While vending is lucrative, inherent hazards are involved, mainly when dealing with food and other related products. Your customers or their visitors may sue you for a variety of reasons, including food poisoning and allergic reactions. Typically, the majority of vendors choose long-term insurance coverage. What if you do not work daily?

If you only work particular days, it does not make sense to spend $396 per year on vendor insurance. You may instead get one-day vendor insurance. What you need is a one-day event insurance policy that covers general liability and product liability coverage for the little time you will be working.

This article will show you some of the best insurers that offer these one-day insurance policies and other information you may need.

- 5 best one-day vendor insurance companies

- What is one-day vendor insurance?

- Why do vendors need one-day insurance?

- How much does one-day vendor insurance cost?

- What are the factors that affect the cost of one-day vendor insurance?

- Different types of one-day vendor insurance: Liquor liability; bartenders; photographers; catering; events; and DJ

5 best one-day vendor insurance companies

Not many insurance companies offer one-day vendor insurance. However, we found 2 companies: InsurePro and Thimble offering exactly one-day coverage. However, we also realized that daily coverage cost is not as cheap as we thought. In some cases, monthly coverage costs may be almost the same as daily coverage. In such cases, we actually recommend you get monthly coverage for the same amount of money. Below are the 5 companies that we believe we should consider when you are looking for one-day vendor coverage. Some of these companies offer 30-day coverage at the same price or even cheaper.

- InsurePro: Best for affordable one-day food vendor insurance

- Simply Business: Best for finding low-cost vendor coverage (30-day coverage is almost as cheap, or even cheaper)

- Thimble: Best for comprehensive one-day vendor insurance coverage

- CoverWallet: Best for comparing vendor insurance companies

- NEXT: Best for fast vendor coverage

InsurePro: Best for affordable one-day food vendor insurance

InsurePro is an insurance broker specializing in micro and small businesses. They are the best option for food vendors that look for one-day coverage. Food vendors can look for one-day policies with top-rated national carriers on InsurePro platform.

These policies may cover a restaurant that is participating in a one-day street festival as well as a food cart that is branching out to corporate and family gatherings. Insurepro may provide food vendors with insurance plans covering general liability, commercial property, and workers’ compensation, among other coverage options.

