Houston, Texas, is the United States’ fourth largest city. As a result of its size, it’s not surprising that it has a diverse talent pool that contributes to its very favorable business climate.

From 2018 to 2020, Space City has seen over 760 business expansions and relocations. Your business will likely see huge growth and success in Texas, but you’ll need Texas business insurance to protect your business.

In this piece, we’ll describe some of the best companies where you can get business insurance in Houston. We also have a list of other information you may need regarding the policy.

- 6 best business insurance companies in Houston, Texas

- What does business insurance cover in Houston, TX?

- How much is the average business insurance cost per month in Houston, Texas?

- How to find cheap business insurance in Houston, Texas

- Who needs business insurance in Houston, TX?

- Insurance requirements for businesses in Houston, Texas

6 best business insurance companies in Houston, Texas

- CoverWallet: Best for comparing quotes

- Simply Business: Best for low-cost coverage

- InsurePro: Best for on-demand and pay-per-day coverage

- Thimble: Best for general liability insurance for small businesses

- biBERK: Best for workers comp insurance

- Progressive: best for commercial auto

CoverWallet: Best for comparing quotes

CoverWallet is not a provider of insurance, but then they are a genuine insurance broker. The company takes pride in offering businesses across the United States competitive digital insurance quote comparison and online policy management solutions. The company was purchased by Aon in 2020.

CoverWallet’s best feature is its online quote comparison platform, which makes finding low-cost small-business insurance online a breeze. Those who use CoverWallet benefit from a simple online insurance application process and the assistance of online insurance agents.

Customers can also use MyCoverWallet to pay, download proof of insurance, access policy documents, quickly purchase optional coverages, and locate a carrier’s contact information to file a claim.

Pros

- They have a live chat system so customers can easily find help from insurance agents.

- Very high customer satisfaction reviews and ratings

- Affiliated with the top insurance carriers in the United States

- Fast and easy to use

Cons

- They only offer insurance provided by their partners

Simply Business: Best for low-cost coverage

If you plan to get affordable insurance without compromising coverage, you should look to simply business. Although the company does not offer insurance policies, they are one of the best online brokerages helping businesses find affordable coverage.

Using technology, data, and insurance knowledge, the company helps simplify the insurance-buying process for small businesses. Their job is to help you find the most suitable policy at the best price.

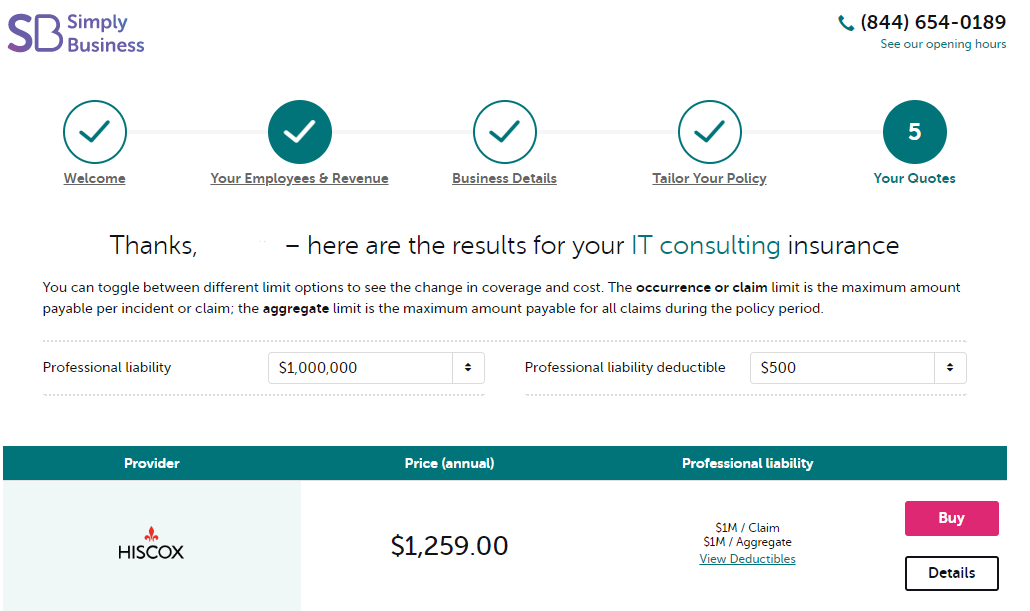

The following is a sample quote obtained for professional liability insurance from Simply Business for a small IT firm in Houston.

