Mentioning the Sunshine State, many people think of beaches, palm trees, and alligators. But Florida is also a large and diverse state, with different regions offering different types of lifestyles and costs of living. The northern part of the state is mostly rural, while the southern part is more urban and expensive.

Florida general liability insurance is a necessary expense for any business or individual operating in the state. The cost of general liability insurance varies depending on the region, with policies costing more in Miami and Orlando than in rural areas. However, even in the most expensive areas, policies are relatively affordable when compared to other states. For example, a business in Miami could expect to pay around $2,000 per year for general liability coverage, while a business in New York City could expect to pay over $10,000.

The cost of coverage can vary depending on the size and nature of your business, but it is important to have some protection against potential lawsuits. A good Florida general liability policy will safeguard your assets in the event that you are sued for damages or injuries that occur as a result of your business operations.

- How much does general liability insurance cost in Florida?

- What factors affect the general liability insurance cost in Florida?

- How to find cheap general liability insurance in Florida?

- Which businesses need general liability insurance in Florida?

- How to buy general liability insurance online in Florida

- General liability insurance requirements in Florida

- What does general liability insurance cover?

How much does general liability insurance cost in Florida?

The average cost of a $1M/$3M general liability insurance policy in Florida is $38 per month, or $456 per year. Most small businesses in Florida pay between $250 to $5,000 per year for their general liability coverage. It is a wide range since general liability insurance cost varies significantly from one company to another depending on several factors, which we are discussing in the detail below.

Different insurance companies will give you different quotes since they have different underwriting criteria. Be sure to shop around with a few companies or with a digital broker to compare several quotes to select the best and cheapest one for your company. Getting online quotes is an easy way to compare them, we recommend the following:

- NEXT: the best digital carrier with affordable rates

- Simply Business: the best broker to get and compare several quotes in one place

- Smart Financial: the best broker if you prefer working with experienced agents

What factors affect the general liability insurance cost in Florida?

The cost of general liability insurance is determined by your specific business requirements. Your company is one-of-a-kind, and so are the risks. Cost is influenced by several factors, including:

Industry of your business

The type of industry where you work and the types of risks associated with the industry will primarily affect the cost of your premium. Companies that work in risky industries will have to pay more compared with those that work in industries with less risk. For instance, an accounting service firm might not have to pay as much as a contracting or construction business because accounting service firm has a much lower risk profile than contracting or construction business.

Location of your business

If your business is located in the south of Florida, you will pay more than those in the northern part of Florida. That is because large cities have more people, and there are more chances that issues will happen there. Similarly, if you work in a city where the claims rate is higher based on historical data, you will pay more.

The number of employees

The more employees you have, the more the chance of making mistakes that can cause problems for your client. So, companies that have more employees will likely pay more for their general liability insurance.

The number of locations

The more locations your business has and the bigger the location is, the more likely you’ll have customer injuries in your business’s locations, which could result in more lawsuits.

The number of customers and revenue

The more customers you have, the more revenue your business generates, the more likely your customers get injured at your business locations or their property is damaged due to your business operations, and the more likely they will sue. All of these lead to a higher rate for your general liability insurance.

Your policy’s coverage limits

A higher limit means you are getting better coverage. The maximum amount the insurer will pay you if an incident occurs. However, the higher your limits, the higher your premium. A typical general liability insurance policy in Florida has $1M/$2M or a smaller one of $100K/$300K

Your policy’s deductibles

Your deductible is the amount you will pay from your pocket when the incident occurs—the higher your deductible, the lower the cost of your premium. But then, a higher deductible means you way pay more if an incident occurs.

Years of experience in business

New companies tend to pay more for general liability than giant corporations.

Your business’s claim history

Prior general liability claims are a major red flag for insurers. It tells the insurer that you are a risky business owner. As such, you will pay more to get their protection.

How to find cheap general liability insurance in Florida?

The following are ways to get affordable general liability insurance in Florida.

