Handymen do a lot more than just putter around clients’ homes fixing things. They often work with dangerous tools, do tasks at significant heights, carry heavy items, and perform duties around expensive, fragile, and breakable items. These are just a few of the risks faced by handymen and women every day.

Note: We are using the term handyman not because we agree with it, but because it is the insurance industry standard.

In this article, we’ll explain everything you need to know to get the coverage that’s right for you at a fair price and reveal the top four insurance companies for handymen and what makes each one unique.

- How much does handyman insurance cost?

- What factors affect the handyman insurance cost?

- How can I find cheap handyman business insurance?

- What types of insurance are needed for a handyman business?

- What other types of insurance do handymen get?

- Is handyman insurance required to operate a business?

- Top 5 insurers for handyman coverage

How much does handyman insurance cost?

Handyman insurance is relatively inexpensive. The typical policy runs between $350 and $1,000 per year. The average cost of handyman insurance is $65 per month or $800 per year. This is only for the most essential policy that all handymen would need, which is general liability insurance. Of course, if you add more coverage, the cost will increase. Below is the breakdown of the handyman insurance costs for different coverages:

| Handyman insurance coverages | Average costs |

| General liability insurance | $65 a month |

| Commercial auto insurance | $150 a month |

| Workers comp insurance | $315 a month |

| Contractor tools and equipment insurance | $15 a month |

These are just the averages. It’s a good idea to get a few handyman insurance quotes from different providers and compare coverages and costs. Working with a broker like CoverWallet, Simply Business, or InsurePro is a good way to get several quotes and compare them easily. It’s the only way to get the protection you need at the best possible price.

What factors affect the handyman insurance cost?

There are several factors affecting the handyman insurance cost. Below are some important ones:

The service that you offer

A handyman is an umbrella term for different types of contractors. Sometimes, a handyman can perform as simple work as fixing a fence or repainting a desk. Some other times, they can do riskier work such as trimming trees, or repairing a leaking roof, or building a new deck, etc. Different services have different kinds of risk exposure and different levels of risk.

Construction and contracting businesses tend to pay the highest premiums for general liability coverage. Other handyman operation types that provide less risky services usually pay less for coverage.

Location

When it comes to insurance premiums, location always plays a role. If you live and work in a crime-prone neighborhood, your insurance premiums always tend to be higher than your similar counterparts in a better neighborhood.

Insurance companies also have good historical data on claims and lawsuits in different states and cities. Some states and cities just tend to have a higher claim and lawsuit rates than others. And insurance companies will take this into consideration as they price your handyman insurance policy.

Coverages that you acquire and coverage limits

As you see from the cost table above, different coverages cost differently. Some coverage is a lot more expensive than others. For a handyman, workers comp insurance is particularly very expensive because a handyman can do a simple painting job, but can also do dangerous roofing and tree trimming work. The more coverage you need, the higher premiums you’ll pay. Even for the same coverage, higher coverage limits will result in higher premiums.

Business size and the number of employees

The bigger your business is and the more employees you have, the more expensive your handyman insurance premiums are. If you have more customers and do a wide variety of handyman work, that would increase your premiums as well.

For some coverages, you have to pay premiums per employee like workers comp insurance or commercial auto insurance, so the more employees you have, the more expensive your premiums are.

Your experience level

Insurance companies always prefer experienced businesses to new businesses. The more experience you have, the more knowledge you have in managing your business to avoid accidents. Insurance companies take this into consideration as they set the price for your policy. If you are new to the business, you are more likely to make mistakes: cause accidents, and get sued. Your premiums will be higher.

Your claim history

Last but not least, your business insurance claim history affects the insurance cost as well. Insurance companies always charge restaurants with a lot of claims in the past more than those without claims.

How can I find cheap handyman business insurance?

Here are some tips to help you get the coverage you need at a fair price:

Compare several quotes

Get quotes from a few companies and compare them to find the right coverage for you at a reasonable cost. Working with a broker like CoverWallet, InsurePro, or Simply Business is a good way to get several quotes more easily and conveniently. These brokers work with several insurance companies and they can pull quotes from these companies to show you at once. That would make it easier for you to compare several quotes and select the cheapest one for your restaurants.

