On August 1, 1915, the Colorado State Legislature followed in the footsteps of authorities in other states in the US by enacting legislation mandating company owners to have workers’ compensation insurance.

While the law has seen a few amendments over the years, the purpose of the legislation has not. So, if you have employees and own a business in Colorado, you must obtain Colorado workers’ compensation insurance.

In this article, we’ll tell you exactly what you need about this policy and how to get it in Colorado.

As an employer in Colorado, you can obtain your workers’ compensation in different ways. To get your policy consider the following options:

- Buy workers comp insurance in Colorado from digital brokers

- Buy workers comp insurance in Colorado from insuretech companies

- Worker’s comp through self-insurance in Colorado

- Buy workers comp insurance in Colorado from the state fund

- Buy workers comp insurance in Colorado from traditional insurance companies

- Is workers’ compensation insurance required in Colorado?

- Workers’ comp exemptions in Colorado

- What benefits do workers comp insurance provide in Colorado?

- What is the cost of workers’ compensation insurance in Colorado?

Buy workers comp insurance in Colorado from digital brokers

A digital broker does not provide insurance; instead, they collaborate with giant insurance firms to help company owners obtain appropriate insurance plans.

You may quickly compare quotations from several firms with the help of these companies. As a result, you will be able to make quick judgments about where to get your worker’s compensation insurance. Examples include CoverWallet, CoverHound, Policy Sweet, and others.

To purchase insurance from one of these businesses, simply go to their website. There you will fill in your details and get your online quotations in less than 10 minutes.

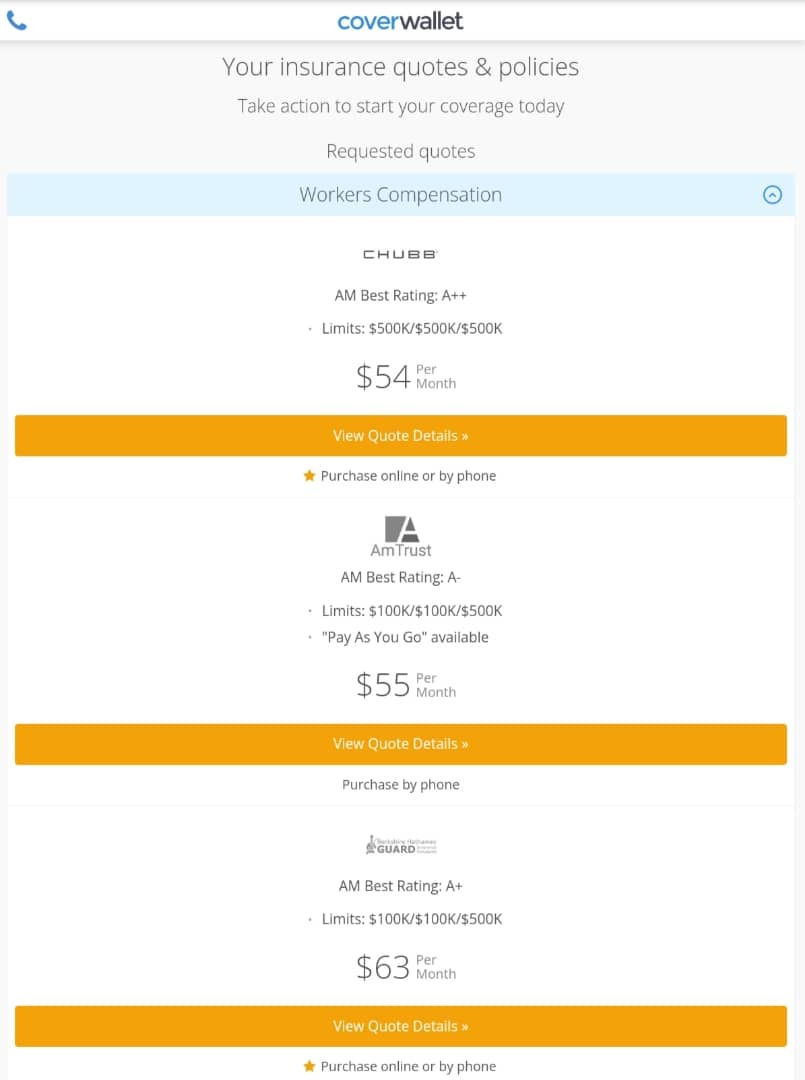

Here is a sample quote generated from CoverWallet for a small accounting firm with 2 full-time employees, an annual payroll of $170,000, and annual revenue of $500,000 located in

Pros of buying from a digital broker

- Digital brokers make it easy to find and compare quotes

- They are perfect for new business owners that don’t know where to start

- You can monitor and manage multiple policies on these websites

Cons of buying from a digital broker

- Digital brokers only offer policies from their partners. That means you have limited options.

