The vast majority of small businesses in California must carry workers’ compensation insurance. This coverage, often referred to as workers’ comp, provides benefits to employees if they become injured or ill because of job related reasons.

If you need to buy workers comp insurance in California, this is our comprehensive guide providing everything you need to know.

- How does workers’ comp function in California?

- Is workers’ compensation insurance required in California?

- What benefits does workers comp insurance provide in California?

- How can I purchase workers’ comp in California?

- What if I don’t have required workers’ compensation insurance in California?

- What do employers need to know about California workers’ comp law?

- How are workers’ compensation claims made in California?

- How much does workers comp insurance cost in California?

- How do I find cheap workers’ comp insurance in California?

How does workers’ comp function in California?

Workers’ compensation insurance will help your employees if they become injured or ill at work. The ultimate goal of the program is to have people return to work. However, if an incident causes severe harm, it pays for job retraining, disability benefits, death benefits, and funeral costs. Workers’ compensation premium costs (in part) and benefits (in full) are based on an employee’s average weekly wage. The actual amount varies, based on the type of benefit.

Is workers’ compensation insurance required in California?

California businesses with at least one part- or full-time employee are required to purchase workers’ comp. California law states that an employee as anyone working for a company, whether the arrangement is:

- Expressed or implied

- Oral or written

- For lawful or unlawful unemployment.

The only people who aren’t required to be covered by workers’ compensation insurance in California are:

- Sole proprietors, although they can choose to get coverage if they want it. Learn more at the best workers comp insurance for sole proprietors.

- Executive officers and directors who own the business

- Limited liability company (LLC) members who don’t work in the business.

Business owners aren’t required to cover independent contractors, as well. To find out if a worker is an employee or independent contractor, use the ABC test that’s a part of California Assembly Bill 5:

A worker is considered an employee and not an independent contractor, unless the hiring entity meets all three conditions of the ABC test:

- The person is independent of the hiring organization when performing their work, both under the work contract and in fact.

- The person performs work that is done outside of the hiring entity’s business.

- The person regularly does work in an independently established trade, occupation, or business that is the same as the work being requested and performed for the business.

Learn more at the best workers comp insurance for independent contractors.

What benefits does workers comp insurance provide in California?

Workers comp insurance provides the following benefits in California:

- Payments to cover medical treatments required because of the injury or illness.

- Temporary disability payments if an injury prevents an employee from returning to work while recovering.

- Permanent disability payments if the injury or illness is one the employee can’t recover from. Depending on the type of injury or illness, an employee may qualify for a life pension payment.

- Supplemental job displacement vouchers, which help cover the costs to retrain the employee if they’re able to return to work but can no longer handle their normal job responsibilities.

- Death benefits for immediate family members, usually a spouse and dependent children, if a worker loses their life because of an on the job injury or illness.

California employers also benefit from having workers’ comp insurance. Employees are not able to sue you over work related injuries or illnesses, even if you’re negligent, if you have the coverage.

How can I purchase workers’ comp in California?

If you need workers’ compensation insurance, California businesses can buy coverage from:

- An established insurance company like Employers, Chubb, or The Hartford

- Pros: Dependable, good service, financially solid

- Cons: Can be more expensive than other types of insurance providers

The Hartford will not provide a quote for this coverage online.

- An insuretech startup such as Pie, Cerity, or Foresight

- Pros: Relatively low cost and easy to get coverage. Easy to get quotes and buy policy online.

- Cons: May not be as responsive or financially sound as more established companies

Pie does not collect the information it would take to generate a quote and only provides a very rough estimate with a request to call them.

