Owners and operators of food businesses often divide their time between managerial duties, cost analyses, and routine maintenance. With so much to do and manage, it’s difficult to foresee, prepare for, and prevent accidents from happening.

Even if you have a firm knowledge of the ins and outs of running and marketing a successful food business, several variables outside your control can still hinder your efforts. This is where food business insurance comes in.

In the event of lawsuits, employee injuries, or other potential liabilities, food business insurance can help cover repair or replacement costs.

In this article, we’ll look at the cost of the food business insurance market, the many policies and coverage options available to you, and their associated prices.

- How much does food business insurance cost?

- Food business insurance quotes

- What factors affect the cost of food business insurance?

- How to find cheap food business insurance?

How much does food business insurance cost?

Usually, each food business is unique and will require different policies. However, in most cases, general liability and commercial property insurance are the two most common types of food business insurance plans.

The average cost of food business insurance is $48 per month, or $576 per year. This is for a general liability insurance policy only. It is also the most important insurance policy for food businesses. If you add product liability coverage, the average cost will be around $64 per month, or $768 per year.

This is just the average cost. Your rates will be different. Be sure to shop around with a few companies or work with a digital broker to get and compare several quotes to find the cheapest one for your food business. We recommend the following:

- Simply Business: Best brokerage firm to get and compare several quotes to find the cheapest one

- NEXT: Best carrier offering a great digital experience and very affordable rates

- CoverWallet: Best brokerage firm if you want to get several quotes from top-tier carriers

To understand the policies you need for your food business, you must understand the risks associated with your business. By understanding these risks, you can carefully select the right kind of insurance policy that can mitigate these risks.

The following are the most common types of food business insurance policies and their relative cost:

General liability insurance cost for food businesses

A food business general liability coverage can shield your business from legal actions for food poisoning, cross-contamination, or other food-related incidents.

The policy may also offer protection from claims of slander, libel, or other general negligence on the part of your staff. General liability aids in covering damages due to customers’ medical costs and expenses.

For their general liability insurance, food companies pay an average premium of about $48 per month, which comes to about $520 per year.

Commercial property insurance cost for food businesses

In case of a fire, flood, electrical problem, or severe weather, your food business property, and equipment may be replaced or repaired thanks to the commercial property insurance coverage.

The average cost of a commercial property insurance policy for food businesses is $116 per month.

Business Owner’s Policy (BOP) cost for food businesses

Many business owners of eating establishments choose a Business Owner’s Policy (BOP) which is often a cheaper alternative. This policy combines general liability and commercial property insurance into one policy at a discounted rate.

Companies in the food and beverage industry pay an average premium of $137 per month, or $1,612 per year, for business owners’ policies.

The cost of a Business Owner’s Policy will, however, depend on several aspects, including the value of the property insured, the location of your food business, the kind of kitchen appliances utilized, and so on.

Worker’s compensation insurance cost for food businesses

Worker’s compensation insurance provides the needed financial assistance to cover medical bills, partial wages, and other related costs for employees that are injured on the job. Worker’s comp is considered compulsory in most states of the United States. Your business should have this policy if you plan to employ at least one employee.

Even if you are a solo business owner, getting workers comp is a good idea. Your health insurance company may reject your claim if you sustain an injury on the job, leaving you responsible for paying for costly medical care out of pocket.

The policy’s price tag varies depending on factors like the total number of workers you have, where your food business is located, and what kind of cuisine you serve.

The average cost of a policy is $1,524 per year, or $152 per month, with the cost ranging from $600 to $10,000 annually. It’s possible that your insurer charges more to insure your eatery if there is evidence of many past injuries among your staff.

Liquor liability insurance cost for food businesses

If you sell alcoholic beverages as part of your food business, you should consider getting liquor liability insurance. This policy protects you if the inebriated customers you serve alcohol hurt themselves or others or damage your property.

Liquor liability is usually required in most states with dram shop laws. In such states, establishments like restaurants and stores that sell alcoholic beverages must carry this insurance. However, insurance coverage standards usually differ from state to state.

