Work-related accidents and incidents happen all the time. In a litigious state like New York, it’s essential for small business owners to protect themselves against lawsuits and the other risks they face. The best protection they can get is complete business insurance coverage. Not having the right types of insurance — and enough of each type — can be the same as not having it at all, leaving businesses with inadequate protection against different kinds of losses.

We researched more than 20 insurance companies, as well as several brokers and online insurance marketplaces. I reviewed the types of coverage they offer in New York state, the industries they serve, their ratings for financial stability, and customer satisfaction scores. That allowed us to come up with my list of the top 7 insurers for different coverages in New York. Following the list, I also provide all the information you need to get complete protection for your New York small business.

- Top 7 small business insurance companies in New York for different coverages

- Why do I need business insurance in New York?

- What insurance do I need for my New York small business?

- What is the average cost of small business insurance in New York?

- How can I find cheap business insurance in New York?

Top 7 small business insurance companies in New York

Here are my choices for the top business insurers in New York and the coverages they are best for.

- CoverWallet: Best for comparing several quotes online

- Liberty Mutual: Best for business owners policies (BOPs)

- Cerity: Best for workers’ comp coverage

- The Hartford: Best for general liability coverage

- Hiscox: Best for commercial property and liability coverage

- Embroker: Best for cyber insurance

- Progressive: Best provider of commercial auto insurance

CoverWallet: Best for comparing several quotes online

CoverWallet makes it easy to compare insurance quotes from several providers within minutes, all on one screen.

How is CoverWallet able to do this?

CoverWallet is a cutting-edge insurance provider. The firm has developed its proprietary state-of-the-art platform, based on its own algorithms, to ensure it can connect small businesses with the professional liability and other business insurance they need at a fair price.

The firm’s experts have used their extensive experience to make sure you only have to input the information needed to generate quick and accurate quotes. The entire process should take less than ten minutes.

You can feel confident knowing that CoverWallet is a part of Aon, an established company that provides advice to businesses on things like risk, health, and retirement.

Once you get your quote, CoverWallet makes it easy to purchase professional liability coverage — or a complete business insurance package — online or through an agent. When you get your insurance through CoverWallet, it’s simple to manage your coverage online, including downloading a certificate of insurance, filing a claim, renewing your policy, and more.

