Workers’ compensation insurance (often referred to as workers’ comp) has been in existence in New York state since 1914. Despite being around for more than a century, most small business owners still don’t fully understand it.

In this article, I’ll explain everything small business owners in the Empire State must know about workers’ compensation insurance so you can get the coverage you need to protect your employees and comply with state laws.

- What is workers’ compensation insurance?

- Who needs workers’ compensation insurance in New York state?

- Who doesn’t need workers’ comp insurance in New York?

- Is workers’ comp necessary in New York for part time employees?

- Do you need workers’ compensation in New York if you are self-employed?

- What do employers need to do when an employee makes a workers’ comp claim?

- What are New York’s workers’ comp benefits?

- Why do business owners need to comply with New York’s workers’ comp laws?

- What else do employers need to know about workers’ comp laws?

- How can business owners get workers comp insurance in New York?

- How much does workers’ compensation insurance cost in New York?

What is workers’ compensation insurance?

Workers’ comp insurance protects employers and their employees against financial losses associated with work related injuries or illnesses. When it comes to workers’ compensation coverage, New York State considers day laborers, leased and borrowed staff, volunteers, part-time workers, and family members, as well as most subcontractors, to be employees.

Who needs workers’ compensation insurance in New York state?

The following business types must carry workers’ comp insurance:

- All for profit businesses that have employees, or any types of workers that the state workers’ compensation board considers to be employees.

- People who hire domestic workers, nannies, and home health care aids who work 40 hours per week in their home.

- Most nonprofit organizations.

When it comes to independent contractors, any working under your direct control are likely to be considered by New York state to be your employees for workers’ comp purposes, regardless of their tax status. You may need to secure workers’ comp coverage for them even if they’re receiving 1099s.

How can business owners get workers comp insurance in New York?

There are three ways you can get coverage:

Private insurance: Hundreds of private insurance companies are authorized to write workers’ compensation insurance policies in New York State. These include traditional insurers like the Hartford, Chubb, Employers, AmTrust Financial, etc. and insuretech ones such as Pie, Cerity, etc.

