In 1915, Pennsylvania joined other states in the US in signing into law the Pennsylvania Workers’ Compensation Act. It became compulsory for businesses to carry worker’s compensation insurance for their workers ever since.

Unfortunately, the terms that surround these laws can be challenging to understand. More so, over 300 insurance companies offer this policy in Pennsylvania. These issues sometimes make it confusing for some employees. This article will explain what it means to buy workers’ comp insurance in Pennsylvania. We also have a list of options to get the policy and the pros and cons of each option.

As an employer in Pennsylvania, you can obtain your workers’ compensation in five different ways. The options available to you include the following:

- Buy workers comp insurance in Pennsylvania from digital brokers

- Buy workers’ comp insurance in Pennsylvania from traditional insurance companies

- Apply for self-insurance status in Pennsylvania

- Buy workers’ comp insurance in Pennslyvania from insuretech companies

- Buy workers’ comp insurance in Pennsylvania state via the State Workers’ Insurance Fund (SWIF)

- Is workers’ compensation insurance required in Pennsylvania?

- Workers’ comp exemptions in Pennsylvania

- How much does workers’ compensation insurance cost in Pennsylvania?

Buy workers comp insurance in Pennsylvania from digital brokers

A digital broker works as an insurance agent. The only difference is most of their operations are online. These companies do not offer insurance policies. Instead, they partner with large insurance companies to ensure that business owners find suitable insurance policies.

With these companies, you can easily compare quotes from different companies. That way, you can make fast decisions regarding where to buy your worker’s comp insurance. Good examples of companies in this category include CoverWallet, Commercialinsurance.net, Policy Sweet, CoverHound, etc.

To buy a policy from these companies, simply visit their website. They offer quotes online in less than 10 minutes.

