Commercial property insurance is one of the basic insurance needs of companies. The policy protects company assets from fire, break-in, vandalism, wind, and other natural or man-made calamities.

In Texas, fire is the most dangerous of all these disasters, with companies sometimes recording as high as $35,000 in losses in single fire incidents. For some companies, that can mean the end of the business.

Therefore, commercial property insurance is a good idea for any business. So long you have tangible assets, you’ll need this policy to protect them, whether you are a big or small business. This article explains the details of commercial property insurance and how you can get the best of it in Texas.

- 6 best commercial property insurance companies in Texas

- What does commercial property insurance cover?

- How much does commercial property insurance cost in Texas?

- Factors that affect commercial property insurance costs

- How to find cheap commercial property insurance in Texas

- Who needs commercial property insurance in Texas?

6 best commercial property insurance companies in Texas

- CoverWallet: Best for comparing quotes

- Thimble: Best for flexible coverages

- Hiscox: Best for small companies

- Nationwide: Best for customer satisfaction

- Chubb: Best for large enterprises

- Hartford: Best for merchants

CoverWallet: Best for comparing quotes

If your goal is to compare several quotes to choose the cheapest one, you may want to start with CoverWallet. CoverWallet is a leading insurance broker specializing in serving small businesses. They partner with several leading insurance companies such as Chubb, Hiscox, Liberty Mutual, CNA, etc. Once you submit a quote application online, they will be able to pull quotes from these providers for you to compare and select the cheapest one.

CoverWallet stands out among online business insurance brokers. The company does well to provide professional guidance for anyone seeking insurance. CoverWallet has an easy-to-use assessment tool that will assist you in determining the type and cost of coverage you require for your commercial property. Its carrier agreements have a diverse appetite, ensuring that they can serve small businesses in a wide range of industries and provide all coverages small businesses might need.

As you see below, when we submit a quote request for a commercial property policy, they recommend us having a Business Owners Policy instead, which is probably the most popular policy for small businesses, combining general liability and commercial property coverages in one single policy. If you insist having commercial property insurance policy only, they can still provide quotes on the phone.

Thimble: Best for flexible coverages

Small businesses have a problem with insurance policies because the terms can be too rigid. These strict rules make the policies too expensive for some small businesses to afford. However, Thimble, a relatively new company, makes things easy. Thimble is an insure-tech company with the aim of making it easy for small businesses to enjoy the benefits of insurance.

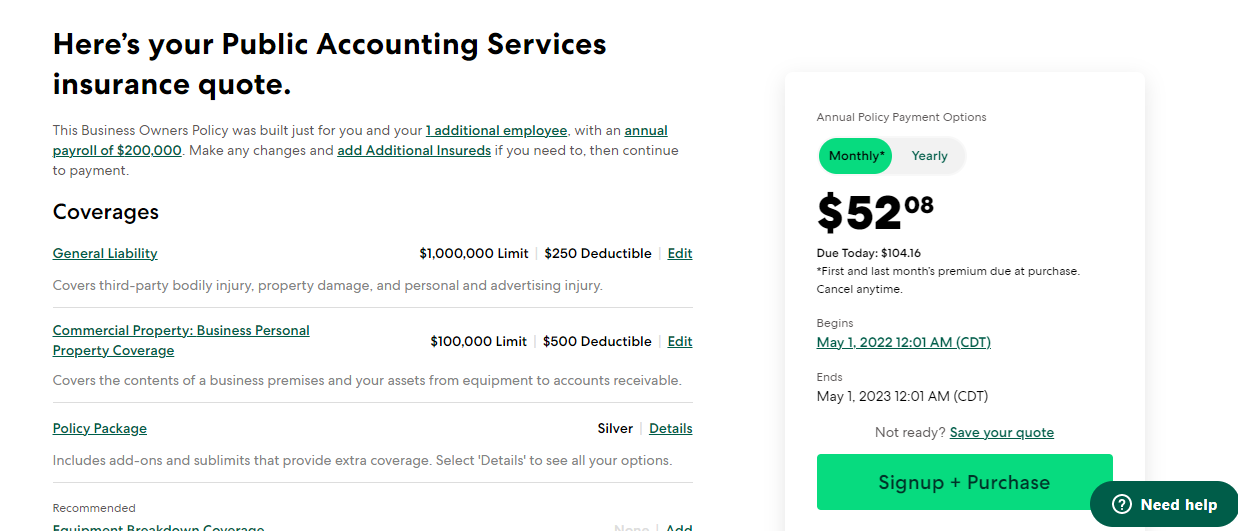

Getting a quote online from Thimble is fast and easy. The whole process shouldn’t take more than 10 minutes. Below is a quote example for an accounting firm based in Houston, Texas.

