General liability insurance is probably the most popular policy for small businesses. Nowadays, most small business owners manage part of their businesses online, especially the financial and insurance services. That’s the reason why small business owners may prefer to buy business insurance online as well. Buying general liability insurance online is convenient, fast, and cheap.

- Where to buy general liability insurance online

- Where can you get general liability insurance quotes online

- How to get general liability insurance quotes online

- Types of businesses that find it easy to buy general liability insurance online

- Types of businesses that find it difficult to buy general liability insurance online

- The steps to buying general liability insurance online

- Buying a policy online, getting a certificate of insurance online

- Managing your general liability insurance policy online

Where to buy general liability insurance online

You have options when it comes to buying any type of business insurance online. Buying general liability insurance online is probably the easiest kind of insurance to buy online because it’s a general policy that every small business needs. Therefore, almost every insurance company sells it.

Any insurance company that sells business insurance will sell general liability insurance. You can get a Business Owner’s Policy (BOP) instead, which is general liability insurance coupled with commercial property insurance. Sometimes they include business interruption insurance or cyber insurance.

You have three main options to buy general liability insurance online: digital brokers; traditional insurance companies; and insuretechs.

Digital brokers:

Digital brokers such as CoverWallet, Policy Sweet, and commercialinsurance.net, partner with insurance companies to bring you online quotes from several of them, making it easy to comparison shop.

Pros of buying general liability insurance online from a digital broker

- Gives multiple quotes when you fill out one form

- Makes comparison shopping easy

- Manage your policy online as well

- Can get quotes from multiple types of insurance and can manage your policies in the same “wallet”.

Cons of buying general liability insurance online from a digital broker

- Digital brokers don’t underwrite their own insurance

- Most of these companies are less than ten years old

- Quotes are not always instant

Traditional insurance companies:

Companies such as The Hartford, Liberty Mutual, Hiscox, Chubb, and Progressive have decades, sometimes centuries, worth of experience. There’s nothing they haven’t seen or covered.

Pros of buying general liability insurance online from traditional insurance companies

- A wealth of experience to draw on

- Discounts may be available

- Easy to bundle your policy with other policies you need

- Likely to have a depth and breadth of options and flexible coverage

Cons of buying general liability insurance online from traditional insurance companies

- Some will work only through agents

- Brick-and-mortar businesses have higher overhead, and consequently, often higher prices

Insurtech companies:

Insurtech companies streamline the process of insurance by using artificial intelligence (AI) to predict risk. They operate entirely online.

Pros of buying general liability insurance online from insuretechs:

- Using AI makes providing quotes easy and often instant

- The whole process can take place online

- Saves time and money

Cons of buying general liability insurance online from insuretechs:

- Most of these companies are less than ten years old

- May not have the resources to pay big claims

- Some may have limited insurance offerings, making it difficult to bundle

Learn more at the best general liability insurance companies

Where can you get general liability insurance quotes online

More companies are offering general liability insurance quotes online. That makes it easy for small businesses to compare quotes and buy a policy online. Below is the list of companies that we know offering quotes online for your consideration:

| Types of companies | Companies that offer general liability insurance quotes online |

| Digital brokers | CoverWallet, CoverHound, Simply Business, Huckleberry, and Embroker |

| Traditional insurance companies | The Hartford, Hiscox, Liberty Mutual, Progressive, Nationwide |

| Insuretechs | NEXT and Thimble, |

How to get general liability insurance quotes online

Wander over to your top choices and hit the button that says, “Get a Quote.” Then you’ll have to answer some questions.

Information you’ll need to get a quote

We chose Next to get a quote from. This is the information they required:

- Type of work you do

- State

- Email address (just in case they can’t give you an instant quote, and also to follow up with you

- Other types of insurance you might be interested in (so you can get a bundled quote)

- First name

- Last name

- Phone number

- Business name

- Business address

- Structure of your business (individual/sole proprietorship; partnership; limited liability company (LLC); Corporation; Trust; Other)

- What year did you start your business?

- Number of owners

- Number of employees (do not include owners or subcontractors)

- Expected subcontractor cost in the next 12 months

- Expected payroll in the next 12 months (not including the owners)

- Expected total sales

- Has your commercial insurance ever been canceled, revoked, or not renewed in the last three years?

- Has your business or any of its owners been convicted of a felony, declared bankruptcy, or had business-related lawsuits filed against them?

- Have you filed any insurance claims in the last three years?

After you answer all of these questions, you will have to check boxes indicating you understand what the policy covers and does not cover. Then there is a list of exclusions to the policy. Lastly, you’ll choose when you want your coverage to start.

This was the quote we got from Next for an accounting firm with four employees and $400,000 in revenue:

What types of businesses need general liability coverage?

Because general liability insurance is so…well, general, that almost every small business needs it.

