Business owners are often advised, if you only get one type of insurance, it should be general liability insurance. Let’s see how much general liability insurance costs small businesses.

- How Much does General Liability Insurance Cost?

- What factors affect the general liability insurance cost?

- How to get cheap general liability insurance?

- What is General Liability Insurance?

- Who Needs General Liability Insurance?

- Compare General Liability Insurance Quotes

How Much does General Liability Insurance Cost?

Of course, one of the most important things you’ll want to consider when choosing your coverage is cost. The average cost of general liability insurance for small businesses is around $500 a year.

- Almost half of businesses paying between $300 and $600 a year

- 17% pay less than $300 a year

- 35% pay more.

That means the median payment for general liability insurance is about $40 a month, which won’t break the bank. Keep in mind that the cost will be affected by factors such as the size of your business, and if your business is in a high-risk industry.

However, the cost of general liability insurance for your own company or business will be different and it varies by providers. Make sure you shop around with at least 3 companies or a digital broker that can provide several quotes so that you can compare to get the cheapest quote for you. We recommend the top 3 providers below:

- Simply Business: Best for finding cheap coverage from top-tier carriers

- NEXT: Best for contractors and local businesses who want to have fast and affordable quotes

- CoverWallet: Best for comparing several quotes online

>>MORE: Cheap General Liability Insurance for Contractors

What factors affect the general liability insurance cost?

Several factors affect the general liability insurance cost of your business. Below are the main ones. The list will give you some idea why your general liability insurance cost may be a lot more or less expensive than your neighbor business.

Your industry:

General liability insurance provides businesses with protection against “slip and fall” claims. Some industries have a higher risk of this type of claims than others. For example, a retailer or cafe chain with several store fronts are more likely to have claims against “slip and fall” incidents than an IT business.

Higher risk industries will pay more for general liability insurance coverage. Construction and contracting businesses have the highest premiums for general liability insurance policies, following by cleaning and landscaping. On the other hand, photographer and IT businesses have the lowest premiums.

Size of the business:

Larger businesses typically require more insurance protection, which costs more. The more the storefronts your business has, the bigger the storefronts are, and the more customers you have, the more likely you’ll have claims. As a result, your general liability insurance policy is more expensive. As your business grow, the premiums for your general liability insurance will be likely to increase.

Insurer:

Different insurance companies calculate general liability policy premiums in different ways. And they may have different preferences (appetites) for covering certain types of businesses. This will impact the quotes insurers provide. It’s the reason you owe it to yourself, and your business, to get quotes from several insurance providers.

Claims history:

This is a simple insurance concept most people understand. If you’ve made a lot of claims on your general liability insurance, it’s a sign to an insurer that you’re more likely to file more claims in the future. If you’ve filed claims in the past, you can expect to pay higher premiums. The lesson: Not all incidents are preventable, but it’s still important to operate your business in as careful a way as possible to avoid unnecessary claims that could increase your insurance costs.

Credit score

The credit score of the business owner who is the policyholder can also impact the cost of general liability insurance. Credit scores are considered to be a measure of how reliable a policyholder will be in paying their insurance premiums in full and on time. They are also reflective of how responsible people are. If you have a low credit score, you will likely pay more for general liability insurance because you’re viewed as a bigger risk. The good news: A high credit score can save you money on coverage.

Location. Location. Location

Some cities and states are known for their high rates of lawsuits. If your business is located in one of them, you’ll pay more for general liability protection.

These aren’t all the factors that will influence your general liability premium, but they’re the ones that will have the biggest impact.

How to get cheap general liability insurance?

Here are some tips to help you find the coverage you need at a fair price:

Compare several quotes to find the best value.

Get quotes from a few companies so you can compare coverage and prices. Shopping around and comparing several quotes is the only way to find the best and the cheapest quote for your contracting business.

Don’t stop shopping around.

Make sure you get new quotes before you renew your policy. Insurance companies change their quotes and rates very often. Your quotes will change in 12 months. So when it is time for renewal, make sure you shop around again to find the cheapest one for your business again.

Take advantage of discounts.

