Florida offers sunshine, miles of sandy beaches, and tax policies favorable to small business owners. However, you will need workers’ compensation insurance if you have more than four employees, or if you work in construction—in construction you’ll need workers’ compensation insurance if you have one employee. You have options on where to find workers’ compensation insurance.

- Buy workers comp insurance in Florida from traditional insurance companies

- Buy workers comp insurance in Florida from insuretech companies

- Buy workers compensation insurance in Florida from a digital broker

- Buy workers comp insurance in Florida from the state fund

- Self-insure workers comp in Florida

- Florida requirements for workers compensation insurance

- Who is exempt from workers comp insurance in Florida?

- What are the penalties for not having workers’ compensation insurance in Florida?

- How much does workers’ compensation insurance cost in Florida?

- Where can I find cheap workers’ compensation insurance in Florida?

- Can’t I just employ independent contractors in Florida?

Buy workers comp insurance in Florida from traditional insurance companies

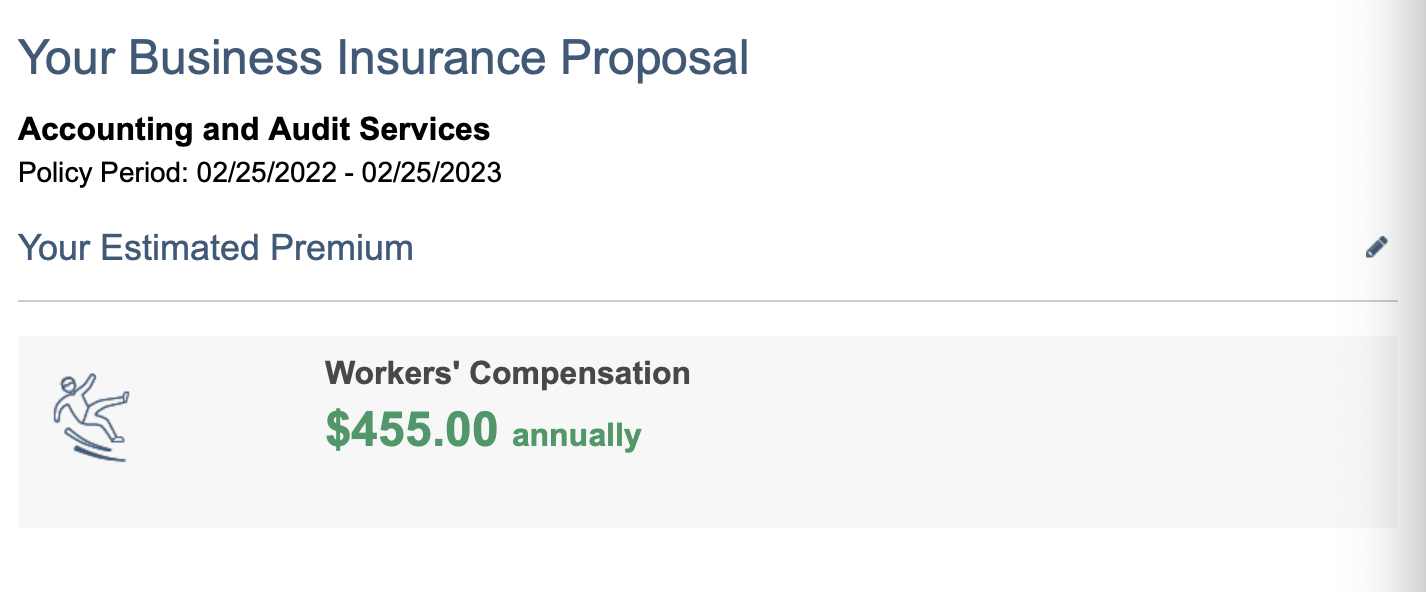

You can use a traditional insurance company to buy your workers comp insurance in Florida. Companies such as The Hartford, Employers, Travelers, Liberty Mutual, and Nationwide all offer workers’ compensation insurance for small businesses. Workers’ compensation insurance is pretty straightforward, so some companies offer online quotes. This one is from The Hartford for a small accounting firm in Florida with four employees and $350,000 in payroll.