Buy workers comp insurance in Colorado from insuretech companies

Insuretech companies are relatively new in the insurance space. These companies leverage the latest technology to help companies find the cheapest and most suitable insurance policies.

The internet has given rise to the growth of these companies, and there are many of them today. Good examples include Cerity, Pie, Biberk, etc., and most of them provide workers’ compensation insurance.

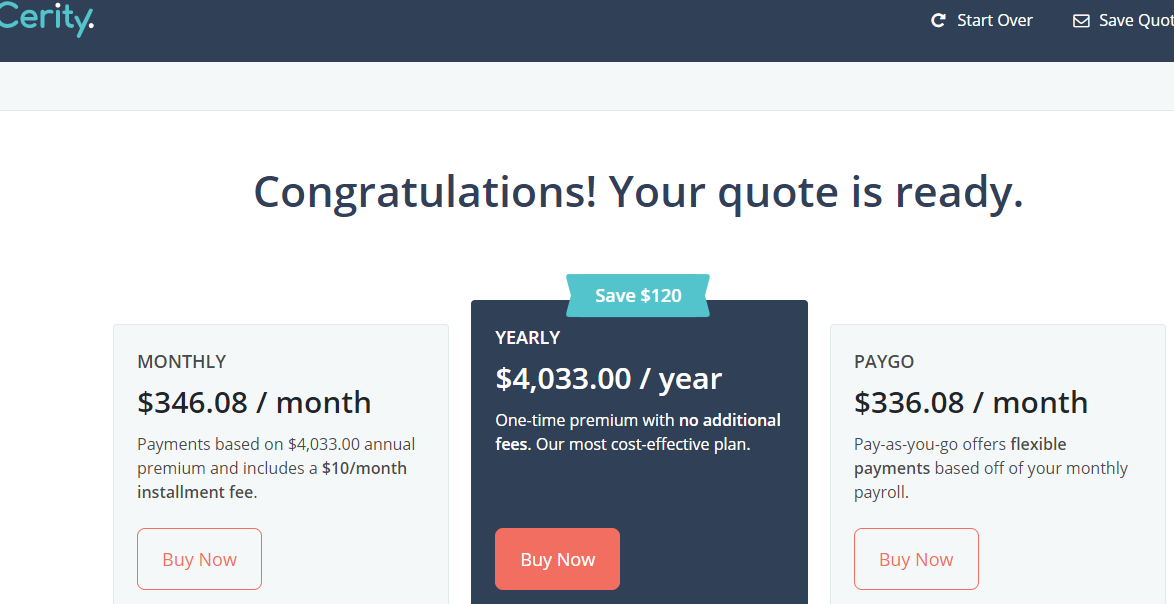

The following is a sample quote generated from Cerity for a small accounting firm with 2 full-time employees, an annual payroll of $170,000, and annual revenue of $500,000.

Pros of using Insuretech companies:

- You get instant online quotes from these companies

- They use data and artificial intelligence to find the best policy for you.

- They can help you find discounts.

Cons of using insuretech companies

- They offer limited types of insurance policies

- Most of them are new companies that do not have enough experience.

Worker’s comp through self-insurance in Colorado

Self-insurance is another method of getting worker’s compensation. Employers on this policy pay for the liabilities themselves.

Employers must have at least 300 employees or $100 million in assets to qualify for self-insurance. However, if the company wants the policy and cannot meet the requirement, they can join a group or pool for workers’ compensation insurance. This program is run by the Division of Insurance in the Department of Regulatory Agencies.

Pros of self-insurance

- Some self-insurance groups in Colorado sometimes pay excesses back to their members at the end of the year.

