In 2015 B.C., the first workers’ compensation laws in history were passed in ancient Sumer, which is present-day Iraq. It took several thousand years for Wisconsin to pass the first comprehensive workers’ compensation law in the United States in 1911. Mississippi was the last state to pass workers’ comp legislation in 1948.

Between those milestones and in the intervening years, the workers’ compensation system in the United States has become a confusing patchwork of state laws.

In this article, we’ll explain everything small business owners must know about workers’ compensation insurance so you can get the coverage you need to protect your employees and comply with state laws.

- What is workers’ compensation insurance?

- Who needs workers’ compensation insurance?

- Who isn’t required to get workers’ comp insurance?

- Workers’ comp insurance for self-employed workers or business owners

- Workers’ comp insurance for independent contractors

- What does workers’ compensation insurance cover?

- How does workers’ comp coverage differ from liability coverage?

- How do I get coverage?

- How much does workers’ compensation insurance cost?

- How do I find the cheapest workers’ comp insurance coverage?

What is workers’ compensation insurance?

Workers’ comp insurance protects employers and their employees against financial losses associated with work-related injuries or illnesses. Most states require small businesses with employees to get coverage. In return, employees can no longer sue over injuries and illnesses that can be traced back to the work they do.

Who needs workers’ compensation insurance?

Most states have laws that make getting workers’ compensation insurance a requirement for businesses that have employees. Different worker exemptions exist in different states and I cover them in the top ten states by population in the next section.

Choosing not to secure workers’ comp insurance can put your business at significant financial risk. Employees or their families could sue you over workplace-related injuries, disabilities, or deaths. Your state could also fine you for breaking the law, prevent you from conducting business, or worse.

Here’s another way to think about it. Worker’s compensation insurance doesn’t just protect your employees, but your small business, as well. If your workers’ comp coverage is compliant with your state laws, employees who receive benefits cannot sue you for their injuries, lost wages, pain, or suffering. If they find a legal loophole and sue you, workers’ comp will pay your legal costs if you have the coverage.

Who isn’t required to get workers’ comp insurance?

Let’s look at the top ten states by population to see how they carve out exemptions for coverage.

California

California is one of the most demanding workers’ comp states. It only allows two exemptions to getting coverage:

- Sole proprietors who decide they don’t want it don’t have to get it

- Employers who are allowed to self-insure, meaning they create their own workers’ comp payment fund.

Learn more at the best workers comp insurance companies in California.

Texas

Employers do not have to carry workers’ compensation coverage in Texas, except for private employers contracted to work with the state government.

Learn more at the best workers comp insurance in Texas

Florida

Businesses with four employees or more must carry workers’ compensation insurance in Florida. Some exceptions include:

- Businesses in the construction industry must purchase coverage if they have one or more employees (this is an industry, not a state requirement)

- Agriculture businesses don’t have to provide coverage unless they have six or more non-seasonal employees and/or 12 seasonal ones

- Independent contractors don’t need to get coverage.

Learn more at the best workers comp insurance companies in Florida

New York

Employers in the Empire State are required to have workers’ comp coverage. Exemptions include:

- Certain real estate salespersons, media sales reps, insurance agents, and brokers who work under an independent contractor contract

- Coaches and athletic team supervisors operating on a nonprofit basis as long as they aren’t professional athletes or work for a professional athletic organization

- People who volunteer their time and services to nonprofit organizations and do not receive compensation for it

- People who work in religious positions, including:

- Ordained, commissioned, or licensed ministers, priests, and rabbis

- Sextons

- Christian Science readers

- Members of religious orders

- Federal government employees protected under federal workers’ compensation laws

- Interstate railroad employees insured by another workers’ compensation system

- New York City police officers, firefighters, and sanitation workers covered by the New York State General Municipal Law

- People who teach at nonprofit religious, charitable, or educational institutions

- People who work for nonprofit religious, charitable, or educational organizations that don’t do manual labor

- Anyone who receives support from a religious or charitable institution and does work in return and aren’t under contract to do that work

- People who work in certain maritime trades

- People, including minors, who do yard work or other chores for pay in and around one-family, owner-occupied homes, or for nonprofit, noncommercial organizations

- Sole proprietors, partners, and one or two-person corporate offices that have no one providing business services to the organization.