Pros and Cons of buying workers comp insurance from traditional insurance companies

Pros:

- Usually offer many other types of business insurance, so you can get everything you need from one company

- Some offer pay-as-you-go coverage

- Some offer online quotes

- Established companies with excellent to superior financial strength

Cons:

- Most don’t allow you to buy insurance online: you have to call

- Rates and discounts vary by location

Buy workers comp insurance in Florida from insuretech companies

There are many insuretech companies these days, and they do everything from workers’ compensation to payroll to health insurance. Most of these companies can offer you a quote within minutes, and once you have a quote, you can buy the insurance, manage your policy and pay your bill online. Many insuretech companies for workers comp such as Pie, Cerity, and Biberk. Some of them offer other types of business insurance as well, but not all do.

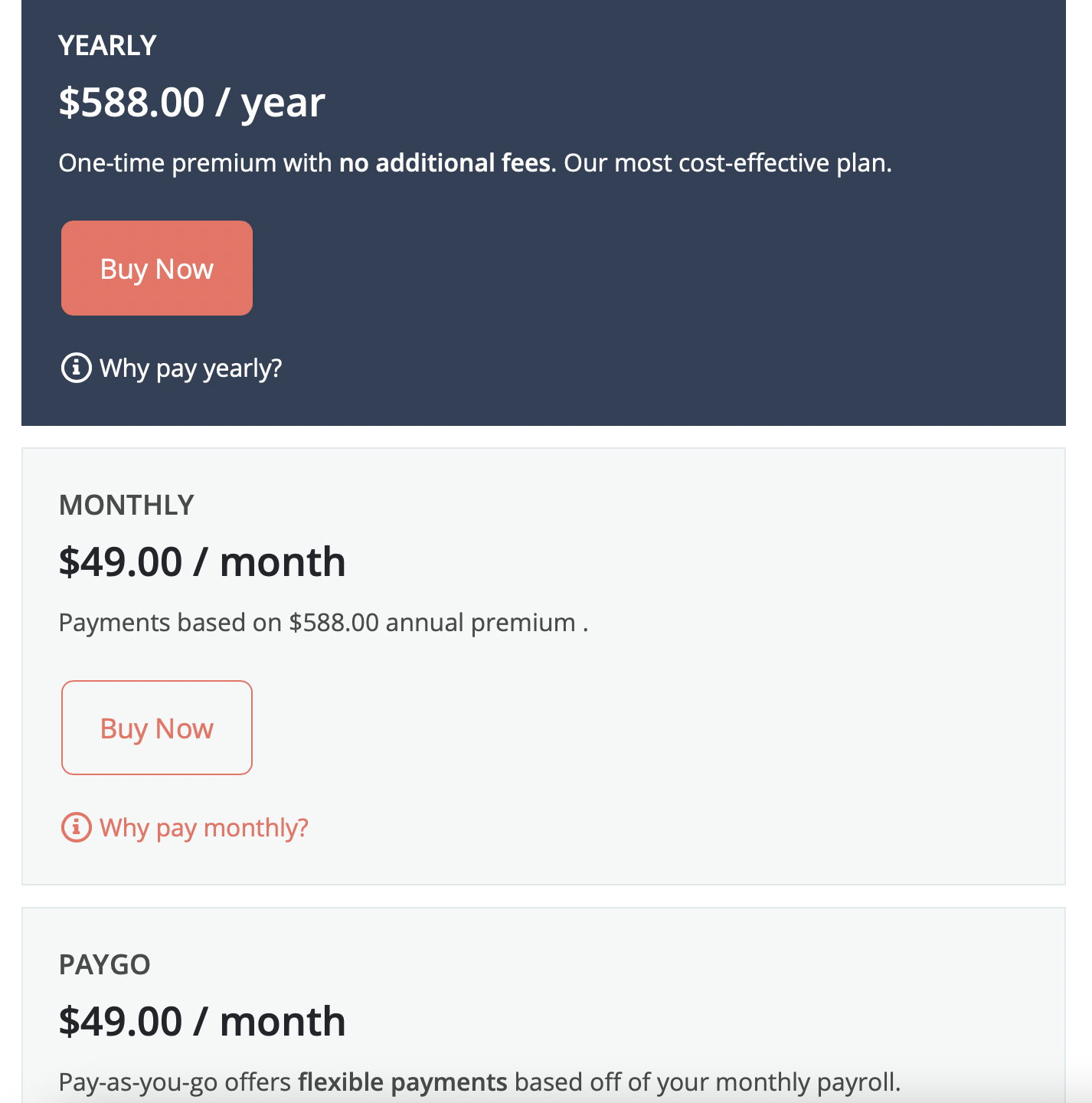

This is a quote from Cerity for an accounting firm in Florida with four employees and $350,000 worth of revenue.

Pros and Cons with buying insurance from insuretech companies

Pros:

- Most offer online quotes

- Buy insurance, manage your policy and pay your bill, all online

- Most claim to save you money

Cons:

- Many of these companies are less than five years old

- May not offer every type of business insurance you need

Buy workers compensation insurance in Florida from a digital broker

Companies like Policy Sweet, CoverWallet, and Commercialinsurance.net, and CoverHound are not insurance companies, but rather they partner with various insurance companies to help you get quotes online quickly. This allows you to compare quotes from several different companies, making comparison shopping quick and easy.

To mix things up, we went with CoverHound for a quote. We got these three quotes for our accounting business with four employees in Florida. You can try CoverWallet or CommercialInsurance.net. They all offer quote comparison online.

Pros and Cons of buying workers comp insurance in Florida from a digital broker

Pros

- Makes it easy to compare quotes

- Once you’ve purchased insurance, you can manage all your policies from one website

- Many offer multiple policies, although you won’t necessarily get all your insurance from the same company

Cons

- Quotes are not always instant: sometimes, they can take as long as 24 hours

- Only give you quotes from companies they are partnered with

Learn more at the best workers comp insurance companies in Florida.

Buy workers comp insurance in Florida from the state fund