Pros

- Daily coverage is available at a reasonable price

- User-friendly website

- Covers up to 300 professions

- Support is available all-day

Cons

- Relatively new company

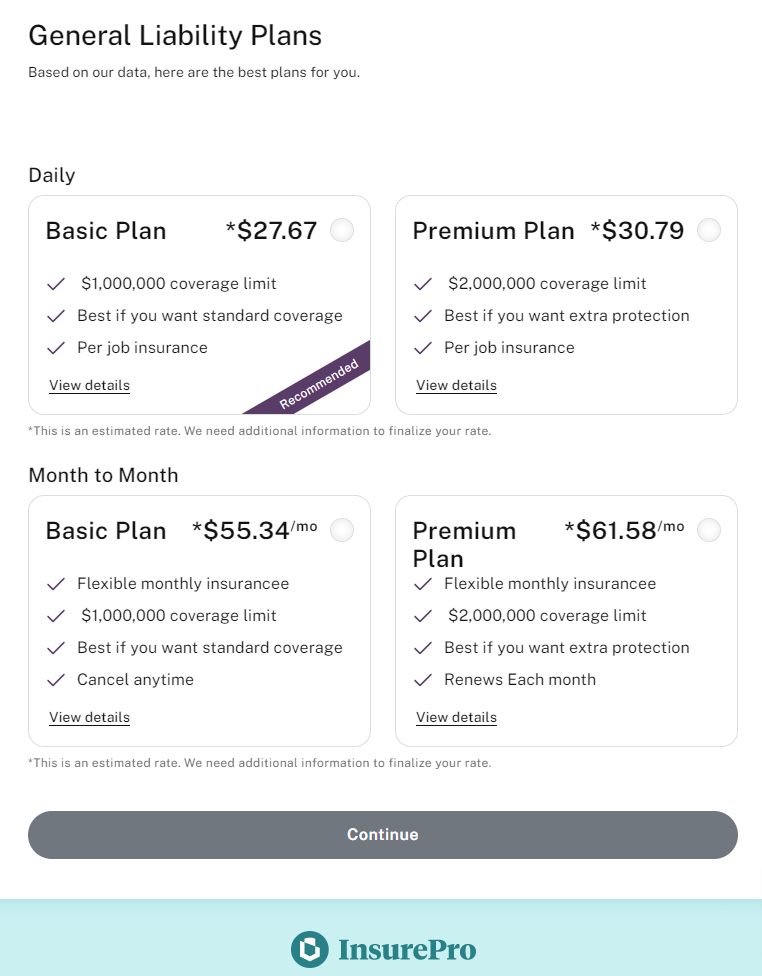

As you can see below, one-day coverage for a food vendor offered by InsurePro costs just $27.67 per day for the basic plan; the premium plan costs $30.79 per day. InsurePro also offers you monthly plan as well if that’s something you want to consider. The advantage of a monthly plan is that it only costs twice the daily plan, so you may be able to get a lot more for your bucks.

Simply Business: Best for finding low-cost vendor coverage

Simply Business has one of the best user-friendly websites and offers high-quality insurance policies. Simply Business is the ideal supplier for vendors since it provides insurance for vendor insurance as well as special event insurance.

The vendor and special event insurance coverage take into consideration the nature of the gathering, the location of the event, the number of visitors, and whether or not any celebrities will be in attendance.

The liability limit of the coverage is one million dollars. Terrorist acts are covered under the insurance, but you have the option to opt-out of having that coverage, which would result in a reduced premium for you.

Pros

- Quotes are obtained in minutes

- User-friendly website

- Robust financial backing from Travelers

- Allows you to obtain multiple quotes from different insurers

Cons

- You can’t file a claim with Simply Business. You have to do that directly with the insurance company

- If you are interested in a particular insurance company that they are not working with, you are out of luck

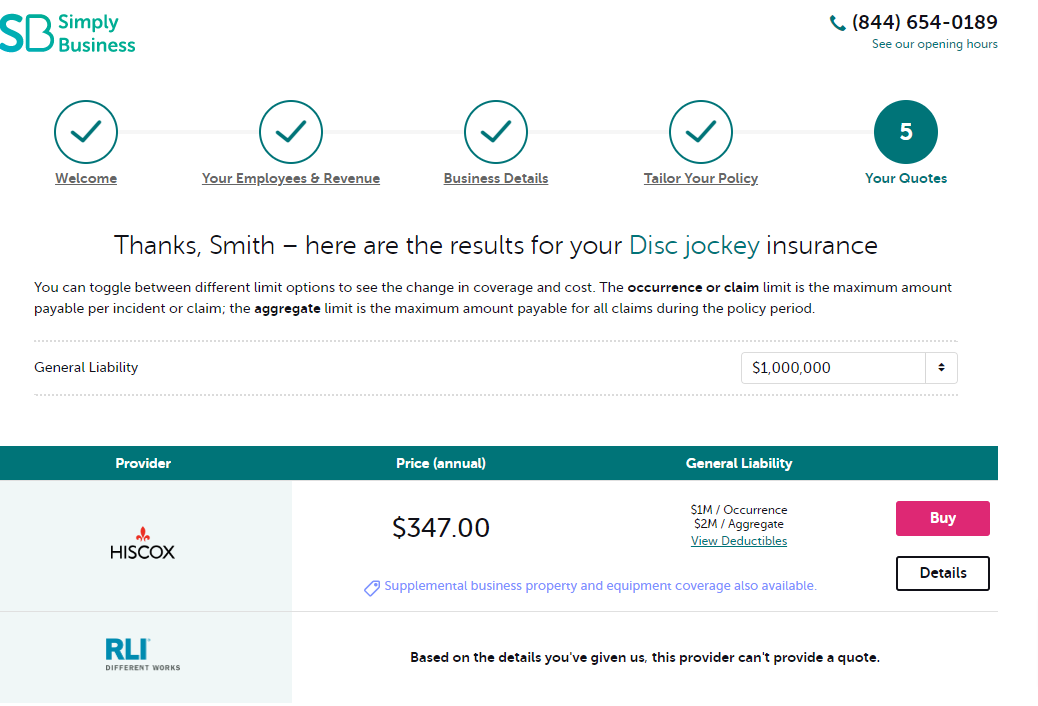

Below is a quote we got from Simply Business for a DJ working at an event. Although Simply Business couldn’t give us a quote for one-day coverage, they were able to find us a very affordable quote, just $29 per month or $347 per year. While a daily plan from InsurePro is already at $28 per day. It may be worth it getting a monthly plan at $29.