If they’re not offered to you when getting a quote, ask about them, whether you’re buying online or through an agent. Insurance companies always have the list of discounts, make sure you utilize any of them that is available to your business. Whenever possible, bundling several business insurance policies to get bundle discounts to save on premiums.

Taking these steps will help ensure you’re not paying too much for your general liability coverage.

>>MORE: Cheapest General Liability Insurance for Small Businesses

What is General Liability Insurance?

In case you’re in the dark, general liability insurance guards your business against claims for bodily injury, damage to property, or personal injury, as well as advertising injuries and potential legal costs. If a customer is injured on your property, or you accidentally destroy a client’s merchandise, you’ll want general liability insurance.

>>MORE: General Liability Insurance: Everything You Need to Know

Who Needs General Liability Insurance?

Did you know that roughly 40% of small businesses will file a claim in any 10-year period? And that 54% of small businesses have general liability coverage? General liability insurance covers some of the most common and expensive claims, so you should consider getting this type of insurance.

Anyone whose business is open to the public will benefit from general liability insurance. In addition, you should consider general liability insurance if you:

- Advertise or create marketing for your business

- Use social media

- Use third-party locations

- Clients require it

One high-cost lawsuit could easily put you out of business. Since general liability insurance is not very expensive, smart business owners will want to get themselves a policy.

Compare General Liability Insurance Quotes

Fortunately, there are many resources available online for you to compare and contrast quotes from different insurance companies. The digital brokers listed below are some of the best and easiest ways to compare rates online:

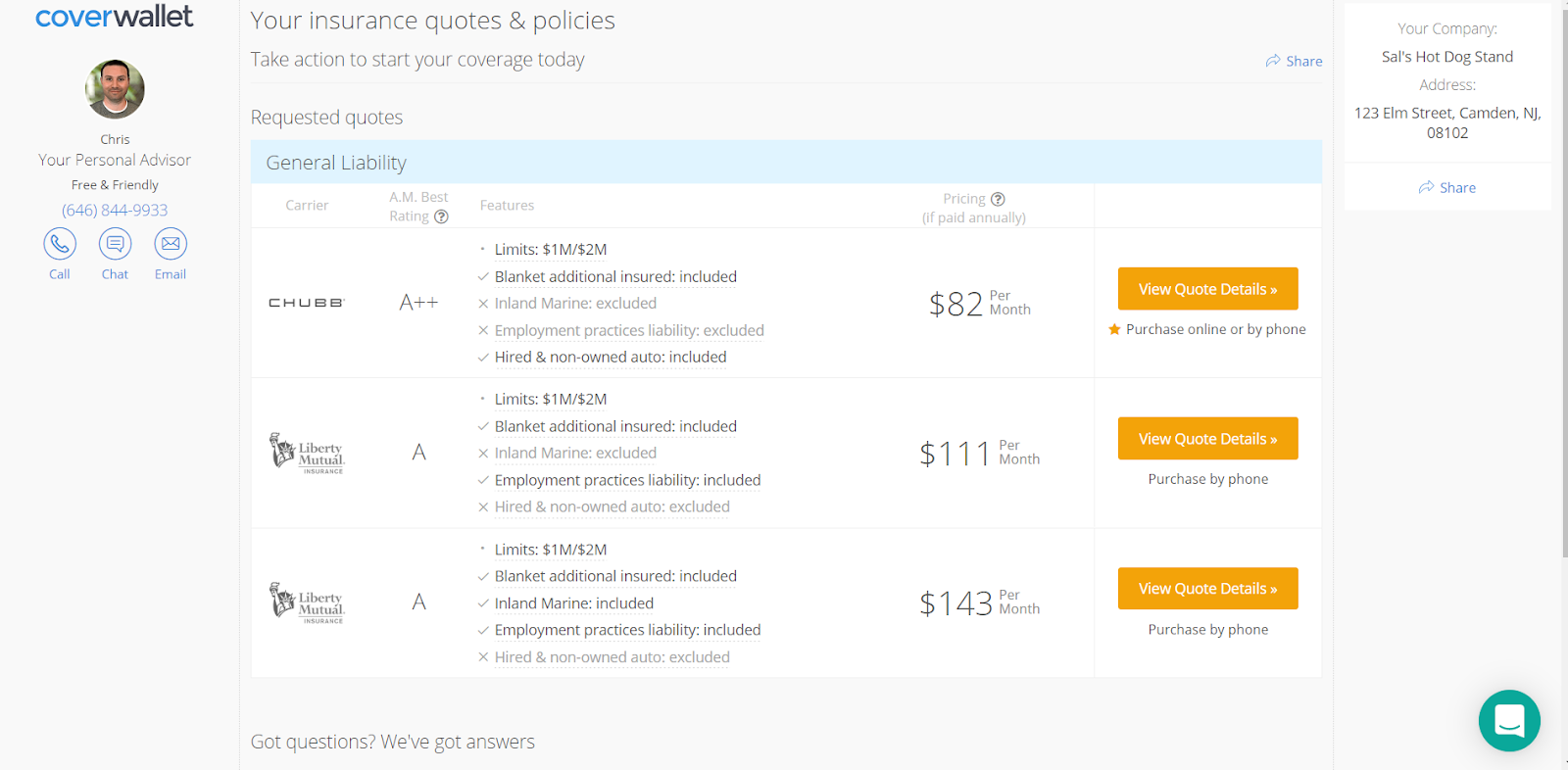

CoverWallet:

Great for small business owners. Features an easy-to-use online system to compare rates. Filling out the information may take a few minutes, but once you’re done you’ll be able to compare quotes from different companies.

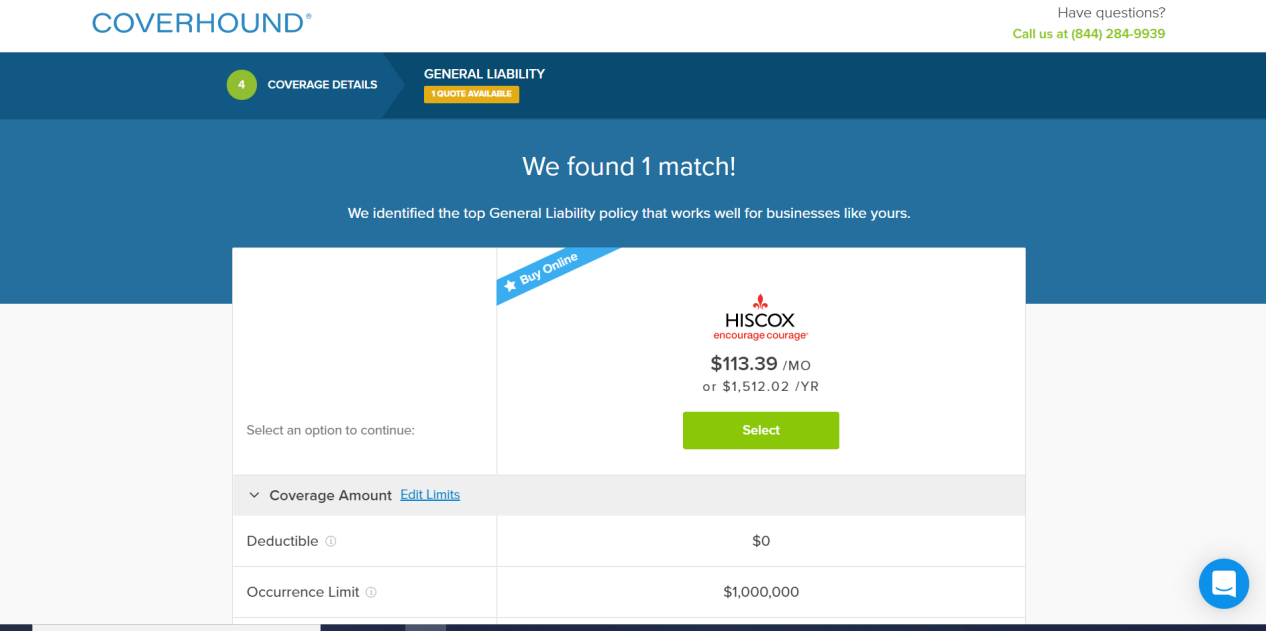

Coverhound:

Coverhound not only lets you compare rates, but sells insurance as well. It also works with several prominent insurance companies to make sure you have the most up-to-date rates and policies. Entering your info is a fairly quick process, and it will match you with the best rate for your company.