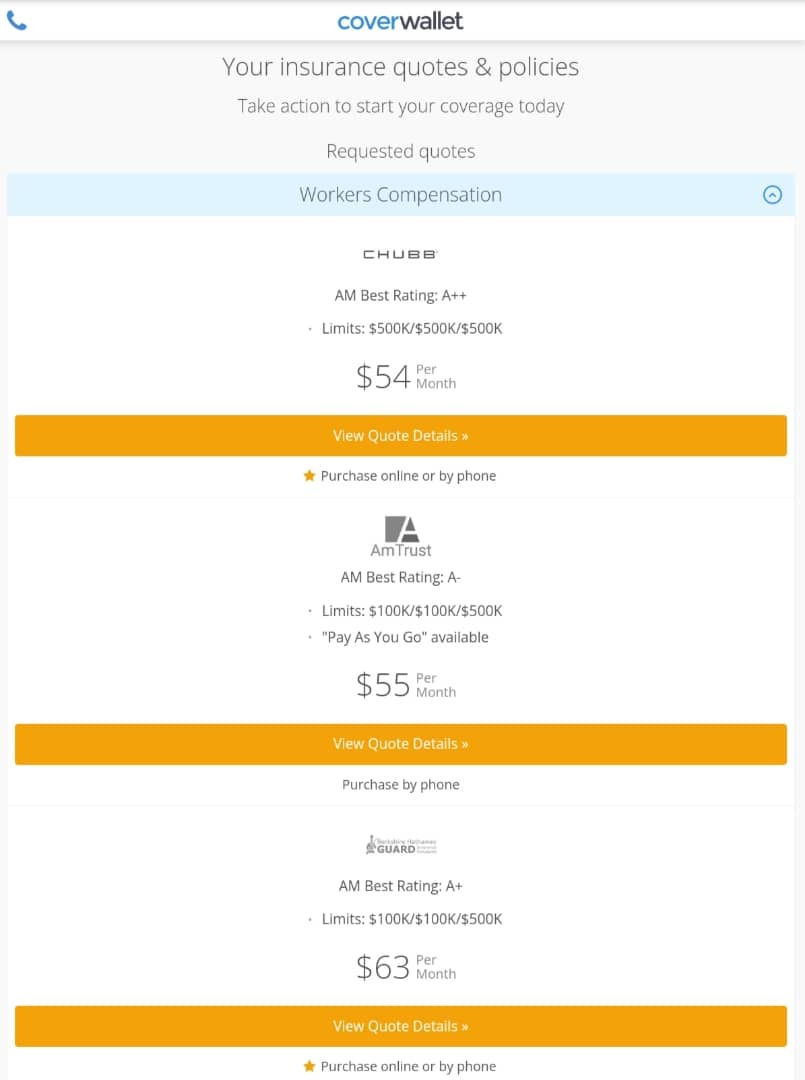

The following is a sample quote for Workers’ Comp for a small cleaning PA firm with total annual revenue of $500,000 and an annual payroll of $170,000 from CoverWallet.

Pros of buying from a digital broker

- It’s easier to find and compare quotes

- You can monitor and manage multiple policies on the websites

Cons of buying from a digital broker

- You can only get quotes from their partners.

Buy workers’ comp insurance in Pennsylvania from traditional insurance companies

A more popular option is to obtain coverage directly from the insurance company of your choice. There are more than 300 private sector insurance firms that write workers’ compensation plans in Pennsylvania.

In most cases, the process is straightforward. Most companies now offer their quotes online. In about 5 minutes, you should get your quote after supplying the necessary details.

Some examples include the following:

- The Hartford

- Liberty Mutual

- Nationwide

- Huckleberry

- Employers,

- Travelers, etc.

All these companies offer workers’ compensation in Pennsylvania at reasonable rates.