Compare several rates to find the best deal.

The only way to find the best and cheapest quote for your contracting business is to shop around and compare several quotes.

The mistake most people make is to do that once and stop. Even after getting the best bargain, you still need to find another one. Insurance companies frequently change their rates. So, when it comes time to renew, make sure you shop around again to find the best deal for your company.

We recommend getting and comparing quotes online from NEXT, Simply Business, InsurePro, and Smart Financial. They all offer fast quotes online, which shouldn’t take you more than 10 minutes. Simply Business is the best if you want to compare to find the cheapest quotes for your business.

Take advantage of special offers

Insurers always have offers for their clients. If they don’t mention it to you, you need to ask. Whether you’re buying online or through an agent, there is always some discount.

Good insurance companies always have a list of discounts on their websites where you can check if you qualify. Make sure you take advantage of any of those discounts available to your company.

Bundle the policies

Bundling several business insurance policies can also help you get discounts. Whenever you can, try to obtain your policies from the same place to obtain bundle discounts and save money on premiums.

Implement safety practices and standards

General liability insurance cost is correlated with the likelihood of having customers getting injured and property damages and sue your business. Implementing different safety practices at your locations and for your employees can potentially reduce the number of “accidents” happening to your customers. Many insurance companies also offer discounts based on the safety practices that you implement.

Learn more at the cheapest general liability insurance companies

Which businesses need general liability insurance in Florida?

The best way to protect your company is to have it correctly insured. General liability is best suited for businesses that have the following characteristics.

- You rent/ lease properties

- Your customers are at your business locations

- You have to meet your clients either at your worksite or in their homes.

Listed below are a few examples of businesses that may fit the bill:

- Artisan contractors

- Consulting

- IT contractors

- Janitorial services – Learn more about cleaning business insurance

- Landscaping companies – Learn more about landscaping insurance

- Plumbing contractors – Learn more about plumbing insurance

- Marketing

- Real estate agents

- Restaurants – Learn more about general liability insurance for restaurants

- Schools or offices

- Hair salons – Learn more about hair salon insurance and hairdresser insurance

- Nail salons – Learn more about nail salon insurance

- Beauty salons – Learn more about beauty salon insurance

Each business is unique, so make sure you inquire if the policy is right for your business.

How to buy general liability insurance online in Florida

You have several options to purchase general liability insurance in California for your business. To make things easier, the options are divided into three broad categories as follows:

Digital brokers in Florida

Digital brokers work like insuretech companies. However, they have more experience. These companies do not have their policies; instead, they assist businesses in connecting with their insurers so that they can purchase the policies of their choice. If you have never purchased a policy before, this is probably a good place to start.

Examples you can use include:

- Simply Business

- Smart Financial

- CoverWallet

- Tivly

- InsurePro

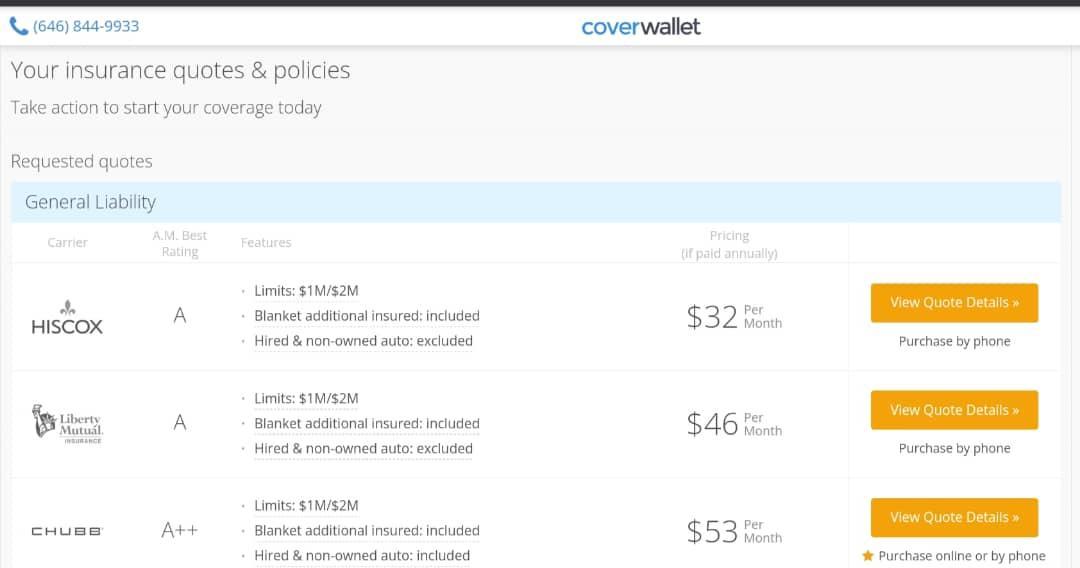

Here is a sample quote for an accounting firm with 2 full-time employees obtained from CoverWallet.

Pros

- Fast online quotes, in most cases

- Companies that have issues finding policies may find something here.

Cons

- They only offer policies from their partners

- You have to file a claim directly with the carrier.

Learn more at the best general liability insurance companies in Florida

Traditional insurance companies

As the name suggests, companies in this category are those that come to mind when people think of insurance. The majority of them have the experience and financial stability to provide you with superior coverage options. They cover the majority of businesses, including those in the riskiest industries like construction.

Examples of companies in this category include:

- Chubb

- Hiscox

- Liberty Mutual

- The Hartford

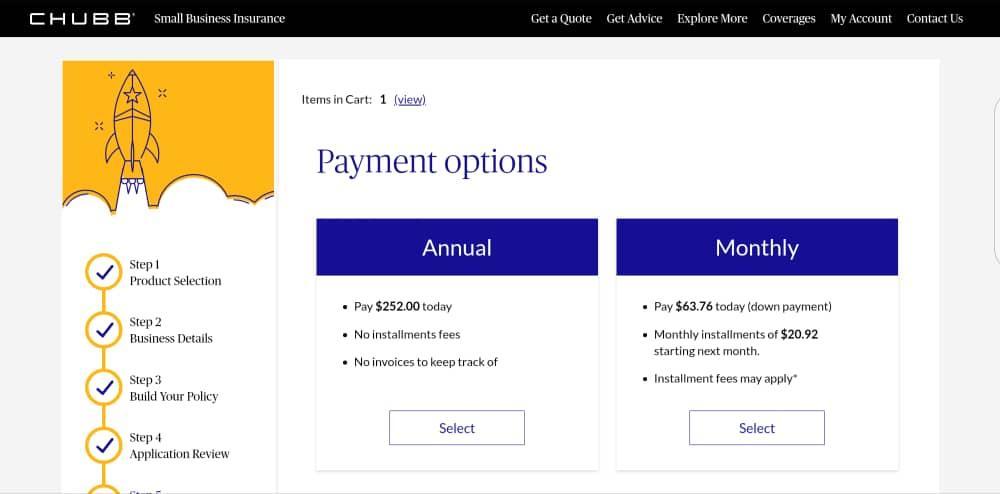

The following picture is a sample quote for an IT consulting firm with 2 full-time employees obtained from Chubb insurance.

Pros

- You get reliable coverage for almost any industry.

- Most of them have extensive experience to give you the best coverage.

- They have other policies that you can buy and bundle for discounts

Cons

- The policies from these companies might be expensive

- These companies don’t usually ofer quotes online. You are more likely to work with their agents

Learn more at how and where to get and compare general liability insurance quotes

Insuretech companies

These businesses are new to the industry. These are tech companies that aim to make insurance affordable and straightforward. They assist businesses in locating the most appropriate and cost-effective quotes for their operations online. They do this using the latest technology tools like artificial intelligence.