Pros

- Choose from a variety of policies to tailor your coverage.

- Coverage for most professions is available.

- They have a library with helpful business insurance resources

Cons

- Inconsistent and confusing customer service hours.

InsurePro: Best for on-demand and pay-per-day coverage

Insurepro is a relatively new company changing how insurance should work. Most small businesses find insurance a little bit too expensive, but at the same time, it is necessary. But then, why buy a policy when you are not in business.

Most businesses have to pay monthly or yearly for their insurance. However, some companies do not need their coverages every day. With insurepro, companies can buy policies for only the time they need. That is, they can buy daily policies for their business.

Insurepro helps companies compare policies from over 20 insurers. They also help them find the cheapest policies in minutes.

Pros

- Fast quotes in minutes

- Best rates compared across over 20 companies

- On-demand insurance

- Mobile app available for easy service

Cons

- Relatively new company

biBERK: Best for workers comp insurance

Worker’s compensation insurance can sometimes be costly for small business owners. However, small business owners need insurance to protect their staff from accidents and cover themselves from lawsuits. It gives them peace of mind knowing their business is well-protected.

biBERK does well to provide affordable workers’ comp insurance that prioritizes user convenience. It’s one of the top small business insurers in the US in terms of workers’ comp and other business policies. Business owners can manage and pay for policies online using their website.