Types of businesses that find it easy to buy general liability insurance online

- Accounting

- Consulting

- IT

Businesses such as IT, computer networking, or consulting will find it easy to get quotes online for general liability insurance. For one thing, the risk that someone will fall down and hurt themselves while going to their accountant is pretty remote (although possible).

Types of businesses that find it difficult to buy general liability insurance online

- High-risk businesses such as construction, trucking, roofing, etc.

- Businesses that vary tremendously, such as restaurants

Since restaurants can mean anything from a taco truck to a full-scale elegant restaurant, the process to get a quote is more detailed. That doesn’t mean you can’t get a quote, however: you just may have to fill out more information.

If you’re a contractor or another high-risk occupation, there will be many questions about the services your business does and does not provide, plus a declarations page about what isn’t covered.

Learn more at the following articles:

- the best general liability insurance for contractors;

- the best general liability insurance for constructions companies; and

- the best general liability insurance companies for handyman

The steps to buying general liability insurance online

If you google “General liability insurance” google will return companies that can sell you a policy. For example, when we googled general liability insurance, these companies were the top ranking:

- Next

- Hiscox

- biBERK

- Progressive

Choose the top companies that appeal to you and get a quote. Some traditional insurance companies will not offer online quotes, so you’ll have to call them to get a quote. This could be good or bad. If you speak to an agent who knows more about business insurance that you do, they could steer you in the right direction and make recommendations. On the other hand, agents work on commission, so expect a sales pitch.

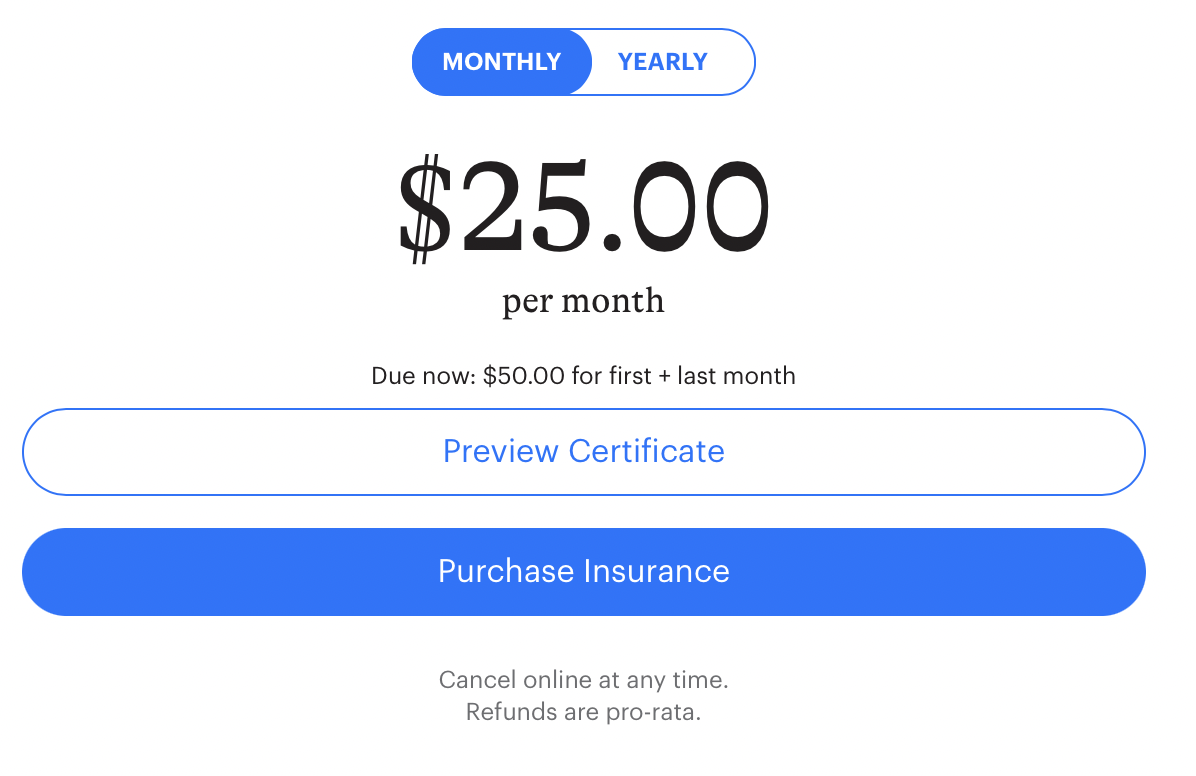

Buying a policy online, getting a certificate of insurance online

If you have decided to go with an insurtech company or a digital broker, you can just click where it says, “Purchase insurance” and then you can pay with a credit or debit card. If you have found a traditional insurance company you like, you may or may not be able to purchase the policy online. Some will have you call to buy the insurance.

Likewise, insurtech companies and digital brokers can usually supply a certificate of insurance as soon as your payment goes through. With a traditional insurance company, you might have to wait a few days.

