or events.

However, vendors or vending businesses are exposed to risks similar to other businesses. That’s the reason why vendors need liability insurance to protect themselves from any legal claims that may arise from their business activities. Vendor liability insurance provides financial protection in the event that someone is injured or their property is damaged as a result of the vendor’s actions.

- 5 best vendor liability insurance companies

- What is vendor liability insurance?

- What does vendor liability insurance cover?

- How much does vendor liability insurance cost?

- What factors affect the cost of vendor liability insurance?

- How to find cheap vendor liability insurance?

- Requirements for vendor liability insurance

- Vendor liability insurance for different events and markets: Food vendor insurance; Vendor insurance for events; Flea market vendor insurance; Farmer market vendor insurance; food vendor insurance for festivals; wedding vendor insurance; craft vendor insurance

5 best vendor liability insurance companies

Vendor liability insurance usually come in general liability, product liability, or professional liability insurance policies. Hundreds of insurance companies offer vendor liability insurance. Here are our recommendations of the top 5 providers for your consideration:

- InsurePro: Best for on-demand short-term vendor general liability insurance

- Simply Business: Best for finding low-cost vendor liability coverage

- NEXT: Best for a great digital experience and competitive rates

- CoverWallet: Best for comparing several quotes from top-rated carriers

- RVNA: Best for event vendors

InsurePro: Best for on-demand short-term vendor general liability insurance

InsurePro is an insurance broker specializing in serving small and micro businesses. Their unique product is on-demand short-term general liability insurance, which can provide coverage for small businesses for just one day, or a few days, or a few weeks. If small businesses don’t need a traditional permanent and long-term insurance policy, this is a great option for them to save money on their coverage.

Pros

- On-demand short-term coverage for just one day or a few days

- Compare different prices beginning at $10/month.

- Apply online in minutes

- Coverage starts within 24 hours

Cons

- Some policies are state-specific

- Claims must be filed directly with the provider.

Here is a sample quote from InsurePro for a food truck vendor in Dallas, Texas.

Simply Business: Best for finding low-cost vendor liability coverage

In less than 10 minutes, Simply Business’s online form enables vendors to get coverage options and rates from 20+ insurance providers. Simply Business specializes in partnering with carriers offering low-cost coverage so that they can help small businesses, and vendors, find the cheapest coverage available.

Their website is an attractive option for people who like to compare rates side-by-side or who are uncertain about the sort of coverage they should have.