Most policies for liquor liability insurance cost between $310 and $3,120 per year, with the average cost being $640 (or $54 per month).

Commercial auto insurance cost for food businesses

This policy protects your business against financial losses incurred as a result of vehicle-related incidents. These incidents include bodily injuries and property damage to third parties caused by collisions involving your commercial vehicle.

This policy is important as your personal auto policy will not cover your vehicle if you use it for business purposes. Even if the vehicle is registered in your name, your insurer might argue that a personal policy does not cover business operations.

The average cost of commercial motor insurance for food and beverage companies is $165 per month or $1,960 per year.

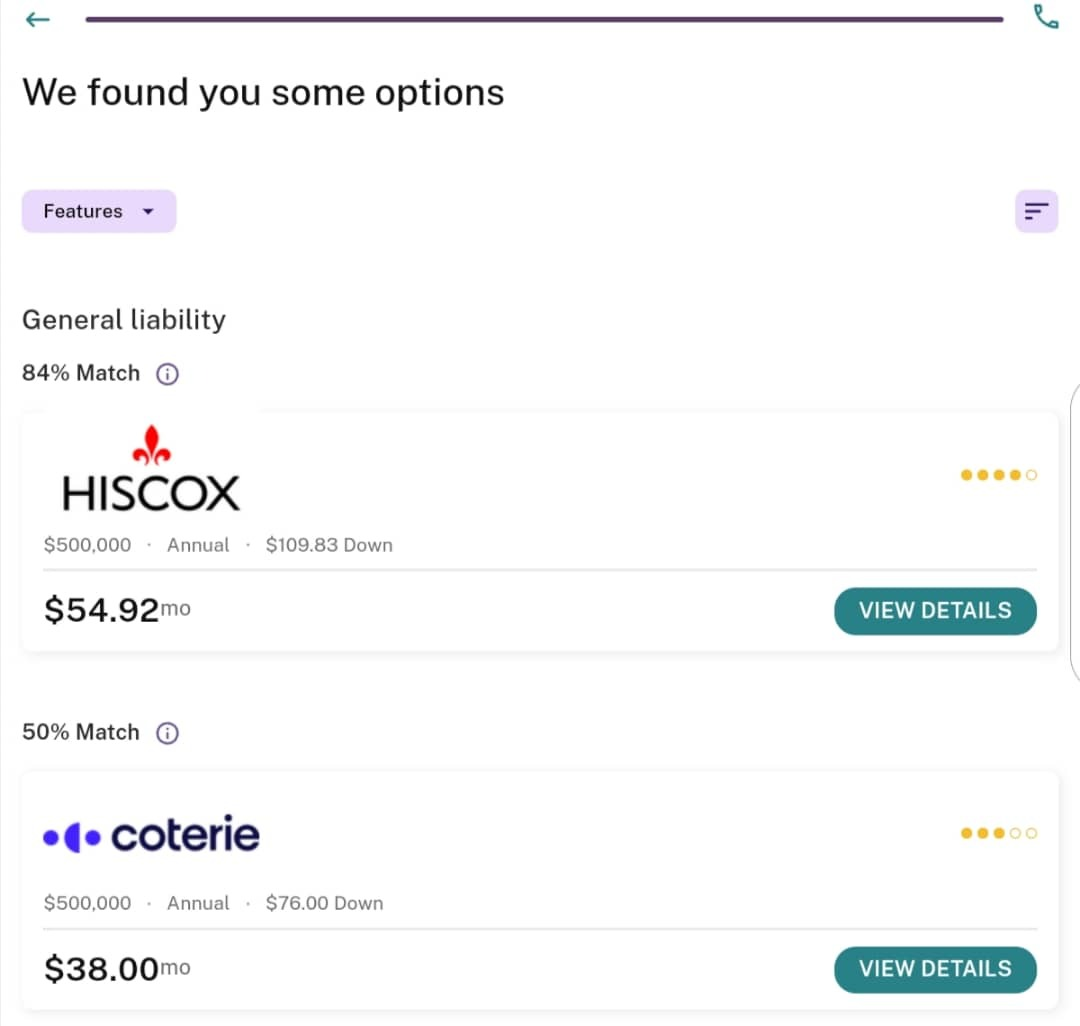

Food business insurance quotes

To illustrate how easy it is to get several quotes from different providers, we have gone ahead to get quotes for a small food business. The following are some food business insurance quotes from some leading insurers: Simply Business, NEXT, and CoverWallet. All quotes are for a general liability insurance policy for a food business only.

