If you’re a sole proprietor, independent contractor, freelancer, or owner of any other one person operation, it’s likely that your state doesn’t require you to get workers’ compensation insurance. However, there are a few situations where you will need to get it.

In this article, we’ll reveal the top 5 providers of worker’s compensation insurance for sole proprietors, explain the situations in which sole proprietors need to have workers comp coverage, and provide all the information you need to understand the benefits of having the coverage, what it covers, and how to get it.

- Top 5 workers’ comp insurers for sole proprietors

- Why do sole proprietors need to have workers comp insurance coverage?

- What does workers’ compensation for sole proprietors cover?

- How much does workers’ compensation insurance for sole proprietors cost?

- What other coverages do sole proprietors typically need?

- How does workers’ comp coverage differ from liability coverage?

- How do sole proprietors get workers comp coverage?

Top 5 workers’ comp insurers for sole proprietors

- CoverWallet: Best for sole proprietors who want to compare quotes quickly

- Cerity: Best for stand alone workers’ comp coverage

- biBerk: Best for low-cost sole proprietor workers’ comp coverage

- THREE: A one stop shop for all your business insurance needs, including workers’ comp

- The Hartford: Best for single person businesses that want an ethical insurer

CoverWallet: Best for sole proprietors who want to compare quotes quickly

CoverWallet is a cutting-edge insurance provider. The firm has developed its own state-of-the-art platform, based on its own algorithms, to ensure it is able to connect small businesses with all the business insurance they need, at the most reasonable price. The platform makes it quick and easy to get quotes from several providers at once, making it possible to compare quotes from highly reputable insurers all on a single screen.

The firm’s experts have used their extensive experience to make sure you only have to input the information needed to generate quick and accurate quotes. The entire process should take ten minutes or less.

You can feel confident knowing that CoverWallet is a part of Aon, an established company that provides advice to businesses on things like risk, health and retirement.

Once you get your quote, CoverWallet makes it easy to purchase business insurance online or through an agent. When you get your policy through CoverWallet, it’s simple to manage your coverage online, including downloading a certificate of insurance, filing a claim, renewing your policy, and more.