Managing your general liability insurance policy online

Most insurtech and digital brokers allow you to manage your policy online. This lets you:

- Pay your bill

- Register for eDocuments (coverage selection, declarations page, etc.)

- Get Proof of insurance

- Register for EFT (Electronic funds transfer, so your payment comes out of your bank account on the same day each month)

- File a claim

- View and update policy information

- Make changes to your policy (increase or decrease limits, raise or lower deductible, buy additional policies, etc.

Traditional insurance companies may vary in what they offer online: some are very up-to-the-minute, and some are more dated. Be sure to ask about this before you purchase a policy.

How much does general liability insurance cost?

The average cost of general liability insurance for a small business is $1,200 a year. Most small businesses pay between $300 to $5,000 a year for a general liability insurance policy.

These are just the average. Different small businesses will pay different amounts for their general liability insurance policy. Be sure to shop around with a few companies or with digital broker to compare several quotes online to choose the cheapest one for your business.

What factors affect the general liability insurance cost?

There are many factors that affect how much you’ll pay for your general liability insurance coverage. Some of them include:

Amount of coverage

Higher amounts of coverage are obviously more expensive and you will have to pay more. Lower coverage will result in lower premiums. However, lower coverage might not be enough to cover all expenses when you are sued, so be sure to select the right coverage limit for the policy. Small businesses usually have $1M/$2M coverage for their general liability insurance coverage.

Deductibles

The higher the policy’s deductibles are, the lower the premiums are. However, you need to be mindful selecting the right deductible amount that your business can afford when it needs to.

Type of business

Higher risk industries pay more for insurance. If you’re a contractor, for example, there is a lot of potential for clients, customers, and passersby to trip over something and injure themselves. If you’re a locksmith, the risk is much lower. In general, construction, contracting, and trucking businesses are paying the most while accounting or IT services are paying the least for general liability insurance policy.

How many years of experience you have in this industry

The more experience you have in your current industry, the less likely you will have lawsuits since you have accumulated sufficient experience to do the right things and follow the right process to avoid lawsuits.

How many years you’ve been in business

The longer you have been in business, the less likely that you’ll have lawsuits since you have learned how to manage your business the right way and have established the right safety practices for your business to avoid accidents and lawsuits.

How big your business is

General liability insurance is most commonly known to protect against slip-and-fall accidents by your customers. The more customers equal more opportunities for one of them to injure themselves. The more storefront your business has, the more likely accidents happen.

Location

If you’re reading this, your location is Texas, but some cities in Texas will have higher rates than more suburban or rural locations. Business locations in populated cities are smaller and more crowded with customers, which will be likely to cause accidents.

Claims history

If you’ve had claims before, your rates will be higher. If you have a clean record, no claims, your rate will be lower.

What is general liability insurance?

General liability insurance is a very basic type of business insurance. It protects you from lawsuits that frequently come up during the normal course of business. If you don’t have general liability insurance, you would have to come up with the money yourself.

For the most part, general liability insurance isn’t required by law. However, if you are a contractor or a developer, some states do require it to obtain a license. Also, many, if not most clients, will want a contractor to have general liability insurance because of the risks. They will ask to see your certificate of insurance before work begins.

What does general liability insurance cover?

General liability insurance covers:

- Third-party bodily injury

- Third-party property damage

- Personal and advertising injury

Third-party bodily injury

This coverage refers to injuries suffered by clients, vendors, or customers. For example, if you own a small grocery store and one of your customers trips on a grape and breaks an ankle, general liability will cover that customer’s medical costs. If, however, one of your employees injures themselves, general liability insurance won’t help you: you need workers compensation insurance for that.

Third-party property damage

This covers you for damage to someone else’s property caused by your business or employees. If you damage your own property, that’s not covered: that would be covered under commercial property insurance.

Advertising injury

This means if you say something against a rival in public, general liability will cover you. Now that everyone uses social media, the opportunities to be sued for slander have multiplied exponentially. You can even purchase a separate policy for social media liability. Alternatively, you can get general liability insurance and an umbrella policy for additional protection.

What doesn’t it cover?

In addition to the above-mentioned scenarios, there are some things that general liability insurance won’t cover.

- Vandalism (commercial property insurance covers this)

- Operations limitations: high-risk businesses, such as contractors or construction, often have this clause in their contract. It limits your general liability insurance to very specific circumstances. If you are a general contractor, you should read this part of your policy very carefully.

- Contractor and subcontractor exclusions: similar to the above, but specific to contractors.

- Pollution liability: if your business creates environmental hazards, you need pollution liability insurance.

- False advertising: if you claim you have product A, but you don’t: you have product B, which is similar but more expensive, that’s false advertising and general liability insurance doesn’t cover that.

- Product recalls

- Data breaches

- Intentional damage by you or your employees

Last thoughts

And that’s it! Hopefully, we’ve told you everything you need to know about buying general liability insurance online. If we’ve missed something and you have questions, feel free to reach out to us.