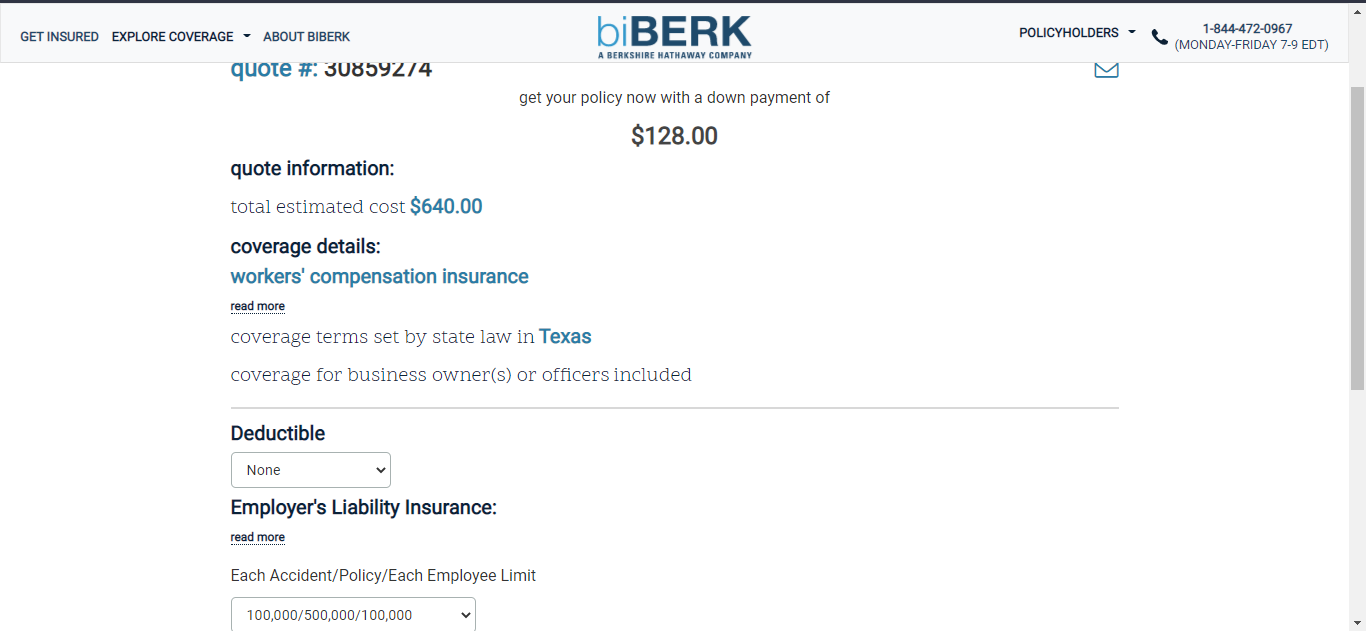

Here is a sample quote obtained for workers’ comp from biBerk for a small IT firm in Houston.

Pros

- biBerk is a direct insurer

- May offer 20% lower prices than other insurance companies

- Offers fast online quotes so business owners can buy coverages in minutes

- Allows online policy management and phone cancellation

- Great customer service team

Cons

- Only offers commercial insurance

- They do not offer disability benefits insurance

Thimble: Best for general liability insurance for small businesses

Small business owners usually want cheap, straightforward commercial insurance without fancy product names and terms. Thimble seems to understand that no one wants to spend hours trying to buy insurance.

Thimble guarantees insurance in under an hour, and its policies cover most small-business risks. Thimble should be considered for cheap general liability for small businesses. The company has 50 employees, 23 investors, and a $22 million valuation and offers the best general liability policy for small companies.

Thimble also has other insurance products for computer shops, technicians, software developers, and programmers.

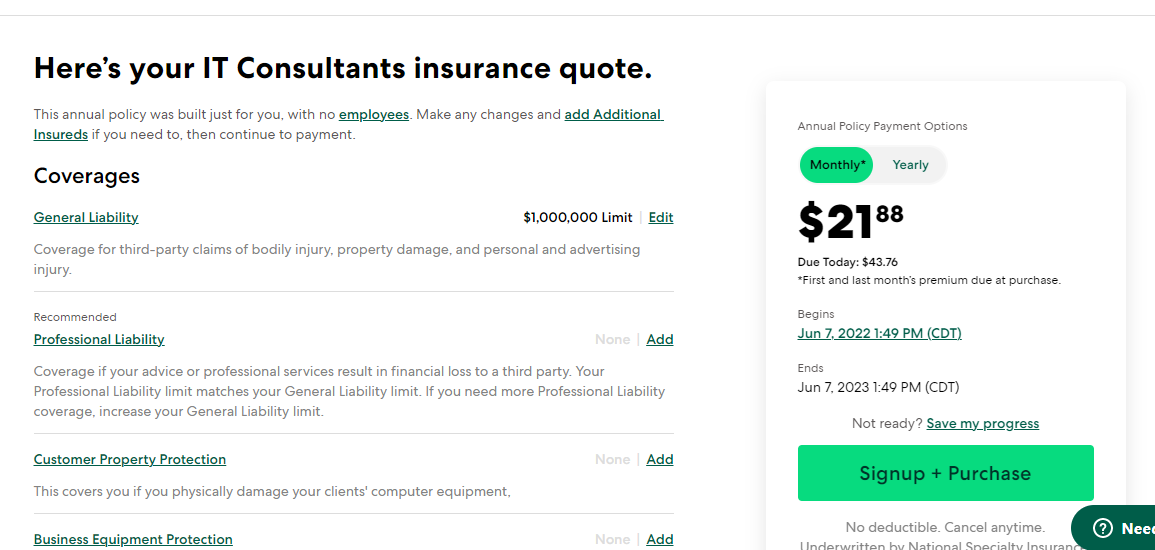

The following image is a sample quote obtained for general liability insurance from Thimble for a small IT firm in Houston.