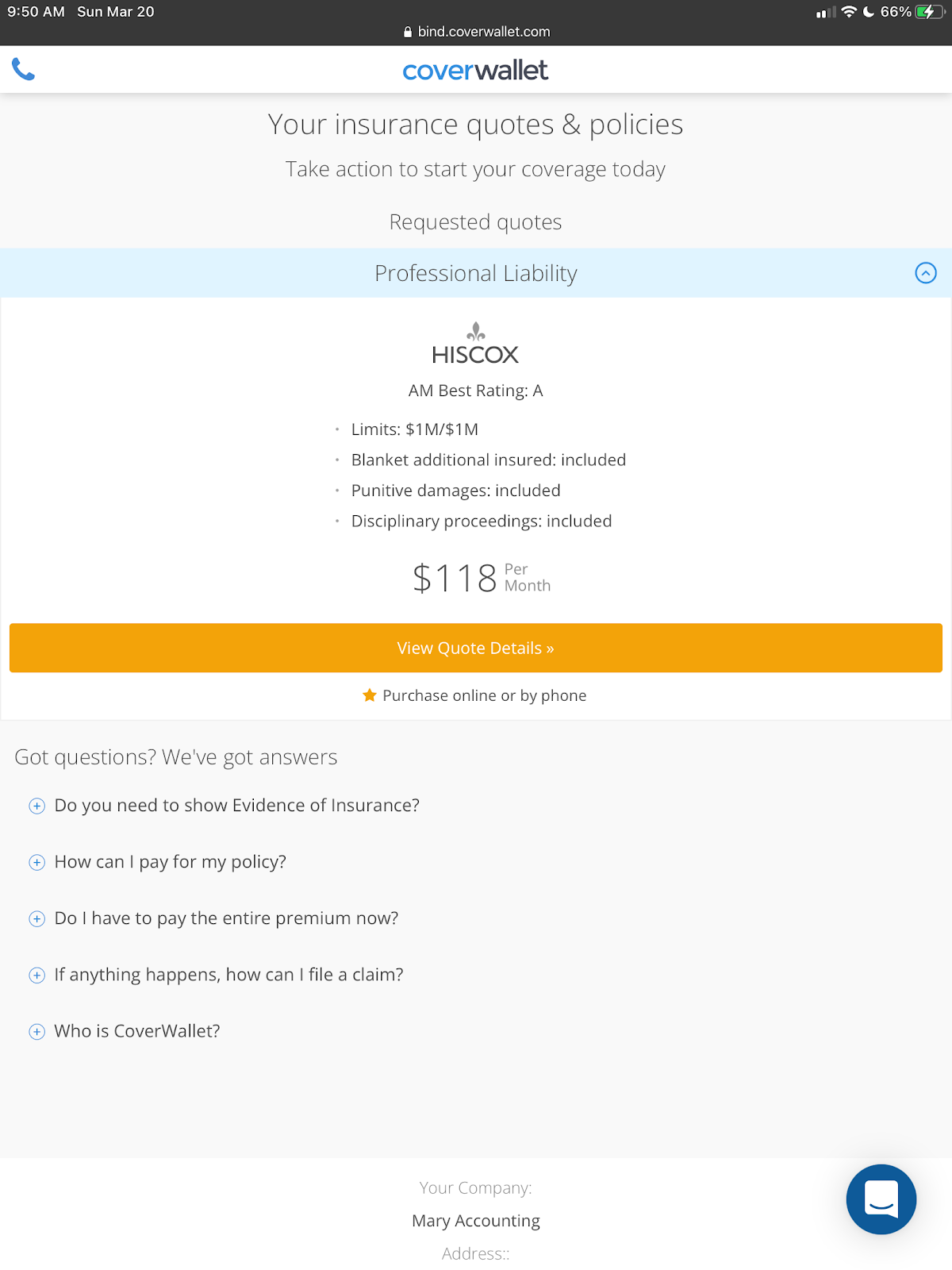

Here is a simple professional liability insurance quote for a small accounting firm.

Liberty Mutual: Best for business owners policies (BOPs)

Small businesses change over time, and their insurance needs evolve. Liberty Mutual is uniquely able to serve their changing insurance needs. In addition to core business owner policy protection, they offer one of the most comprehensive ranges of business coverage of any insurer. They can customize policies to meet the needs of virtually any business. In addition to this, their experts are always looking ahead to identify new business risks and find efficient ways to cover them.

In addition to its flexibility, Liberty Mutual is a Fortune 100 company and one of the largest insurance firms in the United States and across the globe. You can feel confident knowing that Liberty Mutual will have the funds to cover any claim you make.

Liberty Mutual is also known for its workplace safety programs. By implementing them, you may be able to save on your BOP and other insurance costs over time.

Liberty Mutual makes it easy to find an agent on its website that you can purchase coverage through. Or you can submit your contact information and an agent will get back to you.

Cerity: Best for workers’ comp coverage

Cerity is our top workers’ compensation provider for New York businesses because it specializes in the coverage. It’s a relatively low-cost provider, yet delivers a high level of service. Policies start as low as $25 per month, and the company has fewer fees than most insurers. Cerity makes it fast and easy to get a quote online.

Cerity isn’t low-cost because it cuts corners. It actually uses artificial intelligence to up its efficiency. However, everything at Cerity isn’t technology based. When you require help, you will have access to a team of licensed policy and claims experts. You can rest assured knowing Cerity has been in business for more than a century and is rated highly by their clients.

It is relatively fast and simple to get a quote from as long as you have your federal employer identification number handy.

The Hartford: Best for general liability coverage

The Hartford is one of America’s oldest companies and a solid, stable, and ethical insurer. The company is known for its general liability insurance and other core coverages. You can get a free quote on The Hartford’s website or through an agent that represents the company’s products. If you get a quote online, insurance experts are available to help if you have any questions.

