If your small business has any employees at all, you need workers compensation insurance in Pennsylvania. Even if you have only part-time workers, even if they’re your own family members, you still need workers compensation insurance—there’s no getting around it. We cover more details around workers compensation insurance requirements, how much it costs, and recommend the 5 best workers compensation insurance company in Pennsylvania.

- 5 best workers compensation insurance companies in Pennsylvania

- Workers compensation laws in Pennsylvania

- What does workers compensation insurance cover?

- What doesn’t workers compensation insurance cover?

- Who is exempt from workers comp insurance in Pennsylvania?

- How much does workers compensation insurance cost in Pennsylvania?

- How to find cheap workers compensation insurance in Pennsylvania?

- How is workers compensation Insurance different that general liability insurance?

5 best workers compensation insurance companies in Pennsylvania

We research ~20 companies offering workers compensation insurance in Pennsylvania and here are our recommendation of the top 5 providers for your consideration.

- Simply Business: Best for finding the cheapest coverage

- CoverWallet: Best for comparing online quotes

- The Hartford: Best for bigger businesses in Pennsylvania

- biBERK: Best for low-cost coverage and a great digital experience from a reputable brandname

- Tivly: Best if you prefer working with an experienced agent

Simply Business: Best for finding the cheapest coverage

Simply Business is an insurance brokerage firm, focused 100% on serving small and medium-sized businesses. Simply Business offers all coverages that small or medium-sized businesses may need. They work with 30+ carriers with one single goal of helping small businesses find the coverage they need at the cheapest rate available. If your main goal is to find the cheapest rate quickly, you may want to work with Simply Business.

Pros:

- Easy to get and compare several quotes to find the cheapest one

- All carriers have good financial strength ratings and tend to offer low-cost coverage. These carriers may not be easily accessible outside of Simply Business platform

- Great customer satisfaction rating on trustpilot

Cons:

- In some cases, quotes may not be available online. You have to call to discuss your cheapest quote options

- If you prefer working with a particular carrier that Simply Business doesn’t work out, you may need to look elsewhere