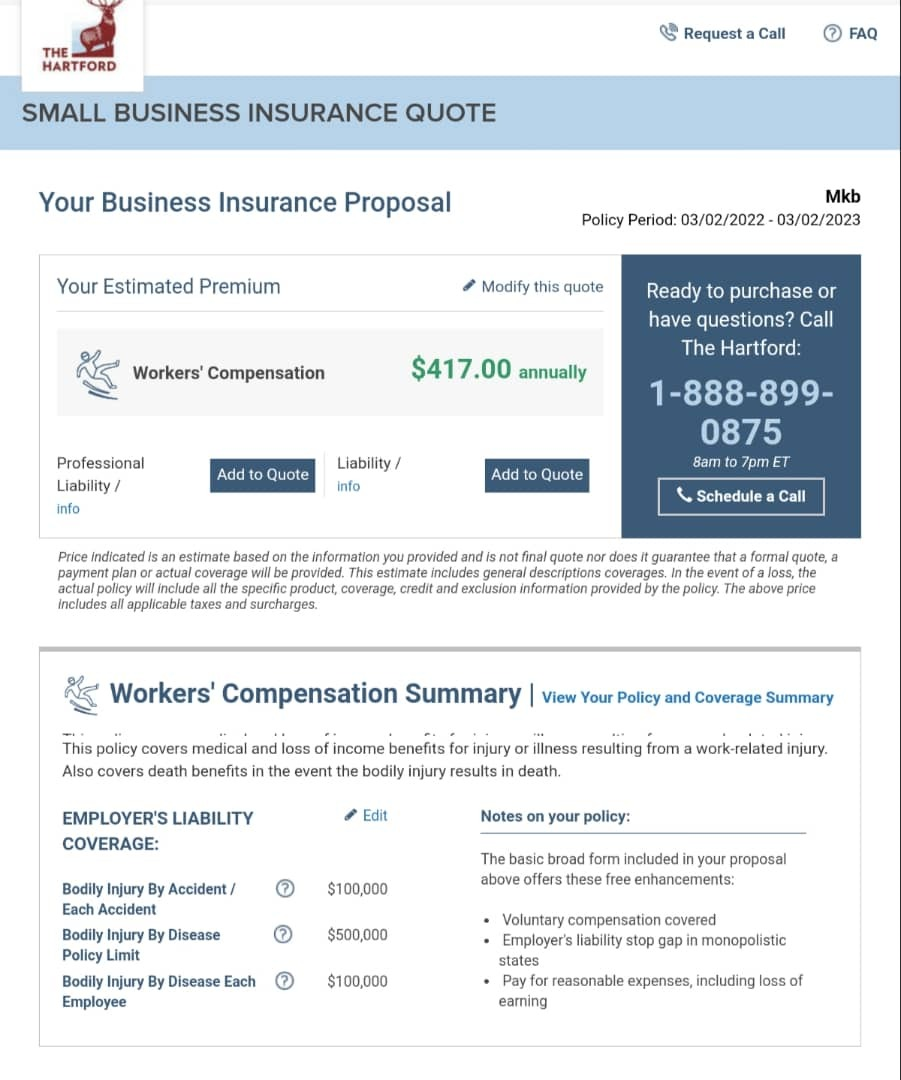

The following is a sample quote for Workers’ Comp for a small firm in Pennsylvania. The sample was obtained from The Hartford Insurance, assuming the company has total annual revenue of $500,000 and an annual payroll of $170,000.

Pros of buying from a traditional insurance company

- You get straightforward online quotes in most cases

- You can buy all your policies in one place and get discounts

- These companies have experience and superior financial strength

Cons of buying from a traditional insurance company

- It might be the most expensive option

- There are so many options to pick from, and you might be confused if you are new to buying worker’s compensation.

Learn more at the best workers comp insurance companies in Pennsylvania

Apply for self-insurance status in Pennsylvania

Large, financially sound employers that have been in business for three years or more may apply to self-insure their potential liability. Employers may also be qualified to join a recognized group self-insurance fund if one exists for their industry.

Pros of self-insurance

- It might be a less costly option if there are no injuries in your workplace.

- Self-insurance funds sometimes pay excesses back to their members at the end of the year.

Cons of self-insurance

- It can result in significant financial losses if there are reoccurring accidents.

- You lose the protection against employee laws suits with this policy

- Most small businesses do not meet the requirements for the policy

Buy workers’ comp insurance in Pennslyvania from insuretech companies

Isnuretech companies work like digital brokers. Most of these firms provide you with a quote in minutes and allow you to buy the insurance and manage your policy online. Many insuretech firms, such as Pie, Cerity, and Biberk, provide workers’ compensation insurance. Some of them also provide other forms of company insurance, but not all.

Pros of using Insuretech companies:

- Most of them offer instant online quotes

- You can buy multiple policies and manage them in one place

- They can help you find discounts sometimes.

Cons of using insuretech companies

- Their insurance offerings are limited

- Most of them are new companies that do not have enough experience.