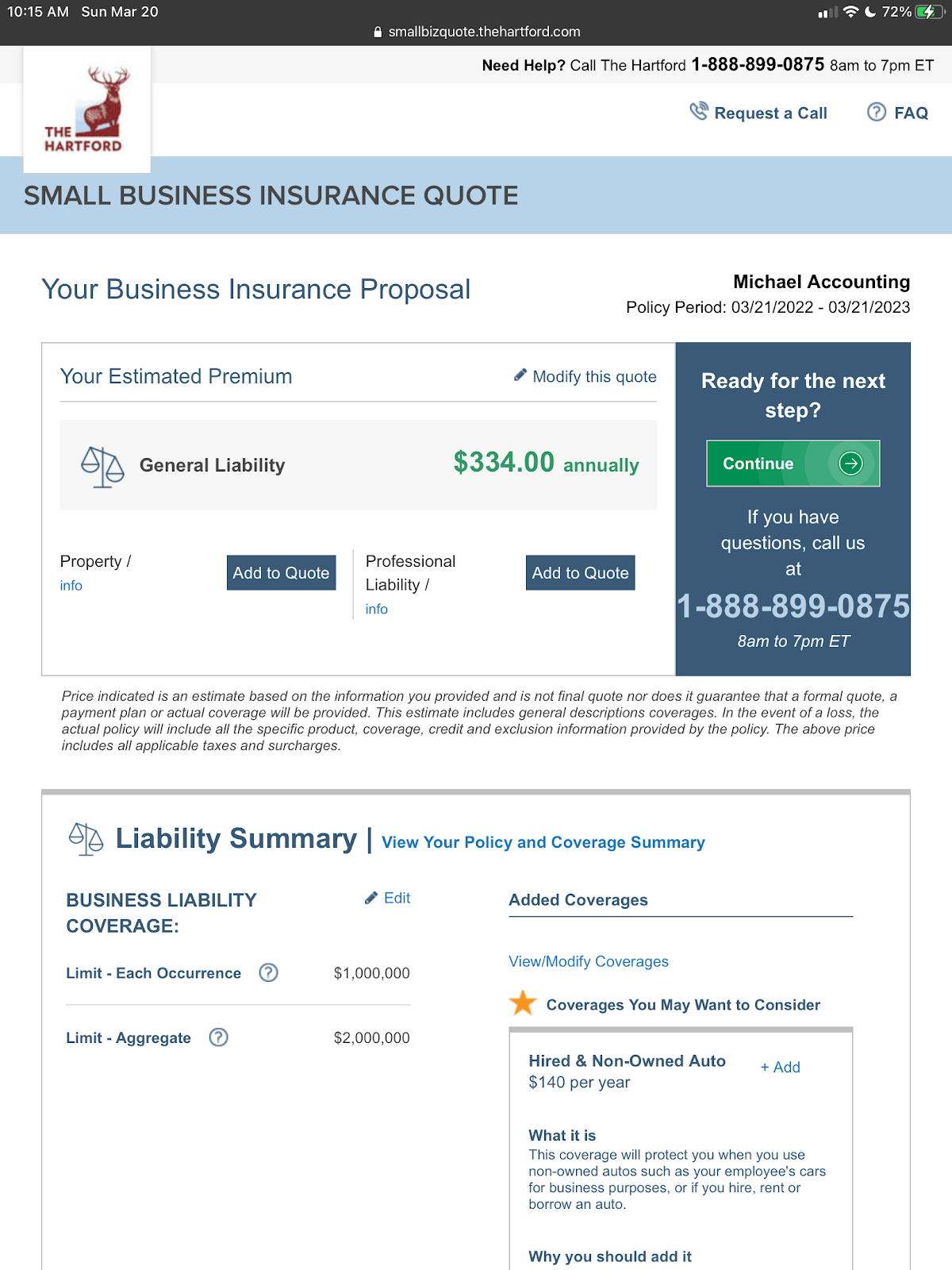

Here is a sample general liability insurance quote for a small accounting company from The Hartford.

Hiscox: Best for commercial property and liability coverage

Hiscox is a leading insurer that specializes in small business insurance. It offers a complete array of business coverages, but is known for the core property and liability insurance protection every business needs.

Hiscox makes it easy to purchase business property, liability, and other types of insurance online. You can also speak with experienced business insurance experts who can help you customize your coverage to meet your unique company needs. Hiscox also offers top tier service and provides fast quotes, instant coverage, and quick claims processing.

If you choose Hiscox for your business coverage, you can rest assured knowing you’re entrusting your organization to a firm that’s been in operation since 1901. More than 400,000 companies choose Hiscox for their coverage.

Embroker: Best for cyber insurance

Some of the biggest risks faced by small businesses today are getting hacked, having private customer and business data becoming compromised, or being the victim of a ransomware attack. That’s why it’s important for business owners to secure cyber insurance, and Embroker is a leader in this type of coverage.

Embroker is an online business insurance marketplace that makes it easy for you to compare quotes from multiple insurance companies for cyber insurance and other business coverages and select the best deal. You simply answer some questions about your business and coverage needs online. Within a few minutes, you’ll have quotes for cyber and the other types of insurance you need from several different insurance companies. If you require help selecting a policy, you can connect with a licensed insurance expert over the phone. Embroker is licensed to sell insurance in New York.