CoverWallet: Best for comparing online quotes

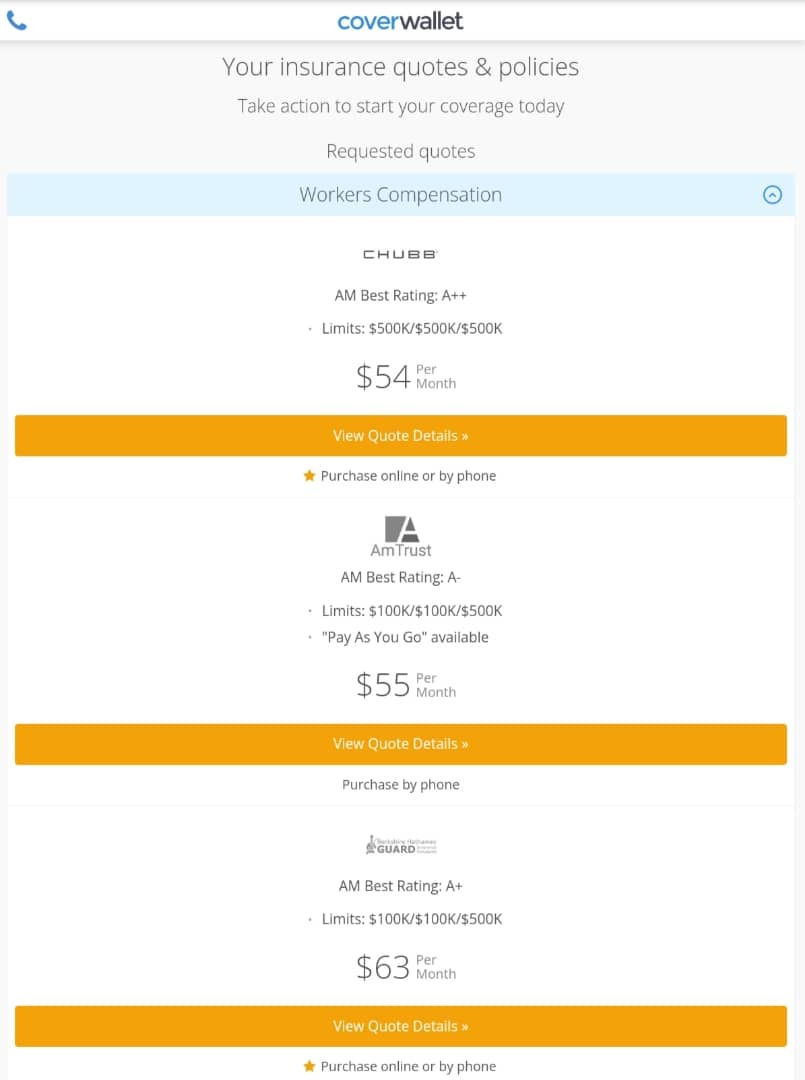

CoverWallet is a good place to start when you’re looking for business insurance. They are a digital broker and work with several leading business insurance companies.

We said we had a small accounting firm with 2 full-time employees and an annual payroll of $170,000. Here are the quotes from CoverWallet:

We received 3 quotes: Chubb, AmTrust, and Guard. All three companies are great with great financial strength rating and customer satisfaction. Chubb quote is a bit cheaper than the other two.

We also got another quotes for a small landscaping contractor with 4 full time employees and an annual payroll of $350,000. As you may know, landscaping is considered one of the high-risk work, thus has more expensive workers comp insurance.

We received three quotes from three different companies: Guard, a subsidiary of Berkshire Hathaway; AmTrust; and Chubb. In this particular case, Guard offers the cheapest quote, and cheaper than AmTrust.

However, this might not be the same for your own case. So make sure to apply for your own quotes and compare to select the cheapest one for you.

Once you’ve got your quote, you can purchase a policy online, or be connected to an agent. They recommend other types of business insurance for you, too. They are licenses in all 50 states, so wherever you live, you can get a quote.

The Hartford: Best for bigger businesses in Pennsylvania

The Hartford is one of the oldest name in the insurance industry. They have been around for more than 100 years and have had a lot of experience in insuring both individuals and businesses.

They offers all types of business insurance, and you can also tack on your personal auto or homeowners insurance for a discount. The quote process isn’t very lengthy, although this is the first time the Hartford gave us a quote for anything—usually, they say we’ll have to call.

The Hartford likes to post stellar reviews on its own website, but if you look on more neutral websites such as Trustpilot, they are far less glowing. For example, on Trustpilot, the Hartford earns 1.8 stars out of five. It should be noted that this does cover all of their insurance options, both personal and business. Some of them caution that if you give them your phone number or email address, you will be inundated with offers for insurance.

biBERK: Best for low-cost coverage and a great digital experience from a reputable brandname

biBERK is backed by Berkshire Hathaway, which is Warren Buffet’s company. They claim to use an automated analytical system to generate quotes. Most internet companies do this these days, and most can spit out a quote in under five minutes. However, we’ve never not gotten a quote from biBERK, they’ve never told us to come back later or they would email us the results. It’s very easy and straightforward. Rates are usually pretty good.

Tivly: Best if you prefer working with an experienced agent

Tivly is another brokerage firm specializing in serving small businesses. They partner with 50+ carriers and offer all coverages small businesses may need, including workers comp insurance. One unique aspect of Tivly is they believe that small business insurance is quite complex and small business owners should work closely with an experienced agent to make sure they understand the right coverages that they need. That’s the reason why Tivly’s main focus is to match small business owners with an agent who has significant experience in the same industry and niche.