Thimble: Best for comprehensive one-day vendor insurance coverage

Thimble’s one-day vendor insurance is accessible to vendors participating at trade fairs, conferences, festivals, marketplaces, and flash retails. The policy only offers $1 million or $2 million in general liability coverage. However, policyholders benefit from Thimble’s vendor insurance because it can be purchased as a short-term policy by the hours, days, weeks, or months. Customers of Thimble who currently have an entertainment and events policy can add vendor insurance to their policy as an additional coverage option.

Pros

- Short-term vendor insurance may be obtained in less than a minute

- Coverage can be obtained online using Thimble’s website or mobile app

- Comprehensive coverage including general liability, professional liability, and performance property protection

- Instant evidence of insurance is provided

Cons

- Coverage is limited to general liability only

- You cannot buy equipment coverage on a daily basis

- Thimble only offers $1 million or $2 million policy limits

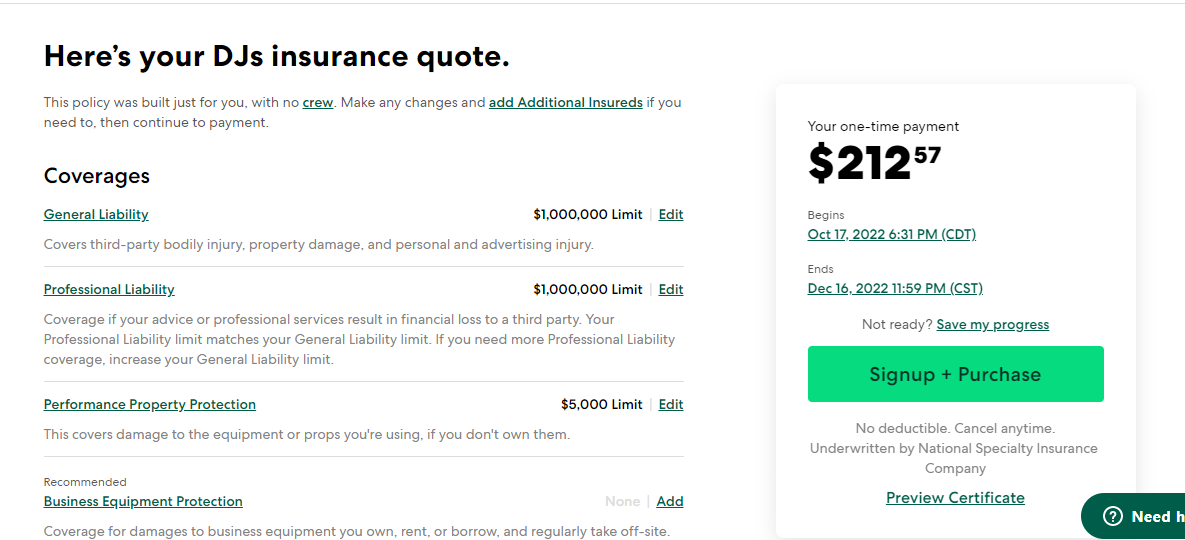

The quote we received from Thimble is for 2 months. For some reason, they couldn’t give us one-day quote online. We had to call them to inquire for an one-day quote.

CoverWallet: Best for comparing quotes from reputable companies

CoverWallet is an insurance broker that makes it simple for vendors to obtain one-day insurance whenever needed. Their online platform for comparing quotes enables you to get quotations from many carriers and see their offerings and prices.

This firm provides one-day insurance policies for food vendors, farmers market vendors, and many other vendors with general liability, workers’ compensation, commercial property, and additional coverage options.