Pros

- Good option to compare and find low-cost coverage

- User-friendly platform

- Quotes generation takes about 10 minutes

- Partners with prominent insurance carriers

- Abundance of industry-specific information

Cons

- Customer support hotline hours are restricted and vary regularly

- Sometimes only return one quote from one carrier

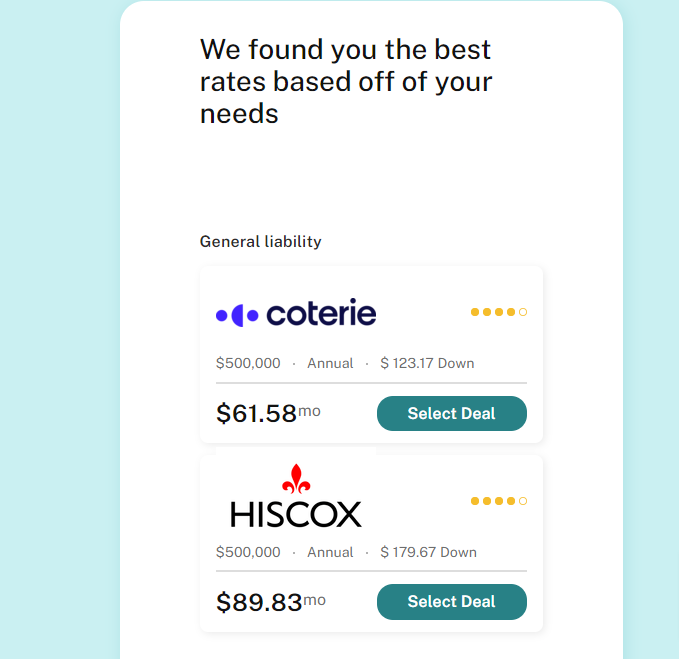

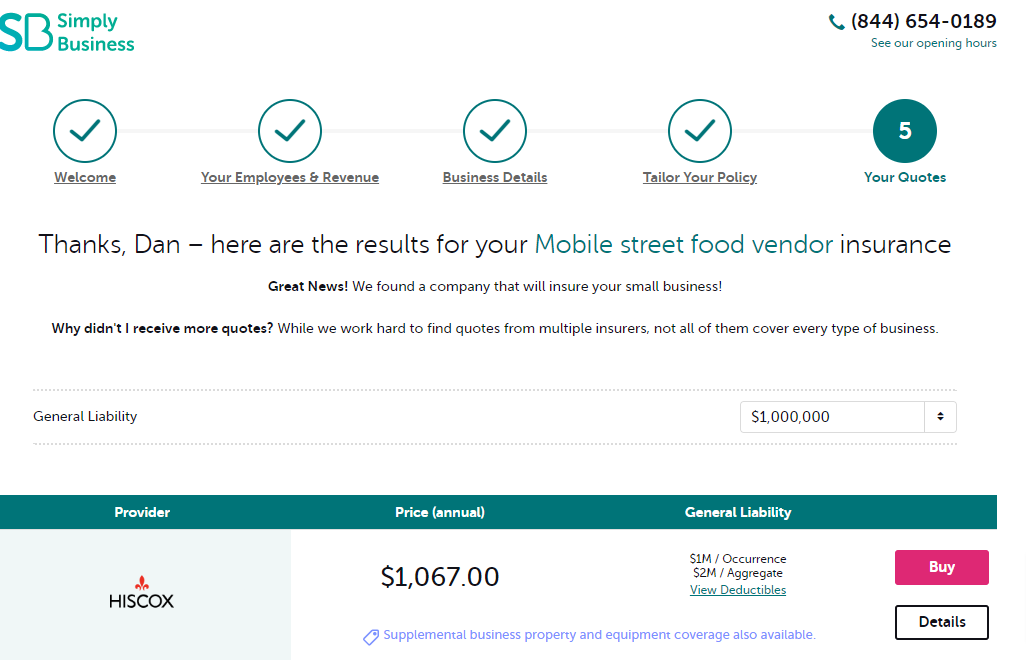

Here is a quote from Simply business for a food truck vendor in Dallas, Texas.

NEXT: Best for a great digital experience and competitive rates

NEXT is an insurtech firm that offers insurance to vendors. The company offers different policies, including general liability, commercial property, and other policies, depending on their location and company. Customers may save money by purchasing several insurance policies from NEXT. It also offers fast insurance coverage through its mobile app. Their rates, especially for general liability insurance, tend to be competitive and affordable.