Pros:

- A large network of agents who are very knowledgeable and experienced in all industries and niches

- A large network of carriers ensures that small businesses have access to the right coverages at affordable prices

- Simple and fast experience to match small business owners and agents

Cons:

- Limited digital capabilities, ie. no online quotes

- If you prefer doing everything online, you may need to look elsewhere

>>MORE: 10 Best Workers Compensation Insurance Companies for Small Businesses

Workers compensation laws in Pennsylvania

If you own a small business in Pennsylvania, workers compensation insurance is required, with only a few exceptions. You can apply with the State Workers’ Insurance Fund (SWIF) to obtain insurance. Or you could apply for self-insurance status, which is available to large, financially independent companies that promise to cover workers’ compensation claims themselves.

Other people who are exempt from workers compensation insurance in Pennsylvania include:

- Longshoreman

- Railroad workers

- Domestic workers

- Federal employees

If you don’t have workers compensation insurance, you may face civil and criminal penalties, including a $2,500 fine and up to a year in jail if you accidentally failed to provide workers’ compensation anda $15,000 fine and up to seven years in prison if the courts decide you failed to provide coverage deliberately.

How to buy workers comp insurance in Pennsylvania?

You can choose one of the following 4 ways to buy workers comp insurance in Pennsylvania:

- from a digital brokers like CoverWallet or Policy Sweet or Commercialinsurance.net;

- from a insuretech company like Pie or Cerity;

- from a traditional insurance companies like the Hartford, AmTrust, Employers, Travelers, etc;

- from the state fund

- or apply for self-insurance

Each way has its own pros and cons and why it makes sense for you to make sure you compare several quotes to select the cheapest one for your company. Learn more about the details at Buy workers comp insurance in Pennsylvania online

What does Pennsylvania workers compensation insurance cover?

Workers compensation insurance protects your employees just in case they are injured on the job. It covers:

- Medical expenses

- Death benefits

- Missed wages

- Lawsuits

- Vocational training

Vocational training covers education if your employee can no longer do the job they were hired to do.

Workers compensation will cover your court costs and any settlements if the injured employee decides to sue you. If the worst happens and an employee dies while on the job, workers compensation n covers the funeral and burial expenses. It also provides a settlement to the victim’s family.

Keep in mind that diseases employees were exposed to while at work can also be covered under workers compensation. Carpal tunnel syndrome for office workers and black lung disease for coal miners are two well-known occupational hazards that can be covered by workers compensation insurance.

What doesn’t workers compensation insurance cover?

Workers’ compensation doesn’t cover everything. It won’t cover:

- Independent contractor injuries

- Client injuries

- Employees who are intoxicated or high

- Wages for temporary workers while the worker recovers

- OSHA fines

- Injuries that occur after the employee has left work (assuming they’re not doing something under the scope of employment)

- Vandalism or intentional injuries

Who is exempt from workers comp insurance in Pennsylvania?

Pennsylvania employers with one or more people working for them must provide coverage. There are some exemptions for:

- Casual workers

- Certain agricultural laborers

- Domestic workers who are not covered under the Workers’ Compensation Act

- Executive officers who have been granted an exemption by the Pennsylvania Department of Labor and Industry

- Federal government employees

- Licensed real estate people or associate real estate brokers

- Longshoremen

- People who have been granted exemption due to religious beliefs by the Pennsylvania Department of Labor and Industry

- Railroad workers

- Sole proprietors, partners, and corporate officers.

How much does workers compensation insurance cost in Pennsylvania?

The cost of workers compensation insurance varies according to:

- Amount of payroll

- Claims history

- Number of employees

- Coverage limits

- Location

- Level of risk

If you want to calculate your workers compensation costs, in Pennsylvania it’s $1.35 per $100 of payroll, on average. You then multiply this by class code, which is how the insurance industry categorizes workers, and then that’s multiplied by an experience modification rate, which is how your business compares to other businesses. Costs of workers compensation insurance tend to go down over time because of experience, unless you have a claim.

If you want to reduce the cost of workers compensation insurance for your business, make sure you shop around with at least 3 companies or with a digital broker like CoverWallet to compare several quotes and select the cheapest one for you.

