If you own a business in New York, you probably already know that rates for workers compensation insurance are the highest in the country. Workers compensation insurance pays for medical costs should your employee become injured or fall ill while on the job. It’s required in New York, so you should consider getting a quote from several companies. Here are our top six picks.

- Top 6 Providers of Workers Compensation Insurance in New York

- Workers Compensation Laws in New York

- What Happens If I Don’t Have Workers Compensation Insurance in New York?

- Factors Affecting Your Workers Compensation Insurance Rates

- How Much does Workers Compensation Insurance Cost in New York?

- How to Find Cheap Workers Compensation Insurance in New York?

- What does New York Workers Compensation Insurance Cover?

- How does Workers Compensation Insurance Differ from General Liability Insurance?

Top 6 Providers of Workers Compensation Insurance in New York

We crunched the numbers and studied more than 20 insurance companies providing workers compensation insurance in New York state. Here are our recommendation of the top 6:

- CoverWallet: Best for comparing several quotes online

- New York State Insurance Fund (NYSIF): Best Overall

- The Hartford: Best for free additional coverages

- Biberk: Best for online quotes and purchase; and excellent financial strength

- Pie Insurance: Best for online quotes and purchase; and positive consumer reviews

- Huckleberry: Best for online quotes and purchase

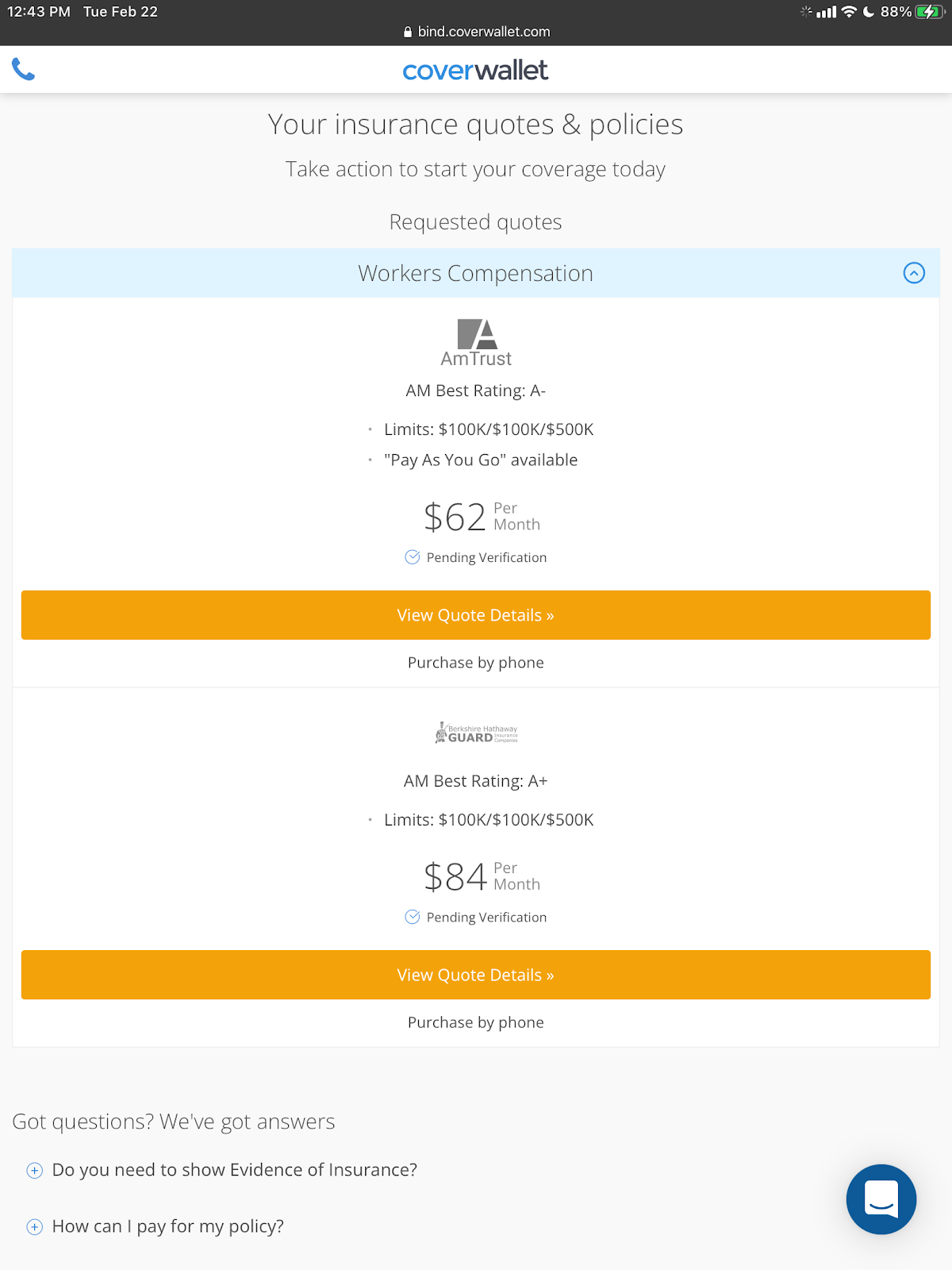

CoverWallet: Best for comparing several quotes online

CoverWallet is a digital broker specializing in small business insurance. They work with several leading small business insurance providers. The biggest benefit of working with CoverWallet is to be able to compare several quotes from these providers online after completing a simple quote form on CoverWallet. The quote process on CoverWallet only takes about 10 minutes or less.

CoverWallet has worked with several companies and they are able to pull quotes from these companies for small businesses in a wide range of industries. Regardless of the industry your small business is in, you can count on CoverWallet finding you the best quotes.

CoverWallet is a subsidiary of Aon, one of the biggest brokerage in the world. They also earn a good customer satisfaction rating of A on BBB.

Below is a quote sample from CoverWallet for a small accounting firm based in Brooklyn, New York, having 4 full time employees, $320,000 annual payroll, and $600,000 annual revenue.

New York State Insurance Fund (NYSIF): Best Overall

NYSIF is the largest insurer in the state of New York. Their mission is to provide the lowest possible rate for workers compensation insurance to employers and to provide timely indemnity and medical payments to injured workers. You answer ten questions and they can provide you with a quote. Questions include things like:

- Industry

- Estimated payroll

- Prior workers compensation insurance information

- Personal information

NYSIF is particularly good to get a quote from if you’ve had issues in the past, such as past claims or if you work in a high-risk industry.

The Hartford: Best for free additional coverages

We couldn’t get a quote from the Hartford, but there’s usually pretty competitive and are at least worth a look. They have thousands of positive reviews from happy small business owners, and if you need additional insurance, they have many small business policies. They add things to your policy that other companies charge for, such as extended filing and stop gap coverage. Read our review of the Hartford Small Business Insurance