Work with an experienced agent or broker

There are a lot of nuances in handyman insurance as you can see. Any small details in your handyman business operations can have a big impact on the cost of insurance. However much you can learn on your own, it will not be comparable to an agent or broker who does this for a living and has worked with hundreds, if not thousands, of handymen. Partner with an agent or a broker that you could trust so that they can advise you on the right coverages that you should have. They could also help you get several quotes to compare as well if you decide to work with a broker.

Emphasize safety in your operations

Insurance is always more expensive if you have claims and insurance companies give you a bad assessment of safety practices and standards. Emphasizing safety practices with both your employees and your customers, and requiring all of your employees to complete safety training and implement safe practices at the workplace will help reduce the number of accidents and claims in the future. Doing those may also decrease your current premiums since insurance companies’ underwriting engines may take these factors into consideration.

Ask for discounts

If they’re not offered to you when getting a quote, ask about them, whether you’re buying online or through an agent. Insurance companies often offer several discount programs that you can take advantage of. Even if you may not eligible for one or many of these programs today, you can still make changes in your operations so that you can be qualified to get these discounts in the future.

Taking these steps will help ensure you’re not paying too much for your handyman coverage.

What types of insurance are needed for a handyman business?

The primary type of insurance a handyman should secure is handyman liability coverage. This is a type of general liability insurance that will pay for damage to a client’s property or client injuries that are a result of the work you do. For example, general liability insurance pays if you accidentally flood a client’s basement and it results in damage or if a customer trips on an extension cord, is injured and sues you.

General liability insurance for handymen

General liability insurance protects you from being financially liable if you cause harm to a customer’s home or business location or if the customer gets injured while you’re providing services to them.

While many handymen are concerned about the cost of getting insurance, the truth is that they really can’t afford to be without it.

Ask yourself: Would you be able to pay to repair a client’s house if you cause significant damage to it or the legal and settlement costs if you’re sued by a client over harm to their property?

Typically, these expenses are large enough to put a handyman out of business. However, handyman liability insurance would pay them if any of these things ever happen to you.

What other types of insurance do handymen get?

While some people offering handyman services will only need a general liability policy, there are five other types of coverages worth considering.

- Commercial auto insurance

- Commercial property insurance

- Workers compensation insurance

- Tools & equipment insurance

- Professional liability insurance

Commercial auto insurance for handymen

If you drive a business-owned vehicle or a personal one for business reasons, you’ll need commercial auto insurance. A personal auto policy won’t cover damage or injuries that happen while conducting business. Commercial coverage for your car, truck, or van typically runs between $150 and $200 per month. It will help you rest assured knowing you won’t have to pay for vehicle damage or injury-related medical costs out of pocket if you’re involved in an accident while working.

>>MORE: Best Commercial Auto Insurance Companies

Commercial property insurance for handymen

Do you have a lot of inventory or tools, whether at home or in a separate business location? Then you should consider commercial property insurance. It will protect you from theft or property damage caused by fire, accidents or natural disasters, including things like your tools and equipment when they’re stored away on your property. If your items are damaged while at your home, your homeowners policy won’t cover them because you use them for business. You’ll need commercial property coverage.

>>MORE: Best Commercial Property Insurance Companies

Workers’ compensation insurance for handymen

If you have employees, workers’ compensation insurance is required in most states. It covers your employees (and you) if anyone is injured or becomes ill because of work-related reasons. It pays medical expenses, disability, and a portion of lost wages or funeral expenses if someone dies on the job. Having workers’ comp will protect you from certain lawsuits that injured employees could file against you.

Workers’ comp is likely not required for self-employed handymen with no employees. However, if you’re in this situation, you may want to get it because it provides a level of financial security if you become injured on the job and can’t work for a while.

>>MORE: Best Workers Comp Insurance Companies

>>MORE: Best Workers Comp Insurance Companies for Independent Contractors

Tools and equipment insurance for handymen

Handymen need their tools to get the job done. It can be devastating if something happens to them. The good news is that tools and equipment insurance can cover them if they’re damaged or stolen from a job site. Coverage is typically under $50 per month, depending on the types of tools and equipment covered. This could be a smart investment for most people working in the handyman trade.