Food business insurance quotes from Simply Business

Below are the quotes we receive from Simply Business. It

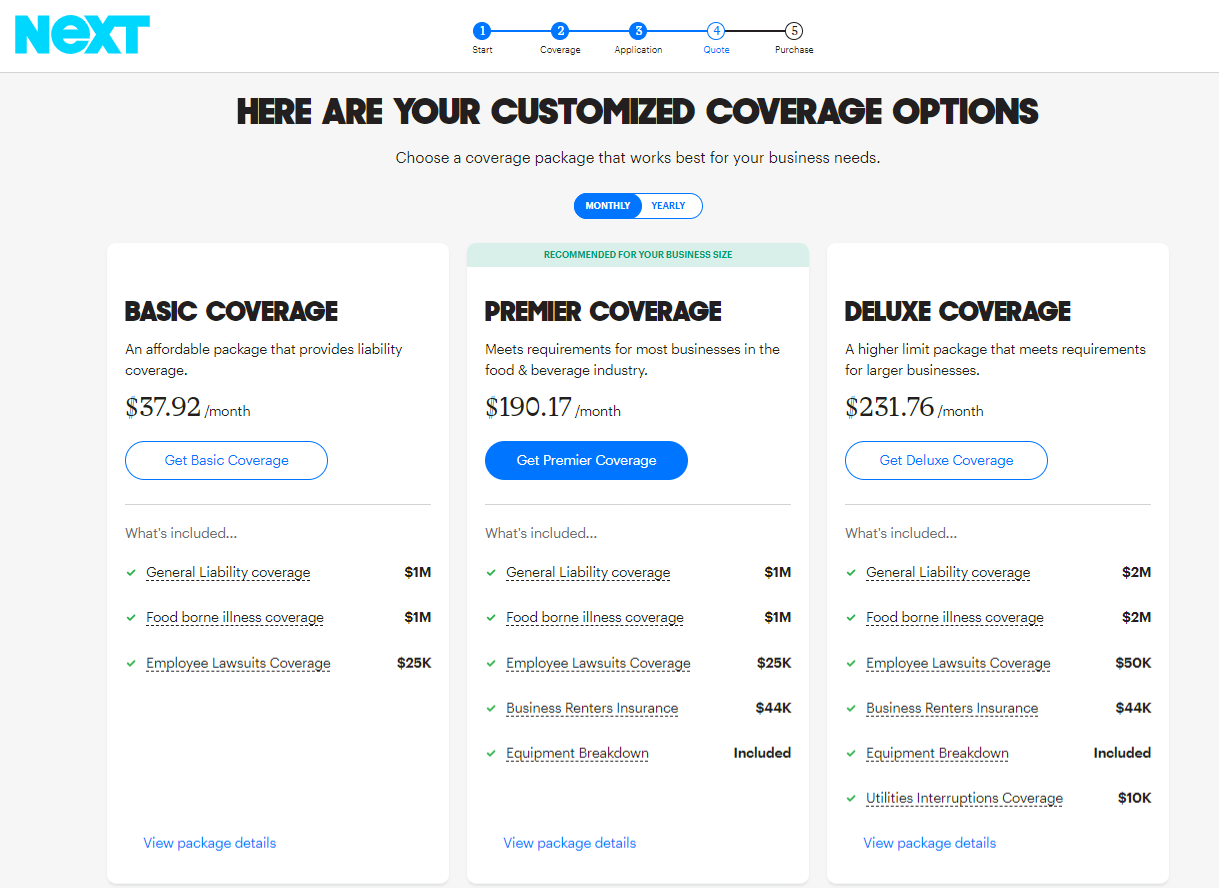

Food business insurance quotes from NEXT

Below are different quotes that we got from NEXT for a small restaurant. The basic option only costs $37.92 per month and it includes general liability, food borne illness coverage, and employee lawsuit coverage.