Pros

- Offers small business coverages

- Quick insurance app

- Thimble offers cheap short-term general liability insurance for hours, days, or weeks.

- Thimble offers small business general liability insurance from $5, making it an affordable online option.

- Good online experience

Cons

- Thimble may not cover specialty businesses’ risks.

- Other non-IT sectors may cost more with Thimble.

Progressive: Best for commercial auto and commercial truck insurance

Progressive’s business auto insurance is popular. In fact, it has been named among the best in the United States many times. The company offers great rates, no fee spikes, and an easy filing process for commercial auto insurance.

Besides, Progressive is financially stable, with $42.7 billion in revenue and 45,000 employees in 2020.

Progressive’s business owner’s policy is also remarkable because it covers equipment breakdown, damaged stocks, and property damage. Progressive’s specialty risks have cheap, stable rates.

If your business avoids road accidents and maintains vehicles regularly, you will enjoy generous discounts with Progressive’s commercial auto insurance.

Pros

- Customers with good driving records get cheap commercial auto insurance rates.

- Helps customers get custom coverages with discounts

- Custom limits to meet business owner’s anticipated costs

Cons

- Customers say Progressive suddenly raises rates.

What is business insurance?

Business insurance refers to a group of policies designed by insurers to assist companies in creating a protective cushion for financial support in the event of a variety of challenges that could arise at any time.

What does business insurance cover in Houston, TX?

Insurance companies provide various commercial insurance options to help protect Houston companies. The more coverage you obtain, the better protected your company will be. You can choose from a varisous options, including:

Professional liability insurance

Liability insurance for professionals in Texas will assist you in defending lawsuits alleging that you made a mistakes in the professional services you provided.

Learn more at professional liability insurance cost and the best professional liability insurance companies in Texas

General liability insurance

General liability insurance helps a company defend itself against claims of bodily injury, advertising injury, or property damage.

Learn more at general liability insurance cost and the best general liability insurance companies

Commercial property insurance.

Protect your owned or rented building and business property with commercial property insurance. Learn more at commercial property insurance cost and the best commercial property insurance companies in Texas

Commercial auto insurance

Commercial auto insurance can help protect you and your employees on the road if you drive for business.

Learn more at commercial auto insurance cost and the best commercial auto insurance companies in Houston, TX

Workers’ compensation insurance

Workers’ compensation insurance provides income benefits to your employees in the event of a work-related injury or illness. Workers’ compensation insurance is not a must-have policy in Texas, and employers are not required to carry it.

Learn more at workers compensation insurance cost and the best workers comp insurance companies in Houston, Texas

What is the cost of business insurance in Houston, Texas?

Houston’s small business owners currently pay a median annual premium of $49 per month for a general liability insurance policy. When you look at each industry in detail, you’ll notice that insurance costs vary significantly.

Construction businesses may pay closer to $170 per month. The higher rate is because of, the higher risks involved in the business. In contrast, fitness professionals typically pay about $15 per month. Different factors influence each company’s costs, mostly unique to how they run their business and the insurer they use.

That is to say that no two businesses will have the same quote even if you check with the same insurer.

How much is the average business insurance cost per month in Houston, Texas?

Above is the average cost of a general liability insurance policy for small businesses in Houston, TX. If you add more coverage, you’ll pay more for your business insurance coverage. Below are the average costs of different coverage for small businesses:

| Business insurance coverage | Average costs in Houston, TX |

| General liability insurance | $49 per month |

| Professional liability insurance | $56 per month |

| Workers comp insurance | $117 per month |

| Commercial auto insurance | $106 per month |

| Cyber liability insurance | $94 per month |

| Commercial property insurance | $82 per month |

These are just the averages. As you know, the insurance rates vary significantly by industry and other factors. Your rates will be different. Be sure to shop around with a few companies or work with a top broker like Simply Business or CoverWallet to compare several quotes to choose the cheapest one for your business.

What are the factors that affect your business insurance cost in Houston, Texas?