Professional liability insurance for handymen

Professional liability coverage is also known as errors and omissions (E&O) insurance. It protects against claims of negligence while conducting business. If you ever provide a client with advice that isn’t correct or complete or perform a handyman service someone isn’t happy with, and they sue you, professional liability insurance would pay legal and settlement costs.

>>MORE: Best Professional Liability Insurance Companies

>>MORE: Best E&O Insurance Companies

Is handyman insurance required to operate a business?

If you answer YES to any of the following questions, you probably have to buy handyman general liability insurance:

- Does your state require insurance to conduct home repairs?

- Do you plan to work in apartment complexes that require proof of insurance before you can get started?

- Are you planning to work on bank-owned properties?

- Are you planning to get a contractor’s license?

- Do you do plumbing and electrical work?

- Do you have to wear a helmet when you work?

Even if you didn’t answer in the affirmative to any of these, it could still be worth getting general liability insurance to protect your livelihood.

How much coverage does a handyman insurance policy include?

A typical handyman liability insurance policy will come with the following coverage:

- $1 million liability coverage per claim

- $2 million per year aggregate coverage limit

- $1,000 deductible.

Here’s what this means: If you file a claim, the insurance will cover up to $1 million per incident, with a maximum of $2 million per year. You will have to pay $1,000 out of your own pocket with this deductible before your insurance coverage kicks in.

Top 5 insurers for handyman coverage

Here are our choices for the top companies that offer handyman insurance:

- CoverWallet: Best for comparing handyman insurance quotes online

- Progressive: The best for discounted handyman business insurance

- biBerk: Best for low-cost handyman coverage

- Next: Best online experience

- Hiscox: Best for handymen with unique insurance needs

CoverWallet: Best for comparing handyman insurance quotes online

CoverWallet is a digital broker. They work with several leading small business providers and are able to pull quotes from these companies for you to compare and select the best and the cheapest one. Their quote flow is simple and fast. Within 10 minutes, you are able to compare several quotes conveniently.

After buying a policy through CoverWallet, you will be able to manage all of your business insurance policies on their digital dashboard. The dashboard offers several useful features such as downloading the certificate of insurance, renewing a policy, and filing a claim.

CoverWallet earns an excellent consumer rating on BBB (A).