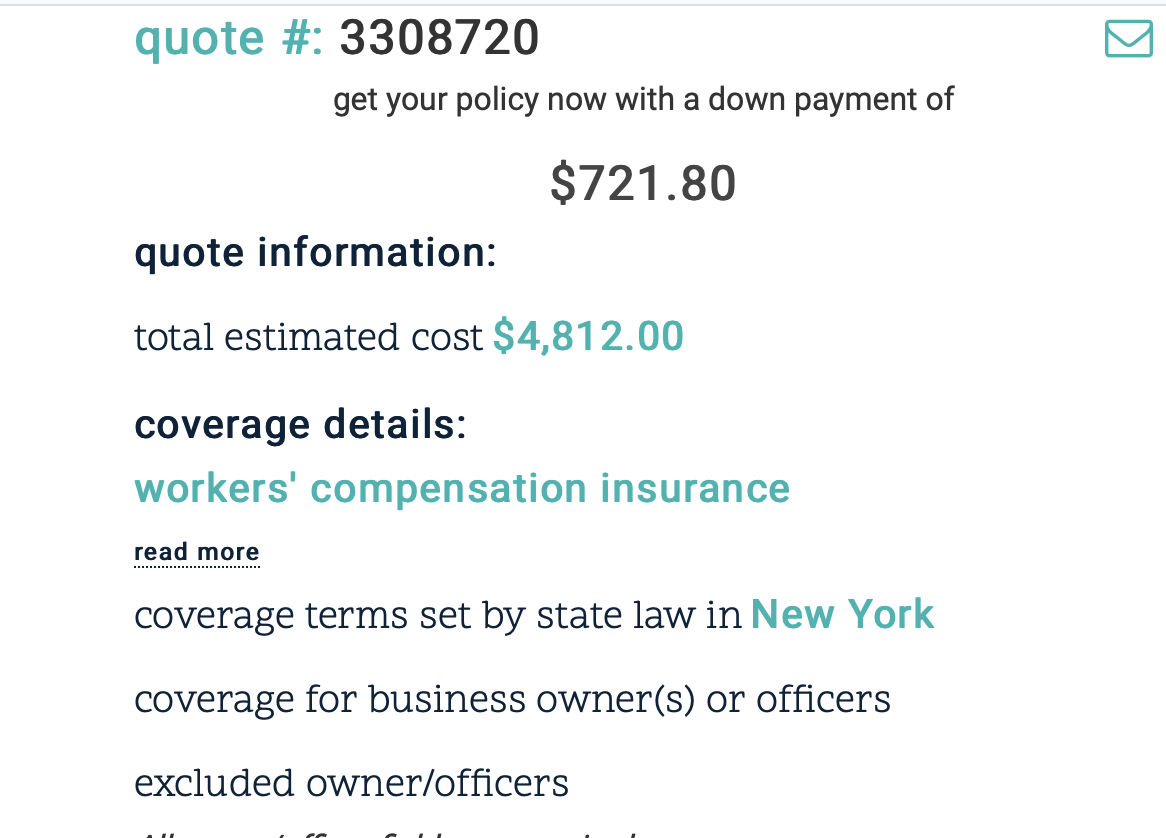

Biberk: Best for online quotes and purchase; and excellent financial strength

Biberk specializes in small business insurance. You can get a quote, pay, and get covered in less than ten minutes. They have thousands of positive reviews, and the rock solid financial strength that comes from being part of Berkshire Hathaway. The quote below is for a café in Albany with five employees and $160,000 in payroll.

Read our review of biBERK small business insurance.