The following are the main factors that affect business insurance costs in Houston, Texas:

What you do or what you sell

The cost of insurance is determined by the type of business you operate. The higher the risk, the higher the price. Because they work with (and potentially damage) other people’s property, janitors, construction workers, and manufacturers, for example, have some of the highest rates for general liability insurance. It’s also important to consider your liability risk. For example, a company that provides security services faces a higher risk of being held liable for third-party injury than a company that provides accounting services.

Where do you do business in Houston?

Property damage is more likely in high-hazard flood or wildfire zones than in areas where weather-related incidents are less likely, and insurance premiums frequently reflect this difference in risk. You can reduce the risk of property damage from natural disasters. Still, if your company is located in one of these high-hazard areas, you should expect property insurance to be more expensive than in other areas.

Business property description

Do you operate your business from a rented location, or do you own the property? Depending on your business, each scenario comes with its own set of risks. Suppose you rent space for a restaurant, for example. In that case, you’ll likely pay a higher property insurance premium than if you rent space for a real estate business because the risk exposures from restaurant equipment are higher than risk exposures in a general office environment. However, suppose you own the space where your restaurant is located. Your property insurance premiums will almost certainly be higher than if you rent because your coverage will typically cover damage to the building itself, not just the contents inside.

Your previous insurance claims history

If you have a claim history, insurance companies will also look at it. For example, if you’ve been sued several times for mistakes you made while providing services, an insurer may view this as a trend that will continue and charge a higher premium to compensate for the increased risk. Alternatively, suppose one of your delivery drivers has a history of accidents. In that case, your auto insurance premiums may be higher than if all drivers on the policy have a clean driving record.

Number of employees

The more employees you have, the likely you will have high premiums. Your employee affects your workers’ comp insurance because it is valued per employee.

Types of insurance purchased.

The more insurance policies you carry, the more protection your company has. However, more coverage means you have to pay more money. Also, having policies with high coverage limits will amount to higher premiums.

How to find cheap business insurance in Houston, Texas

The following are some ideas that may help you cut costs on business insurance:

Get only the necessary business insurance coverages

Your small business may not need all business insurance coverages. You may save some money by carefully evaluating your risk and buying only the needed policies.

Bundling business coverages saves money

Your business may need multiple coverages for full protection. Bundling business insurance coverages instead of buying them individually may help you save money. Some small businesses get Business Owners Policy (BOP) that combines general liability and commercial property insurance. Some BOP policies may also include business income interruption coverage.

BOP policies can also include cyber security and employment practices liability as endorsements. These additional endorsements may cost more, but they’re cheaper than buying separate policies.

Check multiple online quotes.

You can compare quotes from multiple insurance companies to avoid overpaying for business insurance. Different companies may assess your business’s risk differently based on their strengths and industry focus. You can work with digital brokers to save time since they offer multiple quotes at once.

Who needs business insurance in Houston, TX?

Most small businesses in Houston, Texas (TX) need business insurance. Most insurers provide insurance to businesses in a variety of industries, including:

- Shops that sell cosmetics

- Consulting firms

- Photographers/ videographers

- Retail companies

- Technology consultants and IT firms

- Business and finance institutions

- Construction workers, etc.

Insurance requirements for businesses in Houston, Texas

In Texas, business insurance isn’t required by law. In fact, Texas is the only state where private employers are not required to carry workers’ compensation insurance.

However, there is one exception: companies that have a contract with the government must provide workers’ compensation for each of their employees until the project is completed.

Choosing not to have workers’ compensation or any other type of business liability insurance is risky because it removes some of your legal protection and exposes you to costly lawsuits.

Also, businesses in Houston that use vehicles must have commercial auto insurance. Usually, the minimum liability required varies by the weight of the car. The following are the minimum requirements for auto liability insurance in Houston, Texas:

- Liability for bodily injury of $30,000 per person

- Liability for bodily injury of $60,000 per accident

- Property damage liability is $25,000 per accident.