- A digital insurance broker like CoverWallet or Simply Business or Policy Sweet

- Pros: Easy to compare costs and coverages from multiple insurers all in one place

- Cons: Brokers may not represent all possible insurers

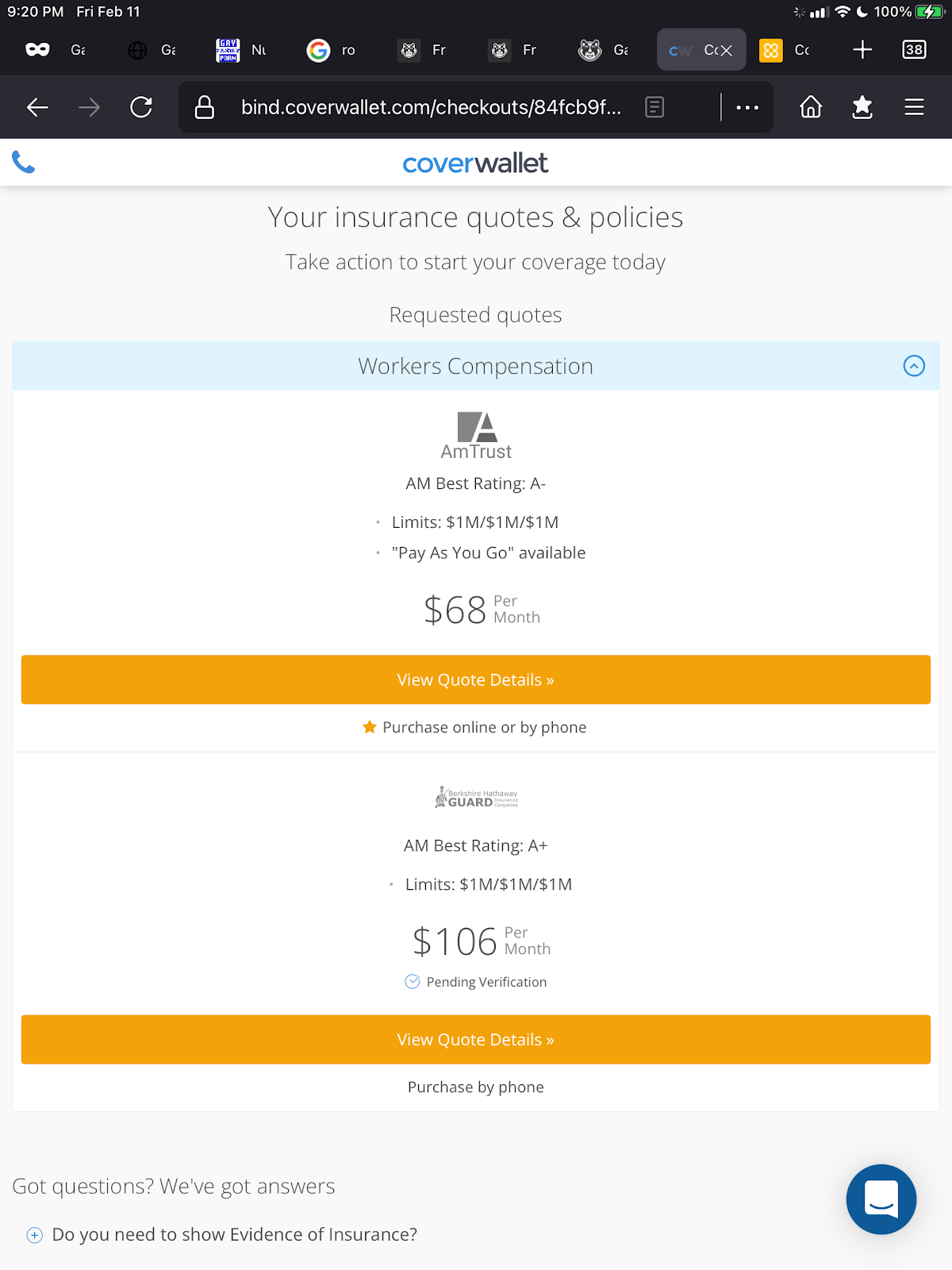

Here is a sample workers’ comp quote for a small California accounting company from CoverWallet:

- The California state fund, which offers workers’ comp through a state agency

- Pros: Companies that can’t get insurance elsewhere can usually get it through the state fund

- Cons: Insurance from the state fund is typically more expensive than through other providers.

