The truth: The possibility for a media company making mistakes and errors and getting sued over them can be even greater than for many other professions. The cost of lawsuits and settlements can be high — enough to put a small media company out of business.

The best way to control these risks and costs is through media liability insurance. This article will reveal the 6 best insurers for the coverage, the pros and cons of each, and what you need to know to get media liability insurance for your company.

- 6 best media liability insurance companies

- What is media liability insurance?

- What does media liability insurance cover?

- Who needs media liability insurance?

- What other types of insurance do businesses in the media industry get?

- How much does media liability insurance cost?

- How to find cheap media liability insurance?

6 best media liability insurance companies

Media liability insurance is a professional liability policy customized for media companies. It is actually a specialized coverage and quite difficult to find. We have done intensive research and here are the 6 best media liability insurers that we recommend:

- CoverWallet: Best for comparing several quotes

- Hiscox: Best for combining media liability with general liability in one policy

- Chubb: Best for specialized coverage for different types of media companies

- AIG: Best for its risk management program tailored for media companies

- Dinghy: Best for freelance writers and small bloggers

- Thimble: Best for a fast online quote and immediate coverage

CoverWallet: Best for comparing several quotes

CoverWallet makes it fast and easy for media business owners to get several quotes on a single screen from its network of insurers.

PROS:

- CoverWallet allows media company owners to get several quotes — and buy insurance — in just a few minutes.

- Despite the complexity of media liability insurance, CoverWallet makes it relatively fast and easy to apply for coverage online or through a representative.

- CoverWallet an connect you with coverage unique to your business.

CONS:

- You don’t get insurance directly from CoverWallet, meaning that if you have to make a claim, it’s through the insurer you get your coverage from.

- For media liability coverage, you may need to speak to their agents to get and compare several quotes.

Bottom line: CoverWallet makes it easy for busy media business owners to get several professional liability quotes all in one place.

Hiscox: Best for combining media liability with general liability in one policy

Hiscox is a well-established insurance company that has a high appetite — or desire — to cover media companies. That means it is very likely you’ll be able to get media liability coverage from the insurer at a fair price.

PROS:

- Hiscox USA is a leading insurer that traces its history back to 1901. It is part of the Hiscox Group, which has over 3,000 employees in 14 countries, and customers worldwide.

- Hiscox is able — and willing — to customize coverage for different types of media businesses.

- The insurer makes it easy to get support from an experienced Hiscox representative who understands the media business landscape.

CONS:

- Coverage from Hiscox can sometimes be more costly than other insurers.

- The Hiscox online application process isn’t as easy to complete as those from online insurance providers.

- Hiscox offers limited online policy management capabilities.

Bottom line: If you’re willing to pay a little more for your media errors and omissions coverage to get a higher level of support from an established insurance company, Hiscox may be right for you.

Chubb: Best for specialized coverage for different types of media companies

Chubb is unique in that it provides media liability insurance protection through its MediaGuard program, tailored specifically to the needs of different kinds of media businesses along with extended coverage types.

PROS:

- Chubb offers specialized coverage for members of the National Newspaper Association, public TV and radio stations, and television and film producers.

- Chubb offers professional liability protection that’s more extensive than most other providers.

- You can apply for coverage online or purchase it through an affiliated agent.

CONS:

- Chubb’s robust coverage comes at a premium price.

- It can take more time to apply for insurance than through online insurance companies.

- You may not be able to get fast coverage through Chubb.

Bottom line: Chubb’s extended media liability protection could be right for you if your business faces unique or extensive professional risks.

AIG: Best for its risk management program tailored for media companies

AIG is a top-tier insurance company that offers broad and extensive media liability and other business insurance coverage. It offers a robust risk management program to help companies manage risks effectively. The risk program has special customization for media companies, which makes it unique and valuable.

PROS:

- AIG resolves claims quickly and provides expert advice on navigating professional lawsuits.

- The firm has a team of specialists that ensures the right people review even the most complex claims on day one.

- AIG provides resources and advice to help your media business avoid common professional risks.

CONS:

- You cannot apply for or buy coverage online from AIG.

- You have to buy your insurance through an insurance agent representing AIG.

- AIG has an extensive network of representatives but may not have agents in all areas.

Bottom line: AIG is an established, old-school insurer. If you prefer to do business online, it’s not the right company for you.

Dinghy: Best for freelance writers and small bloggers

Founded in 2017, Dinghy’s unique value to its customers is that it offers insurance to freelance writers only and allows them to turn their insurance off and on (or up and down) with ease, only charging them for coverage when they need it.

PROS:

- Dinghy provides you with a daily quote for your coverage, and you pay for what you’ve used at the end of the month.

- Applying for Dinghy insurance only takes minutes, and you can manage your policy on the Dinghy smartphone app.

- The firm has partnered with AmTrust, one of the world’s biggest insurance companies, to offer coverage for freelance writers.

CONS:

- Insurance is available for freelance writers and bloggers only.

- You can only get limited types of coverage beyond professional liability from Dinghy.

- You will get limited support from the company during the insurance buying process.

Bottom line: Dinghy could be the ideal insurance provider for freelancer writers who need control over their coverage and costs.

