There are currently more than 650,000 small businesses in Colorado. If you own a small business in the state, you probably need workers’ compensation insurance. If you have anyone working for you, Colorado law requires you to have it. If you don’t have coverage that meets standards set by the state, you could face significant financial penalties.

In this article, we’ll cover:

- 5 best workers’ compensation insurance companies in Colorado

- Workers’ compensation laws in Colorado

- What does Colorado workers’ compensation insurance cover?

- What doesn’t workers’ compensation insurance cover?

- How is workers’ compensation insurance different than general liability insurance?

- How much does workers’ compensation insurance cost in Colorado?

- How to find cheap workers’ compensation insurance in Colorado

- Important timing information related to filing workers’ comp claims in Colorado

5 best workers’ compensation insurance companies in Colorado

We checked out countless companies that offer workers’ compensation insurance in Colorado to come up with our top five for different reasons.

- Simply Business: Best for finding the cheapest workers comp coverage

- CoverWallet: Best for businesses that want to compare quotes quickly

- Cerity: Our top choice for stand alone workers’ comp coverage in Colorado

- The Hartford: Best for businesses that want to partner with a sound and ethical insurer

- biBERK: Best for low-cost coverage from a top carrier

- THREE: Best for simple and easy-to-understand policies with comprehensive coverage

Simply Business: Best for finding the cheapest workers comp coverage

Simply Business is an insurance brokerage firm, focused 100% on serving small and medium-sized businesses. Simply Business offers all coverages that small or medium-sized businesses may need. They work with 30+ carriers with one single goal of helping small businesses find the coverage they need at the cheapest rate available. If your main goal is to find the cheapest rate quickly, you may want to work with Simply Business.

Pros:

- Easy to get and compare several quotes to find the cheapest one

- All carriers have good financial strength ratings and tend to offer low-cost coverage. These carriers may not be easily accessible outside of Simply Business platform

- Great customer satisfaction rating on trustpilot

Cons:

- In some cases, quotes may not be available online. You have to call to discuss your cheapest quote options

- If you prefer working with a particular carrier that Simply Business doesn’t work out, you may need to look elsewhere

CoverWallet: Best for businesses that want to compare quotes quickly

CoverWallet is a cutting-edge insurance provider. The firm has developed their own state-of-the-art platform, based on its own algorithms, to ensure it is able to connect small businesses with the workers’ comp coverage they need at the best possible price. The platform makes it quick and easy to get quotes from many providers at once, making it possible to compare quotes from several highly reputable insurers.

The firm’s experts have used their extensive experience to make sure you only answer the questions you have to — and provide the information required — to generate quick and accurate quotes. The entire process should take less than ten minutes from start to finish.

You can also rest assured knowing that CoverWallet is a part of Aon, an established company that provides advice to businesses on things like risk, health and retirement.

Once you get your quote, it’s easy to purchase a policy online or through an agent. When you get your workers’ comp coverage through CoverWallet, it’s simple to manage your policies online, including downloading your certificate of insurance, filing a claim, renewing your policy and more.

In addition to all this, you can get other types of coverage through CoverWallet, which makes it efficient to secure and manage all your small business coverage.