- Spouses and minor children of farmers, not contracted to work for the farm business.

Learn more at the best workers comp insurance companies in New York

Pennsylvania

Pennsylvania employers with one or more people working for them must provide coverage. Some exemptions include:

- Casual workers

- Certain agricultural laborers

- Domestic workers not covered under the Workers’ Compensation Act

- Executive officers who have been granted an exemption by the Pennsylvania Department of Labor and Industry

- Federal government employees

- Licensed real estate people or associate real estate brokers

- Longshoremen

- People who have been given an exemption due to religious beliefs by the Pennsylvania Department of Labor and Industry

- Railroad workers

- Sole proprietors, partners, and corporate officers.

Learn more at the best workers comp insurance in Pennsylvania

Illinois

If you have a single employee in Illinois, even a part-time one, you must purchase workers’ compensation insurance. The only exceptions are for:

- Real estate agents

- Sole proprietors, partners in a business partnership, and corporate officers.

Learn more at the best workers comp insurance companies in Illinois

Ohio

All employers in Ohio must provide coverage. Exemptions to this include:

- Family farm corporate officers

- Individuals doing business as a corporation with no employees

- Limited liability companies that act as partnerships or sole proprietorships

- Partnerships

- Sole proprietors

- Ordained or associate ministers of religious organizations.

Learn more at workers comp insurance Ohio: How it works and How much it costs

Georgia

Businesses with three or more employees in Georgia must carry workers’ comp coverage. The only exemptions to this are sole proprietors and partners in a partnership.

Learn more at the best workers comp insurance in Georgia

North Carolina

All North Carolina employers with at least one person working for them must provide coverage. Exemptions include:

- Casual employees

- Certain agricultural product sellers and producers

- Certain railroad workers

- Domestic workers employed directly by a household

- Farms with fewer than ten full-time, non-seasonal farm laborers who are regularly employed by the same farm

- Federal government workers

- Sole proprietors, partners, and corporate officers.

Learn more at the best workers comp insurance companies in North Carolina

Michigan

All employers regularly employing one or more employees 35 hours or more per week for 13 weeks or longer during the preceding 52 weeks must provide workers compensation insurance coverage. Exemptions include:

- Agricultural employees who work for businesses with fewer than three employees putting in less than 35 hours per week

- Domestic employees who work for a household with fewer than three domestic employees who put in less than 35 hours per week.

If your business isn’t exempt from getting workers’ comp insurance, take steps today to get the coverage you need. If you don’t have the required coverage, employees could sue you over a work-related illness or injury, and you could face state fines and other legal consequences.

Learn more at the best workers comp insurance companies in Michigan

Workers’ comp insurance for self-employed workers or business owners.

As covered in the previous section, state laws usually require that employers get workers’ compensation for the people who work for them. Still, coverage is typically optional for self-employed people who have no one working for them. There are some situations where getting workers’ comp makes sense for them:

- They work in a high-risk industry: People in some professions face a higher likelihood of getting injured while at work. Repetitive movements, exposure to harsh chemicals or allergens, and doing manual labor are a few work situations where it might make sense for a self-employed worker or business owner to get workers’ comp.

- They need to meet state requirements. Coverage isn’t always optional for self-employed people. For example, in California, roofers must carry workers’ comp whether they have employees or not.

- They must meet contract obligations: Self-employed people may find that other businesses will only agree to work with them if they have workers’ comp coverage because it limits their liability if there is an on-the-job injury.