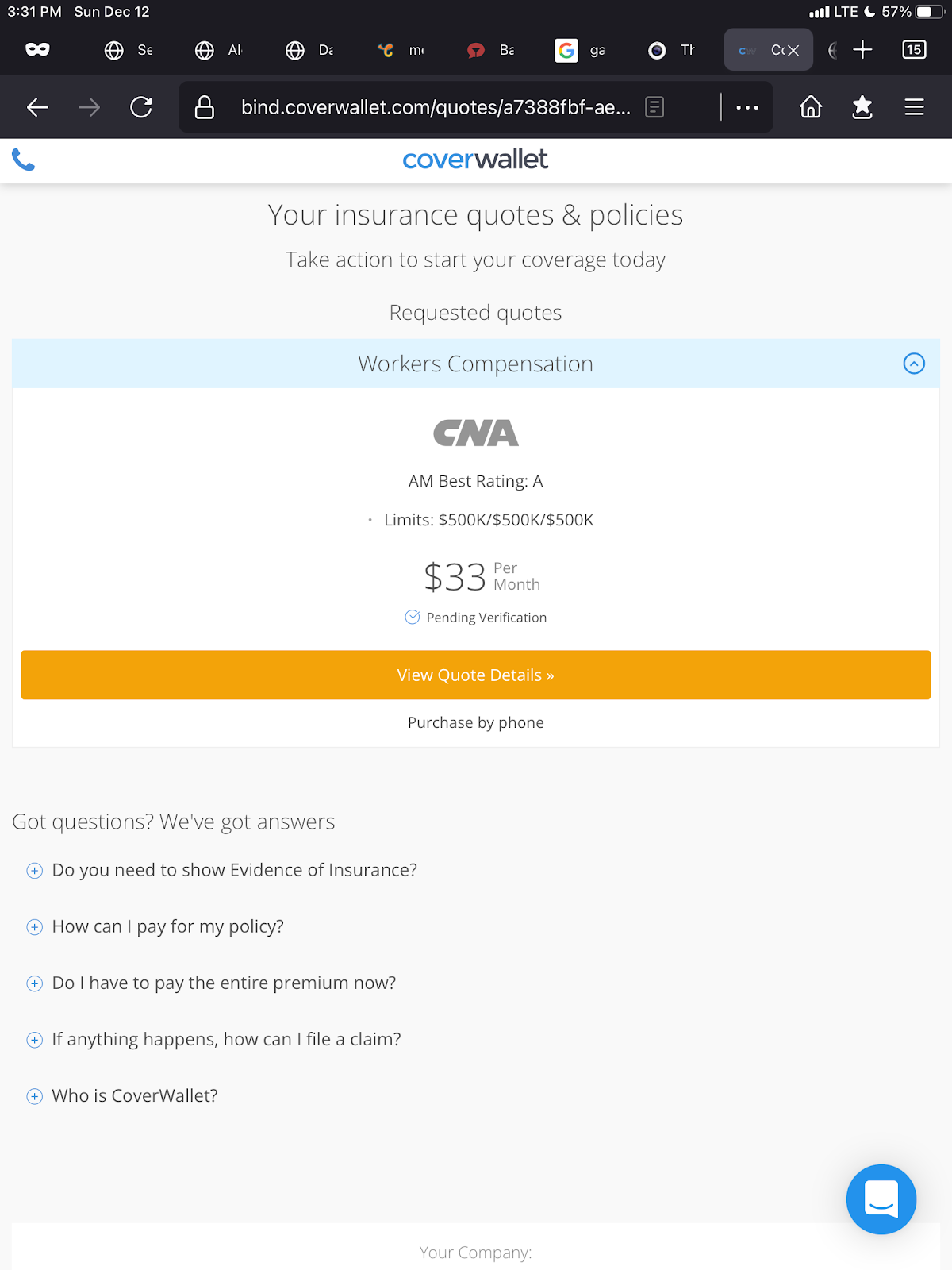

Here s a sample quote from CoverWallet.

Cerity: Best for stand alone workers’ comp coverage

Cerity makes our list of top workers’ compensation providers because it specializes in the coverage. It currently does not offer a Business Owners Policy or other types of insurance. It’s a relatively low cost provider, yet delivers a high level of service. Policies start as low as $25 per month and the company has fewer fees than most insurers. Cerity makes it fast and easy to get a quote online.

Cerity isn’t low cost because it cuts corners. It actually uses artificial intelligence to up its efficiency. However, everything at Cerity isn’t technology based. When you require help, you will have access to a team of licensed policy and claims experts. You can rest assured knowing Cerity has been in business for more than a century and is rated highly by its clients.