Insureon:

Insureon allows you to search for quotes based on business type or industry. Once you enter your information, you’ll have the option to receive a call from one of their professionals to get a quote.

CommercialInsurance.net

CommercialInsurance.net lets you create custom searches for different types of insurance, helping you find exactly what you need. Just answer a few quick questions, and a representative will contact you with more information. They will also list general liability insurance providers in your area.

>>MORE: Best General Liability Insurance for Small Businesses

General liability insurance by profession

The type of industry that your business is in plays an very important factor in the cost of general liability insurance for your business. We are examining a couple of popular industries as follows:

- How Much does General Liability Insurance Cost for Contractors?

- How Much does General Liability Insurance Cost for Handymen?

- How Much does General Liability Insurance Cost for Non-profits?

- How Much does General Liability Insurance Cost for LLCs?

- How Much does General Liability Insurance Cost for Restaurants?

- How Much does General Liability Insurance Cost for a Wedding?

- How Much does a $1M General Liability Insurance Policy Cost?

How Much does General Liability Insurance Cost for Contractors?

Not only do contractors need general liability insurance because they tend to work in risky environments, but also many clients will require that their contractor has general liability insurance. That way, if a customer trips over a hammer you left lying around, you’ll be covered.

As a general contractor, you can be sued for all sorts of reasons, as you are usually working on a third-party site. The potential for someone to injure themselves on a construction site is high. A client could get injured, or just someone out for a walk and not paying attention.

Also, some states require general liability insurance for contractors. Check with your state’s guidelines to see if they require it for contractors or construction workers.

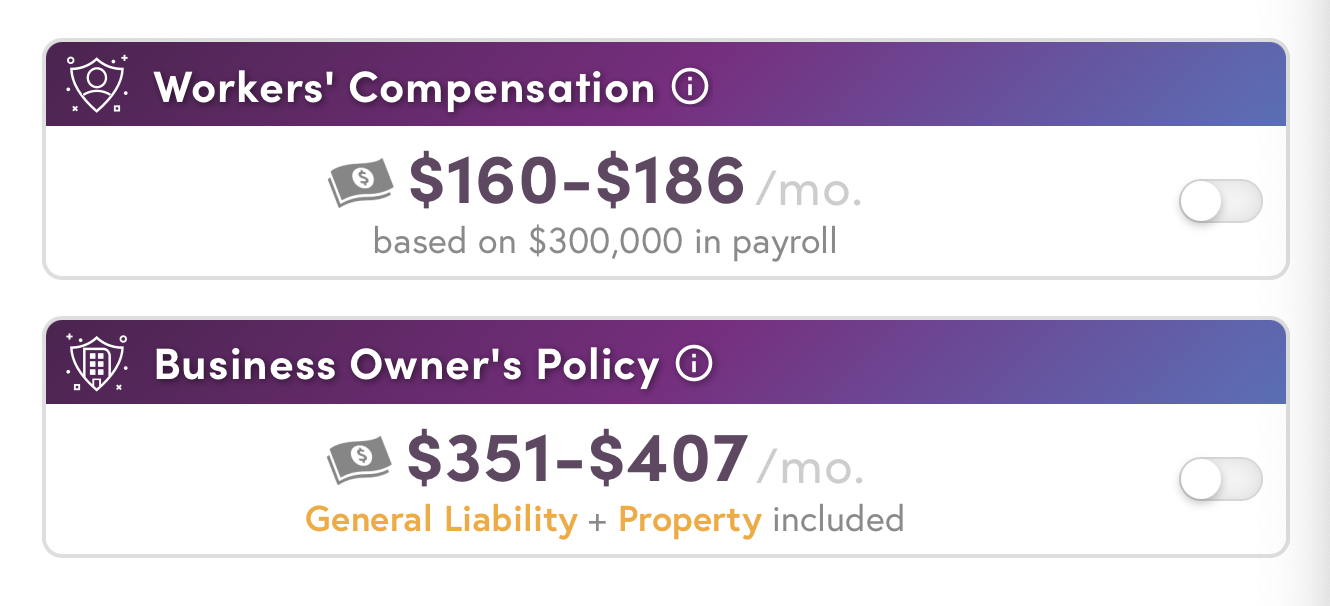

Luckily, general liability insurance is inexpensive, even for contractors. For example, Huckleberry gave us this quote for a general contractor with $1M in revenue:

General liability insurance costs $160-$186 for contractors. Combining with commercial property insurance will cost contractors $351-$407 a month.