Pros

- Fast quotes that take less than 10 minutes

- All operations are done online via the internet

- Easy to use platforms.

Cons

- These companies do not offer policies for risky industries like construction.

Examples include:

- NEXT

- Thimble

- Embroker

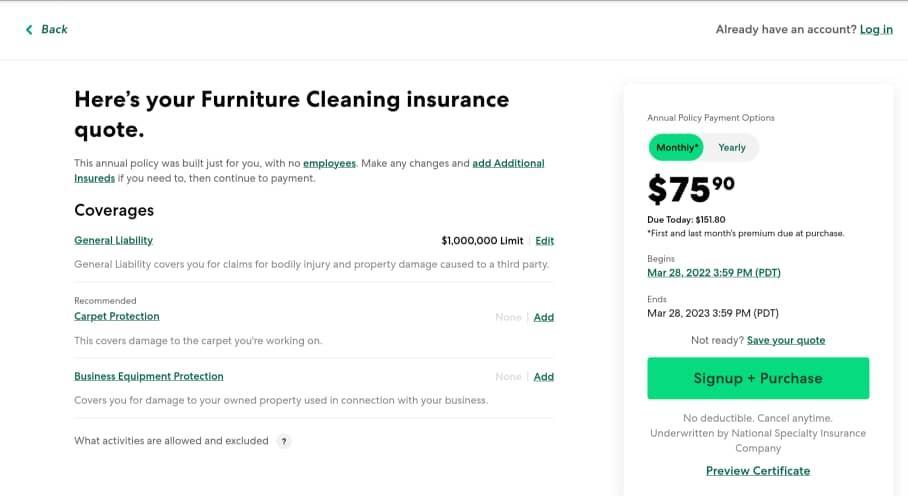

Here is a sample quote for a cleaning firm with 2 full-time employees from Thimble

Learn more about buying cheap general liability insurance online

General liability insurance requirements in Florida

General liability is not compulsory for businesses in Florida. However, it is an intelligent decision to have the policy. General liability insurance protects small businesses against the most common lawsuit, which is slips and falls. A lawsuit usually costs more than $100K, which bankrupts a small business easily.

In fact, many large companies in Florida do not enter business agreements with vendors before they are sure the vendors have general liability insurance coverage.

Nobody wants to do business with a company that will go out of business unexpectedly due to a liability lawsuit (it happens, and it’s not pretty). Carrying this policy shows that you are responsible enough to do business with. It shows that your business is prepared to face almost any risk that comes its way.

What does general liability insurance cover?

General liability insurance (GL), also known as business liability insurance, is coverage that can protect you from a variety of claims arising from your business operations,

These claims include the following:

Bodily injury

General liability insurance protects against business-related incidents that cause bodily harm to a third party. For instance, if one of your employees mistakenly drops on hammer on someone’s foot, this coverage should cover any damages. This coverage, however, only does not apply to employee injuries.

Property damage

General liability can also protect you from any third-party property damage caused by your business operations. For example, imagine you break a client’s window while cleaning their apartment; this policy should cover the damages.

Product liability

General liability insurance protects against liability for faulty products. Products are any goods that your company manufactures, sells, or distributes. This coverage protects a business if such a product causes physical injury or illness. For instance, if your customer becomes sick after buying infected food from you.

Completed operations liability

Completed operations coverage is just like product liability. It, however, protects you against faulty services or work performed by your business. For coverage to apply, you must finish such a project.

For example, a customer hires your service clean their bathroom. However, you forget to turn off a tap in the bathroom, causing the bathroom to flood after you left. Your general liability may cover the damages caused since you already left when the issue happened.

Personal and advertising injury

Your general liability policy may also cover any written or verbal communications that cause harm to a third party. This includes, among other things, libel, slander, malicious mischief, and copyright infringement.

For example, if your local competitor accused you of spreading rumors about their poor customer service. The company can sue you for personal and advertising injury if the competitor’s reputation and profitability are harmed. In such a case, general liability will cover you.