The premier option costs $190.17 per month and the policy also includes business renter insurance and equipment breakdown coverage.

Food business insurance quotes from CoverWallet

Below are the quotes that we receive from CoverWallet. They provide 2 quotes: one from Chubb and the other from Liberty Mutual. They are both reputable carriers and the quotes are only for general liability coverage.

What factors affect the cost of food business insurance?

The amount you pay for food business insurance depends on your business type and the nature of your risk profile. The following factors will, in most situations, affect the cost of your insurance:

Experience

The number of years you have spent in the industry is an important factor that determines your premium. In most cases, insurers will favor clients that have spent at least 5 years in the industry with lesser premiums. The general idea behind this is that, with more experience, you have more knowledge to handle situations better which means fewer claims.

The average number of customers

Your insurer will also like to know the number of customers on average that you serve each year. This is important when calculating general liability and business owners’ insurance policies. Usually, the more customers you serve, the more the possibility of accidents that may lead to claims. Therefore, food businesses with more average customers annually tend to pay more for their premiums.

Number of employees

This works just the same way as the customer count. The more employees you have, the more the possibility of having issues with customers that might lead to claims. Your employee count is also an important metric for calculating workers’ comp. Unlike other types of insurance, workers’ comp is calculated based on the number of employees you have. So, the more employees you have, the more you pay for workers’ comp insurance.

Annual revenue

Companies with large annual revenues tend to pay more for their insurance policies. This is because food companies with larger revenues are usually targeted with lawsuits than smaller ones. Also, when there is a lawsuit, the potential payout is usually larger for companies with huge revenues.

History of compensation claims

If your food business has a long history of insurance claims, irrespective of the insurance type, your premiums might be slightly higher than usual. The reason is companies with a long history of claims tend to continue with their behavior. Therefore, insurers will give them higher premiums in anticipation of future claims.

Business property

The kind of business property you have will determine the cost of your business owner’s policy and your commercial property insurance. To arrive at a quote, your insurer will likely want to know the type of structure you have, whether it is masonry, frame, or metal. Usually, masonry buildings cost more to insure since they can be consumed by flames.

The age of your building is also important. That is because, as your building ages, the more the possibility of issues occurring. Therefore, older buildings may cost more to insure.

Also, your insurer will want to know whether you have firefighting and safety equipment installed in the building. Buildings that do not have this safety equipment tend to pay more.

Finally, the insurer will consider the property’s value, including its contents and equipment. The more expensive the building and the contents are, the more costly the premium.

How to find cheap food business insurance?

Once you have a firm grasp on the various forms of food business insurance and their typical premiums, it is time to begin your search. The following are some ideas that might help you find affordable plans:

Find out what you need.

Many factors, including the specific firm and its location, contribute to every given food enterprise’s risk. A good insurance broker will help you evaluate the threats facing your company and advise you on the policies that would best protect your startup. You should also find out if your state or city has any regulations concerning food business insurance.

Try to get different estimates.

Compare prices and plans from many companies to find the best fit for your company. Don’t take the first deal you get, as it might not be the best bargain available.

Combine multiple policies

For example, a business owner’s policy combines general liability insurance and commercial property insurance. It’s possible that doing so will reduce your regular premium payment.

Pay your full premium at once

In most cases, you can divide the cost of your business owner’s insurance into 12 equal monthly payments. Making smaller monthly payments may be appealing, but you should really consider paying the full price. Many insurance providers provide savings to businesses that pay for coverage on an annual basis. Sometimes these savings can be up to 20%.

Preventatively handle potential dangers

As we mentioned earlier, insurance premiums for food companies are more affordable if the business has a clean claims record. One efficient strategy to get clean claims record is to develop a thorough strategy for managing risks.

The following are some ideas to help you do that:

- Create guidelines for social media posting.

- Create a comprehensive training program for staff.

- Make sure to examine and create checklists for your procedures.