Progressive: Best provider of commercial auto insurance

Progressive may seem like a less-than-serious company because of its ongoing series of commercials featuring Flo.

The truth: It’s a reputable company that’s been offering auto insurance for more than 80 years and business-related coverage for a half century. Progressive provides not just a complete range of commercial auto insurance products, it can also supply all the coverage your business needs. The company is known for its flexibility, great rates, and top-tier service.

Progressive offers the following types of commercial vehicle insurance for businesses in New York:

- Commercial auto and truck – Learn more at the best commercial truck insurance companies

- Tow truck – Learn more at tow truck insurance cost and the best tow truck insurance companies

- Dump truck – Learn more at dump truck insurance cost and the best dump truck insurance companies

- Semi truck – Learn more at semi truck insurance cost and the best semi truck insurance companies

- Log truck – Learn more at the best log truck insurance companies

Progressive is known for its discounts, which could help you save on your commercial vehicle insurance and all your business coverage.

What is business insurance?

Business insurance, also known as commercial insurance, helps protect business owners from unexpected losses.

There are many types of business insurance options to help cover your operation for property damage, legal liability, and employee-related risks.

What is business insurance for?

Business insurance can help you gain control over your company’s risks, which are considerable. It provides you with financial protection against losses that occur while conducting business. When you have business insurance coverage, your insurer helps pay the costs of covered losses up to the limits of your policy. Without coverage, you might have to pay out of pocket, which can easily bankrupt your business.

Why do I need business insurance in New York?

The purpose of the insurance is to help protect your New York based company from common risks most businesses face, along with industry specific ones. It can protect the financial assets of your company, it’s physical property, employees, and intellectual property from:

- Lawsuits

- Property damage

- Theft

- Vandalism

- Loss of income

- Employee injuries and illnesses

- And more.

What insurance do I need for my New York small business?

The coverage you need for your New York based company depends on the type of business and the specific risks faced by it. However, almost all businesses need general liability insurance, which protects you in case someone who is not an employee is injured at your place of business or you cause damage to someone else’s property while conducting business.

Other types of small business insurance coverage that you may need include:

- Workers’ compensation insurance which New York state requires if you have employees

- General liability insurance, the most essential coverage for small businesses in New York especially if you business operates out of a physical location

- Commercial auto insurance if you own or use vehicles for business reasons

- Professional liability, also known as errors and omissions (E&O) insurance, for people who provide professional services including architects, accountants, consultants, and lawyers

- Business Owners Policy (BOP), a bundled policy for small businesses with revenue less than $10M or 100 employees that combine general liability, commercial property, and possibly business income interruption coverages into one policy.

Workers’ compensation coverage: Why do small businesses in New York need this coverage?

If your business has employees, New York, with very few exceptions, will require you to carry workers’ compensation coverage. This insurance provides benefits to your employees to help them recover from work-related injuries or illnesses. Some examples of these include:

- A clerk at your store is stocking shelves, slips off a ladder and breaks her leg. This leaves her unable to do her job.

- An administrative assistant at your business has been working on a computer while sitting on an cheap old chair and comes down with carpal tunnel syndrome. She is no longer able to do her normal work because she’s in pain.

- A carpenter at your cabinet factory has been breathing in saw dust and chemical odors for years and comes down with lung disease. His doctor will not allow him to return to work.

Workers’ comp also pays funeral expenses and death benefits to immediate family members should an employee pass away because of a job related incident.

Learn more about workers comp insurance at the best workers comp insurance companies in New York and the cheapest workers comp insurance companies.

General liability insurance in New York

General liability insurance, also called commercial liability, helps protect your business from claims of bodily injury and property damage that happen in your workplace or while your employees are doing their jobs. This includes things like customer injuries that result from a slip and fall in your office or workplace or client property damage that occurs because of a worker incident in a client’s home.

General liability insurance isn’t required by state laws in New York for most small businesses. However, it is probably the most popular coverage that small businesses carry. Learn more at the best general liability insurance in New York and the cheapest general liability insurance companies.

Commercial auto insurance in New York

Commercial auto insurance pays for damage to vehicles and the cost of medical care if you or an employee is involved in an accident while driving for work related reasons. It is required by New York state law to have commercial auto insurance for your business. Personal auto insurance doesn’t cover you and your vehicle when you drive for work.

