If you own a small business in California, the state laws demand that you carry workers’ compensation insurance. However, comprehending the intricacies of this policy may be difficult. That’s why we put up this guide to help you understand California workers’ compensation laws.

First, how can you obtain workers’ compensation insurance in California? The following are some of the options that you have:

- Buy workers comp insurance in California from digital brokers

- Buy workers’ comp insurance in California from traditional insurance companies

- Apply for self-insurance status in California

- Buy workers’ comp insurance in California from insuretech companies

- Buy workers’ comp insurance in California through the State fund

- What benefits do workers comp insurance provide in California?

- Is workers’ compensation insurance required in California?

- Workers’ comp exemptions in California

- How much does workers’ compensation insurance cost in California?

Buy workers comp insurance in California from digital brokers

Digital brokers are online companies that work as agents. They do not sell policies; instead, they offer companies insurance policies from their partners.

These companies have online platforms where business owners can compare quotes from different companies within minutes. When you find the policy you want, you can buy, monitor, and manage your policy on the website.

Examples of digital brokers in California include:

- CoverWallet

- Policy Sweet

- Commercialinsurance.net

- CoverHound

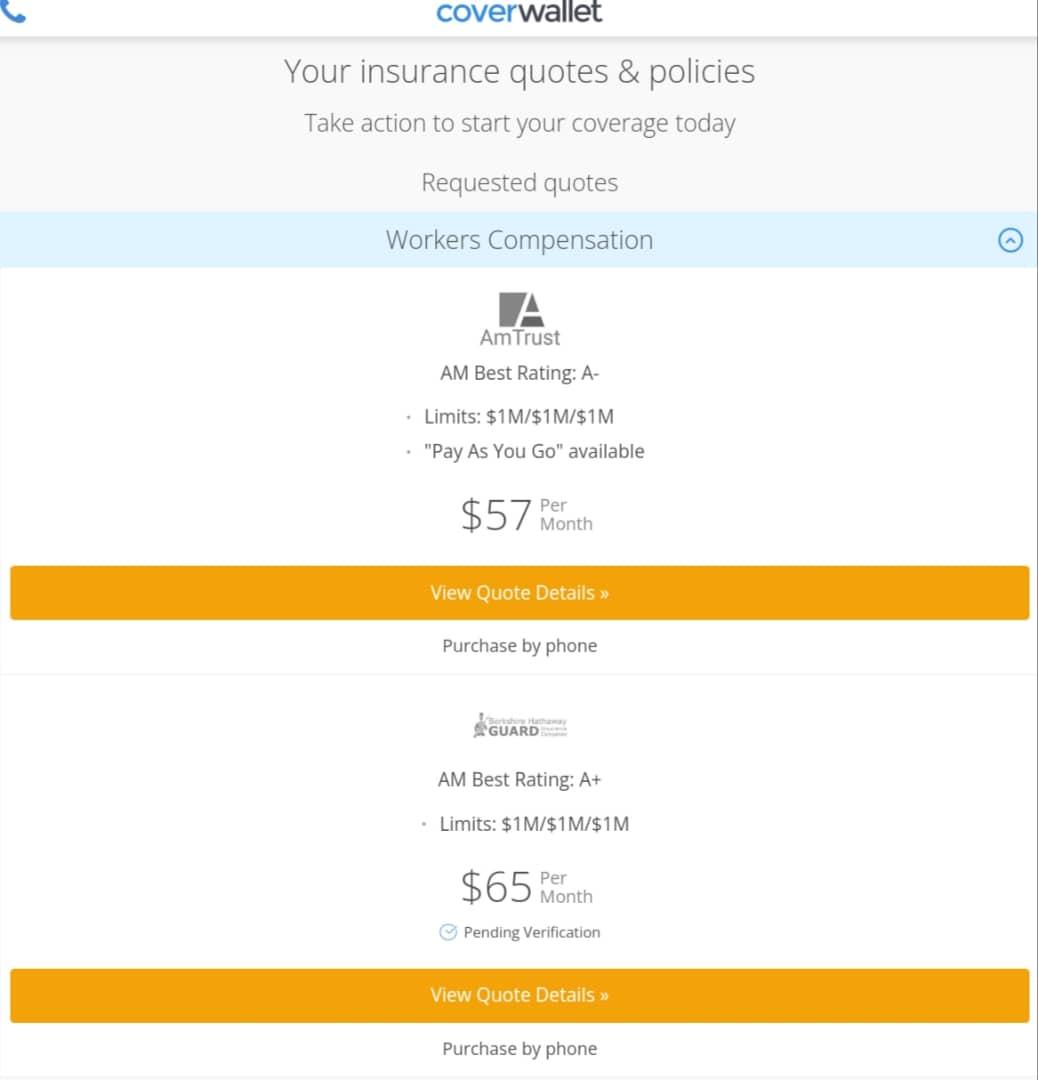

The following is a sample quote generated for a small California accounting firm from CoverWallet. The hypothetical firm has two workers, $500,000 annual revenue and $170,000 annual payroll.