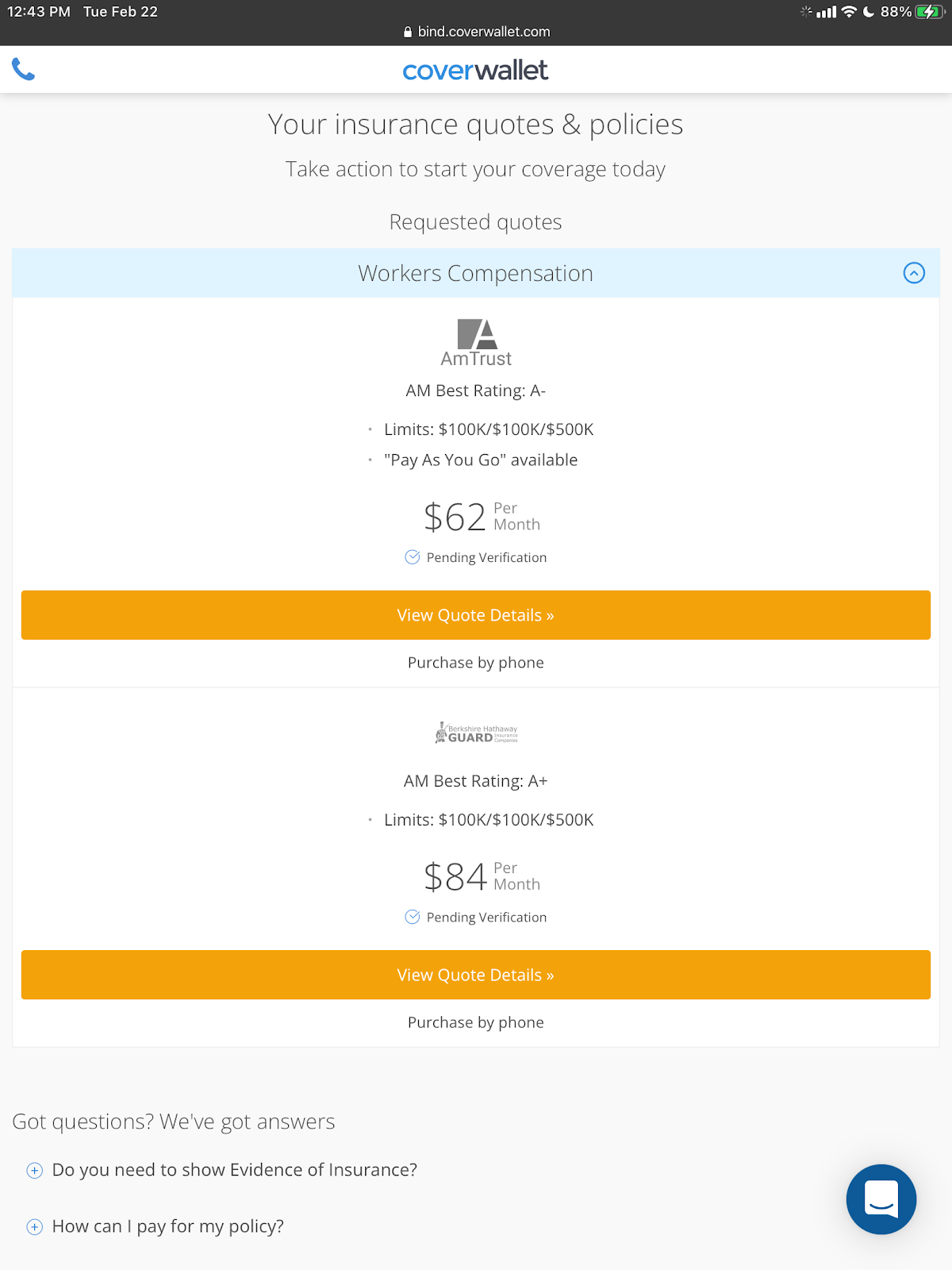

Brokers or agencies: If small business owners want to compare several quotes online to select the cheapest one for their company, buying workers comp insurance from a broker or agency, especially a digital one is the best way. A couple of popular digital brokers include Policy Sweet, CoverWallet, commercialinsurance.net, or Simply Business. Below is a quote sample from CoverWallet for small accounting firm having 4 full-time employees, annual payroll of $300,000, and annual revenue of $600,000.

Public insurer: The New York State Insurance Fund is a self supporting insurance carrier that writes workers’ compensation insurance policies for state businesses. It can be a good solution for companies that are finding it difficult to get coverage, although premiums may be higher than for regular insurers.

Individual self insurance: Larger employers can set aside reserves for insuring their own businesses in a highly regulated process. If your business grows larger in the future, this could be an option for you.

Learn more at the best workers comp insurance companies in New York.

Who doesn’t need workers’ comp insurance in New York?

According to New York law, there are a few instances when a small business would not be required to get coverage, including:

- If the business is owned by a single person and he or she has no leased, borrowed, part-time, or regular employees; unpaid volunteers; or subcontractors.

- If the business is a partnership or corporation and has no employees of any type.

- If the business is owned by one or two people, and those people own all the stock, fill all the officer positions, and there are no other employees.

Exempt business owners in New York are able to get workers’ comp insurance for themselves if they believe they’d benefit from it.

Is workers’ comp necessary in New York for part time employees?

Most people who are paid to do any type of job are considered employees by New York law and would need to be covered by workers’ comp. State law considers day laborers, leased or borrowed employees, part-time employees, unpaid volunteers (including family members), and most subcontractors as employees.

An exception to this are independent contractors, who must meet the following criteria to not be considered employees:

- They’re not under the employer’s control or direction while doing their job.

- The contractor is delivering their usual for hire services.

- They work in an independently established trade, occupation, or business that is related to the service being performed.

In short, most part time employees will need to be covered by workers’ comp in New York.

Do you need workers’ compensation in New York if you are self employed?

If you are self employed or a sole proprietor, you’re not required to buy workers’ comp. However, it might be smart to get this coverage. If you get injured while working and don’t have workers’ comp, you could end up paying for expensive medical bills on your own because your personal health insurance probably won’t cover work injuries. Workers’ comp will also pay part of the wages you lose while unable to work, which could help save your business.

Learn more at the best workers comp insurance for the self-employed.

What do employers need to do when an employee makes a workers’ comp claim?

When an employee reports a work related injury or illness to you:

- Help them find medical care.

- Immediately notify your workers’ compensation insurance carrier. Employers can also notify the New York State Workers’ Compensation Board by filing the Employer’s First Report of Work-Related Injury/Illness (Form C-2F). However, this isn’t required if your insurer has filed an electronic First Report of Injury (FROI) for you. If you fail to report a work related injury to your insurance carrier or the state workers’ comp board, it could result in a penalty of up to $2,500.

- Explain to your insurance carrier whether the employee injury or illness:

- Has caused or will require time off from work

- Will need medical treatment beyond ordinary first aid

- Will require more than two first aid treatments.