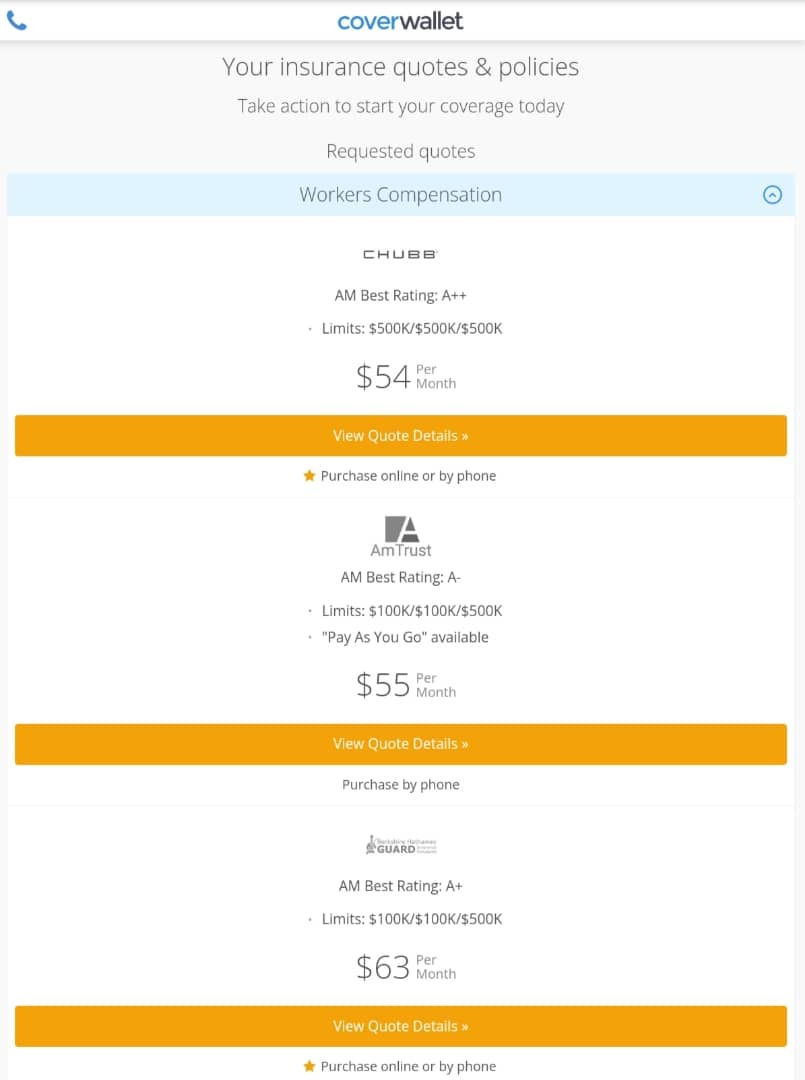

Below is a quote sample from CoverWallet for an accounting firm with 2 full time employees, an annual payroll of $170,000, and annual revenue of $450,000.

Cerity: Our top choice for stand alone workers’ comp coverage in Colorado

Cerity makes our list of top workers’ compensation providers because it specializes in the coverage. It currently does not offer a Business Owners Policy or other types of insurance. It’s a relatively low cost provider, yet delivers a high level of service. Policies start as low as $25 per month and the company has fewer fees than most insurers. Cerity makes it fast and easy to get a quote online.

Cerity isn’t low cost because it cuts corners. It actually uses artificial intelligence to up its efficiency. However, everything at Cerity isn’t technology based. When you require help, you will have access to a team of licensed policy and claims experts. You can rest assured knowing Cerity has been in business for more than a century and is rated highly by their clients.

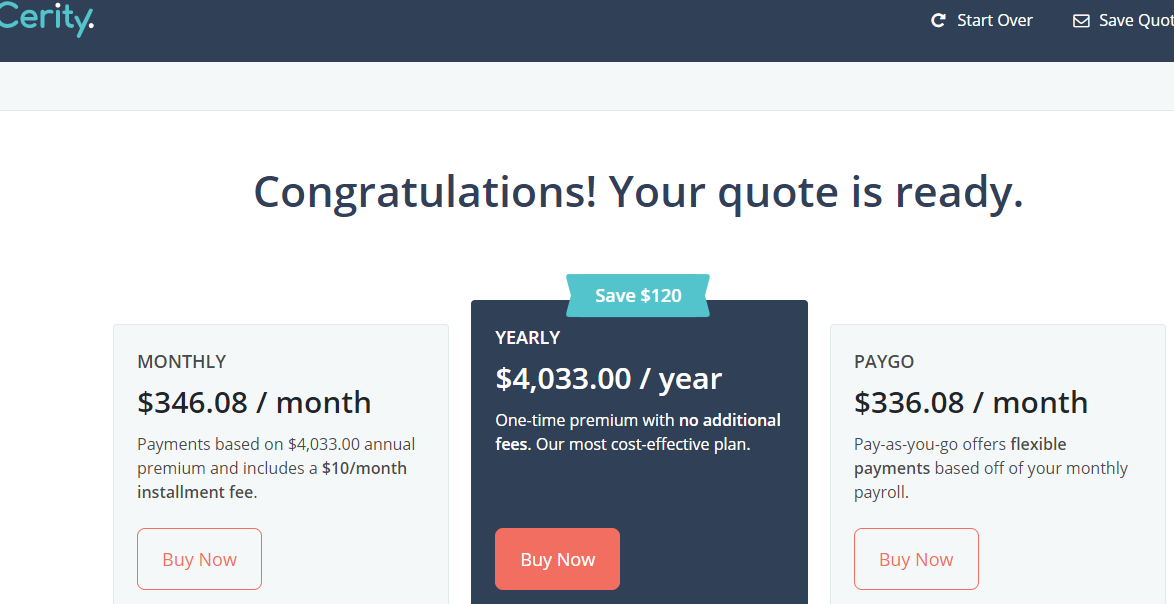

Below is quote sample from Cerity. As you see, it isn’t the cheapest quote.