Since state laws differ, if you’re a self-employed person or business owner, it’s a good idea to consult with a business insurance expert to see if it makes sense for you to get workers’ comp coverage.

Learn more at the best workers comp insurance companies for the self-employed

Workers’ comp insurance for independent contractors

If you’re an independent contractor, your state will likely not require you to purchase workers’ comp coverage. However, if you work as a general contractor or subcontractor, you may need to get workers’ comp if a contract requires it.

Also, if you’re an independent contractor, you should be aware that health insurance policies usually do not cover injuries and illnesses resulting from work-related incidents.

Example: You are an independent contractor working as a decorator. You have health insurance. One day while you’re working, you lift a piece of furniture and injure your back. Your health insurance may not cover related medical costs because your back injury happened while working.

This example demonstrates why it’s essential for independent contractors to have workers’ comp coverage – even if they have health insurance. It can help prevent them from having to pay large healthcare bills out of pocket.

Learn more at the best workers comp insurance companies for independent contractors

What does workers’ compensation insurance cover?

If an employee suffers a work-related injury or illness, worker’s comp will help cover their:

- Medical costs

- Lost wages

- Ongoing healthcare expenses

- Funeral expenses (along with survivor benefits to family members)

- Job retraining costs

- And more.

Here’s an overview of the standard workers’ comp coverages:

Medical expenses

Workers’ comp insurance helps employees pay for medical expenses related to a job-related injury or illness, including things like emergency room visits, doctor appointments, surgeries, and prescription drugs.

Example: If one of your carpenters cuts his hand while remodeling a customer’s home, workers’ compensation insurance can help cover his hospital visits and ongoing treatment.

Illness

There are situations when working conditions expose employees to harmful chemicals or allergens that cause illness. If a worker becomes sick because of exposure in the workplace, workers’ comp insurance will help cover their costs for necessary treatment and ongoing care.

Example: An employee at a cabinet factory is exposed to noxious fumes and dust in the workplace for years. This situation causes severe lung and breathing issues. Workers’ comp will cover related medical care and ongoing therapy.

Missed wages

Workers’ compensation helps replace some of an employee’s lost income if they have to take time off to recover from a job-related injury or illness.

Example: If a chef at your restaurant burns her arm on a fryer and can’t work because of it for a month, workers’ compensation coverage will replace some of her lost wages.

Ongoing healthcare

What happens if a work-related injury or illness is so severe that your employee needs treatment over a long time period? Workers’ comp will cover all those treatments.

Example: If a worker hurts her back when lifting heavy boxes at your store and her physical issues last a long time, workers’ comp insurance will cover her ongoing costs for physical therapy.

Funeral expenses

If an employee loses their life because of a job-related accident, workers’ compensation insurance will help cover funeral costs and provide death benefits to immediate family members.

Example: A car strikes a roadway construction worker, and he dies on the job. Workers’ comp will pay funeral costs up to a certain limit and his beneficiaries will receive a payout.

Repetitive injury

Not all job-related injuries happen because of a single incident. Injuries that result from repeated movements, such as carpal tunnel syndrome, can take months or years to occur. Workers’ comp will pay for therapy and other treatments.

Example: If your administrative assistant develops carpal tunnel syndrome after years of typing while sitting at an uncomfortable desk and chair, workers’ comp can help cover treatment costs and ongoing healthcare bills.

Disability

Some workplace injuries are severe enough to temporarily or permanently disable a person, preventing them from working. Workers’ compensation coverage provides disabled workers with benefits that pay their medical bills and replace a portion of their lost wages.

Example: Your warehouse foreman loses the use of one of his arms in a work-related incident and cannot do his job because of it. He needs continued medical and financial support. Workers’ comp will cover his treatment costs and supplement some of his missed wages through disability benefits.

Job retraining

If a workplace injury makes it impossible for someone to return to doing the work they usually do, workers’ comp will pay to retrain them for a new position.