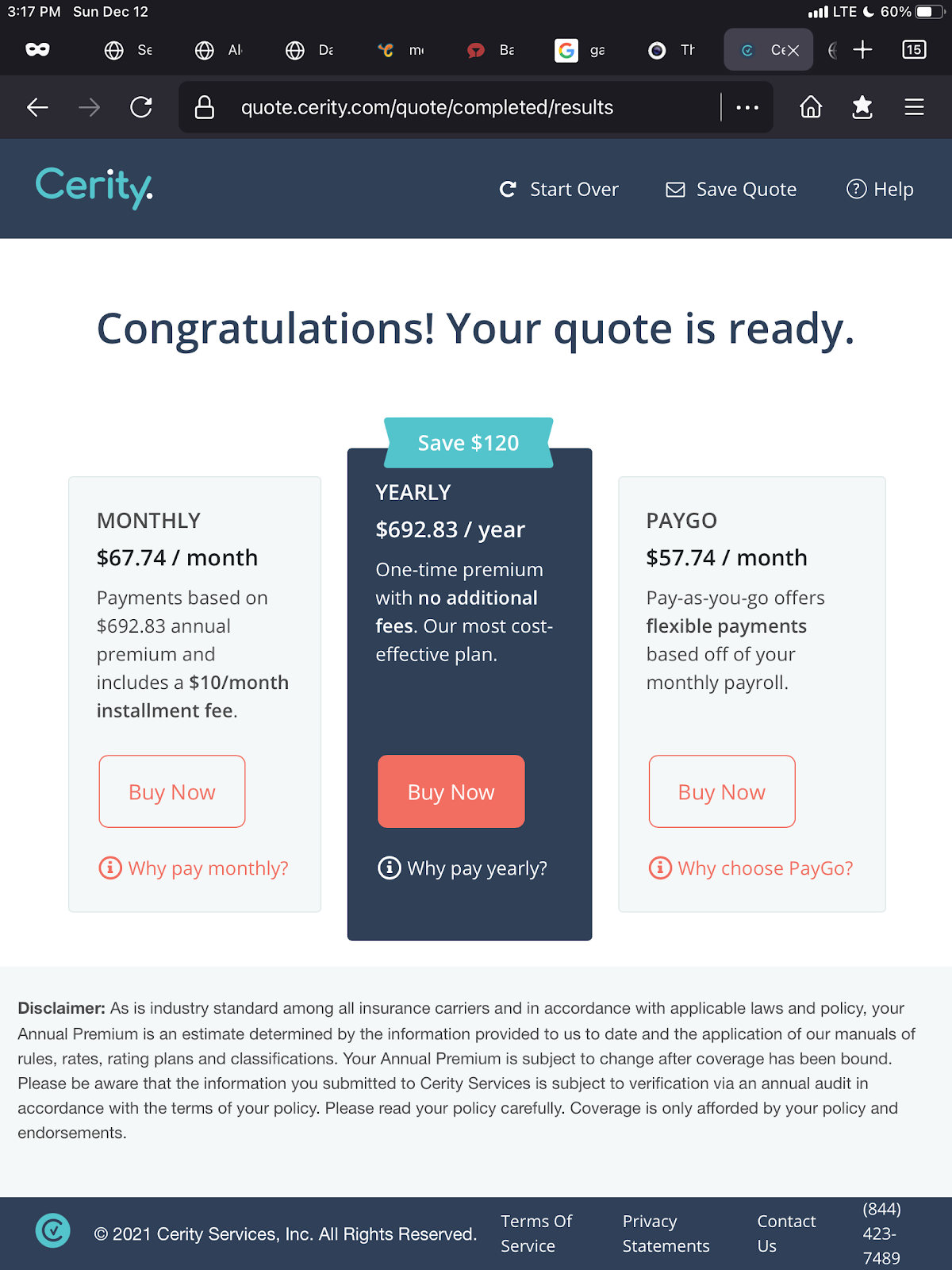

Here is a sample quote for a one person marketing agency from Cerity.

biBerk: Best for low-cost sole proprietor workers’ comp coverage

After the last few years, few one person operations are sitting on extra cash to spend on insurance. If that’s the case with you, biBerk could be the ideal insurer for you.

biBerk is a low-cost business insurance provider. Despite saving money on your business coverage, you can rest assured knowing you’re still getting quality protection for the company you’ve worked so hard to build. biBERK is able to lower insurance costs by almost 20 percent because it insures small businesses directly, without the added expense of having to work through a middleman or insurance broker.

You can feel confident knowing biBerk is a part of Berkshire Hathaway, a company headed by well-known investor Warren Buffett. It’s a firm that has millions of satisfied customers that’s been insuring businesses for more than 75 years.