Pros

- Digital brokers make it easy and fast to compare quotes across multiple companies.

- This option is the best if you have not bought a policy before. It gives you an ideal place to start if you don’t know which company to choose.

- You can manage all of your policies with digital brokers.

Cons

- Digital brokers don’t offer all their quotes online. If your business model is too complicated, you might need to speak with a representative.

- Digital brokers can only suggest the policies from their partners. So, if there is someone offering something cheaper out there, you might not know.

Buy workers’ comp insurance in California from traditional insurance companies

This is the most common method to get workers’ comp insurance in California. Those who opt for this method buy their policies from insurance companies and handle claims through their insurance company.

Traditional insurance requires employers to pay a predetermined premium to an insurance company to ensure coverage. The payments might be monthly or annually, depending on the business owner.

Some traditional insurance companies that offer the workers’ comp in California include:

- The Hartford

- Liberty Mutual

- Amtrust Financial

- Chubb

- Employers

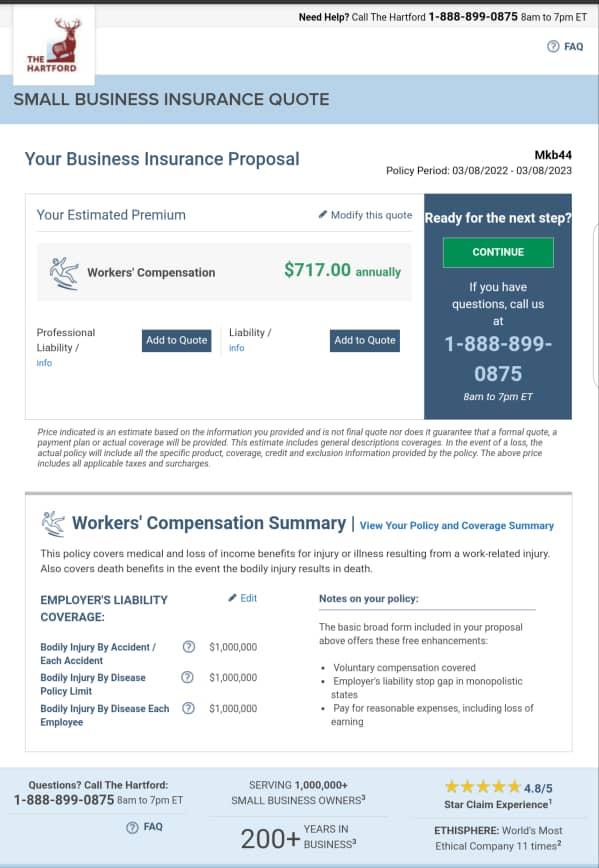

The following is a sample quote generated for a small accounting firm from The Hatford. The hypothetical firm has two workers, $500,000 annual revenue and $170,000 annual payroll.

Pros

- Many traditional companies now offer online services. That means you can access their services online at a fast rate.

- These companies have been around for years, so they offer workers’ comp to almost all industries.

- Traditional insurance companies also offer other business insurance policies. You can bundle them together and get discounts.

Cons

- This can be expensive, depending on where you buy the policy.

- There are too many options that might be confusing for new business owners.

Apply for self-insurance status in California

Self-insurance refers to a scenario where employers opt to pay for their liabilities independently. To self-insure in California, employers must seek approval from the Department of Workers’ Compensation of California.

Such companies must be worth $5million or more. They must also have a net annual income of at least $500,000 and a security deposit.

Pros

- Companies that self-insure do so to cut the cost of high premiums.

- It helps companies stay aware and control the inherent risks in their company since they are paying for them.

Cons

- Not every business qualifies for the requirements of self-insurance

- Risk assessment can be tricky. If not correctly done, the company might pay more in the event of injuries.

Buy workers’ comp insurance in California from insuretech companies

Insuretech companies are relatively new players in the insurance industry. These are tech companies that help businesses find the right insurance policies. Like digital brokers, they do not offer any policies. Instead, these companies use the latest tech tools such as artificial intelligence to help their clients find the best policies.