If you don’t have proper business vehicle insurance, when you are involved in an accident as you are driving for work, your personal auto insurance company will refuse the claim and might drop you from their coverage as well. Learn about the differences between commercial auto insurance and personal auto insurance and why small businesses need to have commercial auto insurance coverage.

Commercial auto insurance is usually a bit more expensive than personal auto insurance, but without it, you may have to pay out of pocket a lot more. Learn more at the best commercial auto insurance in New York and how to find cheap commercial auto insurance.

Professional liability insurance in New York

Professional liability insurance covers you and the people who work for you if you’re ever sued by a client for giving them bad advice or not performing services to their satisfaction.

If you are in the business of providing customers with advice and services, you might need professional liability insurance, also called errors and omissions (E&O) in the real estate, insurance, or finance industries, or malpractice insurance in the healthcare and legal industries.

Professional liability coverage details are different in different industries. Use our guides specific to each industry and specialty to find the coverage that you need:

- Lawyers – Top 5 Providers of Legal Malpractice Insurance & How Much It Costs

- Accountants & CPAs – Professional Liability Insurance (E&O) for Accountants and CPAs

- Tax preparers – The Best E&O Insurance for Tax Preparers

- Doctors – The 5 Best Providers of Medical Malpractice Insurance

- Consultants – Professional Liability Insurance (E&O) for Consultants

- Real estate agents – Top 5 Providers of Real Estate E&O Insurance & Costs

- Insurance agents – E&O Insurance for Insurance Agents: Cost and Top 5 Providers

- Engineers – Top 5 Providers of Professional Liability Insurance for Architects and Engineers

- Marketing and advertising services

- Psychologists – Top 4 Providers of Malpractice Insurance for Psychologists and Counselors

- Nurses – The Best 4 Providers of Nursing Malpractice Insurance

- Nurse practitioners: The Best Malpractice Insurance for Nurse Practitioners

- Dentists – Top 5 Providers of Dental Malpractice Insurance

- Dental hygienists – The Best Malpractice Insurance for Dental Hygienists

- Physician’s assistants – The Best Malpractice Insurance for Physician’s Assistants

- Physical Therapists – The 6 Best Malpractice Insurance Providers for Physical Therapists

- Chiropractors – 4 Best Choices for Cheap Chiropractic Malpractice Insurance

- Pharmacists – The Best Malpractice Insurance for Pharmacists and Costs

- Social workers – The Best Malpractice Insurance for Social Workers

Business owners policy (BOP)

A business owners policy combines multiple types of insurance in a single policy. Most BOPs include commercial general liability and property coverage, as well as small amounts of coverage for endorsements such as inland marine or umbrella coverage. By combining these coverages into a single policy, business owners are usually able to save money on their total premiums.

It’s important to know that while a BOP includes several types of coverage, it doesn’t protect against all the risks your business may face.

What does a Business Owners Policy cover in New York?

A Business Owners Policy (BOP) will help protect your business property, income, and financial assets. A BOP typically includes three types of coverage:

Business property coverage:

This coverage protects the buildings your business operates out of, whether you own or rent them and the equipment used to run your company. This includes your:

- Physical location

- Tools

- Inventory

- Supplies

- Computers

- And more.

General liability insurance

General liability covers legal claims against your business related to:

- Bodily injury

- Property damage

- Reputational harm, such as libel and slander.

Business income insurance

This coverage is often referred to as business interruption coverage, helps replace lost income if you can’t operate your business because of property damage that’s covered by your business policy. This includes damage from fire, wind, weather events, and burglaries. Learn more at the best business income insurance companies.

Depending on the specific needs of your business, you can work with your insurance agent or company rep to figure out what other coverages you may need.

In addition to these foundational types of business coverage, there are many other types of insurance that New York business owners may need to purchase to cover risks.

- Product liability, which covers you if a product you manufacture or sell is faulty and doesn’t perform as intended and you’re sued because of it. Learn more at the best product liability insurance companies.

- Cyber insurance, which helps pay expenses related to the theft or loss of critical customer, employee, or business information. Learn more at the best cyber insurance companies and the best data breach insurance companies.

- Directors and officers, or D&O insurance, which will help pay legal expenses and damages if a director or officer at your company is sued because of a business-related decision. Learn more at the best D&O insurance companies.

- Inland marine insurance if you transport inventory or other things for commercial purposes.

What does small business insurance NOT cover in New York?