You need to shop around with a few insurance companies to compare quotes to find the best one for you. Shoping with a digital broker like CoverWallet or Simply Business is a good way to compare several quotes in one place, conveniently.

Learn more the general liability insurance costs for different contractor types.

>>MORE: Cheapest General Liability Insurance for Contractors

How Much does General Liability Insurance Cost for Handymen?

You need a license to work as a handyman in most states. Handymen typically work with lower budgets than contractors, but things can still go spectacularly wrong. If you’re hired to lay down carpet and you accidentally ruin the customer’s hardwood floor in the process, general liability insurance will cover you. Since handymen always work at the customer’s home, the potential for property damage is high.

Handymen can expect to pay between $360 and $1000 per year for general liability insurance, with handymen doing roofing or power washing paying a little extra.

How Much does General Liability Insurance Cost for Non-profits?

Since general liability insurance covers risks like bodily injury and property damage, and advertising injuries, it’s important for even non-profits to get a policy. Non-profits usually work with the public, meaning the potential for a lawsuit. In addition, many non-profits host events such as charity events and fundraisers, which attract many people. The chances that one such person trips over something and breaks an ankle is pretty high. Luckily, the average non-profit pays just $45 a month for general liability insurance.

How Much does General Liability Insurance Cost for LLCs?

One of the questions you will need to answer when applying for general liability insurance online is, how is your business structured? In other words, is it a sole proprietorship, a corporation, an LLC, or a partnership?

Many business owners start their businesses as a sole proprietor and then later switch to an LLC. It’s easy to start a business as a sole proprietor, but it views you and your business as one and the same. In other words, if someone sues you, they can sue you for everything owned by your business and your personal property, such as your house. An LLC limits your liability to the business since it legally separates your personal property from your business property.

Changing from a sole proprietor to an LLC is usually just a matter of filling out paperwork and then filing your business taxes separately from your personal taxes. Insurance wise, there isn’t much of a difference in rates. It’s when you jump to a corporation that you’ll need more insurance.

You can expect to pay between $300 and $1,000 a year, depending on your profession.

How Much does General Liability Insurance Cost for Restaurants?

Restaurants can have wet floors that customers can slip on, making general liability insurance a necessity. This is especially true if you serve alcohol. According to Insureon, restaurant owners typically pay about $175 a month for a business owners policy. A business owners policy bundles general liability insurance with property insurance, with a discount for having the two policies together.

How Much does General Liability Insurance Cost for a Wedding?

General liability insurance for a wedding is necessary, even though it’s only for one day. There are many people at your wedding, and you don’t want to risk someone injuring themselves or damaging the venue’s property. According to The Knot, general liability insurance for a wedding costs about $185.

How Much General Liability Insurance does My Business Need?

Okay, you’re convinced you need general liability insurance for your small business. Now, the next question is, how much do you need?

Generally, the more risk your business is exposed to, the more liability insurance you should have. You can also add special situations to your policy, called endorsements. Endorsements can include:

- Product liability

- Hired and non-auto insurance

- Liquor liability insurance

That said, many small businesses go with a $1M/$2M policy. This means the policy will cover you up to $1M in a single claim, and up to $2M a year.

How Much does a $1M General Liability Insurance Policy Cost?