Pros

- You can get insurance in less than 5 minutes,

- You can get insurance certificate online

- Online insurance prices, coverage, and management

- Online live assistance

- Competitive and affordable rates

Cons

- NEXT does not cover vendors in all states yet

- Quotes for other coverages may not be available online

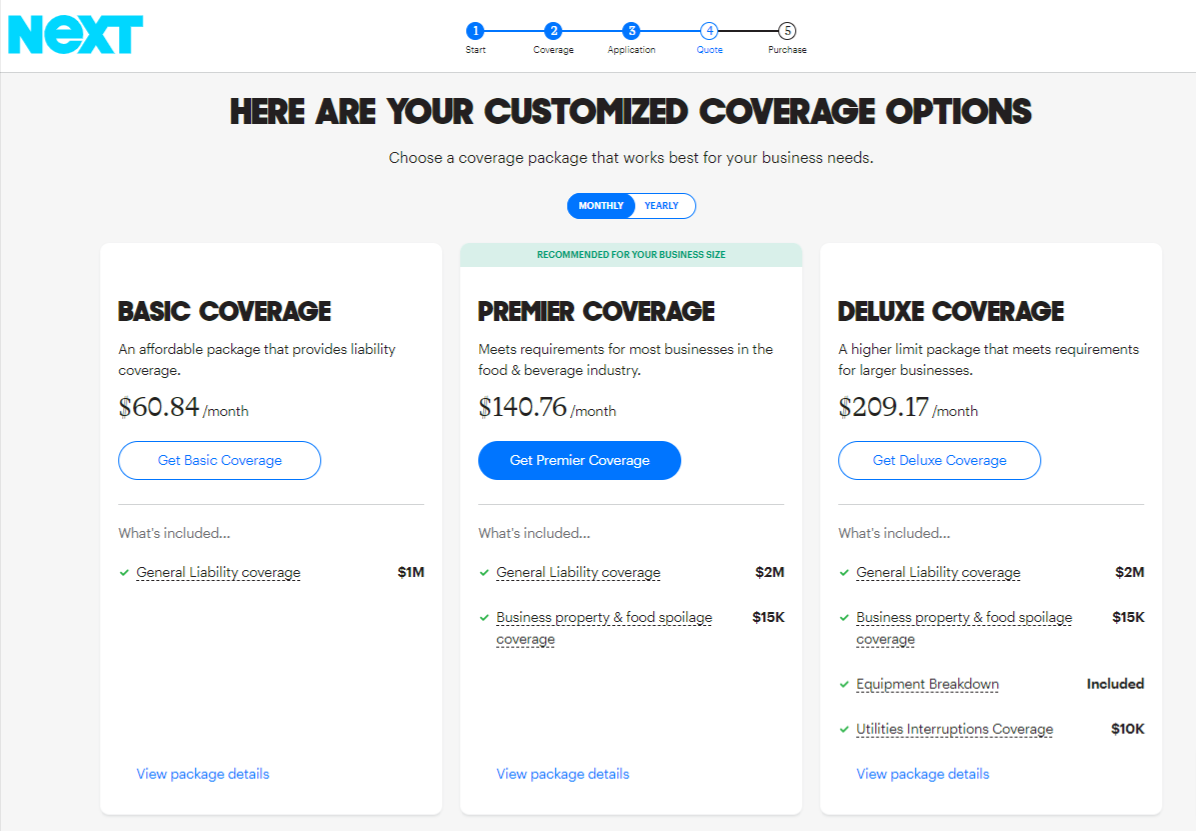

This is a sample quote generated from Next insurance for vendor liability insurance.

CoverWallet: Best for comparing several quotes from top-rated carriers

CoverWallet is ideal for vendors that prefer comparing several quotes of the top-rated carriers. They don’t want to compromise on the carriers’ reputation for reasonable rates. They may use CoverWallet, an online business insurance broker, to browse for policies from the top-rated carriers. CoverWallet makes sure to work with only the top rated carriers on their platform. They offer several vendor liability coverages such as general liability, product liability, professional liability, cyber liability, and workers’ compensation.

