How much does vendor insurance cost? That’s a question that many business owners have, but not many people know the answer to. That’s because the cost of vendor insurance can vary greatly depending on the coverage you choose, the company you buy it from, and other factors.

That said, there are some general ballpark ranges that you can expect to pay. For example, basic liability insurance for vendors can start at around $500 per year, but it could be more or less depending on your needs. If you want to include product liability coverage in your policy, that will add to the price. And if you need additional coverage for things like workers’ compensation or property damage, the cost will go up from there.

- How much does vendor insurance cost?

- Average vendor insurance costs for different types of events and locations

- Where to get vendor insurance quotes?

- What factors affect the cost of vendor insurance?

- How to get cheap vendor insurance?

- What does vendor insurance cover?

- Vendors at different types of events and locations: Event vendors; Garage sales vendors; Famer markets vendors; Wedding vendors; Food vendors; and Craft vendors

- Best vendor liability insurance

How much does vendor insurance cost?

Vendors can buy insurance for different periods, depending on their needs. 3-day coverage of vendor insurance can cost as little as $45 only.

If you need permanent long-term coverage, you can get a traditional policy with monthly coverage. The average cost of a $1M general liability insurance policy for vendors is $55 per month, or $660 per year. However, vendors can choose different coverage periods depending on their needs. Below are the average costs of vendor insurance for different periods:

| Different coverage periods of vendor liability insurance | Average costs |

| 3-day coverage | $45 |

| 7-day coverage | $89 |

| 90-day coverage | $139 |

| Monthly coverage (permanent long-term policy) | $55 per month |

These are just the average rates. Your rates will be different. Be sure to shop around with a few companies or work with a broker like InsurePro, Simply Business, and CoverWallet to get and compare several quotes to find the cheapest one for you.

Average vendor insurance costs for different types of events and locations

Vendor insurance comes in different types depending on your company. The following are some common types. Because vending is a low-risk sector, insuring your small company is generally relatively inexpensive.

A $1 million general liability policy for any of the following types will cost about $19 -$100 per month. This works out to $228 – $1,200 each year. We recognize that this is a wide range, and that is because vendors at different types of events and locations are exposed to different types of risks. Below are the summary of vendor insurance costs for different types of events and locations.

| Different types of events and locations | Average vendor insurance costs |

| Event vendors | $34 per month |

| Garage sale vendors | $18 per month |

| Farmer market vendors | $26 per month |

| Wedding vendors | $36 per month |

| Food vendors | $47 per month |

| Craft vendors | $23 per month |

Where to get vendor insurance quotes?