While small business insurance covers your business for legitimate losses, it doesn’t protect against damages caused by negligence or fraud, whether committed by you or someone who works for you.

It also won’t cover workers’ comp claims if you lie about the nature of your business, misclassify your employees, or under report payroll to reduce premiums.

Most policies, especially commercial property, also don’t protect against losses related to natural disasters like floods, earthquakes, or hurricanes, unless coverage is added to for these events.

For companies that have many policies or several coverages combined in a BOP, coverage limits aren’t fungible. That means that if a business suffers a loss for which they have too little coverage, a business owner can’t use coverage from other parts of their policy unless their insurer explicitly allows it.

On top of this, certain types of insurance have things that aren’t covered that are unique to them. For example, even though workers’ comp protects employees if they’re injured because of a workplace accident, policies typically don’t cover injuries that result from horseplay. Similarly, commercial vehicle insurance doesn’t pay for damages that relate to accidents that happen when a business vehicle is used for non-business reasons, such as running a personal errand.

Business interruption insurance is another example of a coverage that has limits. It will help replace lost income for a business when it’s unable to operate for reasons covered by their insurance. However, it may only replace that income within limits for a defined period of time.

What coverages should New York businesses with employees get?

As covered earlier in this article, New York requires businesses with employees to carry workers’ compensation insurance.

You may also want to consider getting employment practices liability insurance. It helps protect your business if a current or former employee makes an employment-related claim. For example, if you are sued for wrongful termination or discrimination, employment practices liability insurance can help cover your legal costs.

Also, if you or your employees drive their own or company owned vehicles for work, it’s a smart idea to get commercial auto insurance. That’s because personal auto insurance does not cover accidents that take place while conducting business. If you have a work-related incident, you would have to pay for any damage or injuries that happen to you and your vehicle and anyone else impacted by the accident.

How can I prevent business losses in New York?

Many business insurers offer programs that can help you reduce business related risks. This includes doing things like eliminating workplace hazards and encouraging safe work practices. By doing these things, you could save on your business insurance costs. Check with your business insurer to find out whether they offer workplace safety programs.

Is there an easy way to get business insurance coverage in New York?

The simplest way to get small business insurance coverage is through a business owners policy (BOP), which typically bundles together business property and liability coverage. A BOP makes it easy to add on additional types of coverage beyond these.

The types and amount of coverage you need depend on a number of factors including:

- Your industry

- The size of your business

- It’s location or locations in New York

- The number of employees

- And more.

At a minimum, you probably want to have liability and property coverage through a BOP. And if you have employees, the state of New York will likely require you to get workers’ compensation insurance. When you apply for coverage online, it’s likely that the insurer will suggest the additional coverages you should get. An experienced business insurance agent or company rep can recommend coverages to you, as well.

What is the average cost of small business insurance in New York?

The average cost of small business insurance in New York is $175 a month. Small businesses in New York should expect to pay from $75 a month to $3,000 a month. That is a wide range because New York is a large and diverse state. It’s primarily based on industry, location (urban versus rural area), and coverage types.

However, business owners who have physical business locations or own equipment, have people working for them, or provide professional advice should expect to pay more to protect against risks associated with these things. Prices are also higher for business owners who choose higher coverage limits, lower deductibles, more coverages, and additional endorsements.

What’s important is that you get quotes from a few of the providers on my list so you can compare coverages and costs to get the best and most cost effective coverage for your business.

How can I find cheap business insurance in New York?

Here are some tips to help you find the coverage you need at a fair price:

Shop around

Get quotes from a few companies or compare the multiple quotes provided by a digital broker or agency like CoverWallet or Policy Sweet. Different insurance companies have different underwriting policies and they will give your business different quotes. Also, different insurance companies might have different preferences for a certain industries over others, thus might provide different prices based on their preferences.

Buy a bundle policy

Some insurers offer bundled policies that combine the coverages of different policies such as BOP or professional liability insurance endorsement on a general liability insurance policy. These bundled policies will offer you several coverages at a cheaper rate.

Ask for discounts

Insurers might also offer several discount programs. Some offer you a discount for being a new customer. Others may offer you a discount for paying for an annual subscription, and in some cases, you can get discounts for paying with your credit card.

So, if you need a discount, ask the insurer to know if you qualify for one.

Have a risk management plan

If you take precautions to guard against risk, your liability insurance premiums may be lower than the national average. Risk management can include installing security systems on your premises or offering employee training programs.

Taking these steps will help ensure you’re not paying too much for your New York small business insurance.