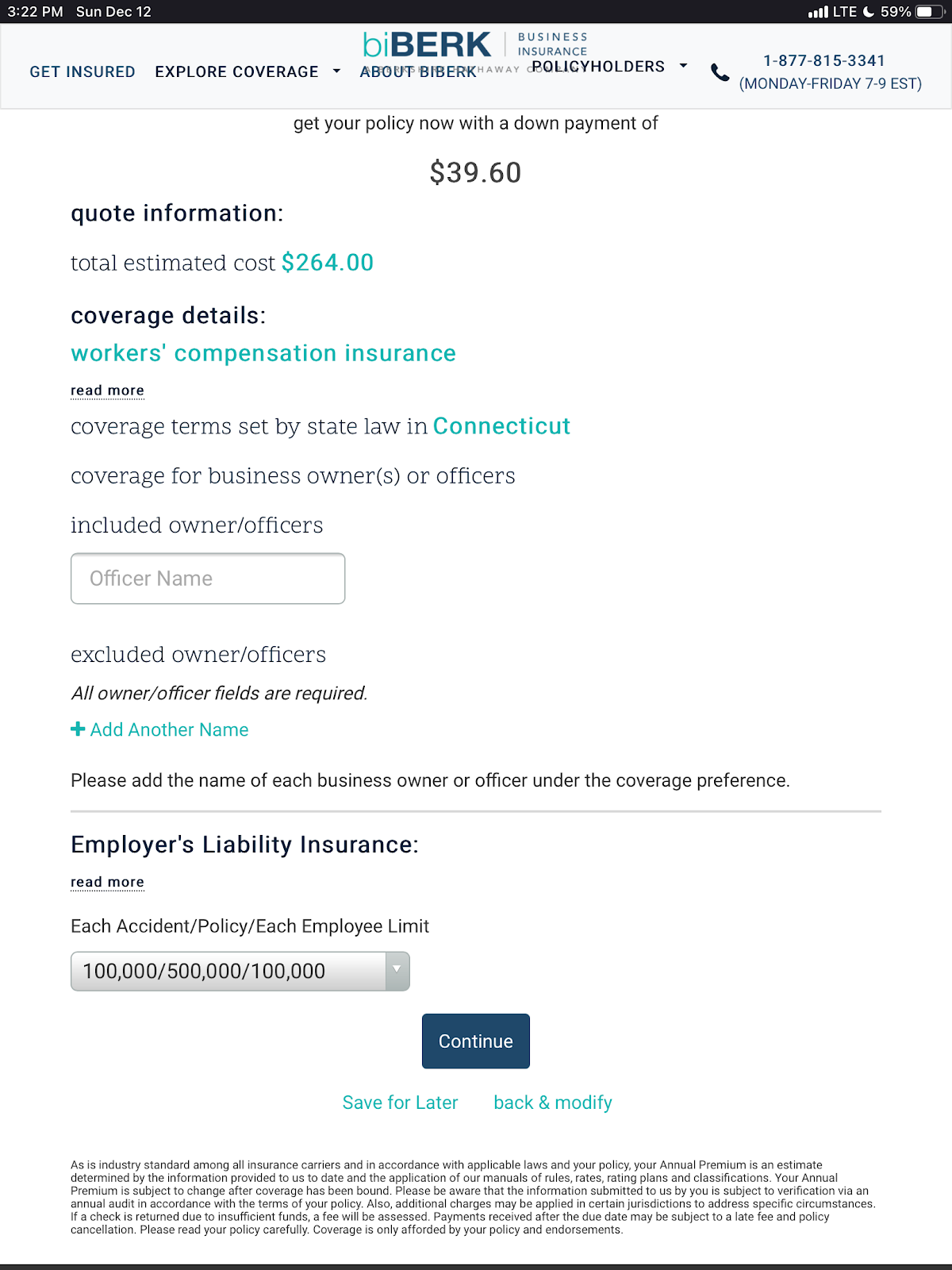

Here is a sample workers’ comp quote from biBerk.

THREE: A one stop shop for all your business insurance needs, including workers’ comp

If you’re a busy independent contractor who doesn’t have much time to shop for workers’ comp and other business insurance, THREE could be the ideal solution for you.

THREE is also a part of the Berkshire Hathaway family of companies. It offers a single policy that covers most of the risks faced by sole proprietorships and other types of businesses. The firm prides itself on the fact that it has a simple three page policy with no fine print or surprises.

The single policy covers:

- Workers’ comp: Complete on-the-job protection against injuries

- Liability: General liability, errors, and omissions, and employment practices

- Cyber: Cyber liability, data compromise, and incident response. Learn more at the best cyber insurance companies and the best data breach insurance companies.

- Property and business interruption: Fire, theft, flood and water damage, wind and hail, and earthquake. Learn more at business property insurance and the best providers of business property insurance and the best business interruption insurance companies.