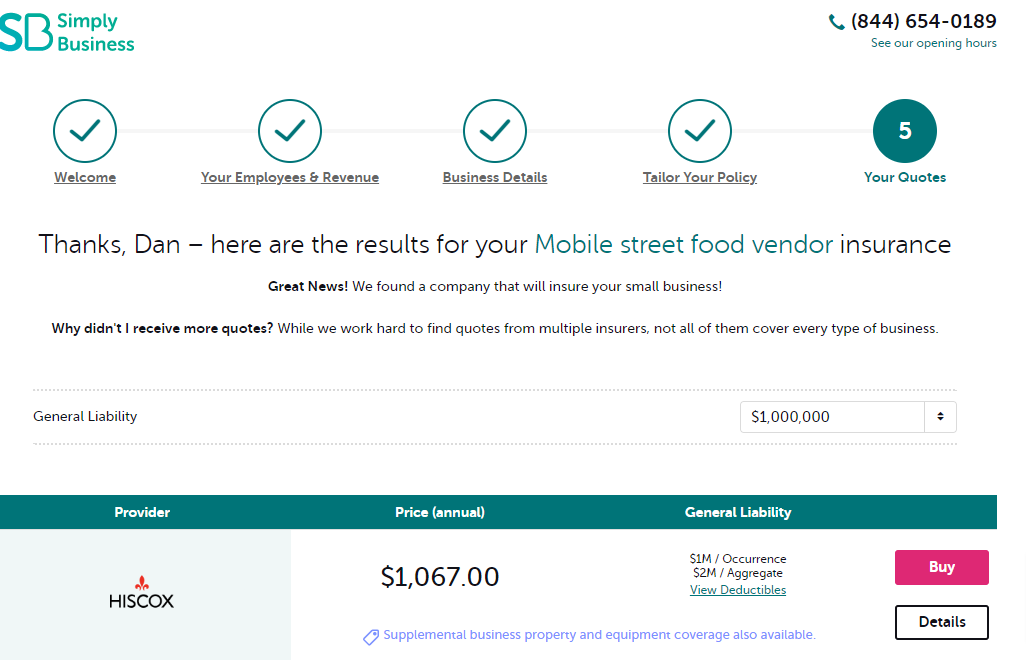

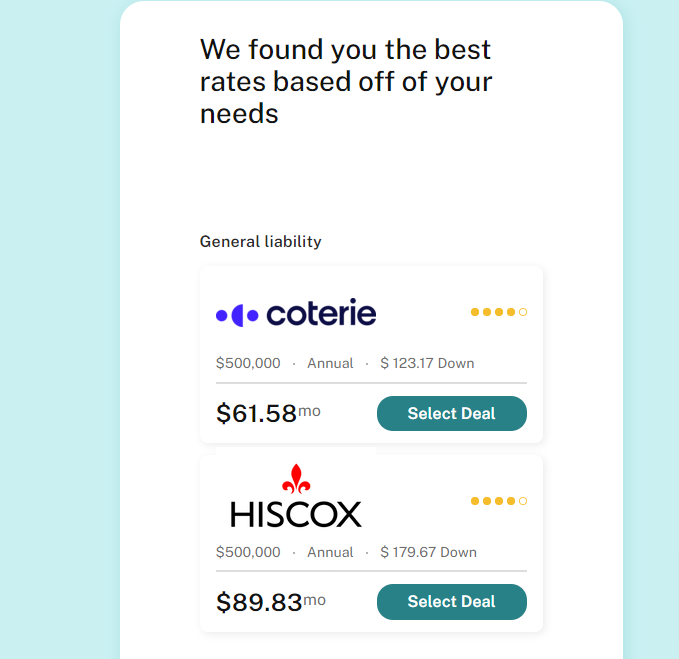

Getting and comparing several quotes is the best way to find the cheapest quotes for yourself. Only a few companies offer quotes online. We have tried a few and below are some of the best companies offering vendor insurance quotes online:

- Simply Business: Best for finding low-cost vendor insurance coverage

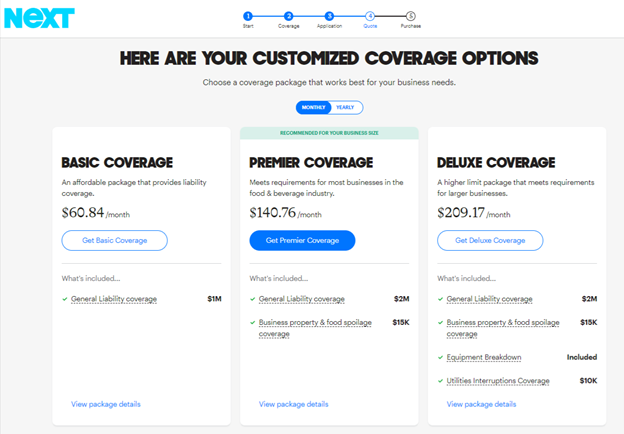

- NEXT: Best for fast quote and reasonable rates

- InsurePro: Best for short-term pay-per-day coverage

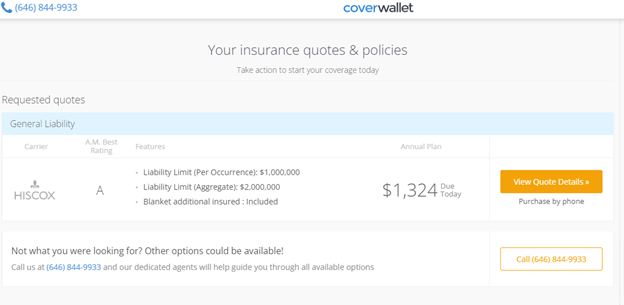

- CoverWallet: Best for comparing several quotes from top-rated carriers

The following are some vendor insurance quotes from some top insurance companies.

What factors affect the cost of vendor insurance?

Here are a few factors that affect the cost of your insurance:

Coverage periods

As we learn above, vendors can get coverage for different periods depending on their needs, from one day, to 3-day, 7-day, 30-day, or even 90-day coverage. The rates are different for different periods. Sometimes it may make sense for vendors to get a permanent, long-term policy and pay the premium monthly.

Annual and anticipated gross sales

Vendors with more sales and revenue typically pay more for their vendors’ insurance. More sales and more revenue means that they are likely to have more customers and more activities, which increases the risk of accidents and lawsuits.

Previous insurance claims

The more claims you had in the past for vendor’s insurance or any other type of insurance, the more the cost of your insurance.

Type of merchandise sold

Vendors that sell food and costly items like jewelry tend to pay more for their vendors’ insurance.

Years of practice

Vendors that have been selling items for an extended period tend to pay less for their insurance. This is because they are more experienced in running their operations and less likely to make mistakes or cause accidents.

How to get cheap vendor insurance?