Example: A clerk in a retail store falls off a ladder and breaks her leg. It doesn’t heal correctly and she is unable to stand for long periods of time, so she can’t return to her job. Workers’ comp would pay to retrain her to handle office duties.

What does workers’ compensation insurance NOT cover?

Every state has different workers’ compensation regulations; however, there are certain situations it won’t cover ever. Here are a few of them.

Commuting to and from work

If someone is injured while getting to or coming home from work, the coming and going rule usually applies. According to it, travel to and from your regular work site is not considered part of your employment.

Example: If a car strikes an employee during their regular morning commute to the office, any injuries from the incident are not covered by workers’ comp.

Note: There are some exceptions to this rule, mainly if someone drives a company car, doesn’t have a specific worksite, or runs a work errand before going to the office. For example, a traveling salesperson might get workers’ compensation benefits if she got hurt while driving from home to her first morning appointment with a client. Similarly, an administrative assistant injured while picking up her boss’s dry cleaning on the way to work may be covered.

Recreational activities

Many businesses host team building and recreational events for their workers. How an injury happens at a company picnic, softball game, holiday party, happy hour, or other event, will determine whether or not it will be covered by workers’ comp insurance. Here are some things that make it more likely it will be covered:

- The employee was required to attend the event or believed his attendance was mandatory

- The employer benefited from the employee’s attendance at an event (for example, the injured worker participated in a brainstorming session)

- The activity took place on business premises during regular work hours.

However, if an event is entirely voluntary and for the employee’s benefit only, an injury that happens at it will typically not be covered by workers’ comp insurance.

Example: A worker goes to a baseball game at the invitation of their employer. It’s an opportunity for people who work together every day to have some fun. The employee slips on the steps on the way to her seat and breaks her leg. It’s unlikely workers’ comp will cover the injury.

Intoxication or drug use

Most state workers’ comp regulations exclude injuries that occur because a worker is drunk or incapacitated due to drug use.

Example: If a painter falls from a scaffold because he was drinking on the job, the workers’ comp claim will likely be denied.

Horseplay and fighting in the workplace

Horseplay, fighting, practical jokes, and other similar things aren’t considered a part of a person’s regular employment, so injuries resulting from these types of things are typically not covered by workers’ comp. However, there are some exceptions to this rule. An example is a business owner who allows horseplay in his workplace. It is more likely a related claim would be approved in this case. The same is true if an uninvolved person is injured because of horseplay. Workers’ comp would probably cover her injuries.

Similarly, most injuries caused by fights in the workplace are not covered by workers’ comp. An exception is if an argument is over a work-related issue, such as a dispute over a manufacturing problem. If this can be proved, workers’ compensation may take care of related injuries.

Examples: If someone gets into a fight with a coworker about a sports team, injuries related to it will probably not be covered. However, it may be covered if an employee hits a coworker after he complains about how she treated a customer.

These exceptions vary by state. A state workers’ comp expert or insurance professional will be able to tell you what’s not covered by your insurance.

What other coverages do small businesses typically need?

Instead of purchasing workers’ comp insurance as a stand-alone, many small business owners find it cheaper to buy it as an add-on to their Business Owners Policy (BOP).

Depending on the coverage you choose, a BOP helps protect your business building and property against financial losses related to things like theft, fire, wind, falling objects, and lightning. It is similar to the insurance coverage on your home or apartment.

Many businesses add some of the following coverages to their BOP:

- General liability: Covers medical and legal costs if a customer or visitor is injured on your business property.

- Business interruption: Covers you if you cannot conduct business at your business location because of things like a fire or damage from a severe weather event or utility work.

- Professional liability: Pays costs related to errors made while providing services to clients and customers.

- Errors and omissions: Provides coverage if you or someone who works for you makes a mistake, provides inadequate information to a customer, or misrepresents the products you sell or services you offer.

- Cyber: Pays expenses related to the loss or theft of personal or company information.