The Hartford: Best for businesses that want to partner with a sound and ethical insurer

The Hartford is one of the oldest companies of any kind in the United States. It’s been offering insurance solutions for more than 200 years and has helped one million plus businesses with their insurance needs. The company takes pride in the fact that the Ethisphere Institute named The Hartford a World’s Most Ethical Company twelve times. The Hartford’s longevity and focus on ethics makes it a company that you can feel good about entrusting your business to.

The Hartford offers some unique features as part of its workers’ comp insurance coverage including:

- A preferred medical provider network which makes it easy to get access to medical professionals all over Colorado experienced in treating workplace injuries.

- A prescription drug program that includes pharmacies all over Colorado that are able to fill prescriptions, usually with no out-of-pocket costs. The program also includes convenient mail order service.

- The needle stick reimbursement program helps pay for the initial testing of someone who works for you and their patient if the worker gets hurt with a needle. It also pays for ongoing testing, if necessary.

- The nursed back to health program has experienced nurses to help coordinate medical care and provide therapeutic support.

- Pay as you go billing solutions that base your workers’ comp coverage on your actual payroll. This is great for companies that have a regularly changing workforce and want to get better control over their cash flow.

The Hartford is a solid and ethical insurance provider you’ll feel good about working with.

biBERK: Best for low-cost coverage from a top carrier

biBERK is a subsidiary of Berkshire Hathaway. They focused completely on selling insurance coverage to small businesses. Workers comp insurance is one of their coverage offerings. biBERK sells insurance completely online, offering a simple and fast online quoting. Within 10 minutes any small business owner should be able to buy a workers comp insurance policy on their website

Pros:

- Backed by one of the very best insurance brand names, Berkshire Hathaway, with unparalleled financial strength and reputation

- One of the best digital experiences, from getting quotes, buying a policy, and managing the policies completely online

- One of the most affordable rates in the industry. They claim that their customers save 20% on average

- Great customer support experience, including claim assistance

Cons:

- Their policies may have lower coverage, although still satisfying the minimum coverage requirements by the state. If you compare several policies, you should pay attention to the coverage limits of all policies

- If you prefer working 1:1 with an agent in-person, you may look elsewhere

THREE: Best for simple and easy-to-understand policies with comprehensive coverage

THREE is another direct-to-consumer carrier belonging to the Berkshire Hathaway family. THREE was founded with a belief that all business insurance policies should be less than 3 pages and free of insurance jargon.

Pros:

- Great digital experience. Easy to get quotes, buy a policy, and manage a policy online

- Simple and extremely easy-to-understand policies

- No exclusions buried in the policy’s fine print

- Comprehensive coverage

Cons:

- Rates may not be as competitive, but reasonable for a comprehensive coverage

- Online quotes may not be consistent. Sometimes you have to call to get quotes

>>MORE: 10 Best Workers Comp Insurance Companies

How to buy workers comp insurance in Colorado?

You can choose one of the following 4 ways to buy workers comp insurance in Colorado:

- from a digital brokers like CoverWallet or Policy Sweet or Commercialinsurance.net;

- from a insuretech company like Pie or Cerity;

- from a traditional insurance companies like the Hartford, AmTrust, Employers, Travelers, etc;

- from the state fund

- or apply for self-insurance

Each way has its own pros and cons and why it makes sense for you to make sure you compare several quotes to select the cheapest one for your company. Learn more about the details at Buy workers comp insurance in Colorado online.

Workers’ compensation laws in Colorado

Colorado’s workers’ compensation requirements are simple when compared with many other states. The law states that if you have one or more employees working for you, you must have workers’ compensation insurance and maintain it at all times. This applies to all employers, along with all types of employees, whether they are part-time, full-time or family members, with a few exceptions. Colorado has additional insurance requirements for companies in the construction industry. (Your insurance agent can advise on these if they apply to you.) Failure to carry workers’ comp insurance in Colorado could result in fines.

Exceptions to the requirement to carry workers’ comp coverage include people in the following positions:

- Sole proprietors

- Corporate officers

- Limited liability company members.

Although not required, these types of workers can choose to get the coverage.