Your insurance prices are determined by a variety of things. However, if you want to ensure that you acquire affordable vendor insurance, consider doing the following:

Compare quotes

Comparing quotes from many insurance companies is the best approach to acquiring a fantastic bargain and affordable vendor insurance. To be sure you are getting the best deal, consider obtaining quotes from about three insurers.

Pay your premium in full

Paying your premium monthly might seem easier. But when you pay for the whole insurance premium a year in advance, you get discounts. For instance, if your insurance costs 30 dollars monthly, paying every month will cost 360 dollars annually. However, if you pay outrightly, it might only cost you 300 dollars or even less, depending on the insurer.

Sign up for automatic billing.

Automatic billing is an alternative to paying annually. Some insurers may offer discounts if you allow them to deduct monthly payments automatically.

Buy multiple insurance policies

Insurers offer discounts to clients that buy multiple policies from them. So if you want a discount, consider combining your vendor insurance with additional plans from the same company.

Request higher deductible

Although this is not a good idea, it can help reduce the cost of your insurance. Your deductible is the amount you pay to cover an incident. Choosing a higher deductible means you will pay more if a covered incident occurs.

Improve your credit rating

Your credit rating speaks a lot about you. It tells the insurer how risky it is to insure your business. To get better insurance, ensure you have good credit scores.

What is vendor insurance?

Simply put, vendor insurance protects your firm against claims and lawsuits arising from its involvement as a vendor at an event. This could include claims based on foodborne diseases, injuries, or property damage.

In the event that a claim is brought against your business for injuries or damages that occurred during an event at which you were a vendor, your insurance would cover the costs of defense and claims up to the limits of your policy.

For example, one of your staff spills water on an expensive phone and damages it, and the event manager holds your company responsible for the replacement cost. Your vendor’s insurance might help your business pay to replace the phone or, if you so choose, defend you in court against the event manager’s claim.

What does vendor insurance cover?

Vendor insurance provides the comprehensive protection that vendors require by combining many coverages. Typically, a vendor’s insurance package will consist of the following coverages:

General liability insurance for vendors (CGL)

General liability insurance is the most basic insurance requirement for vendors. The policy protects you if your business is accused of causing bodily harm or property damage. Typically, the event organizers will carry liability insurance, but you may be required to have your own CGL policy.

Suppose you were a food vendor, someone stumbled over your tent’s rope. Regardless of the lawsuit’s outcome, CGL may cover the cost of medical expenses and legal fees if a customer is hurt and sues you.

Product liability insurance for vendors

This policy is necessary for vendors that make, distribute, or sell any product, including food. This coverage protects you financially against claims of alleged property damage or bodily injury caused directly by your goods.

Three of the most prevalent causes of product liability lawsuits are:

- Design flaws (the product’s design is unsafe or faulty)

- Manufacturing defects (errors during the production process)

- Marketing problems (such as incorrect instructions or a lack of safety warnings)

Suppose a consumer is injured by a product you produce and sell due to the above; product liability insurance could cover the lawsuit and associated costs.

Commercial property insurance for vendors

Vendors’ commercial property insurance provides financial protection for your products and business-related equipment from unforeseen perils, such as fire, theft, and flooding. For instance, if your merchandise and equipment were damaged by a flash flood at the market, this coverage may give the funds necessary to restore or replace them.

Vendor event insurance

Vendor event insurance is a sort of vendors insurance coverage that, as its name suggests, applies when a vendor is involved in the following:

- Charitable and fund-raising activities

- Comic book and gaming conventions

- Football and race activities

- Other occasions

- Performing arts

- Trade fairs and expositions

The insurance provides primary general liability and property coverage while the vendor is at these events. General liability covers slips and falls, tripping, and fire outbreaks that vendors may cause due to inadequate crowd and space management. Property insurance, on the other hand, will protect against theft and stock damage.

Before working with a vendor, some event organizers look for a certificate of insurance, making this policy crucial. Vendor event insurance comes with a certificate of insurance, depending on the provider. A certificate of insurance is evidence that a vendor is insured and will not transfer liability to event organizers.

Insurance for garage sale vendors

Insurance for flea market vendors includes both general liability and product liability coverage. General liability coverage safeguards flea market vendors against accusations of deceptive advertising and physical injury. In contrast, product liability will reimburse any costs incurred when a buyer purchases a defective, used item.

This insurance is vital since vendors in flea markets offer used products. Unlike brand-new objects, flea market vendors bear risks associated with potentially defective products. Antiques sold at flea markets can easily have quality and customer safety concerns.

Vendors that sell items like toys, thermometers, and furniture are usually the most affected because these items are more prone to degradation. With degradation, these items can trigger allergic reactions.

Severe allergies can result in customer harm claims resulting in heavy lawsuits for medical expenses, lost income, pain and suffering.