- Business auto: Collision, comprehensive, auto liability, and hired and non-owned. Learn more about the differences between commercial auto and personal auto insurance and the best commercial auto insurance companies.

If simplicity and comprehensive coverage are important to you, THREE could be a good provider for your one person operation.

The Hartford: Best for single person businesses that want an ethical insurer

Do you want to get your workers’ comp coverage from an honest and ethical provider? The Hartford could be the perfect insurer for you.

The Hartford is one of the oldest companies in the U.S. It’s offered insurance solutions for more than 200 years and has helped one million plus businesses with their insurance needs.

The company takes pride in the fact that the Ethisphere Institute has named The Hartford a World’s Most Ethical Company twelve times. The Hartford’s longevity and focus on ethics makes it a company that you can feel confident about entrusting your business and the well being of your employees to.

Why do sole proprietors need to have workers comp insurance coverage?

It is likely that your state doesn’t require you as a sole proprietor to have workers comp insurance. However, you may still be required to carry it in the following cases:

- When clients require it. It’s possible that a sole proprietor could be injured while working at a client’s work site. If this happens, it’s possible that the client could be held responsible for the medical and other costs related to the injury. Many businesses have faced workers’ comp claims from independent contractors who got hurt on the job. If a client views this as a possible risk, they may require you to get workers’ comp coverage to protect themselves, and most states don’t have laws against this. It’s likely that they won’t hire you if you don’t get protection.

- If you hire subcontractors. Some states have laws that require independent single person businesses to purchase workers’ comp coverage if they hire subcontractors, even for a limited period of time. If you don’t get coverage and a subcontractor is injured while working for you, you may be held liable for covering their medical care and other things related to their injuries, along with penalties and fines because you didn’t have the required workers comp coverage. If you have a single person business and decide to hire someone to work for you, even for a short period of time, it’s a good idea to check with your state’s workers’ comp agency or board — or your business insurance agent — to find out if you need coverage. Another option may be to require your subcontractors to get their own coverage. Again, your state workers’ comp website or an insurance expert can advise you on whether this is a possibility.

- Non-W-2 workers. As a sole proprietor, you don’t have W-2 employees. However, your state may view part time, or other non-W-2 workers, as employees and because of that, it may require you to get workers’ comp coverage for them. It’s worth checking into because your state may come down hard on you if you hire another independent contractor, they become injured on the job, and you don’t have required coverage. The ramifications could be similar to those in the section above.

In the end if there are any doubts about whether you need to purchase workers’ comp insurance, you should:

- Review the applicable regulations on your state’s workers’ comp bureau or agency website.

- Consult with your attorney, business insurance agent, or insurer rep to find out if you need coverage.

One more thing to think about: Even if you’re a sole proprietor with no employee related issues, it could still be a good idea to get workers’ comp insurance. If you’re ever injured on the job, it will pay for medical expenses and other benefits, which we will cover in greater detail later in this article.

Learn more at Are Sole Proprietors Required to Have Workers Comp Insurance?

What does workers’ compensation for sole proprietors cover?

In short, if you or a subcontractor suffers a work-related injury or illness, worker’s comp will help cover:

- Medical expenses

- Lost wages

- Ongoing care costs

- Funeral expenses (along with benefits to family members)

- And more.

Here’s an overview of the standard workers’ comp coverages:

Medical expenses

Workers’ comp insurance helps pay for medical expenses related to a job-related injury or illness. This includes things like emergency room visits, doctor appointments, surgeries, and prescription drugs.

Example: If you cut your hand while remodeling a customer’s home, workers’ compensation insurance can help cover your hospital visits and ongoing treatment.

Illness

There are situations when working conditions could expose you to harmful chemicals or allergens that cause illness. If you become sick because of your work, workers’ comp insurance will help cover your costs for necessary treatment and ongoing care.

Example: You have been refinishing cabinets for years, which exposed you to noxious fumes and dust. This results in serious lung and breathing issues. Workers’ comp will cover your related medical care and ongoing therapy.

Missed wages

Workers’ compensation helps replace some of your lost income if you have to take time off to recover from a job-related injury or illness.