Pros

- These companies might be able to find the cheapest policy for your company

- They offer a good user experience and a fast quote generation process.

Cons

- Most companies in this category are new. They lack the experience to offer policies for companies in risky industries like construction.

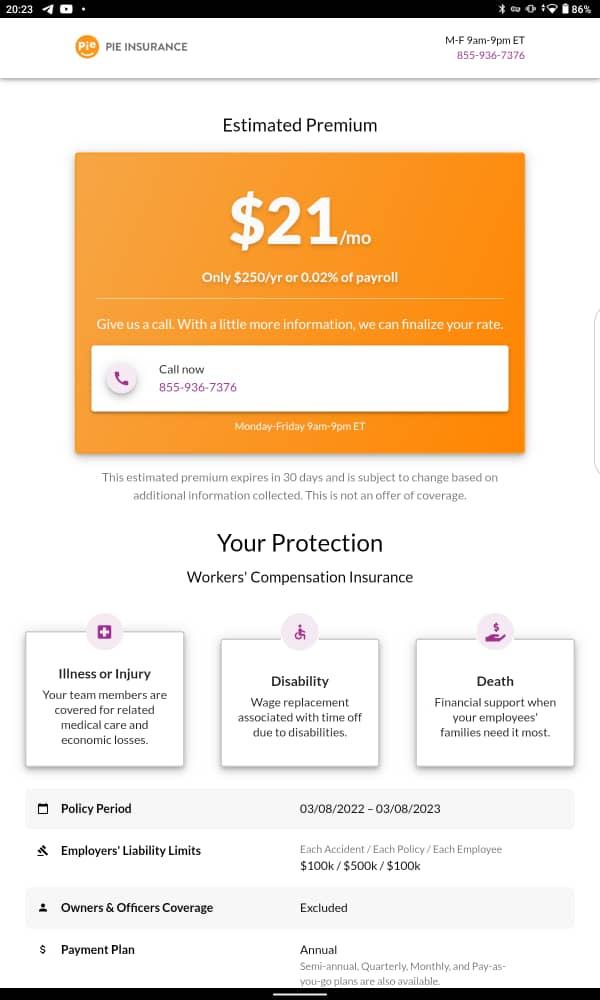

The following is a sample quote generated for a small accounting firm from Pie insurance. The hypothetical firm has two workers, $500,000 annual revenue and $170,000 annual payroll.

Buy workers’ comp insurance in California through the State fund

California has a state fund for workers’ comp insurance called the State Compensation Insurance Fund (SCIF). SCIF is a non-profit organization that sells workers’ compensation insurance. The State Compensation Insurance Fund also serves as a last-resort insurer when private insurance firms refuse to provide workers’ compensation to a business.

Learn more at the best workers comp insurance companies in California

How does workers comp function in California?

Under California Labor Code Section 3700, all California companies must give workers compensation benefits to their employees. The policy is monitored and regulated by the state’s Department of Workers’ Compensation (DWC).

The compensation payments under this insurance policy cover incidents such as:

- A single occurrence at work might cause employee harm. Examples include a fall that chemical burns, back injuries, and car accidents while on delivery duties.

- Repeated workplace exposures that lead to injuries or illnesses. Examples include carpal tunnel syndrome resulting from straining the wrist, back, or wrist injuries resulting from repeatedly lifting heavy items or loss of hearing due to persistent loud noise.

Some, but not all, stress-related (psychological) ailments caused by your employees are covered by workers’ compensation.

Furthermore, workers’ compensation may not cover an injury reported to the employer after the worker has been informed that they would be fired.

What benefits do workers comp insurance provide in California?

Injuries and illnesses are normal occurrences in any workplace. Even when you take all the precautions, workers can still have work-related accidents or illnesses.

In such situations where businesses face these injuries, worker’s comp insurance in California steps in to make things easier for employers and their employees.

The following are some benefits that employees get from worker’s compensation insurance in California:

- Expenses of any medical treatment required to address workplace accidents or sicknesses

- Partial pay for the injured worker while they’re out of work healing from your accident or sickness. These are also known as temporary disability benefits.

- Permanent disability benefits in a situation where the employee does not fully recover from the illness or accident. For instance, if the incident results in a permanent disability that limits the employee’s capacity to work.

In the sad situation where the employee dies due to the job injury or sickness, surviving dependents may receive death benefits.

For employers, workers’ compensation helps reduce the possibility of paying heavy compensation for work-related injuries and illnesses. It also stops the employee from suing the employer since employees that receive payment benefits cannot sue their employers.