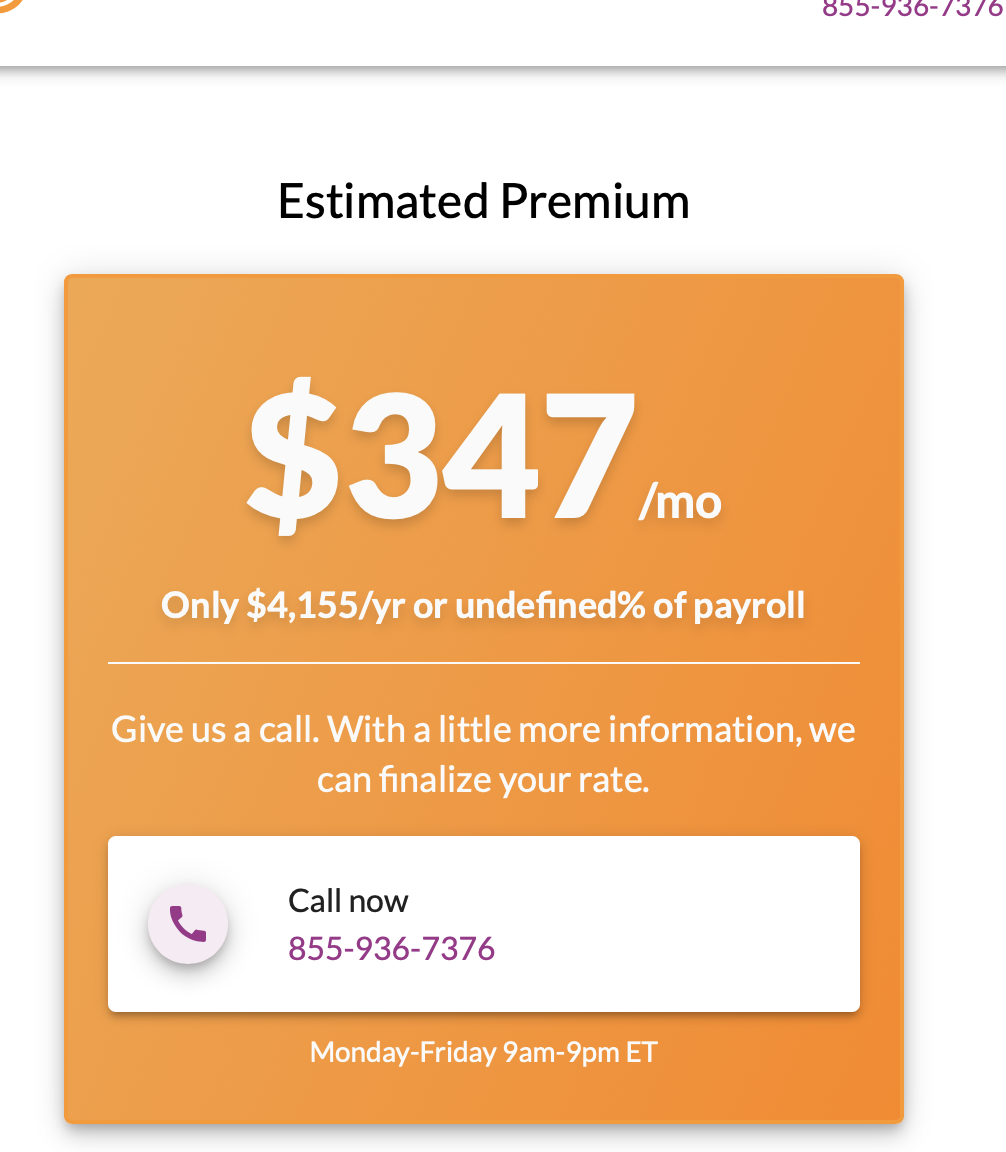

Pie Insurance: Best for online quotes and purchase; and positive consumer reviews

Pie has excellent reviews on Trustpilot with an average score of 4.6 out of five stars. Most of the reviews praise how easy it was to get insurance and how helpful and responsive the sales people were. You can get a quote online or you can call, if you prefer. They cover lots of different industries, and their rates are competitive.