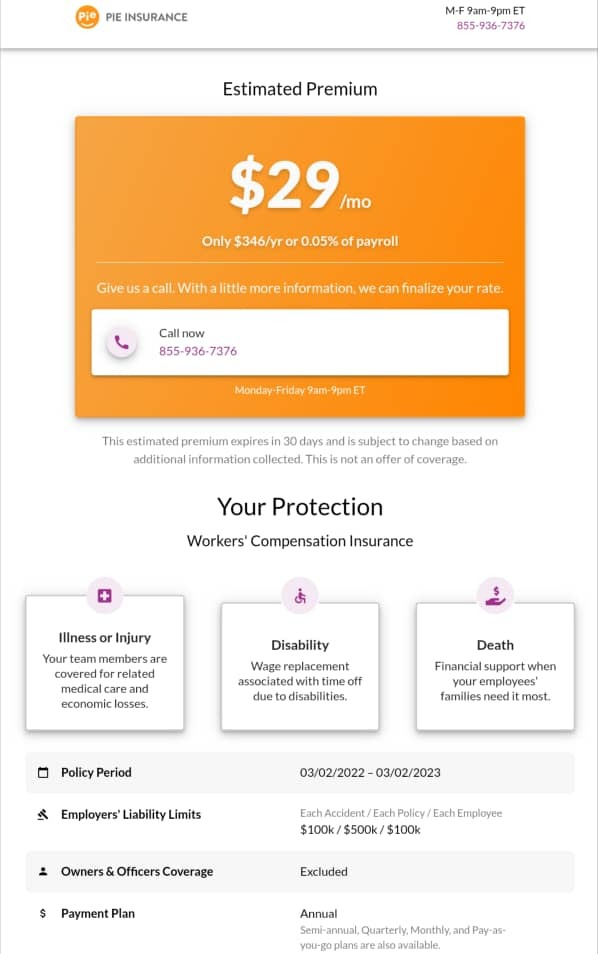

The following is a sample workers’ comp insurance quote obtained from Pie Insurance. The quote is for an accounting firm with 3 employees, $170,000 annual payroll, and $500,000 annual revenue.

Buy workers’ comp insurance in Pennsylvania state via the State Workers’ Insurance Fund (SWIF)

Because of their inexperience, most new enterprises have trouble getting workers’ compensation insurance. SWIF, as a state organization, is mandated to offer coverage to all enterprises, particularly those who are unable to receive coverage from private-sector insurers. This page contains general information regarding SWIF.

A SWIF application for workers’ compensation insurance is also accessible online.

How does workers’ comp function in Pennsylvania?

Workers’ compensation is an insurance policy that pays for medical treatment for job-related injuries and diseases. The insurance is monitored by the Pennsylvania Department of Labor and Industry.

Usually, the insurance policy covers diseases such as back traumas, carpal tunnel syndrome, black lung disease, and other diseases that occur due to one’s profession. The idea behind the policy is to help reduce the financial burdens of medical treatment on the injured or sick worker. That way, the worker can heal and return to work as soon as possible.

It also offers a portion of the employee’s salary when they cannot work. It covers payments for job retention, disability, death benefits, and burial expenses in severe cases.

Is workers’ compensation insurance required in Pennsylvania?

Pennsylvania follows other states in the US in terms of Worker’s Compensation. As such, almost all businesses in Pennsylvania must carry worker’s compensation so far they have an employee. Businesses that have no employees are often allowed to exempt themselves from coverage.

That means, if you have at least one person on your payroll, you must carry a workers’ compensation coverage in Pennsylvania. The specifics of the job are also irrelevant. The rule applies whether your employee is full-time, part-time, or seasonal.

Workers’ comp exemptions in Pennsylvania

Sole proprietors and partners are exempted from this policy coverage. So, if you run a company all by yourself as a sole proprietor or with a partner, you do not need to have a workers’ comp policy. However, if they wish, they can be covered by the policy. Learn more at the best workers comp insurance for sole proprietors.

Independent contractors are generally exempt from this coverage as well. Companies hiring independent contractors are not required to provide workers comp insurance to them. However, many of them do, especially in risky industries like trucking. Learn more at the best workers comp insurance for truckers. If trucking companies do not offer their drivers who are independent contractors workers comp coverage, they probably offer a cheaper alternative called occupational accident insurance. Learn more at the best occupational accident insurance companies for truckers. In general, independent contractors are encouraged to obtain the coverage for themselves since it is a very important and critical protection. Learn more at the best workers comp insurance for independent contractors.

On the other hand, corporate officers are always covered by the policy; however, they might be exempt or excluded if they wish.

Other workers that are generally exempted from the coverage include the following:

- Domestic workers

- Federal employees, railroad workers, etc., who already carry the policy

- Agricultural workers who work below 30 days monthly and earn less than $1,200

- Employees who do not want the policy due to religious beliefs

What benefits do workers comp insurance provide in Pennsylvania?

Workers’ comp in Pennsylvania offers many benefits to employees, including the following:

Medical Care

This is perhaps the essential part of the workers’ comp insurance. Medical care benefits cover all medical expenditures incurred due to the treatment of a work-related injury or illness.

These benefits include:

- Health-care services

- Surgical procedures

- Hospitalization, services, and supplies

- Medication

- Physical rehabilitation

Wage-Loss Compensation

When employees fall sick or get injured at work, they might not come to work for a while. That means their employer might not pay them for that period.