- It might be a less costly option if there are not many injuries

Cons of self-insurance

- Most small businesses in Colorado cannot meet the requirements for the policy.

- The employer might face significant financial losses if there are reoccurring accidents.

Buy workers comp insurance in Colorado from the state fund

The final option is to use the Colorado State fund insurance. Colorado State has a competitive workers’ compensation state fund administered by Pinnacol Assurance. This option is suitable for companies that cannot find suitable policies.

Buy workers comp insurance in Colorado from traditional insurance companies

The most common method of buying workers’ comp in Colorado is to get the coverage directly from the insurance company of your choice.

Most of the time, the procedure is uncomplicated and straightforward since you can obtain your quotes online. After providing the essential information, you should receive your quote in around 5 minutes.

Some examples where you can find workers’ compensation in Colorado at reasonable rates include the following:

- Liberty Mutual

- Nationwide

- The Hartford

- Employers,

- Travelers, etc.

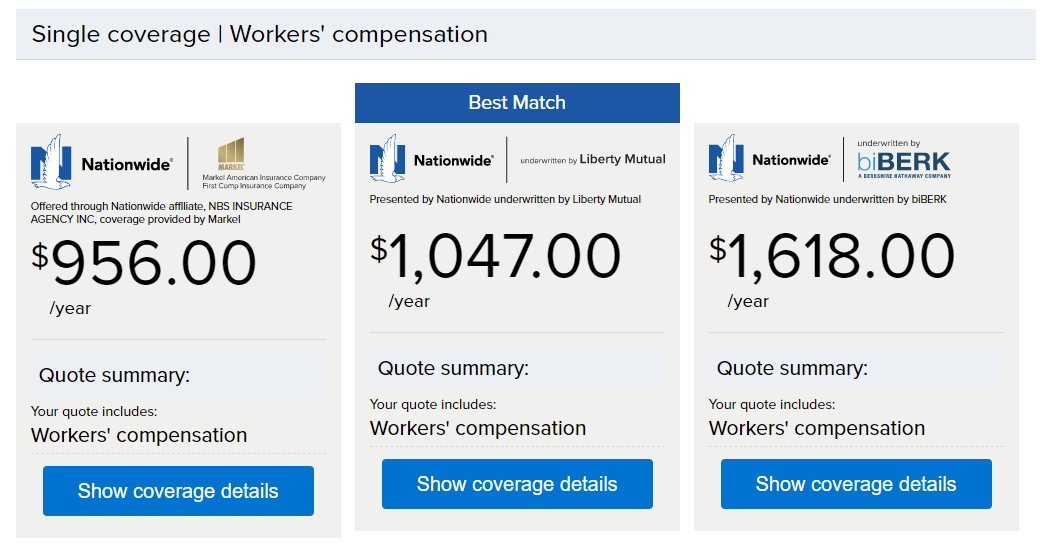

The following is a sample quote for workers’ comp for a small accounting firm with 2 full-time employees, an annual payroll of $170,000, and annual revenue of $500,000 from Nationwide Insurance.

We notice that Nationwide offers quote comparison from several insurance companies as an agency. The lowest quote is from Markel at $956/ year or $79.7/month.

Pros of buying from a traditional insurance company

- The process is usually straightforward, fast, and accessible.

- Since these are standard insurance companies, you can bundle this policy with other policies and get discounts.

- These companies have years of experience and superior financial strength

Cons of buying from a traditional insurance company

- If you are new to buying worker’s compensation, you might not know which company to choose.

- You might get expensive premiums.

Learn more at the best workers comp insurance companies in Colorado.

How does workers’ comp function in Colorado?

Workers’ comp insurance is a protection policy that benefits Colorado employers and employees. The primary goal of the policy is to assist employees with essential medical treatment and salary replacement if they are harmed on the job.

On the other hand, the policy protects employers due to the exclusive remedy. The exclusive remedy states that an employee who takes workers’ compensation payments cannot sue their employer for their injury.

More so, many of these plans include employer liability insurance. The plan helps pay for legal costs if an employee sues the company for an injury.

The Division of Workers’ Compensation in Colorado enforces compliance with Colorado workers’ compensation rules. It also offers information to businesses and employees regarding the policy.

In a conflict or related concerns, the division also offers resolution, and it manages self-insurance programs.