Hiscox: Best for small companies

Microbusinesses usually struggle with finding the right commercial property insurance. They have a special business structure that requires specialized policies. Unfortunately, large companies tend to overlook them.

Hiscox is a small business insurance firm that comes to the rescue. Hiscox offers specialized policies designed to meet the needs of micro-businesses, independent contractors, and emerging enterprises that have less than five workers. Hiscox leverages technology and policy bundling to help micro-businesses that major insurers sometimes overlook.

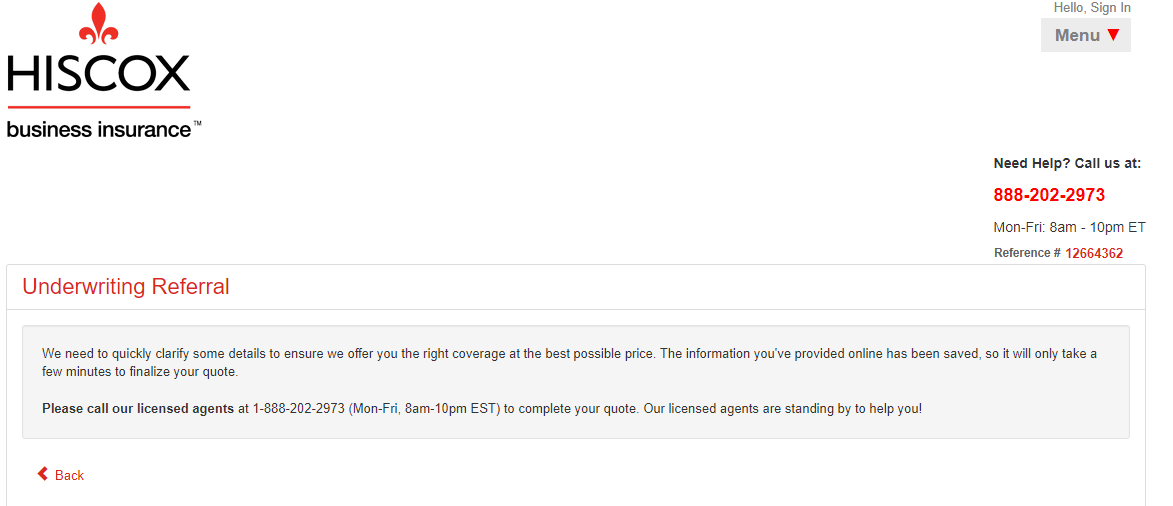

Hiscox can usually provide quotes online pretty fast. However, for the same accounting firm based in Houston, Texas, they are not able to provide quotes online. Instead, you have to call them to discuss your quotes.

Nationwide: Best for customer satisfaction

If you are concerned about customer satisfaction, Nationwide ticks all the boxes. Nationwide is a national leader in property and casualty insurance, providing exceptional contractors’ equipment protection and a broad range of business insurance coverage.

It has continuously obtained excellent ratings from credit-rating firms, providing clients confidence that Nationwide would keep its pledge to make them whole if a loss happens.

Unfortunately Nationwide doesn’t provide quotes online, you have to contact their agents to obtain quotes.

Chubb: Best for large enterprises

If you have a company with large annual sales of at least 30 million dollars, you must be careful with your insurance. You will need a company with good financial standing and tailored policies.

As one of the world’s leading publicly listed property and casualty insurers, Chubb can offer large enterprises a wide range of products. Chubb also offers a robust business owner’s policy (BOP) to enterprises with $30 million in annual sales. So, you can bundle your commercial property insurance for better deals. Interestingly, they also have policies for small enterprises.