Read our review of Pie Insurance

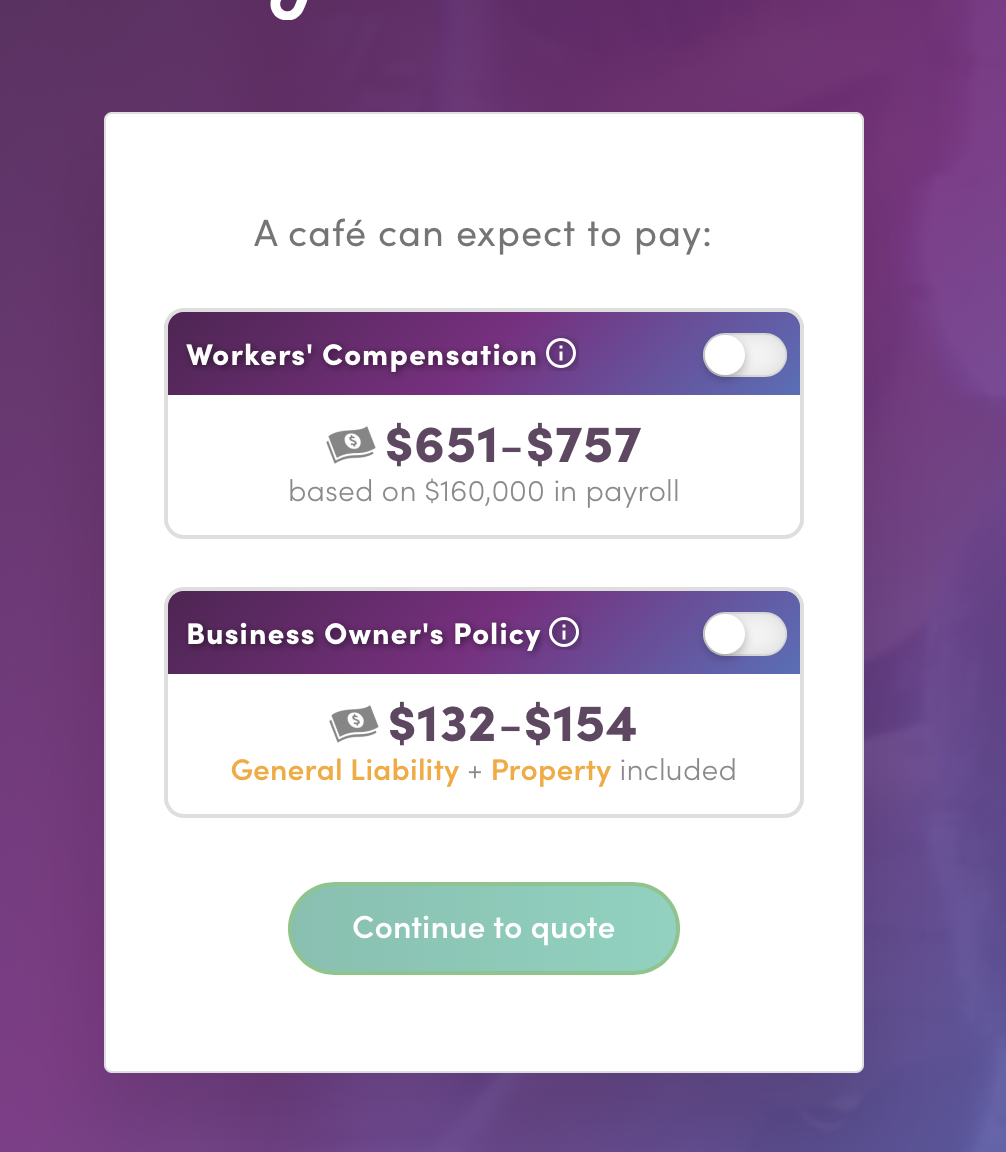

Huckleberry: Best for online quotes and purchase

Huckleberry is a relatively new company, but they’re backed by Markel, which has been in business since 1930. It’s easy to get a quote, and you can pay online and be insured in minutes. They cover lots of different industries, with optional coverages that include liquor liability, spoilage coverage and more.

The following is a ballpark estimate. You’ll know it’s official when you see a button that says “Pay now.”

Read our review of Huckleberry small business insurance

Workers Compensation Laws in New York

Like almost every state, workers compensation insurance is mandatory if you have one employee or more. The only exceptions are sole proprietors or business partners without employees, although you can buy it for yourself.

New York is also a no-fault insurance state, which means it doesn’t really matter whose fault it was that your employee injured themselves at work, they still receive benefits.

Part-time employees also count and you must get workers compensation insurance to cover them. You don’t need to get workers compensation for independent contractors, but the contractor has to not be under the employer’s control.

What Happens If I Don’t Have Workers Compensation Insurance in New York?

If you have five employees or fewer, you will be subject to a fine between $1,000 and $5,000. If you have more than five employees, it’s a felony and your fine will be somewhere between $5,000 and $50,000. If you say you have five employees when you really have seven, that could result in a fine of $2,000 for every ten days of noncompliance.

Factors Affecting Your Workers Compensation Insurance Rates

A lot of different factors affect how much you pay for workers compensation.

- State laws

- Type of business

- Level of risk

- Prior experience

- Claims history

According to Workers Compensation Shop, the rates for a café in New York range from a low of $2.06 to a high of $4.02 per $100 of payroll. The industry that you’re in is the biggest factor, since the more risk your employees are exposed to, the more money you’ll pay.

If you’d like a formula to figure out your workers compensation rate, it’s roughly:

Class code x experience modification rate x payroll = premium

The experience modification rate reflects things like how many years you’ve been in business and how many workers compensation claims you’ve filed in the past.

You’re probably wondering how you figure out what your experience modification rate is and how to calculate it. There’s a handy rate calculator at Optimum Safety Management.

How Much does Workers Compensation Insurance Cost in New York?

Workers compensation insurance is required in New York state if you have any employees at all.

The good news if you’re a New York employer is that workers compensation rates have gone down and are now at $1.41 per $100 of payroll. You multiply that by the class code dollar number, and then multiply that by the number of employees you have.

Some examples of what you’ll pay for different occupations by class code:

- Jewelry manufacturing: $0.53

- Bookbinding: $3.15

- Road construction: $13.74

- Asbestos Contractor: $29.64

- Clerical: $0.13

- Healthcare: $4.53

For a complete list of class codes in New York State, click here.

This means that if your company operate a clinic. For every $100 payroll you pay your healthcare employees working in the clinic, you have to pay $4.53 in workers compensation insurance. This can get really expensive for companies in road construction or asbestos contracting, so be sure to shop around with a few companies or a digital broker like CoverWallet so that you can compare several quotes before deciding on the cheapest one for your company.

Below is the summary of the workers comp insurance cost from the three top providers fo a small cafe in Albany, NY:

| Carriers | Workers comp insurance cost in New York |

| biBERK | $721.8/month |

| Pie | $347/month |

| Huckleberry | $651 – $757 / month |

>>MORE: How Much does Workers’ Compensation Insurance Cost?

How to Find Cheap Workers Compensation Insurance in New York?

You probably already know that workers compensation insurance is the most expensive in New York. It can be a significant cost to your business. Not having workers compensation insurance can result in even more costly consequences. Make sure you follow the tips below to get the cheapest workers compensation insurance for your company in New York.