Is workers’ compensation insurance required in Colorado?

Workers’ compensation insurance is required in Colorado for all employees, whether public or private. In general, any person who performs work or provides services is considered an employee. That means whether the person works part-time or full-time.

That said, any Colorado company with one employee or more must offer Workers’ comp to all its employees.

Workers’ comp exemptions in Colorado

Although companies in Colorado must provide workers’ comp for all their employees, not every worker in Colorado qualifies as an employee under the state’s laws.

For instance, sole proprietors, working partners, some corporate officers, and members of limited liability cooperation may not be considered employees. People in this category may decide to opt for workers’ comp insurance.

Also, an independent contractor may be exempted from worker’s compensation. However, the exemption is subject to the following conditions:

- Such a person works outside the control of the business hiring him

- Such persons operate a business that offers the service he is hired for.

Other workers that are generally exempted from having worker’s comp insurance include the following:

- Maintenance or repair work that costs less than $2,000 per calendar year

- Domestic work that is less than 40 hours per week or fewer than five days per week

- Commission-based real estate agents and brokers

- Self-employed persons

What benefits do workers comp insurance provide in Colorado?

The finest workers’ compensation insurance in Colorado packages often includes many components. The coverages are as follows:

Unpaid Wages

The missing pay section of a workers’ compensation policy refers to income replacement benefits. The amount of missing pay received by an employee is determined by whether the disability is partial or whole. They also differ depending on whether the handicap is temporary or permanent. The benefit is often a percentage of the employee’s weekly income, based on actual earnings or the state average earnings for the occupation.

Medical Bills

Your workers’ compensation policy also covers medical bills. The medical payments section commits to pay for your workers’ medical expenditures incurred due to an industrial injury or sickness. The policy will cover everything, including medical supplies, Medicare, and other reasonable costs.

Rehabilitation costs

Employees who cannot return to work due to work-related sickness or injury may need to seek alternative employment. Usually, this part of the insurance policy covers schooling or work retraining required for the employee.

Death Benefits

This policy also covers death benefit payments in the unfortunate event that the worker dies. If a worker dies in a work-related event, this benefit compensates for funeral and burial expenses. The death benefits part of workers’ compensation may also compensate eligible dependents for a while.

What if I don’t have required workers’ compensation insurance in Colorado?

In Colorado, failing to have workers’ compensation insurance might mean severe fines for your business.

If a company is operating without adequate insurance, the director of the Division of Workers’ Compensation may issue a cease-and-desist order. Such an order would require such a business to halt all activities until it acquires proper insurance.

Uninsured employers may face fines of up to $250 every day they fail to maintain insurance coverage. If numerous offenses occur, the penalties may be as much as $500 each day.

Also, companies that do not offer insurance risk getting sued by their employees.

What is the cost of workers’ compensation insurance in Colorado?

Workers’ compensation in Colorado costs usually depends on your payroll. The larger your payroll, the more you will likely pay for Worker’s compensation. That said, the rate of workers’ comp in Colorado is about $0.86 for $100 of covered payroll.

In addition to payroll, the following are some other factors that determine the cost of your premium:

- Location of business in Colorado

- Employee Count

- Industry and Risk Factors

- Insurance limitations

- Claims history

Different insurance companies always provide you with different quotes and rates. Be sure to shop around with a few companies or a digital broker to compare several quotes to choose the cheapest and the best one for your company.

Learn more at how much workers comp insurance costs and how to calculate it.

Who pays for workers’ compensation insurance in Colorado?

The employer is responsible for the payment of worker’s compensation in Colorado. Under no circumstance should an employer charge his employees for workers’ comp insurance in Colorado.

How do I find cheap workers’ comp insurance in Colorado?

The Colorado Division of Workers’ Compensation provides discounts to company owners that take proactive steps to prevent accidents.

If you want a discount, consider doing the following:

- Apply to the Premium Cost Containment Board

- Commit to a risk management plan for at least one year

If accepted, your company may be eligible for a 10% decrease in workers’ compensation rates. In addition to the above, you can also do the following to qualify for discounts from your insurance company:

- Pay your premium in full.

- Bundle as many policies as you can into one.

- Pay online with your credit card.

Learn more at the cheapest workers comp insurance companies.