The Hartford: Best for merchants

Merchants face lots of risks in their daily business activities. These risks include building, merchandise, and most importantly, its inventory. Such companies need commercial insurance policies that offer protection from a wide range of dangers and risks.

The Hartford helps these companies fill this void with its broad appetite for business risk. The Hartford provides excellent coverage for merchants who want substantial property protection for their inventory, supplies, and equipment. The company covers businesses across different sectors and sizes.

What is commercial property insurance?

Commercial property insurance safeguards commercial properties from fire, theft, and natural catastrophe risks. Any business can carry commercial property, including manufacturers, merchants, service-oriented businesses, and non-profit organizations. Some of these organizations frequently combine the policy with other types of insurance, such as commercial general liability insurance.

What does commercial property insurance cover?

To meet the demands of companies, insurers provide commercial property insurance in different shades. For example, some firms may want to cover only their buildings without covering the contents. Some others may want insurance for their buildings, content, and possibly lost income benefits.

This is another reason why you have to speak with your insurer first to understand the details before you pay for any insurance policy.

However, the key components of commercial property insurance are quite the same across carriers. The following are coverage options for commercial property insurance:

Commercial building insurance

The most significant aspect of commercial property insurance is coverage for the business’s actual property. The covered structure will be named in the policy, including any fixtures or equipment that are permanently included in the building, such as cabinets, electrical systems, or plumbing.

Coverage for other buildings and structures

A policy can include other connected structures that belong to or are utilized by the business property owner, such as a garage, shed or warehouse. However, a policyholder should not believe that all associated buildings are automatically insured simply because a policy covers their primary building structure. Typically, you and your insurer must agree to include such structures covered under the policy.

Coverage for personal property or contents

Damage to a building in which a business works will almost always result in damage to other property used or stored in that structure. As a result, commercial property insurance plans may cover tangible assets such as equipment and furniture stored in a structure covered by the policy. Some plans offer this as basic coverage, but if not, coverage for structural contents may be added as an add-on.

Business income coverage

If the damage caused by a covered occurrence stops a company from continuing its normal activities, certain insurers will reimburse the company for a portion of its lost income. This enables the insured to continue paying operational expenses while repairs are completed.

How much does commercial property insurance cost in Texas?

Based on our study, small businesses Texas pays, on average, $95 per month, or $1,140 a year, for a commercial property insurance policy. Actually, 56% small businesses pay less than $1,500 a year for a good commercial property insurance policy. However, some businesses in Texas can pay up to $5,000 a year for a policy.

How much a small business pays for a its commercial property insurance policy depends on several factors that we discuss in details below. Each business is likely to have different quotes for their policies from different carriers.

These are just the averages. Your quotes and rates will be different. Be sure to shop around with a few carriers or work with a top broker like CoverWallet, ez.insure, or commercialinsurance.net to get and compare several quotes before making your final decision.

Learn more about commercial property insurance cost

Factors that affect commercial property insurance costs

Various variables will determine the actual cost of commercial building insurance. In general, insurers will assess the amount and value of the property to be insured; business factors, and the conditions for coverage as explained below:

Amount and value of insured property

If your company has more properties to cover, the insurer might require that you pay more. Similarly, if your buildings are costly or you have a lot of high-value equipment on your business premises, your premium may cost more.

Business location

Your insurers might want to know where your firm is located since the risk profile for your business will vary depending on where it is. For example, if your business is in a high-crime area, your business would have a higher risk of theft or vandalism. Therefore, your insurer might increase the cost of your premiums to account for the potential risks.

Similarly, if you do business in areas prone to extreme weather in Texas, you might pay more to insure your property. That is because there is a high possibility that your property may be damaged from occurrences such as lightning, hail, or windstorms.

Characteristics of your business

Property in some businesses may be more or less risky to insure than property in others due to the nature of the job.

To arrive at the value of your premium, your insurer may be interested in the type of equipment that you have in your building. For example, a company with modern manufacturing plants may cost more to insure than a small carpenter shop with manual tools.