Once you’ve done these things, your insurer or state workers’ comp board representative will advise you on what to do next.

What are New York’s workers’ comp benefits?

Workers’ compensation in New York covers the cost of medical bills for employees who suffer a work related injury or disease. It also provides disability benefits when employees aren’t able to work, which are usually two-thirds of their average weekly wage.

Other New York workers’ comp benefits include:

- Job retraining if someone is unable to handle their usual work duties.

- Funeral costs if an employee dies because of a work accident.

- Survivor benefits to immediate family members if an employee dies on the job.

Why do business owners need to comply with New York’s workers’ comp laws?

Businesses could be required to pay a penalty of up to $2,000 for every ten days they don’t have adequate insurance coverage. They could also be forced to pay penalties for misrepresenting their payroll or the work handled by their employees, or failing to keep complete records.

Not carrying workers’ compensation insurance if you have more than five employees is a felony in New York. Not having coverage for five or fewer employees is considered a misdemeanor. In addition, people and businesses that are penalized for workers’ comp infractions are not allowed to apply for public work contracts for one year.

New York state holds business owners who do not have workers’ compensation coverage personally liable for lost wages and the cost of medical care if an employee is injured or becomes ill due to work related reasons.

New York is known for aggressively pursuing workers’ comp offenders with stop work orders.

What else do employers need to know about workers’ comp laws?

Here are a few little known facts about New York’s workers’ compensation regulations:

- Insurers notify the state’s workers’ comp board when they write, modify, or cancel insurance coverage. If coverage is canceled without a replacement policy, the board will contact the business owner about getting new coverage.

- The workers’ comp insurance status of all employers in the state is public information that’s available on the workers’ comp board website.

- It’s unlawful for an employer to discriminate against any worker who files a workers’ comp claim or testifies in a workers’ compensation case.

- Immigration status is not a factor in receiving benefits.

- State law requires employers to conspicuously post a notice about their workers’ compensation insurance coverage. The notice must include the name, address, and phone number of the insurer along with the employer’s policy number.

Knowing the nuances of New York’s workers’ comp laws can help you comply with them so you stay out of trouble.

How much does workers’ compensation insurance cost in New York?

Workers comp insurance costs vary and are based on a number of factors, including:

- Payroll

- Location

- Number of employees

- Employee job responsibilities

- Industry and related risk factors

- Coverage limits

- Claims history.

The average cost of workers comp insurance in New York is $1.41 per $100 in payroll. You can figure out roughly how much you’ll pay by using this formula:

(Payroll/$100) x class code rate x experience modification rate = premium.

The cost you will be calculating is just rough since different insurance companies will add fees and other charges in their quotes.

Learn more how to calculate the workers comp insurance cost in New York.

An insurer that offers workers’ comp insurance in New York can provide you with a premium quote. It’s a good idea to get quotes from multiple providers so you can compare costs to find the best deal for your business.

How to find cheap workers comp insurance in New York?

Workers compensation insurance is the most expensive in New York. It can be a significant cost to your business. Not having workers compensation insurance is not an option since it can result in even more costly consequences. Below are a few tips to help you get the cheapest workers comp insurance in New York.

- Shop around to compare several quotes: Make sure you shop around with a few insurance companies or a digital broker to compare several quotes to get the cheapest one for your business

- State programs: Check if there is any state savings program in New York that your business can be qualified for.

- Group insurance: if your company is a member of a larger association, you may be able to get a group rate on your company’s workers compensation insurance.

- Identify potential hazards and fix them. Once you fix them, make sure you notify your insurance agent (if you have one) or report it to your company. Continue improving the safety standard in your company’s workplace and ask for annual reviews when you need to renew your company’s workers comp insurance.

- Invest in safety education. According to Safety and Health, for every dollar you spend on injury prevention, you’ll earn a ROI of between $2 and $6 dollars. If you’re wondering how to start a safety program, OSHA (Occupational Safety and Health Administration) is a good place to start. After starting the program, you need to make sure to obtain the qualification certificate from the program administrator. Showing the certificate to your workers compensation insurance insurer or agent can help reduce the cost when you renew the policy.

- Check classification levels. Every employee type is assigned a classification level, and each level is assigned a rate that reflects the level of risk this type of job has. Obviously, a secretary is exposed to much less risk than a construction worker, even if they work at the same company. Make sure everyone is classified accurately and regularly update this as you are hiring new employees.

Learn more at the cheapest workers comp insurance companies.