Florida has a state fund for workers’ compensation insurance, which mostly fills the needs of companies that have been denied coverage from more traditional insurance companies. Florida has a Joint Underwriting Association that provides coverage.

Usually, getting insurance through the state fund is more expensive than getting it anywhere else: about 15% to 40% more. However, if you’ve been denied coverage through more traditional routes, the state fund may be your only option. Once you have insurance, you should work to increase employee safety, and eventually, you can get insurance through more traditional (and cheaper) avenues.

Self-insure workers comp in Florida

Companies with robust resources can apply for self-insurance. To be considered, you need a minimum net worth of $10 million dollars, and you’ll need a security deposit of $100,000. Self-insured companies must pay all out-of-pocket costs for their injured employees and assume all financial risk.

Florida requirements for workers compensation insurance

Florida has specific requirements regarding who needs workers’ compensation insurance. If you are in most industries and have four or more employees, you need workers’ compensation insurance. It doesn’t matter if they are full-time or part-time: to Florida, an employee is an employee and must be covered.

Construction industry: If you work in construction, you need workers comp if you have one or more employees. Since construction is a high-risk industry, all employees need to be covered. Here is a list of all the industries that Florida classifies as construction.

Contractors can have up to three corporate officers exempt from coverage if they can prove they owe at least 10% of the business.

Agricultural industry: 6 or more regular employees or 12 or more seasonal employees who work more than a total of 30 days will need to be covered under a workers’ compensation policy.

Who is exempt from workers comp insurance in Florida?

Below are those that are exempt from workers comp insurance in Florida:

- Sole proprietors or partners in partnerships in Florida are exempt from having workers comp insurance in Florida. However, they can choose to have workers comp coverage. Learn more at the best workers comp insurance for sole proprietors.

- Independent contractors are also exempt from workers comp insurance in Florida. However, they can choose to get the coverage to protect themselves if they want to. Learn more at the best workers comp insurance for independent contractors.

- Corporate officers and LLC owners can choose to exempt themselves from workers’ compensation coverage by filing for an exemption with the state’s Division of Workers’ Compensation.