Pros

- Works with reputable carriers only. They work hard to ensure the reputation of their carrier partners

- Quotes are offered online

- Receive free estimates and compare the prices of several carriers online in minutes.

- No hidden charges

Cons

- Coverwallet only sells policies from their partners

- Policy cancellation takes time

NEXT: Best for fast vendor coverage

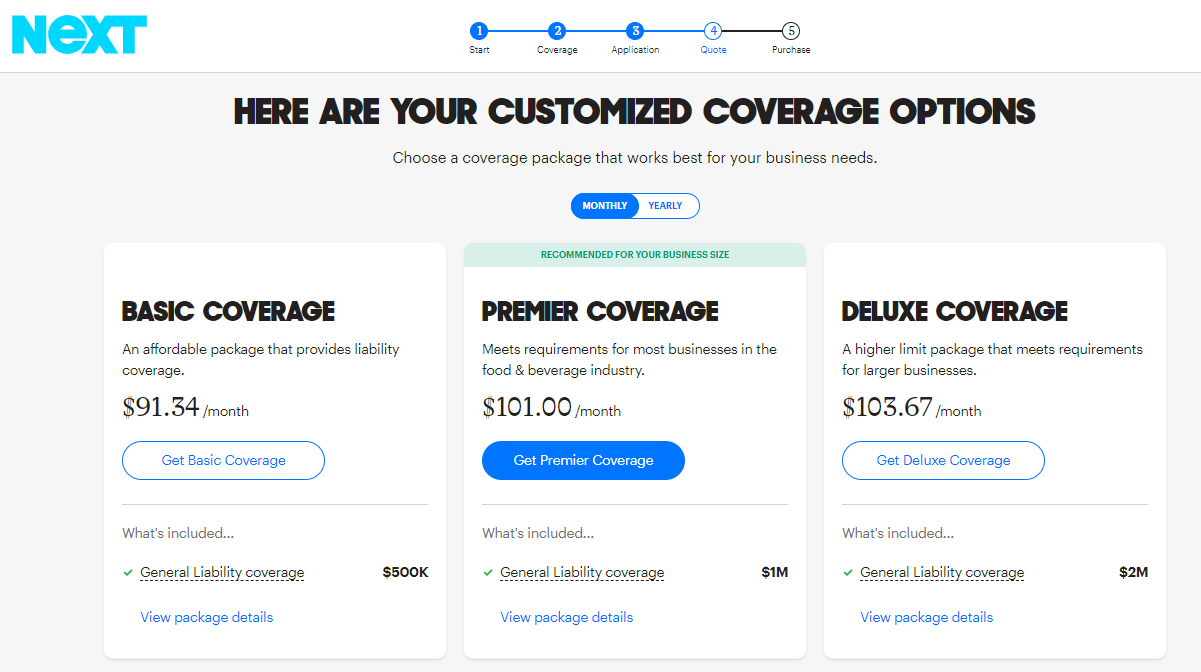

NEXT is now regarded as one of the most successful insuretech businesses. The firm claims it is wholly committed to serving the needs of micro and small businesses, including vendors.

NEXT provides policies for general liability, commercial auto, commercial property, workers’ compensation, business owner’s policy, and other policies that small businesses may need, depending on the location of the companies and the nature of their businesses.

NEXT allows its clients to save money by receiving discounts when they purchase several insurance policies. In addition, it offers an immediate certificate of insurance via its mobile app.

Pros

- Get insured in less than five minutes

- You can obtain discounts

- Get quotes and manage insurance online in one place

- Instant proof of insurance

- Online live assistance that replies promptly

Cons

- Some coverage options are not available in some locations

- Relatively new companies, thus lacking a good claim paying record

What is one-day vendor insurance?

This kind of insurance policy offers protection to vendors for a limited amount of time (often a few hours or days). The policy is also known as one-time event insurance. Typical one-day vendor insurance policies may even include all of the coverages available under an insurance plan for an ongoing event, such as general liability insurance, liquor liability insurance, and rental premises liability insurance, among other coverages.

In addition, some carriers incorporate inland marine coverage in their one-day vendor insurance. Goods in transit insurance will cover the expenses incurred if the things you want to sell at a vending event are lost or damaged en route.