False advertising and product faults are additional issues that flea market vendors may encounter. If a client is determined to make life difficult for the vendor, he can sue for a temporary suspension of the vendor’s selling license on the grounds of misleading advertising and product defects.

Farmers market vendor insurance

Like flea market vendors, farmers market vendors are vulnerable to legal action. Vendors can be sued for many reasons; however, slip-and-fall incidents are the most prevalent cause.

In addition to causing accidents to customers, the tents of vendors at farmers’ markets also pose a hazard. Accidents related to tents occur when:

- A consumer trips on the tent’s ropes or weights

- Powerful winds dislodge the tents

- the tent umbrella suddenly opens and strikes a person in the face or eyes

Some of the factors that may contribute to slip and fall accidents include the following:

- Electrical cords of stalls or tents improperly maintained

- Liquid spilling (oil, gasoline, or water)

- Soggy grass or soil

Farmers’ market organizers may be held accountable for injuries caused by or allegedly caused by vendors. Customers typically turn to the farmers’ market managers if the merchants in question lack coverage.

To prevent this, farmers’ market managers typically prohibit the sale of goods by anyone who lacks farmers’ market vendor’s liability insurance.

In addition, sellers must ensure that their liability insurance permits the inclusion of an extra insured. This is because most farmers market organizers wish to be covered by the sellers’ vendor liability insurance if a client files a claim against all parties involved.

Wedding vendor insurance

Customers’ desire for the finest wedding places a great deal of pressure on wedding vendors. Every couple wants everything to be flawless. That means error-free invitation cards, spotless flowers and lights, beautiful wedding decorations, a good location, and proper organization of the wedding program.

As a result, couples pay lots of money to ensure nothing goes wrong. If something goes wrong, you can be sure that most couples will not accept simple apologies. Many couples will want to sue their vendors to pay for damages.

The most typical reason couples sue wedding vendors is for breach of contract. Couples may also file a lawsuit if the vendor’s delivery differs from what he promised or if critical wedding supplies were not delivered on time.

In situations like this, wedding vendors may incur attorney expenses that can crawl up to thousands of dollars. In addition, if the action is lost, wedding vendors may be required to reimburse the client plus punitive damages and other penalties imposed by the court. Therefore, wedding vendors must obtain general liability insurance coverage for products and completed operations.

Food vendor insurance

Food vendors can cause bodily injuries and property damage if they are not careful. For example, if a food vendor is not careful with their cooking equipment, they could easily start a fire that would damage the property where they are set up. In addition, if food is not stored or prepared properly, it could make people sick and result in a lawsuit. That’s why food vendors need insurance to protect themselves from these risks. Insurance will help cover the costs of any damages caused by the food vendor, as well as any medical bills that might be incurred as a result of someone getting sick.

At a minimum, food vendors should get general liability insurance with product liability coverage addon. They can also consider a separate policy for product liability.

Craft vendor insurance

Most artisans set up at flea markets, farmer’s markets, festivals, or events. Therefore, craft seller insurance covers potential disasters at vending sites. For artists such as sculptors, weavers, metalworkers, potters, and clock smiths, this insurance is available as a short-term or annual policy.

If purchased as a short-term policy, craft vendor insurance provides just basic general liability coverage for a maximum of three months. As an annual standard insurance policy, however, it includes coverage for general liability, product liability, business personal property, and false advertising for a year or a month.

Best vendor liability insurance

Hundreds of insurance companies offer vendor liability insurance. We have researched more than 30 companies and evaluate their pros and cons of their products and their overall strengths and weaknesses as insuance companies. Here are our recommendations of the best vendor liability insurance companies for your consideration:

- InsurePro: Best for on-demand short-term vendor general liability insurance

- Simply Business: Best for finding low-cost vendor liability coverage

- NEXT: Best for a great digital experience and competitive rates

- CoverWallet: Best for comparing several quotes from top-rated carriers

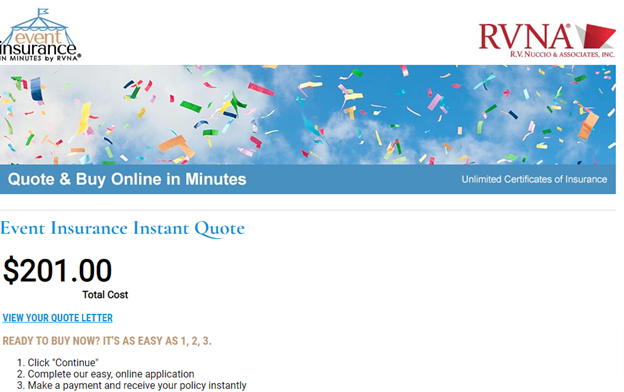

- RVNA: Best for event vendors