- Lastly, non-construction companies with less than 4 employees (both full-time and part-time) can choose not to have workers comp insurance coverage. However, it is not advisable.

Learn more at workers comp insurance exemptions in Florida.

What are the penalties for not having workers’ compensation insurance in Florida?

If you skip workers’ compensation insurance, the fine is double what you would have paid in workers comp insurance in the first place for as long you went without a policy in the last two years. In addition, there’s a fee of $5,000 for every employee you incorrectly classified as an independent contractor. You can also get a stop-work order, which means all of your business will grind to a halt while you go secure workers’ comp insurance.

In addition, you may be subject to civil lawsuits filed by employees who got injured or became sick while working for you. Then you will have medical payments, lost wages, court costs, and attorney fees, both your attorney and the employee’s attorney if they win the case. All of this can add up to bankruptcy.

How much does workers’ compensation insurance cost in Florida?

Workers’ compensation insurance in Florida is actually fairly reasonable, at $1.24 per $100 in payroll. To calculate how much you’ll pay in workers’ comp insurance, use this formula:

Classification rate X Experience modification rate X (Payroll/100) = premium

Most insurance companies use this formula to calculate your business’s workers comp insurance. However, it doesn’t mean they all offer the same rates. They all have different underwriting criteria and fees, so they will give you different quotes. Be sure to shop around with a few companies or a digital brokers to compare several quotes to find the cheapest one for your company.

You can read more in our article: How much is workers’ compensation insurance?

Where can I find cheap workers’ compensation insurance in Florida?

How much you pay for workers’ compensation insurance depends on several factors:

- Annual payroll

- Industry

- Claims history

Every industry is boiled down to a classification code. Each code is four digits long. There’s a list of all classification codes here. The codes reflect the level of risk in an industry. For example, roofers pay about $19 for every $100 in payroll, whereas office workers pay about 0.12 per $100.

Make sure you classify your workers correctly. Being just one number off can wind up costing you hundreds of dollars.

The experience classification code is your claims history. It’s graded from about 0.75 to 1.25—the higher the number, the more you’ll pay. The good news is that your experience modification rate tends to go down over time, so you’ll pay less in insurance (provided you don’t file any claims).

There is something called pay-as-you-go workers’ compensation insurance, which might save you money because it’s based on actual payroll as opposed to projections for the year. So, if you’re down a few employees, you’ll pay less. Some payroll companies will subtract workers’ comp insurance from payroll.

Last but not least, after doing everything correctly, the last yet most important thing to do to ensure you get the cheapest workers comp insurance for your business is to compare several quotes so that you can choose the cheapest one for you. Different insurance companies will provide you with different quotes, so be sure to shop around.

Can’t I just employ independent contractors in Florida?

You wouldn’t be the first employer to try to classify your employees as independent contractors. However, as listed above, the fine for doing so is $5,000 per employee if you get caught. The IRS has three general factors which determine whether someone is or is not an employee:

- Behavioral: Does the company have the right to control what the workers does and how the worker does his or her job?

- Financial: Are the business aspects of the worker’s job controlled by the company (basically, do you provide most or all of the workers’ income)?

- Type of relationship: Are benefits provided? Is the relationship likely to continue?

In addition to workers’ compensation fines, the IRS will also hold you liable for employment taxes.

If you are an independent contractor in Florida, you know that the company that you are contracting with doesn’t provide you with workers comp insurance, you have to get workers comp insurance for yourself. Learn more at the best workers comp insurance for independent contractors.

What does workers comp insurance cover in Florida?

Florida workers compensation covers your employees for the following:

- 100% medical bills

- Wage replacement benefits

- Disability benefits

- Rehabilitation benefits (if they can no longer do the job they were hired to do, retraining is available)

- Death benefits

Employees can still make a claim for a larger settlement benefit, but workers compensation insurance protects the employer as well. There is a two-year statute of limitations employees must file lawsuits under, but there are some exceptions.

Last thoughts

Workers’ compensation insurance is expensive but necessary. Provide a safe work environment and treat your employees with respect and you will save money on insurance.