Pros

- Quotes, purchases, and policy management are made online

- You can monitor your policy online

- Guide to business insurance available

Cons

- It may take some time to produce a quote

- You can get quotes from carriers on their platform only

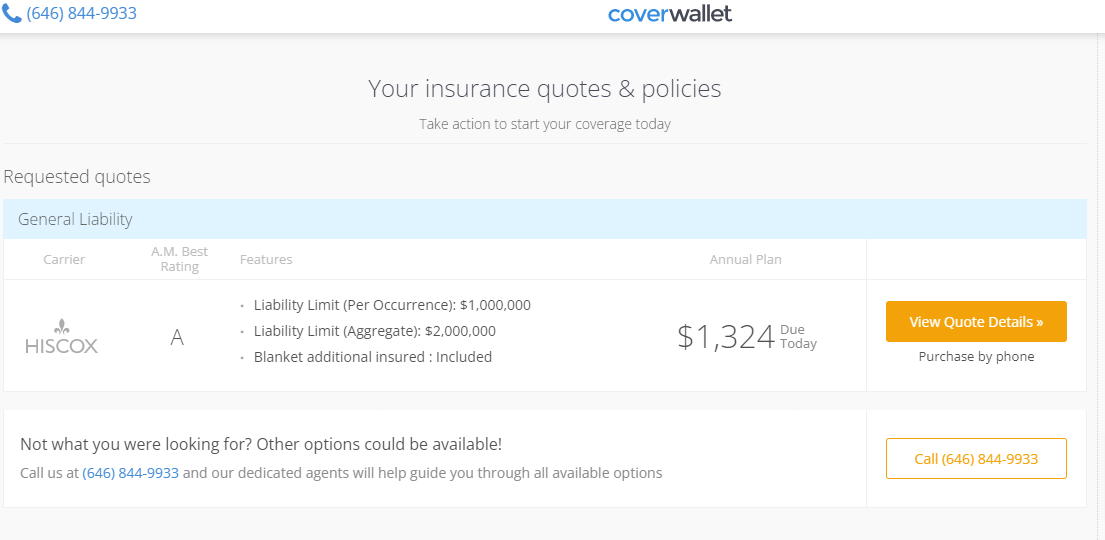

This is a sample quote generated from CoverWallet for vendor liability insurance.

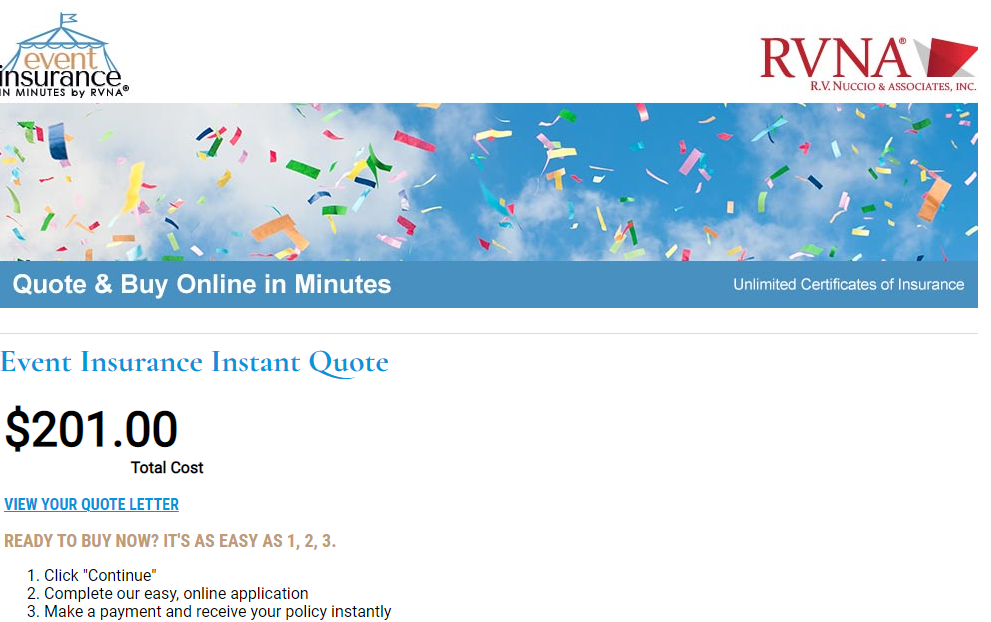

RVNA: Best for event vendors

R.V. Nuccio & Associates (RVNA) is an insurance carrier founded in 1990. RVNA provides excellent coverage for vendors at all events, which is unique. These $50 flexible plans cover liquor liability.

One of the most significant advantages of RVNA is that its vendor liability insurance covers terrorism. Also, RVNA allows vendors to cancel their liability coverage 48 hours before the event for refunds.

The following is a 3-day vendor liability quote from RNVA for a vendor in Kansas.

Pros

- 48-hour cancellation policy.

- Affordable plans start at $50

- Customize production policies with over 20 coverage kinds.

- Online quotes within 2 minutes

- Small and huge events covered.