Contrary to its name, one-day vendor insurance coverage is not restricted to the event day. You may prolong the duration of validity by months or weeks. In addition to one-day vendor insurance coverage, insurers provide specialist coverage. The policy includes food vendor insurance for one day, wedding vendor insurance for one day, etc.

Due to the short duration of one-day vendor insurance, it is much more costly than standard vendor insurance in the long run. However, it is a good choice if you do not need regular long-term coverage or if you only insurance for a particular event.

Vendor liability insurance

If you are a vendor, you know that in order for you to participate in an event, you’ll need to have vendor liability insurance. Vendor liability insurance covers the vendor in the event that a third party files a lawsuit against the vendor alleging that the vendor’s product or services or the vendor’s operations caused harm to the third party This type of insurance can help protect the vendor from financial damages associated with a legal claim.

For example, here are some common examples of vendor liability Insurance coverage at a holiday fair would include: the vendor is covered if a patron slips and falls in their booth, if they cause damage to someone else’s property, or if an accident occurs and someone is injured, or if their products, food, or services cause damages to the third party. A good vendor liability insurance policy should provide coverage that general liability, product liability, and liquor liability policies would cover.

Why do vendors need one-day insurance?

Most people make the mistake that vendors are protected by the event organizer’s insurance if a third party claims the vendor was to blame for the incident.

In reality, this is not true. If your business operations cause an accident that causes injuries or property damages, your business will pay for the damages. For instance, if your cooker burns the venue’s wood flooring, you may be held personally accountable for paying to have it repaired or replaced.

How much does one-day vendor insurance cost?

The average cost of a $1M general liability insurance policy covering just one day is $28. This may look cheap. However, if you can get the same policy covering the entire month for just $29, it may not look as cheap anymore. While one-day vendor coverage may be available at a slightly lower price, you may be better off getting a traditional policy and paying the first month.

The cost of one-day vendor liability insurance might vary from service provider to service provider since every event is unique. The price may change based on the nature of the event, the number of people attending, and the dangers posed.

Everyone will get their own rates from different insurance companies. You should try to get a few quotes or work with a broker like InsurePro, Simply Business, or CoverWallet to compare several quotes to find the cheapest one for you.

What are the factors that affect the cost of one-day vendor insurance?

As we mentioned, insurers charge different prices for their one-day vendor insurance. Be prepared to answer questions regarding the event, including its location, date, nature, and activities, while looking for special event insurance.

Such inquiries will determine if the provider will cover the occurrence and the premium amount. Other particular considerations include the following:

Coverage limits:

Your coverage limit is the maximum your insurer is willing to pay if a covered event happens. Increasing the limit of your coverage will result in a premium rise. But then, the additional precaution may be worth the extra pay.

Alcohol sales

While some event liability packages include liquor liability coverage, others need you to acquire this coverage separately. An extra liquor liability will cost you extra.

Predicted attendance

The bigger the attendance at your event, the higher the probability that someone may get wounded. As a result, if you will be vending at a modest company holiday party, you will pay less compared to someone vending at a three-day music festival.

Duration of event

The duration of the event, including setup and breakdown, will undoubtedly influence the cost of event insurance. Usually, the longer your event, the more expensive your insurance.

There are several types of one-day insurance policies for different professions. Below are a few popular ones for your reference.

The following are some of the most common specialized one-day vendor insurance policies.

How to find cheap one-day vendor insurance?

One-day vendor insurance is necessary. Any vendor should have this coverage before participating in an event. Since it is an important coverage, it can be expensive. Below are a few suggestions to find cheap one-day catering insurance coverage:

Compare several quotes from several vendors

The easiest way to get inexpensive vendor insurance is to shop around and evaluate the policies offered by different insurance providers. Consider obtaining price estimates from a minimum of three different insurers to ensure you receive the best possible deal. Work with a broker like Simply Business or CoverWallet to get and compare several quotes is a good way.

Pay your premium in full

It could seem to be more convenient to pay your premium every month. However, if you pay for the whole year’s worth of insurance premiums in advance, you may be eligible for discounts.