- Invest in high-quality safety systems.

- Reduce potential risks on your property.

What is food business insurance?

Food business insurance is a type of insurance that is specifically tailored to protect food businesses from any losses associated with their operations. Food businesses are exposed to several types of risks and a comprehensive insurance policy customized for food businesses will protect them from these risks.

It typically includes coverage for property damage, general liability, and product liability with food-borne illness, contamination, and spoilage coverage.

What does food business insurance cover?

The coverages that food businesses need will vary depending on the size and scope of their operations. Generally speaking, food businesses such as restaurants or food trucks, or food vendors should consider coverage for property damage due to fire or theft. The policy will cover the physical building and any contents inside it.

Food businesses also need general liability and product liability insurance in order to protect themselves from claims of bodily injury or property damage caused by the products they sell.

- General liability insurance can cover medical expenses, legal fees, and other costs associated with an incident that results in a lawsuit against the business.

- Product liability insurance is also necessary to protect the business in cases where customers claim their product caused injury or illness because of a defect in quality or design. It usually includes all food-borne illnesses, contamination, and spoilage coverage.

Food businesses should consider business interruption insurance due to natural disasters or other events. This coverage will provide them with income loss due to any covered perils.

Additionally, professional liability coverage may be necessary if the business provides advice or consultation services related to food preparation or safety.

Food liability insurance

Food liability insurance is a type of insurance that covers any damage or bodily harm caused by food-related incidents. It can cover legal costs, medical bills, and other damages related to food-borne illnesses, as well as product recalls, spoilage, and contamination. This insurance is necessary for businesses involved in the production, storage, transportation and distribution of food products, as it ensures that they are protected from potential claims brought by customers who may have been harmed due to the negligence of the business.

Food businesses usually get food liability coverage through a comprehensive general liability insurance customized for food businesses. It must include food-borne illnesses, contamination, and spoilage coverage because these are critical for any food business operation.

What kinds of businesses need to have food business insurance?

Businesses that need to have food business insurance include restaurants, catering companies, grocery stores, bakeries, food trucks, and other mobile food vendors, farmers’ markets, food delivery services, meal delivery services, and any other business that handles food for sale.

Bakery shops and home bakery businesses should also consider having food business insurance.

Below are our specific guides for different food business types to buy insurance coverages: restaurant insurance; catering insurance; food truck insurance; food vendor insurance; and bakery insurance.

Food vendor insurance

Food vendor insurance is a type of insurance designed to protect food vendors from various financial losses. It covers the costs associated with liabilities that can occur due to mistakes made while serving food, such as contamination, spoilage, injury, and property damage. It also covers any income lost due to illness or other unforeseen events that prevent the food vendor from operating normally. Additionally, it can provide protection against theft or vandalism of equipment and products.

What insurance coverage a restaurant would need?

A restaurant would need the following insurance coverage:

- General liability insurance: This will provide protection against third-party claims of bodily injury, property damage, and personal injury that could occur on the restaurant’s premises.

- Product Liability Insurance: This will provide protection against any legal claims arising from products sold by the restaurant such as food or beverage items.

- Liquor Liability Insurance: This will provide protection for any alcohol-related incidents that take place during the course of a restaurant’s business operations, such as injuries caused by intoxicated patrons.

- Property Insurance: This will protect the restaurant’s physical assets, buildings, equipment, furniture, etc., in case of theft, fire or other damages due to natural disasters or accidents.

- Business Interruption Insurance: This will cover losses related to revenue due to interruptions caused by events outside of the business’ control such as fires, floods or pandemics like COVID-19.

- Cyber Liability Insurance: This will protect businesses against cyber risks associated with data breaches and other cyber threats that could lead to financial losses or reputational harm. if a restaurant processes customers’ credit cards, they will definitely need this coverage

- Workers comp insurance: This coverage provides financial protection for the business in the event of an employee suffering a work-related injury or illness. It covers medical expenses, lost wages, and other costs that may arise resulting from such an incident. Additionally, it helps protect the restaurant from lawsuits originating from employees injured or ill on the job due to workplace conditions or other types of negligence.