Cons

- Phone claims only

- Only for event vendors

What is vendor liability insurance?

Vendor liability insurance is an insurance policy that covers vendors, exhibitors, and concessionaires. This coverage is designed by insurers to protect persons who sell, show, and promote goods and services at temporary sites and events.

So, whether you are selling products or services at a farmer’s market or other similar events, vendor liability insurance coverage guarantees you are appropriately covered.

What does vendor liability insurance cover?

A vendor liability insurance typically offers various protection depending on the insurer. The following are some of the most common coverages under this policy:

General liability insurance for vendors

General liability insurance protects vendors from claims of personal injury and property damage.

This kind of insurance is often the most common and basic policy offered by most insurers. Having a poorly set up booth or carelessly setting your items can be risky. If people trip over them or they cause some other issues, you might be in danger of paying a lot of money in fines or even court settlements.

Thanks to the protection provided by general liability insurance, you may not worry about these mistakes. However, if you don’t have it, you are responsible for your financial situation if issues like that occur.

Take this case into consideration. You are at a trade fair and a lady falls over a beam attached to your tent, hurting her head. She has been sent to the hospital and needs to pay her bills.

While you may think the market has liability insurance. The market’s liability insurance will only cover claims against the market premises. It will not protect the independent sellers or the installations they have, like in this case. When something like this happens, having general liability insurance for vendors might help.

Learn more at general liability insurance cost and the best general liability insurance companies

Product liability insurance for vendors

Product liability insurance safeguards your business against claims of negligence or injury brought on by your products you sell and distribute to customers.

In the event that a customer files a complaint against your goods, having this kind of insurance shields you from the possibility of suffering monetary damage as a result of the associated legal fees and court charges.

For instance, a customer claims that the eggs you sold her made her ill with Salmonella. You and your company may be hit with some rather serious civil penalties if she proves her case in court. This unfortunate event might wind up costing your company money and wasting its resources, or even worse, it could cost you personally.

The following is a list of scenarios that, in most cases, fall within the protection of product liability insurance:

- Allergic reactions that were brought on by your product

- Faulty packing

- Flammable goods

- Foodborne illnesses

- Homemade products

- Other illnesses and injuries that have been linked to your product.

These are just some situations where having product liability insurance would shield you from the financial burden of legal fees that might put your company out of business.

Learn more at product liability insurance cost and the best product liability insurance companies

Insurance for event equipment

This policy can protect you against unintentional damage, loss, or theft of stock and other equipment you’re renting or bringing to the event, but it isn’t a part of the venue’s fixtures or fittings.

How much does vendor liability insurance cost?

The average cost of vendor general liability insurance is as little as $45 for 1-3 days of consecutive coverage.

However, you can get a more extended policy for an additional fee. Some insurers offer seven-day insurance policies that provide one week of coverage starting at $89, while a 90-day policy providing three months of coverage starts at about $139.

If you are a vendor working full-time from one event to another, from one farmer to the next, you may want to consider getting a permanent traditional policy. A vendor general liability insurance policy costs an average of $65 per month.

Below are the average costs of different coverage periods of vendor liability insurance:

| Different coverage periods of vendor liability insurance | Average costs |

| 3-day coverage | $45 |

| 7-day coverage | $89 |

| 90-day coverage | $139 |

| Monthly coverage | $65 per month |

These are just the average rates. Your rates will be different. Be sure to shop around with a few companies or work with a broker like InsurePro, Simply Business, and CoverWallet to get and compare several quotes to find the cheapest one for you.

Learn more details at how much does vendor insurance cost?

What factors affect the cost of vendor liability insurance?

The cost of your individual policy is determined by some criteria that are unique to you and your company, such as:

The kind of items you sell

Vendors that sell expensive items are more likely to pay more to insure their items. In the event that there are claims, you will need more money to cover expensive items. Also, some products are generally more costly to insure because they attract more lawsuits. Food is an excellent example.