But then, with worker’s compensation, the employee gets compensation for wages lost while he is wounded or recovering. This coverage often includes reimbursement of up to two-thirds of 66.67% of their pay.

However, the specifics of the benefits that employees get are determined by the classification of their injury or disability as follows:

- Temporary Partial Disability

- Temporary Total Disability

- Permanent Partial Disability

- Permanent Total Disability

- Medicals

- Death

The various classes determine how long the employee gets his compensation. The state of Pennsylvania uses the no-fault system for its worker’s comp. Therefore, workers get their benefits regardless of who is to blame for the accident.

As of 2020, the maximum compensation that can be awarded under Pennsylvania workman’s compensation regulations was raised to $1,081 per week.

Specific-Loss Benefits

This benefit pays an employee if the injury or illness results in losing a body part. For instance, if the worker lost his fingers, sensory function, or other deformities. Specific loss can also be the inability to use body parts like the limbs. This type of compensation has a predetermined payment plan for the weeks of loss compensation.

Disfigurement Benefits

Sometimes accidents can lead to disfigurement for the employee. Under the laws of Pennsylvania, the insurance must pay for any lasting disfigurement caused by a working injury.

If the employee suffers from deformity of the head, face, or neck, such person must receive these benefits. These benefits are paid out at the beginning of the first week of injury and continue for 275 weeks. The Pennsylvania workers’ compensation regulations do not specify a monetary figure for such benefits.

Death Benefits

In a situation where an employee dies while working or as a result of a job-related injury or illness, his eligible dependents get death benefits.

Under the laws of Pennsylvania, the next of kin of the dead worker gets to receive the benefits. Such benefits will cover the funeral costs and a certain percentage of the worker’s salary.

The percentage of the salary the dependents will receive will depend on the person receiving the benefit.

What if I don’t have required workers’ compensation insurance in Pennsylvania?

As a business owner in Pennsylvania, the following are some possible penalties for not having worker’s compensation insurance:

- You risk losing your business license or certificate

- The state of Pennsylvania could prosecute you for criminal charges since worker’s compensation is required by law.

- Finally, your employees can sue you for work-related injuries or illnesses. This could lead to thousands of dollars in fines if you are found liable.

How much does workers’ compensation insurance cost in Pennsylvania?

In Pennsylvania, the estimated employer rate for workers’ compensation is $1.26 per $100 of your payroll. The amount you pay is determined by a variety of factors, including:

- Payroll

- Location in Pennsylvania state

- Total number of staff

- Industry and risk considerations

- Coverage limitations

- Previous claims history

Different insurance companies will provide with different quotes. Be sure to shop around with 3-4 companies or with a digital broker to compare several quotes to find the cheapest one for you.

Learn more about the cost of workers comp insurance cost and how to calculate it.

Who pays for workers’ compensation insurance in Pennsylvania?

The business covers the cost of workers’ comp insurance in Pennsylvania. In fact, like in many other states of the US, it is a crime for a business to request its employees to pay for their worker’s compensation.

This is where workers’ comp differs from other insurance and welfare packages like health insurance, social security, etc.

However, the good news is that the law covers employers who offer this insurance policy. So, your employers cannot sue you for accidents or illness no matter what happens.

How do I find cheap workers’ comp insurance in Pennsylvania?

Businesses with premiums of at least $10,000 may be eligible for an Experience Modifier. Experience Modifier is a tool insurance companies use in adjusting premium rates depending on the client’s loss history. Using the tool, businesses that have not filed any claims in the past may be eligible for a discount.

For more discounts you may also want to consider:

- Getting a high deductible plan

- Using a safety committee. If you form a safety committee, you may be entitled to a 5% discount that will last for five years.

- Consider paying with your credit card.

- And lastly, remember to always shop around with a few companies or a digital broker to compare several quotes to find the cheapest one for your company.

Learn more at the cheapest workers comp insurance companies.