Damages to rented property.

Damage to land, buildings, or structures you rent or lease is also typically covered under general liability coverage. For coverage to apply, the insured or their business must be legally liable for the damages.

For example, a local baker may rent a property that catches fire due to a careless employee leaving the oven unattended. General liability may cover the damages because the business operations caused the fire. On the other hand, this coverage would not apply if a lightning strike started the fire.

Learn more about general liability insurance coverage

What does general liability insurance not cover?

Your general liability will not protect you from all business-related risks. To cover some risks, you may require additional insurance coverage not covered by general liability insurance. There are numerous other products available to protect your company. Here’s a quick rundown:

- Damages to commercial vehicles – A commercial auto policy protects vehicles used for business. A personal auto policy will also not cover incidents at work. Learn more at the best commercial auto insurance companies

- Employee injuries – most states require coverage for your employees only through workers’ compensation insurance. Learn more at the best workers comp insurance companies.

- Owned commercial property – this is covered under a business owner’s policy (BOP), along with other equipment and goods. Learn more at the best commercial property insurance companies.

Professional blunders – If your company offers a service or advice, you should look into professional liability insurance. Learn more at the best professional liability insurance companies.

General liability insurance vs. product liability insurance

Some businesses will need both general liability and product liability insurance policies. General liability policies protect businesses from claims of negligence, while product liability policies protect businesses from claims that a product caused injury or damage. There are some similarities between the two types of policies, but there are also some key differences.

One similarity is that both types of policies typically cover legal defense costs. This means that the insurance company will pay for a lawyer to defend the business if it is sued. Another similarity is that both types of policies usually provide financial compensation to victims if the business is found liable for damages.

The key difference between general liability and product liability insurance is that general liability policies typically cover any type of injury or damage, while product liability policies only cover injuries or damages that are caused by a defective product. For this reason, businesses that manufacture or sell products should have a product liability policy in addition to their general liability policy.

We should note that some insurance companies include their product liability coverage in their general liability policy. However this policy may not be available to manufacturers and retailers since these business types would need a more robust standalone product liability policy.

General liability insurance vs. Business Owners Policy (BOP)

Business Owners Policy (BOP) is a type of commercial insurance that combines property and liability coverage into one policy. It is different from general liability insurance in that it provides broader coverage for business-related risks. For example, BOP would typically cover damage to your business property caused by a fire, as well as any injuries or damages sustained by third parties as a result of your business operations.

It is often advised that any small business with less than 100 employees and $10M in revenue should have a BOP instead of buying general liability insurance and commercial property policies separately. This will help save money for the small business.

General liability insurance vs. workers comp insurance

Workers’ compensation insurance is designed to protect employees who are injured or become ill as a result of their job. It provides benefits to employees for medical expenses and lost wages, regardless of who is at fault for the injury. In most states, workers’ compensation insurance is mandatory for employers. If you hire the first full-time. or part-time employees, you will need to buy workers comp insurance policy, otherwise, your company can be fined and its operations can be suspended.

General liability insurance, on the other hand, covers accidents and injuries that occur to people not employed by the business. This policy also provides coverage for property damage caused by the business. It is important to note that general liability insurance does not usually provide benefits for medical expenses or lost wages.

Small businesses should consider purchasing general liability insurance to protect themselves from potential lawsuits. The policy can be tailored to meet the specific needs of the business, and it is typically less expensive than workers’ compensation insurance.

General liability insurance vs. professional liability insurance

Professional liability insurance protects businesses from claims of negligence or malpractice. This type of policy is different from general liability insurance, which covers a business from claims of bodily injury or property damage. Most small businesses should have a general liability insurance policy to protect them from common risks, but professional liability insurance may be a good option for businesses that offer services such as consulting, accounting, or engineering. Many other professionals such as doctors, nurses, lawyers, real estate agents, insurance agents, CPAs, financial advisors, and tax preparers will need professional liability insurance coverage too.