Example: You own a one person muffin business. One day, you burn your arm on the stove and can’t work because of it for a month. Workers’ compensation coverage will replace some of your lost income.

Ongoing care

What happens if a work-related injury or illness is so severe that you need treatment over a long period of time? Workers’ comp will cover all those treatments.

Example: If you hurt your back when lifting heavy boxes at your store and the pain and physical limitations last a long time, workers’ comp insurance can help cover your ongoing costs for physical therapy.

Funeral expenses

If you lose your life because of a job-related accident, workers’ compensation insurance will help cover your funeral costs and provide death benefits to your beneficiaries.

Example: You have a fatal accident while doing gardening work at a client’s home. Your funeral costs will be paid up to a certain level and your beneficiaries will receive a payout.

Repetitive injury

Not all job-related injuries happen because of a single incident. Injuries that result from repeated movements, such as carpal tunnel syndrome, can take months or years to happen. Workers’ comp will pay for therapy and other treatments.

Example: You develop carpal tunnel syndrome after years of typing with poor ergonomics, workers’ comp can help cover treatment costs and ongoing care bills.

Disability

Some work related injuries could be severe enough to temporarily or permanently disable you, preventing you from working. Workers’ compensation coverage will provide you with benefits that pay your medical bills and replace some of your lost wages.

Example: You lose the use of one of your arms in a work related incident and are unable to work because of it. You need continued medical and financial support. Workers’ comp will cover your treatment costs and supplement some of your missed wages through disability benefits.

Important note: Workers’ compensation benefits aren’t approved if you’re injured or become ill when you’re not working. Benefits will also not be approved if you are intoxicated or high when an incident occurs, or if you intentionally injure yourself.

How much does workers’ compensation insurance for sole proprietors cost?

The cost of workers’ comp for most single person operations averages about $40 to $50 per month, but it could vary depending on the type of business you’re in and other factors.

Think about it: Can you NOT afford to spend this minimal amount to protect yourself and the future security of the business you’ve worked so hard to build?

Be sure to shop around with a few companies or with digital broker like CoverWallet, Simply Business, or PolicySweet to compare several quotes to find the cheapest one for you.

What other coverages do sole proprietors typically need?

Instead of purchasing workers’ comp insurance as a stand alone, many sole proprietors find that it’s cheaper to buy it as an add on to their Business Owners Policy (BOP).

Depending on the coverage you choose, a BOP helps protect your business building and property against financial losses related to things like theft, fire, wind, falling objects, and lightning. It’s similar to the insurance coverage you have on your home or apartment.

Many one person businesses add some of the following coverages to their BOP:

- General liability: Covers medical and legal costs if a customer or visitor is injured on your business property.

- Business property: Covers the cost of business property damage that could result from a fire, weather event, burglary, and more. Even if you have a homeowners policy, it won’t cover business related losses if you run your independent business out of your home.

- Business interruption: Covers you if you’re unable to conduct business at your business location because of things like a fire or damage from a severe weather event or utility work.

- Professional liability: Pays costs related to errors made while providing services to clients and customers.

- Errors and omissions: Provides coverage if you make a mistake, provide inadequate information to a customer, or misrepresent the products you sell or services you offer.

- Data compromise: Pays expenses related to the loss or theft of personal or company information.

- Business auto: Covers your vehicle when conducting business.

This is only a small sampling of the business coverages that are available. An online business insurance application system, insurance agent, or insurance company representative can help you identify the coverages your business needs.

How does workers’ comp coverage differ from liability coverage?

Workers comp only covers you and subcontractors you hire. If a client, customer, or random person is injured at your workplace or job site, general liability insurance will cover it. General liability pays for bodily injury and damage caused by you or a subcontractor to someone else’s property.

>>MORE: The Best General Liability Insurance Companies

How do sole proprietors get workers comp coverage?

Most states allow you to choose your own workers’ comp insurance provider. You owe it to yourself to compare costs from several insurers. They have different ways of calculating premium costs and you will likely find a range of prices. You can select one that offers you coverage at the lowest possible cost.

>>NEXT: Where to Get & Compare Free Workers Comp Insurance Quotes Online?