Always compare several quotes:

Make sure you shop around with a few insurance companies or a digital broker to compare several quotes to get the cheapest one for your business

State programs:

Check if there is any state savings program in New York that your business can be qualified for.

Group insurance:

If your company is a member of a larger association, you may be able to get a group rate on your company’s workers compensation insurance.

Identify potential hazards and fix them.

Once you fix them, make sure you notify your insurance agent (if you have one) or report it to your company. Continue improving the safety standard in your company’s workplace and ask for annual reviews when you need to renew your company’s workers comp insurance.

Invest in safety education.

According to Safety and Health, for every dollar you spend on injury prevention, you’ll earn a ROI of between $2 and $6 dollars. If you’re wondering how to start a safety program, OSHA (Occupational Safety and Health Administration) is a good place to start. After starting the program, you need to make sure to obtain the qualification certificate from the program administrator. Showing the certificate to your workers compensation insurance insurer or agent can help reduce the cost when you renew the policy.

Check classification levels.

Every employee type is assigned a classification level, and each level is assigned a rate that reflects the level of risk this type of job has. Obviously, a secretary is exposed to much less risk than a construction worker, even if they work at the same company. Make sure everyone is classified accurately and regularly update this as you are hiring new employees.

What does New York Workers Compensation Insurance Cover?

Workers compensation insurance covers you if your employees becomes ill or gets injured while at work. It pays for:

- Medical payments

- Disability

- Death benefits

- Lost wages

If your employee injures themselves over the weekend while snowboarding, then you’re not responsible for that—they must be injured at work.

>>MORE: How to Find Cheap Workers Compensation Insurance?

>>MORE: Best 7 Workers’ Compensation Insurance Companies for Small Business

Who are exempt from workers compensation insurance in New York?

All employers in the New York state are required to provide workers’ comp coverage. Some exemptions include:

- Certain real estate salespeople, media sales representatives, insurance agents and brokers who work under a contract that defines them as independent contractors

- Coaches and supervisors of athletic teams operated on a nonprofit basis as long as they aren’t professional athletes or work for a professional athletic organization

- People who volunteer their time and services to nonprofit organizations and are not compensated for it

- People who work in religion, including:

- Duly ordained, commissioned, or licensed ministers, priests, and rabbis

- Sextons

- Christian Science readers

- Members of religious orders

- Federal government workers covered under federal workers’ compensation laws

- Interstate railroad employees that are covered by another workers’ comp system

- New York City police officers, firefighters, and sanitation workers who are covered by the New York State General Municipal Law

- People who teach at nonprofit religious, charitable, or educational institutions

- People who do non-manual work for nonprofit religious, charitable, or educational institutions

- Persons who receive charitable support from a religious or charitable institution and do work in return for it and are not under contract to perform the tasks

- People who work in certain maritime trades

- People, including minors, who do yard work or other chores for pay in and around one-family, owner-occupied homes or for nonprofit, noncommercial organizations

- Sole proprietors, partners, and one or two person corporate offices that have no one else providing business services to the organization.

- Spouses and minor children of farmers, as long as they are not contracted to work for the farm business.

Workers compensation insurance in Long Island, New York

Workers compensation insurance coverage is the same across the state of New York, including Long Island. Long Island workers comp insurance provides medical expenses, lost wages, disability benefits, and other related benefits to workers when they are injured and become ill at work.

Workers compensation insurance in Syracuse, New York

Small businesses employ more than 25,000 employees in Syracuse, New York. They are required to provide workers comp insurance coverage for all employees.

Workers comp insurance coverage in Syracuse is the same as in the broader New York state. It provides medical payment, lost wages, disability benefits, and other related benefits, including retraining expenses for the new occupation, if employees are injured or become ill at work.

How does Workers Compensation Insurance Differ from General Liability Insurance?

Some people do get confused about this because they know that general liability insurance covers bodily injuries. That’s true, but general liability insurance only covers bodily injuries that happen to your clients or your customers. Employees who injure themselves are covered under workers compensation insurance. If you as a business owner personally get injured, general liability doesn’t cover that either. Workers compensation insurance would cover you, assuming you included yourself in the policy.

>>MORE: Cheapest General Liability Insurance for Small Businesses

Last Thoughts

New York has expensive rates for workers compensation insurance, but you can’t skip it, as that will lead to fines and possible lawsuits. Shop around for the best rate, and make sure you emphasize safety at your job sites.

>>MORE: Top 5 Providers of General Liability Insurance in New York