Colorado also requires that employers must:

- Display a Notice to Employer of Injury poster

- Record all lost time related to injuries and incidents of occupational diseases

- File an Employer’s First Report of Injury with their insurance company within ten days of an incident

- File Supplemental Report of Accident forms with their insurer when injured or ill people return to work or are terminated.

What does Colorado workers compensation insurance cover?

In Colorado, workers’ comp insurance helps cover:

- Accidents or injuries: Workers’ compensation pays medical costs if an employee gets injured while on the job

- Illness: If a worker is exposed to harmful chemicals or allergens in the workplace that cause an illness, their medical care is covered by workers’ comp

- Lost wages: A work-related injury or illness often forces employees to take time off. Workers’ comp helps replace the lost wages of injured or sick employees while they’re recovering

- Ongoing care: If a workplace injury or illness requires an employee to get ongoing care, such as physical therapy, workers’ compensation will pay for the treatment

- Funeral costs: If an employee passes away because of a work-related incident, workers’ comp pays funeral costs up to a certain limit

- Repetitive injury: If a worker is injured because of ongoing repetitive job related strain, such as carpal tunnel syndrome, workers’ comp will pay for therapy

- Disability benefits: If an injury is so severe an employee never returns to work, or doesn’t for a long time, workers’ comp will pay medical costs and some lost wages over the long term.

What doesn’t workers compensation insurance cover?

Workers’ compensation insurance does not cover things like:

- Injuries to independent contractors, clients or customers

- Employees who are intoxicated or high when they’re injured

- Wages for temporary employees while recovering from a work-related injury

- OSHA fines

- Injuries that occur after the employee has left work

- Vandalism or intentional injuries.

How is workers compensation insurance different from general liability insurance?

Workers comp only covers people who work for you. If a client, customer or random person is injured at your workplace or job site, general liability insurance will cover it. General liability covers bodily injury and damage caused by you or an employee to someone else’s property.

>>MORE: Best General Liability Insurance Companies

How much does workers compensation insurance cost in Colorado?

On average, workers compensation insurance cost in Colorado is $0.95 for $100 payroll. The final workers comp insurance cost for your firm depends on a number of factors, including your:

- Number of employees and size of payroll

- Industry and type of work

- Workplace risks

- Company claims history

- Business age or years in operation.

Taken together, all these things will determine your final premium cost. Different insurance companies will always offer you different quotes, so be sure to shop around with a few companies or with a digital broker like CoverWallet to compare several quotes to select the best and the cheapest one for you.

>>MORE: How Much does Worker Comp Insurance Cost?

How to find cheap workers compensation insurance in Colorado

Businesses in Colorado are able to choose their own workers’ comp insurance provider. You owe it to yourself to compare coverage and costs from several insurers. They have different ways of calculating premium costs and you will likely find a range of prices. You can select the one that offers you the coverage you need at the best possible cost.

Some insurance companies offer good discounts if you have appropriate safety programs in place. Implementing and maintaining these safety programs will reduce your workers comp insurance premiums over time as well.

You can also bundle different business insurance policies to earn additional discounts.

>>MORE: Cheapest Workers Comp Insurance Companies

Important timing information related to filing workers’ comp claims in Colorado

You should be able to find everything you need to file claims on the workers’ comp page of your insurance company’s website. Employees and employers have time limitations when it comes to making claims in Colorado.

- Four days for employees to report work-related injuries to their employers

- Ten days for employers to report employee injuries to their insurance company

- Twenty days for the insurer to respond to a claim.

If a claim is rejected by an insurer, it can be appealed through the Colorado Division of Workers’ Compensation.

Do independent contractors and 1099 employees need workers comp insurance in Colorado?

In Colorado, independent contractors and 1099 employees are not required to have workers’ compensation insurance, and employers are not required to provide it for them. However, if an independent contractor or 1099 employee is injured while working, they may be eligible for workers’ compensation benefits if they can prove that they were an employee, rather than an independent contractor, at the time of the injury.

To determine employee status, Colorado uses a multi-factor test that considers factors such as the degree of control exercised by the employer, the level of skill required for the work, and the type of relationship between the worker and the employer.

If an independent contractor or 1099 employee is misclassified and injured while working, they may be able to receive workers’ compensation benefits from their employer, but they would need to take legal action to prove that they were wrongly classified and to collect the benefits.

It is recommended that independent contractors and 1099 employees obtain their own workers’ compensation insurance coverage to protect themselves in case of on-the-job injury or illness.

Learn more at workers comp insurance requirements for independent contractors and 1099 employees in different states