Regardless who you want to buy workers comp insurance from, be sure to shop around with a few companies to compare several quotes before making your final decision:

Learn more at the best workers comp insurance companies in California

What if I don’t have required workers’ compensation insurance in California?

If you don’t have coverage, you are in violation of the California Labor Code. You could face a:

- $10,000 fine

- One year prison sentence

- $100,000 fine.

The consequences of not having required coverage are severe.

What do employers need to know about California workers’ comp law?

The three key things your business must do to comply with the law are:

- Secure adequate workers’ comp insurance for your business and employees.

- Give a workers’ compensation pamphlet or brochure to each new worker.

- Post a workers’ comp notice to employees poster in your business locations.

Who pays for workers’ compensation insurance in California?

The business pays for coverage. California does not allow business owners to require employees to pay for or offset the cost. Employees should never see a deduction for coverage on their paychecks like they do for health insurance coverage, Social Security, or other benefits. In return for paying for this coverage, in most cases, your employees can’t sue you if they become injured or ill from work.

How are workers’ comp disputes handled in California?

Disputes related to workers’ compensation claims can happen for many reasons. An employer may dispute whether an injury actually happened at work. An employee may have issues with their workers’ compensation benefits.

Not every workers’ compensation claim ends up being disputed or going to trial. In many cases, both parties may agree on a settlement beforehand. Depending on the specific circumstances, most employees can choose from two types of workers’ comp settlements.

1. Stipulated findings and award

Injured workers may choose a stipulated findings and award settlement if they need ongoing medical care because of a permanent disability. The employer pays for the ongoing medical treatments in this type of settlement.

2. Compromise and release

A compromise and release settlement allows an injured worker to accept a one time payment. Accepting the lump sum resolves the workers’ compensation claim and it cannot be revisited again.

How are workers’ compensation claims made in California?

When business owners receive word of a work related injury or illness in California, there are specific steps they must take to file a workers’ compensation claim.

Your employee must report and file a claim within one year of the date of a work related injury or illness. Within one business day after receiving a report of an injury or illness, you are required by California law to provide your employee with a workers’ compensation claim form. After they complete and submit the form to you, you have one business day to:

- Provide a copy of the completed claim form to your employee.

- Forward the claim form and your employee’s report of injury or occupational illness to your insurance company or claims administrator. You can find information about how to do this on your insurer’s website.

- Authorize up to $10,000 in medical treatment.

Depending on the type of illness or injury, you may also need to authorize and assign light duty work to your employee. Once these steps are completed, your insurer will guide you through the rest of the claims and resolution processes.

How much does workers comp insurance cost in California?

Workers comp insurance cost varies depending on the industries, the class codes, the company’s payroll, location, and claim history. The average cost of California workers compensation insurance is $1.56 per $100 of payroll, which is higher than national average.

Some examples of California workers comp insurance costs for different class codes:

- Clerical: $.040

- Restaurant/Bar staff: $4.34

- Plumbing: $7.01

- Masonry: $14.63

- Laborer: $33.57

Clerical is the cheapest classification, and laborers are the most expensive, at $33.57. So if you are employees many laborers at your company, workers compensation insurance can become very expensive, almost 1/3 of your total payroll. Be sure to shop around with a few companies or a digital broker like CoverWallet so that you can compare several quotes to decide on the cheapest one for your company.

Learn more at how much workers comp insurance costs

How do I find cheap workers’ comp insurance in California?

Rates for this coverage are set by California law. However, different insurers may charge different fees for supplying this coverage. It’s worth shopping around to find the best premium price from an insurer that will offer you good claims service and support when you need it.

Learn more at the cheapest workers comp insurance companies