Where you sell your goods

The location where you will be selling your items is another important criterion. Vendors in urban areas tend to pay more for liability insurance than in small cities and towns. The reason is, litigation is more common in urban

Your business income

Your business income is another crucial criterion determining your vendor liability insurance cost. High-income vendors tend to pay more for their vendors’ liability insurance. The reason is businesses with higher incomes tend to pay larger payouts when sued.

The coverage limits you choose

Your coverage limit is the maximum money you can get from your insurer for a particular policy. Usually, a higher policy limit means you will get better coverage but you have to pay more money.

The duration of the policy

The length of coverage is another essential coverage. Vendors can either purchase short-term coverage or long-term coverage. Short-term coverage offers you protection for a short period probably between a day or a month. Depending on the insurer, you may even buy policies per event. This policy is best for vendors who plan only intend to attend one or two exhibits each year or only sell at seasonal events.

The other option is an annual policy. The yearly policy provides the most comprehensive coverage and the most value for your money for vendors. This policy is a better choice if you attend three or more events each year and your items are handcrafted by you.

In terms of cost, the yearly coverage is more convenient and cost-effective for various events that occur throughout the year than obtaining a short-term policy for each show.

How to find cheap vendors’ liability insurance

As we discussed earlier, some factors come into play when calculating the cost of your insurance. Nevertheless, if you want reasonably priced vendor liability insurance, you should think about doing the following:

Compare quotes

The easiest way to get inexpensive vendor insurance is to shop around and evaluate the policies offered by different insurance providers. Consider obtaining price estimates from a minimum of three different insurers to ensure you receive the best possible deal.

Pay your premium in full

It could seem to be more convenient to pay your premium every month. However, if you pay for the whole year’s worth of insurance premiums in advance, you may be eligible for discounts.

If your insurance premium is 50 dollars per month, for example, paying them monthly would result in a total yearly payment of 600 dollars. If you pay for it all at once, on the other hand, it could just cost you $420 to 450, or perhaps even less depending on the insurance company.

Bundle several policies at the same carrier

Customers who purchase numerous policies from the same insurer are eligible for discounts from that insurer. Therefore, if you are interested in saving money on your vendor insurance, you might think about purchasing extra coverage from the same insurance provider.

Requirements for vendor liability insurance

The law in most states does not require vendors’ liability insurance. However, the policy is a must-have as many event planners and market managers require vendors and exhibitors to present evidence of insurance before they can apply for or attend their events.

In most cases, you only need a general liability policy and add the event, venue, or city named as an additional insured. In the event of a claim, this implies that the venue is covered by your insurance. Every guest needs their own insurance coverage and cannot be designated as an extra insured on the policy of another insured.

One-day vendor liability insurance

One-day liability insurance is a policy that provides protection for vendors against any potential legal action that may arise from their actions on the day of the event. This type of policy can be especially beneficial for vendors who are not regular attendees at the event, as it can provide them with some peace of mind in knowing that they are protected in the event of any mishaps. One-day liability insurance is also a great option for vendors who are not already covered by another insurance policy.

Learn more at the best one-day vendor insurance companies

Liability insurance for food vendors

Food vendors should have liability insurance because they may cause injury to others. For example, if a food vendor does not cook their food properly and someone gets sick as a result, the food vendor may be held liable. Another example is if a food vendor sets up their stand too close to another vendor’s stand and someone gets injured in the altercation, the food vendor may be held liable.

Food vendor insurance for festivals

Food vendors at festivals may be exposed to a number of risks, including food poisoning and contamination. They may also be liable for any damages caused by their food, such as illness or allergic reactions. That’s why it’s important for food vendors at festivals to have liability insurance. This will help protect them from any potential legal issues that may arise.

When a food vendor is responsible for property damage at a festival, their liability insurance is responsible for the damages. This type of insurance covers the cost of repairing or replacing any property that was damaged as a result of the vendor’s actions. It can also help to cover any legal fees that may arise from the incident. Having liability insurance in place can help protect both the vendor and the event organizers in the event of an accident.