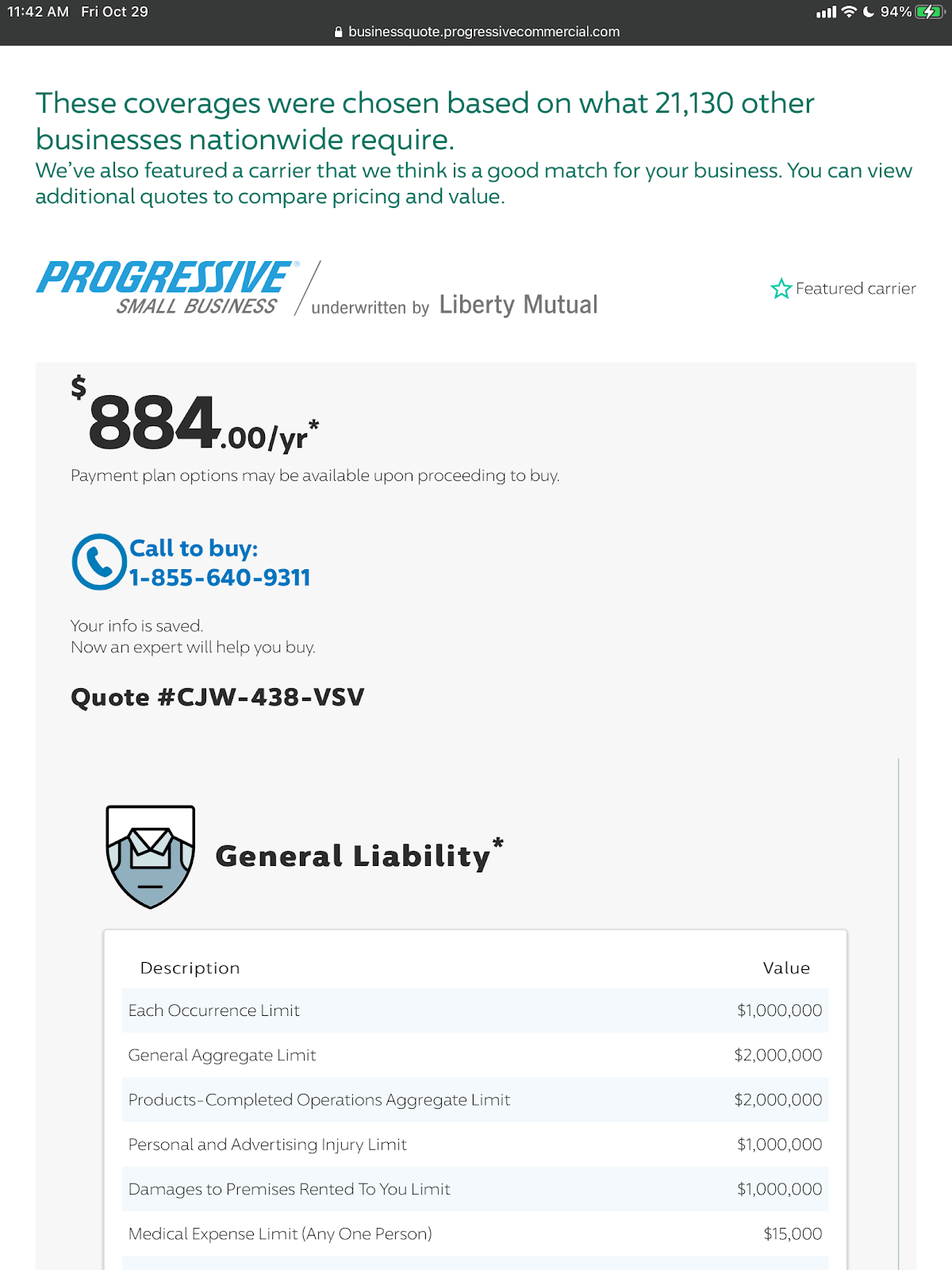

Progressive: The best for discounted handyman business insurance

Progressive may seem like a less-than-serious company because of its ongoing series of commercials featuring Flo. You might feel concerned about entrusting your handyman operation to the insurer.

The truth: It’s a reputable company that’s been in business since 1937. Progressive is known for its flexibility, great rates and highly responsive service.

Progressive is famous for its discounts, which could help you save on your handyman business insurance. You can earn discounts for things like:

- Purchasing multiple coverages

- Implementing safe work site practices

- Paying annually rather than in smaller increments

- Agreeing to autopay.

It’s easy to get a handyman quote online from Progressive. It should take you less than five minutes. Here’s an example of a handyman insurance quote from Progressive.