- Business auto: Covers vehicles used to conduct business.

Of course, workers’ comp would be a part of this package if you have employees.

This is only a small sampling of the business coverages available. An online business insurance application system, insurance agent, or insurance company representative can help you identify the coverage your business needs.

How does workers’ comp coverage differ from liability coverage?

Workers comp only covers people who work for you. If a client, customer, or random person is injured at your workplace or job site, general liability insurance will cover it. General liability covers bodily injury and damage caused by you or an employee to someone else’s property.

How do I get coverage?

In most states, there are three ways to get coverage:

Private insurance companies:

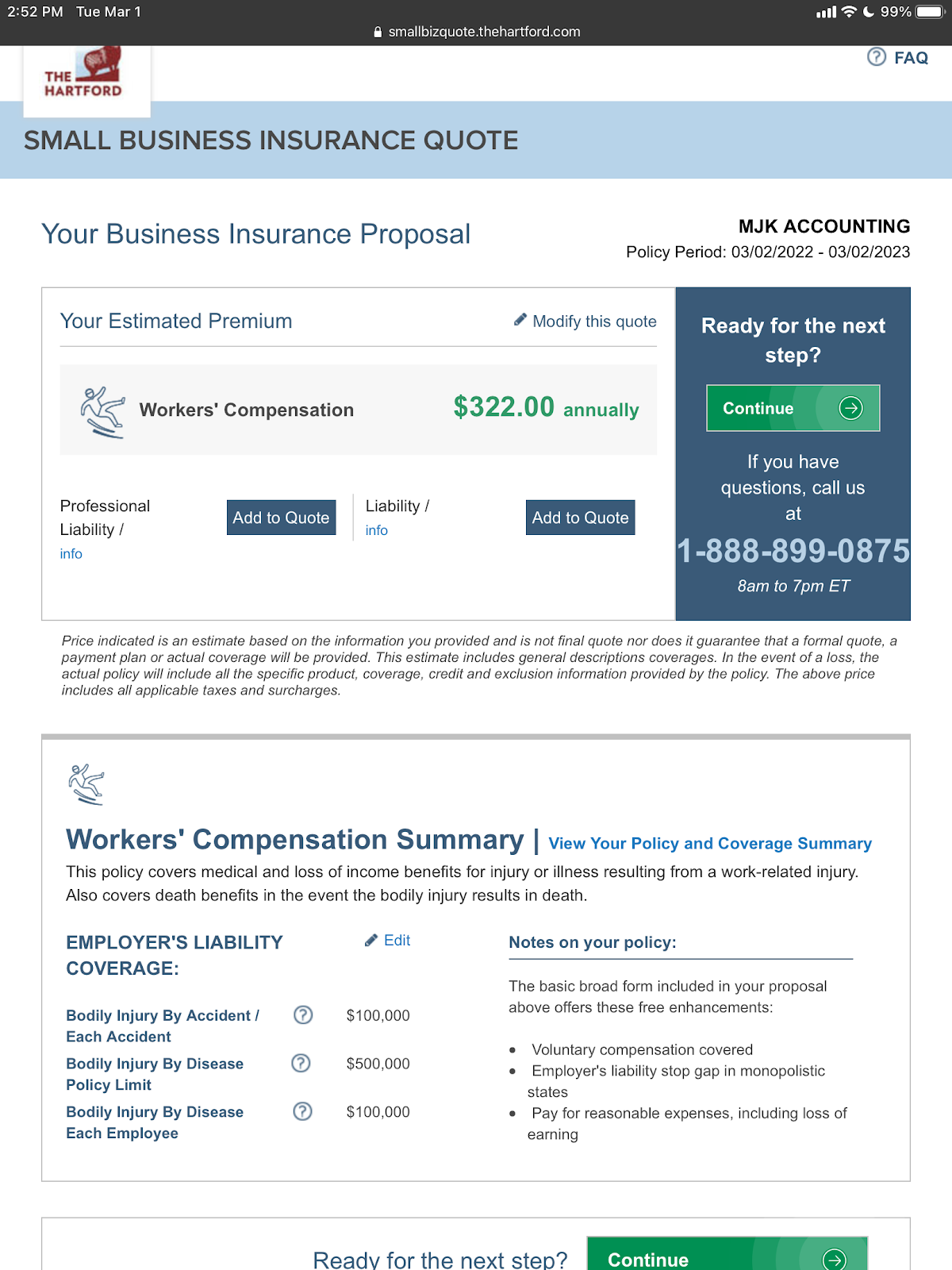

Private insurance companies are authorized by most states to write workers’ compensation insurance policies. These usually include traditional insurers and online ones. For example, the Hartford, Liberty Mutual, Travelers, Chubb, Employers, etc. or Pie, Cerity are newer companies, or also called insuretech startups.

Many of these companies sell workers comp insurance through their agents, but some have offered quotes and allow small businesses to buy online. Below is a quote sample we got from Liberty Mutual

Public insurers:

Some states have insurance funds, which are self-supporting insurance carriers that write workers’ compensation insurance policies for businesses in their state. They can be good options for companies that find it hard to get coverage, although premiums may be higher than regular insurers.

Individual self-insurance:

In some states, large employers can set aside reserves for insuring their businesses in a highly regulated process.