How to find cheap workers compensation insurance in Pennsylvania?

Finding cheap workers’ compensation insurance in Pennsylvania really depends on your claims history and your payroll. It’s always possible to find different rates, especially if you choose an insurer that focuses solely on covering workers’ compensation, like Pie Insurance. You can also find affordable insurance through internet based insurers compared to the more traditional brick and mortar institutions.

As you see above, the cost of workers compensation insurance for the same company in Pennsylvania varies significantly across providers. So make sure you shop around with a few companies or a digital broker like CoverWallet to compare several quotes to select the cheapest one for your company.

It can also pay to ask about any discounts on the insurance policy with an agent. Some insurance companies will provide discounts for having safety policies and return-to-work policies in place. You may also get a discount if you choose to bundle multiple insurance policies with the same insurer.

Lastly, the cost of worker compensation insurance depends on the classification codes of your employees. Construction workers have much more expensive workers compensation insurance than clerical workers, so make sure you classify your employees into the correct codes and remember to update the codes when your employees change the nature of their work.

If you hire 1099 employees in Pennsylvania, do you need to provide workers comp insurance?

No, as an employer in Pennsylvania, you are not required to provide workers’ compensation insurance coverage for independent contractors classified as 1099 employees. However, misclassifying employees as independent contractors can expose you to potential legal and financial risks. If the worker is later deemed to be an employee and not an independent contractor, you may be held responsible for paying employment taxes, unemployment insurance, and potentially even workers’ compensation benefits. Additionally, you may be subject to fines and legal penalties for misclassifying employees. To minimize these risks, it’s important to accurately classify workers as employees or independent contractors in accordance with the relevant state and federal laws.

While it’s not required by law, requiring 1099 employees to have their own workers’ compensation insurance coverage can be a good risk management strategy for an employer. This way, if the worker is injured on the job, the worker’s own insurance policy can cover the medical expenses and lost wages. This can help protect the employer from potential legal and financial liability in case of a work-related injury. However, it’s important to note that the requirement for 1099 employees to have their own workers’ compensation insurance varies by state and it’s always a good idea to check the relevant state laws and regulations.

Workers compensation insurance in Philadelphia, PA

Philadelphia is the biggest city in Pennsylvania. With a population of about 1.6 million, 97% workers in Philadelphia works for ~30,000 small businesses in the city. Similar to the rest of Pennsylvania, workers comp insurance is required for small businesses in Philadelphia. The small businesses in Philadelphia can get workers comp insurance from the 5 best providers we recommend above.

According to zipRecruiter, Philadelphia has the second highest average annual salary in the state of Pennsylvania, which is $61,584, only after Scranton at $62,933. If we keep all other variables the same, this means that workers comp insurance for a small business in Philadelphia is more expensive than that for a similar company is other part of Pennsylvania. This is because annual payroll is an important factor of workers comp insurance cost. If you are looking to buy workers comp insurance in Philadelphia, be sure to compare several quotes before making your final decision.

Workers compensation insurance in Harrisburg, PA

With a population of 575K, Harrisburg is a growing town in Pennsylvania. The median salary of employees in Harrisburg is $62K, according to Payscale. And major industries in Harrisburg are Healthcare, Technology, and Education, according to Forbes. These employers are required to have workers comp insurance for their employees.

Workers comp insurance cost is reasonable in Harrisburg thanks to its affordable cost of living and relatively safe industries. If you are looking for affordable workers comp insurance in Harrisburg, consider the 5 companies we recommend above.

How is workers compensation Insurance different that general liability insurance?

Workers compensation insurance only covers people who work for you. If your client or a customer or even a random passerby is injured on your jobsite, general liability insurance will cover that. General liability covers bodily injury and third-party property damage against you, the business owner.

Last thoughts

Although no one wants to pay a lot of money for workers compensation insurance, the cost of not having it is exponentially more. Make sure you run a safe workplace, and hopefully you won’t have any claims filed against you.