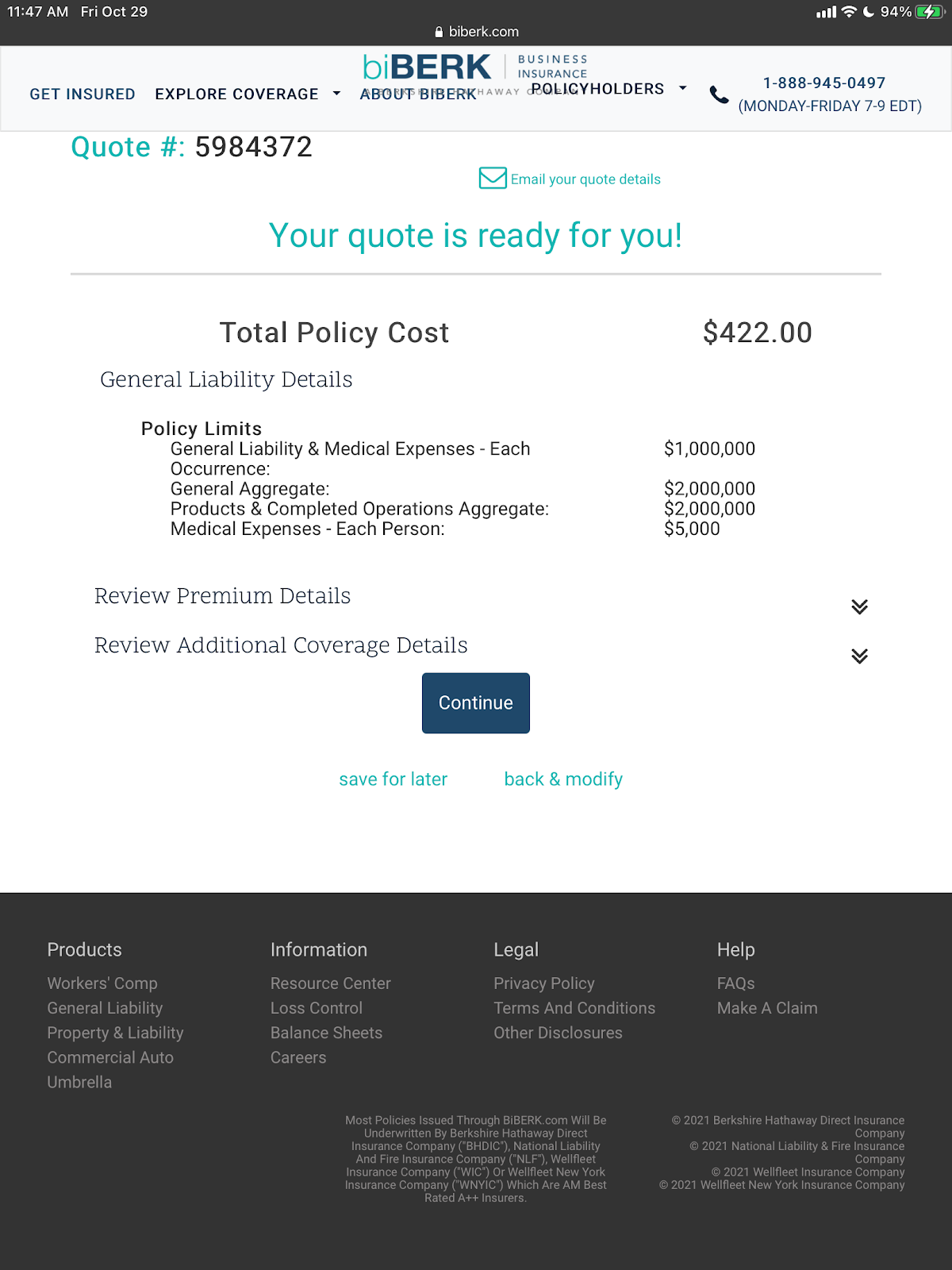

biBerk: Best for low-cost handyman coverage

biBerk is a low-cost business insurance provider. Despite saving money on your handyman insurance, you can rest assured knowing you’re still getting quality protection for your business. biBERK is able to lower insurance costs by almost 20 percent because it insures small businesses directly, without the added costs of having to work through a middleman or insurance broker.

You can feel confident knowing biBerk is a part of Berkshire Hathaway, a company headed by well-known investor Warren Buffett. It’s a firm that has millions of satisfied customers that’s been insuring people and businesses for more than 75 years.

Here is a handyman insurance quote from biBerk.

Next: Best online experience

Next is changing how businesses purchase handyman insurance and other coverage.

Their operation is focused on delivering the ultimate online insurance experience. Because of this, you’re able to purchase a policy, file a claim or get a certificate of insurance any place, any time, 365 days a year. This is particularly important for a handyman that can only work with a client if they can show proof of insurance. Even though Next is an online insurer, you can get expert help over the phone when you need it. The firm is also known for being able to make most claims decisions within 48 hours.

Even though Next is a relatively new and innovative company, you can rest assured knowing it has an excellent rating from A.M. Best, an insurance company rating agency. All the company’s policies are backed by MunichRe, an established insurance company and reinsurer. More than 10,000 business owners have turned to Next for their insurance needs. The firm has earned a solid 4.7 customer rating.

Here is a sample handyman quote from Next.

Hiscox: Best for handymen with unique insurance needs

Hiscox offers specialized insurance coverage for handymen.

It’s easy to buy business insurance for handymen from Hiscox online. A rep can also help you customize your coverage to meet your unique business needs.

If you choose Hiscox for your business coverage, you can rest assured knowing you’re entrusting your protection needs to a firm that’s been in operation for 120 years. It exclusively offers insurance for small businesses and more than 400,000 smaller companies and individuals trust Hiscox for their insurance needs.

Hiscox is known for tailoring unique insurance solutions to the individual requirements of small businesses and sole proprietors. The company offers top tier service, provides fast quotes, instant coverage and quick claims processing.