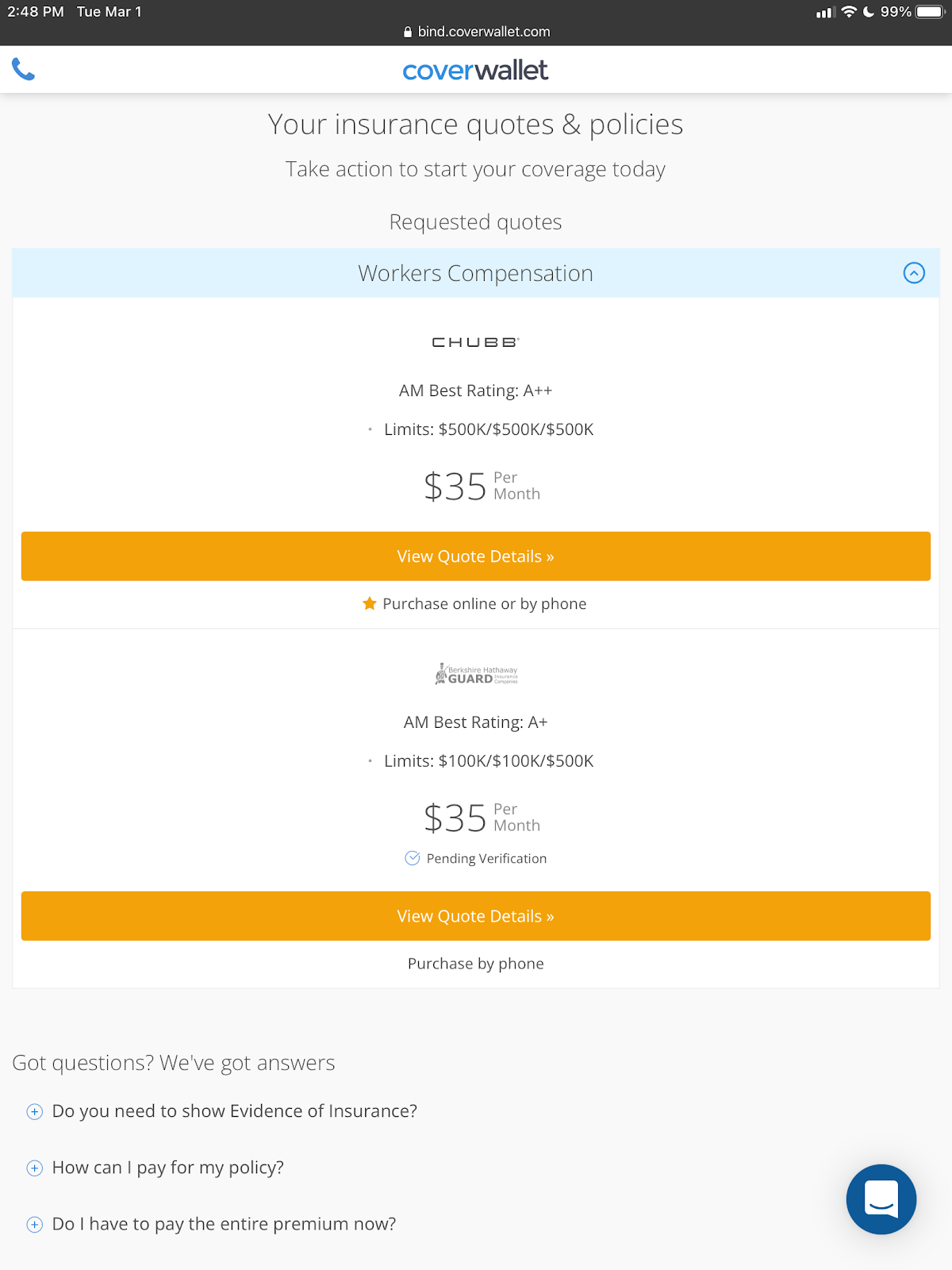

Digital brokers or traditional brokers

Small business insurance is generally more complicated than personal lines of insurance. Working with a broker will help you understand the nuances and select the right coverages. The same goes for worker comp insurance. In addition, working with a broker, especially a digital one will make it very easy for you to compare several quotes to select the cheapest one for your company since these brokers work with several companies and they are able to qull quotes from these companies for you to compare in one place. CoverWallet, Policy Sweet, Commercialinsurance.net, or SmartFinancial are good examples of digital brokers. Below is a quote sample that we got from CoverWallet.

How much does workers’ compensation insurance cost?

Premiums vary and are based on several factors, including:

- Payroll

- Location

- Number of employees

- Employee job responsibilities

- Industry and related risk factors

- Coverage limits

- Claims history.

An insurer that offers workers’ comp insurance in your state or a state workers’ comp fund can provide you with premium quotes. It’s a good idea to get quotes from multiple providers so you can compare costs to find the best deal for your business.

How do I find the cheapest workers’ comp insurance coverage?

Here are some things you can do to find the insurance you need at the best possible price:

- Shop around for the best value. Get quotes from several companies so you can compare premium prices.

- Don’t stop shopping around. Make sure you get new quotes before you renew your policy every year.

- Ask for recommendations. Another business owner may be able to recommend an affordable provider to you.

Taking these steps will help ensure you’re not paying too much for your workers’ comp coverage.

Learn more at the cheapest workers comp insurance companies

How does workers’ compensation insurance settlement work?

Filing a claim is the first step to making a settlement. Visit your insurance provider’s workers’ compensation claims page, where you should find the forms, tools, and information you need to make a claim.

When you file a claim, have the following information available:

- The exact date of the injury, illness, or death

- Type of injury or illness

- Impacted body parts

- The first and fifth day your employee missed work

- Doctor your employee is seeing.

Once a claim is filed, your insurer will review the information you provide and decide whether to approve it and make a payout or deny it. There could be some back and forth during the review process, especially if anything in the application is unclear or if it’s a complex claim.

In most states, employees can appeal a claim that gets denied through their state’s workers’ compensation board or agency.

If you cannot file a claim through your insurer, you can also file one through your state’s workers’ comp agency or bureau. What’s important is that you do so in a timely way. Most states have rules about how quickly you must file paperwork after an accident occurs or an illness is discovered.

Important point: When an employee is injured on the job, you must do everything possible to get them any medical care they need right away.