Is workers’ compensation insurance required in California?

In California, all companies must carry worker’s comp insurance for their workers, even if the company only has one employee.

Workers’ compensation insurance is required by California law for all employees who work in California regularly, even if the company has its headquarters somewhere else. That means, even if you have an employee that works part-time, you must provide worker’s compensation insurance for them.

In addition to having workers’ comp insurance, the state also requires employees to post notifications displayed prominently at the workplace. This poster informs employees about your workers’ compensation coverage and where they may seek medical care for workplace accidents.

Sections 3550-3553 of the California Labor Code contain specific requirements. Failure to publish this notice is a misdemeanor punishable by a civil penalty of up to $7,000 per offense. Contact your insurer to obtain the posting notice and the needed information.

In addition, you must present newly recruited employees with a workers’ compensation handbook that explains their rights and obligations.

Workers’ comp exemptions in California

Although the laws of California state that every company with at least one employee must have workers’ comp, there are a few exceptions.

If your company is a sole proprietorship, single-member LLC, or partnership with no workers, you don’t need to get insurance by law in California. But then, if you are a roofer, the exclusion does not apply to you. Whether you hire employees or not, roofing companies must carry workers’ compensation insurance. If you are a non-roofer sole proprietor, by laws, you are exempt from workers comp insurance. However, it is still a good idea to have the protection. Learn more at the best workers comp insurance companies for sole proprietors.

Similarly, if you hire independent contractors, you are not required to include them in your policy. That’s because they are not legally employees of your company. Similar to the above, it is still a good idea for independent contractors to have workers comp insurance to protect themselves in case they are injured while working. Learn more at the best workers comp insurance for independent contractors.

However, it can be tricky to define who an independent contractor is. Many business owners make the mistake of classifying employees as independent contractors. Such mistakes can be costly and may result in payment for employment taxes and penalties. For clarity, you can consult with your attorney to categorize your employees.

Executive officers in business entities in California are automatically included in workers’ comp insurance. However, they have the right to exclude themselves if they choose to. However, these officers must meet the provisions stated under the California Labor Code Section 3351 and 3352.

This regulation specifies the requirements such as family relationship to governing members, the percentage of ownership, and provisions relating to trusts. Also, such officers must file for exclusion in the form of an affidavit with the state through WCRIB. Some carriers might submit the exclusion for you, but the company owner is ultimately accountable.

To understand if you qualify for an exemption, you should speak with your attorney.

What if I don’t have the required workers’ comp?

It is a crime not to have workers’ compensation coverage. According to Section 3700.5 of the California Labor Code, the following are some penalties you may face:

- Misdemeanor charges punishable by a fine of up to $10,000 or incarceration in a county jail for up to one year, or both.

- State-imposed fines of up to $100,000 if you are unlawfully uninsured.

- You are liable for any medical expenditures incurred due to the injury or sickness while you do not carry the policy.

Moreso, your workers’ comp benefits offer you protection against civil suits in cases of work-related injuries or illnesses. Not carrying this policy means you have to face the consequences of your employees decide to sue you for their injuries or illnesses.

How much does workers’ compensation insurance cost in California?

Workers’ compensation coverage in California costs an average of $183 per month. It is critical to understand that the state does not control workers’ compensation premium rates. Various criteria determine the amount you pay, and your rate may differ from one insurer to the next.

Most insurers calculate the rates using these factors

- The industry of your business and its inherent risks

- The location of your firm

- The types of duties your employees undertake

- The payroll generated by your employees

- The company’s safety record

Be sure to shop around with a few companies or work with a digital broker who can pull several quotes for you to compare and select the cheapest one for your company.

Learn more at how much workers comp insurance costs and how to calculate workers comp insurance cost

Who pays for workers’ compensation insurance in California?

In California, the employer pays for workers’ compensation insurance. Workers’ compensation insurance is included the running cost of the business. Therefore, an employer cannot require employees to contribute to the insurance premium cost.

How do I find cheap workers’ comp insurance in California?

The best way to reduce the cost of workers’ comp insurance is to find the cheapest insurance policy by comparing quotes. Different companies offer different prices for their policies. If you ask around diligently, you might find a company offering the policy at a reasonable price.

Also, you can consider cutting the size of your payroll. This works since the size of your payroll is the most significant factor determining your premium cost. You might want to use independent contractors instead of full staff members.

Another option is to conduct work safety lectures for your workers. Insurance companies generally offer discounts to companies that commit to safe working conditions.

Learn more at the cheapest workers comp insurance companies