If your insurance premium is 50 dollars per month, for example, paying them monthly would result in a total yearly payment of 600 dollars. If you pay for it all at once, on the other hand, it could just cost you $420 to 450, or perhaps even less depending on the insurance company.

Bundle several policies at the same carrier

Customers who purchase numerous policies from the same insurer are eligible for discounts from that insurer. Therefore, if you are interested in saving money on your vendor insurance, you might think about purchasing extra coverage from the same insurance provider.

One-day liquor liability insurance

Alcohol is a fixture at many parties and celebrations since it is used to celebrate accomplishments and milestones. However, selling alcohol to intoxicated visitors without insurance may expose you to several hazards.

In a drunken frenzy, some visitors may ruin and vandalize property, create an accident, or harm themselves. Alcohol insurance for one day protects you against alcohol-related liabilities for the particular day you paid for. The coverage covers medical expenses, legal costs, and settlements associated with such situations.

Learn more at the best liquor liability insurance companies

One-day insurance for bartenders

Bartenders are directly responsible for supplying alcohol at parties, which makes them strong candidates for lawsuits. As a result, the bartender must use discretion and deny service to underage and drunk customers.

If you give alcohol to a drunk visitor or a youngster, you’re liable for any resulting harm. The same is true if an accident occurs under your supervision. One-day bartender insurance protects you against the financial burden of litigation and settlements from any of these scenarios.

General liability and liquor liability coverage are the critical components of one-day bartender insurance. You may also buy professional liability insurance if you want to be covered against claims for mistakes and omissions.

One-day bartender insurance may also contain business car insurance with auto liability coverage that covers your financial obligation in a motor vehicle accident for just one day.

Learn more at the best bartender insurance companies

One-day insurance protection for photographers

Photographer’s one-day event insurance covers general and professional liability for 24 hours. The one-day business insurance protects videographers and photographers from the most frequent disasters.

This policy insures you against physical injuries to third parties, property damage, mistakes and omissions, and property damage with one-day photographer liability insurance.

One-day insurance for photographers also includes coverage for equipment and drones. If your camera is stolen or destroyed while in use, equipment insurance will give reimbursement or a replacement. In contrast, drone insurance covers bodily injury and property damage caused by drone usage.

Some insurers provide event-specific coverage, such as wedding photography insurance for a single day.

Learn more at the best one-day photographer insurance companies

One-day catering insurance coverage

Food vendors who provide catering services may be required to provide proof of insurance by the event organizers. If they already have standard long-term insurance coverage, they should be good. However, if they don’t have standard insurance coverage yet, they may need to get a one-day catering insurance policy. This policy would include general liability and product liability coverage with $1M coverage limit.

Learn more at the best one-day catering insurance companies

One-day event insurance coverage

One-day catering insurance protects you against general, professional, and product liability when catering events, including weddings, parties, and conferences.

The one-day event insurance protects you against property damage and bodily harm that your catering company may cause to customers, suppliers, and third parties.

If they fail to remove safety dangers and employ well-maintained equipment, caterers are accountable for accidents and property losses. One-day catering insurance protects just clients and third parties, although it is helpful if you need a short-term policy to secure a contract.

Learn more at the best one-day event insurance companies

One-day DJ coverage

One-day DJ event insurance coverage protects you against bodily harm and property damage to third parties. You may purchase equipment insurance, which will cover your losses if your DJ equipment is lost or destroyed on- or off-site. The additional policy will cover your records and similar things. However, your software and other data saved on your devices are not backed up.

Learn more at the best DJ insurance companies

Food vendor insurance

A food vendor insurance policy would protect you from accidents that may occur while preparing or serving food to customers. This type of policy would also provide protection if your business was sued for damages caused by a customer. Some examples of accidents that could be covered by food vendor insurance include:

- A customer slipping and falling on a wet floor

- Someone getting sick after eating your food

- A customer being injured by a piece of kitchen equipment

- An electrical fire in your kitchen

To provide coverage for the incidents listed above, a food vendor insurance policy needs to include coverage provided by a general liability insurance and product liability policy. When looking for a good food vendor insurance policy, be sure to look into the coverages carefully to ensure they cover all the incidents above.