Another consideration is the industry’s relative risk level. Restaurants are a perfect example of this since they deal with fires more frequently than many other companies. So, companies like restaurants, metalwork companies, and other companies that deal with risks that can destroy their property tend to pay more.

Insurers may also consider the number of workers working at the business or consumers passing through the area. The assumption for most insurers is that a higher number of people interacting with the property increases the likelihood of damage.

Characteristics of the commercial property

When determining your rates, your insurance company will also consider the specific characteristics of the property you seek to insure. Insurers will be especially interested in the age and condition of any insured structures and the building materials used for the building.

Older properties may be more prone to damage, and some older building materials may also have higher risks. Therefore, older buildings tend to have higher insurance rates. In contrast, having features such as security systems or a well-functioning sprinkler system may assure insurers that your property is better secured from threats. That may result in a lower insurance premium.

Method of property valuation

Because the possible payments differ, insurers do not charge the same premium for plans with real cash value coverage as they do for policies with replacement value coverage. Replacement value insurance is often more expensive since they do not account for depreciation. Actual cash value plans often offer cheaper premiums, but they do come with the risk that a policyholder will have to pay more out of pocket in the event of damage or loss.

Type of coverage

Because the sorts of dangers that might trigger coverage range between policy types, the prices associated with basic, wide, and special form policies vary. Basic and wide forms are “named perils” plans, which means they cover just the risks specified in the policy; the broad form contains more of these eligible hazards than the basic form and is thus more costly. An “open perils” policy is a type of coverage that covers all risks except those expressly excluded in the policy. Special form policies are more expensive than basic or wide form plans since this structure increases the likelihood that the insurer will cover claims.

How to find cheap commercial property insurance in Texas

The following ideas might help you save a few dollars on the price of your premiums for commercial property insurance.

Examine your policy premiums thoroughly to see if there are any unexpected fees

Sometimes, a low premium might imply that you may have an insurance policy with a high deductible. This means your insurance company will not begin paying you until you have spent a lot of money out of pocket.

Consider purchasing an insurance package.

Insurance companies usually offer different insurance plans, including flood insurance, tornado insurance, and liability coverage. Consider combining as many of these coverages from the same insurer as this might help you save money while better protecting your commercial property.

Compare different plans and rates.

This is important since you may get a better insurance bundle if you shop around. Different insurance companies have their advantages and disadvantages. You can find out which insurer suits you by checking online brokers or asking professional insurance agents. You can also do some research by checking their websites, online evaluations, and ratings. While at it, ensure you weigh their prices against the level of protection the company promises your commercial property.

Get online quotes whenever you can. It takes you less than 10 minutes to get a quote on Thimble website. Working with a top broker like CoverWallet or ez.insure or commercialinsurance.net is a good idea to get and compare several quotes without having to go to different carriers and their websites.

Who needs commercial property insurance in Texas?

Commercial property insurance is not mandatory in Texas. However, every business with building properties should consider getting commercial property insurance. Not having this policy means you will have to pay for damages to your company equipment and property out of your pocket. In the worst-case situation, such as a huge fire, that might mean losing your entire business if you don’t have insurance.

If you have any of these particular items or places on your business premises, you might consider insuring them with commercial property insurance:

- Your business building, whether it is owned or rented;

- All office equipment, including computers, phone systems, and furnishings, whether owned or leased; and

- Accounting records and other corporate papers.

- Manufacturing or processing equipment

- Stocked inventory

- Fencing and landscaping

- Signs and satellite dishes

What doesn’t commercial property insurance cover?

Because insurers have a strong interest in limiting their risk levels, property policies are frequently constructed to exclude specific sorts of catastrophes or losses that may be particularly difficult to forecast or for which the insurer would find it difficult to reimburse.

Even more comprehensive plans, like special form insurance, include a list of risks the insurer would refuse coverage. To understand the scope and limitations of your coverage, you should thoroughly analyze any policy with your insurer. However, most insurers have comparable exclusions, which are as follows:

- Electronic information

- Business records (electronic and hard copy)

- Cash, securities, accounts, and bills

- Automobiles, airplanes, and watercraft

- Crops

- Animals

- Paved surfaces (e.g., walkways and roads)