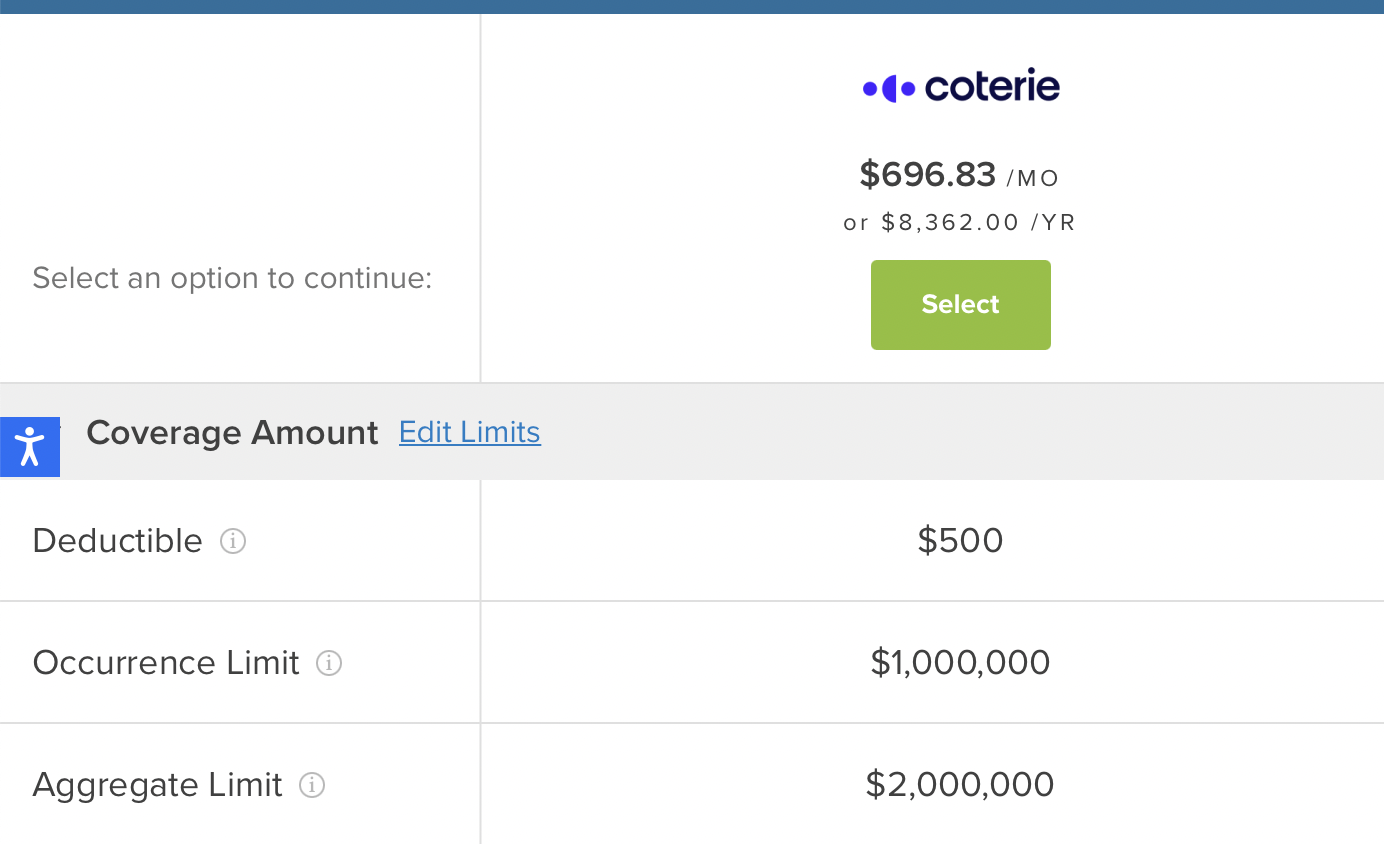

It depends on your location and what type of work you do. Coverhound gave us this quote for an electrician, with a million in revenue and located in California.

Again, be sure to compare quotes of a few companies find the best one for you. Working with a digital broker like CoverWallet or EZ.insure or commercialinsure.net is a good way to compare quotes from several companies in one place, conveniently. These brokers partner with several carriers and are able to provide you several quotes at once.

Final Thoughts

The right insurance company is different for every business. The best way to make an informed decision when it comes to buying general liability insurance is to shop around. Compare quotes from different companies, and see which ones offer discounts to small businesses. The above are just a few of the many online options for comparing rates and quotes, and knowledgeable agents are just a phone call away. General liability insurance is necessary for any business, but if you do your research, you should be able to find great coverage that doesn’t break the bank.