Food vendors at festivals are usually mobile food truck or hot dog cart. They may need different insurance coverage

Liability insurance for mobile food truck

A mobile food truck is probably the most popular food vendor. You can find mobile food trucks at farmer markets, flea markets, or even trade fairs, and private events like birthday or college reunions.

Mobile food trucks need to have vendor liability insurance because they can cause bodily injuries and property damage. Food truck owners can be held liable for the injuries their food truck causes, and they can also be held liable for any property damage their food truck causes. Food trucks can cause a variety of injuries, including: burns, slips and falls, and food poisoning. They can also cause a lot of property damage, such as fires, broken windows, and damaged sidewalks.

Learn more at the best food truck insurance companies

Liability insurance for hot dog cart

Similar to the mobile food truck businesses, hot dog cart operations are exposed to similar risks. So it is a good idea for hot dog cart owners to have the right liability insurance coverage to protect themselves. In most cases, they are required to show insurance evidence before being allowed to sell at an event or a market.

Vendor insurance for events

Vendors are usually required to have insurance coverage before working at different events such as weddings, birthdays, trade fairs, conferences, etc. The most common policy they are required to have is general liability. If they are a food vendor, it may be wise to have product liability coverage as well.

Flea market vendor insurance

Flea market vendors need to have insurance to protect themselves from the many risks and issues they may face while doing business. One of the most important types of insurance for flea market vendors is general liability insurance, which can protect them from lawsuits if someone is injured while at the market. Vendors should also consider product liability insurance, which can protect them if a customer is injured by a product they purchased at the flea market. Other types of insurance that may be beneficial for flea market vendors include property insurance, business interruption insurance, and automobile insurance.

Flea market vendors face a number of common risks and issues, such as theft, accidents, and injuries. Having the appropriate insurance can help protect them from these risks and ensure that they are able to continue operating their business in the event of an incident.

Liability insurance for farmer market vendors

Farmer market vendors need to have insurance because they are often exposed to a variety of risks and issues. These can include things like product liability, property damage, and personal injury. Vendor insurance can help protect these businesses from any potential financial damages that may occur as a result of these risks. Coverage options can vary based on the specific needs of the vendor, but some common types of coverage include general liability, property damage, product liability, and workers’ compensation. By having insurance in place, farmer market vendors can rest assured knowing that they are protected in the event of any unforeseen circumstances.

Wedding vendor insurance

Most wedding vendors, such as caterers, florists, and photographers, need some type of insurance to protect themselves from potential risks. For example, if a caterer accidentally burns down the reception hall, their insurance would help cover the damages. Wedding vendors may need different types of insurance depending on their business. For example, caterers might need liability insurance to protect them from lawsuits, while florists might need property insurance to cover damage to their flowers or equipment and professional liability insurance to protect themselves if their clients are not happy with their service and decide to sue them. No matter what type of insurance a vendor needs, it will likely protect them from a number of issues and risks, such as property damage, liability, and accidents.

One-day wedding insurance

One-day wedding insurance is a type of policy that covers you for damages or losses that may occur on the day of your wedding. This can include things like lost or damaged wedding attire, jewelry, or other items, as well as cancellation or postponement of the event. The cost of one-day wedding insurance varies depending on the coverage you choose, but typically starts at around $100.

Learn more at the best one-day event insurance companies

Craft vendor insurance

Craft vendors are a necessary part of many events, from street fairs to large music festivals. They provide a unique and interesting shopping experience for attendees, as well as adding to the overall atmosphere of the event.

One of the main reasons craft vendors need liability insurance is to protect themselves from potential lawsuits. Craft vendors often sell items that are hand-made or one-of-a-kind, meaning that they can be held liable if someone is injured by one of their products. Liability insurance will help protect the vendor from any legal expenses that may arise as a result of an injury.

Additionally, liability insurance can help protect craft vendors from other risks and issues. For example, if a vendor’s booth catches fire, liability insurance will help cover the costs of any damages that occur. Similarly, if a vendor is accused of copyright infringement, liability insurance can help cover the costs of any legal fees or settlements that may be required.