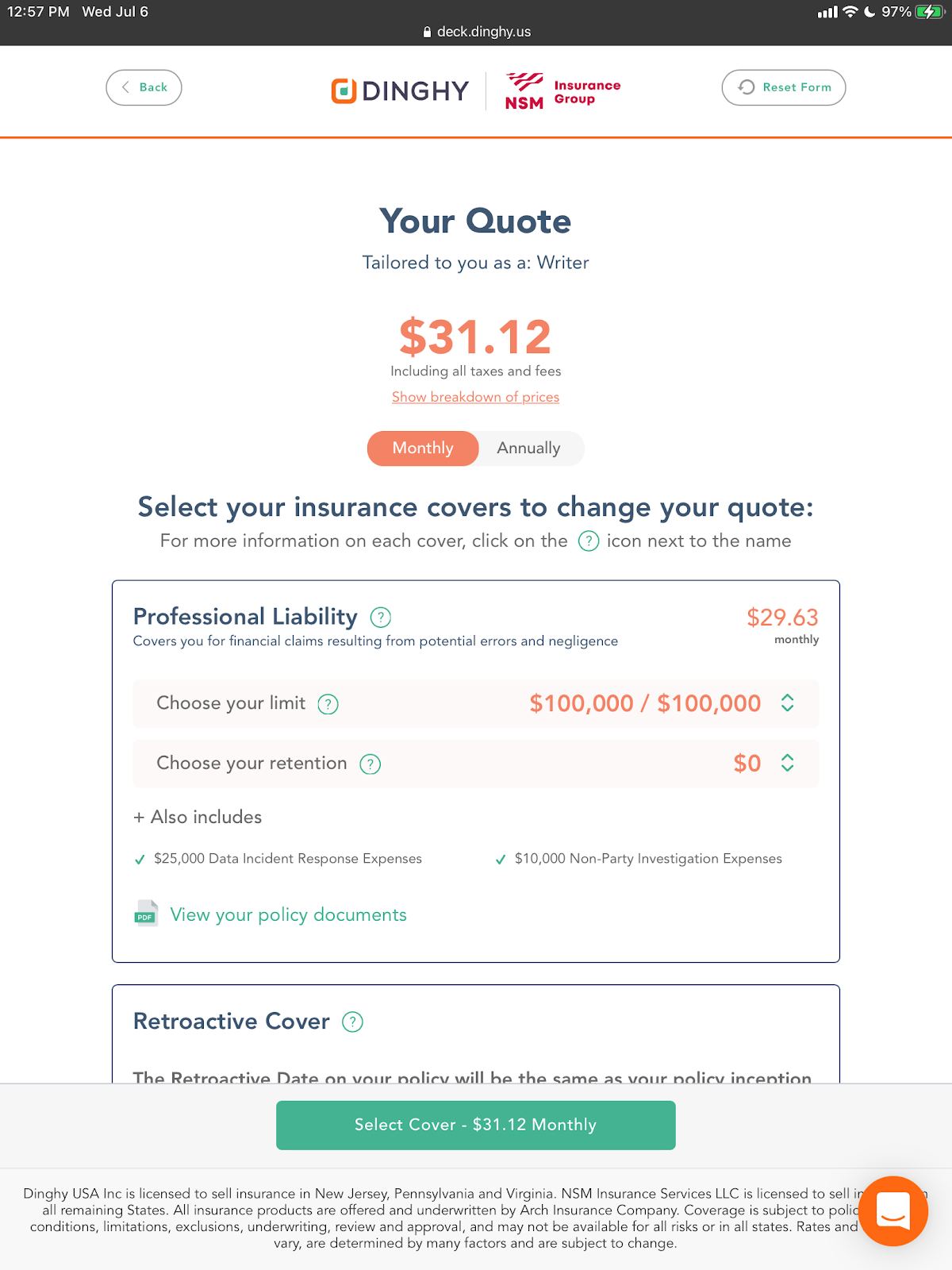

Here is a professional liability quote for a blogger from Dinghy.

Thimble: Best for a fast online quote and immediate coverage

Thimble is unique because it offers media liability coverage by the hour, day, or month. You only pay for insurance when you need it. They offer one of the best digital experience for small businesses to buy insurance in general. If you need immediate coverage, you should consider getting a quote from Thimble.

PROS:

- Thimble’s limited-time coverage makes its insurance affordable for companies that don’t need continuous protection.

- It’s easy to get a quote on the Thimble website or its mobile app. All you have to do is input a few details about your business and review your free quote.

- With Thimble, you can get coverage in just a few minutes and download a certificate of insurance in less than 60 seconds.

CONS:

- Media liability insurance coverage often needs to be customized to a company’s needs. Thimble offers limited customization options.

Bottom line: Thimble could be your best choice if you need on-demand professional liability coverage.

What is media liability insurance?

Media liability insurance, often referred to as professional liability insurance for people in the media industry and errors and omissions insurance, protects small businesses against the costs of client lawsuits over mistakes, advertising issues, and unsatisfactory work. The costs covered by media liability insurance include hiring a lawyer to defend yourself and business and settlements.

A simple mistake made by your advertising or media company could result in financial harm to a client. If that client sues, it could cost your business six figures or more, depending on the seriousness of the issues and the financial consequences of them.

A media professional liability policy provides protection related to:

- Work mistakes and oversights

- Missed deadlines

- Advertising issues, such as libel and slander

- Wrong or incomplete advice.

This insurance covers the most common issues media-related companies are sued over.

Learn more at professional liability insurance cost and the best professional liability insurance companies

What does media liability insurance cover?

Here are some of the things this type of insurance will cover:

Work mistakes and oversights

If a client believes you made a mistake or your work does not meet their standards, you could be sued for negligence. For example, a website you develop contains errors, does not meet the company’s brand standards, and generates far less revenue than expected because of the problems. You’re taken to court over it.

The lawsuit becomes an expensive legal battle because the client believes your business caused them severe financial harm. Media liability insurance helps cover your legal costs, whether you’re at fault or not.

Missed deadlines

Project delays can significantly impact the bottom lines of your clients. If you are taken to court over a missed deadline, for instance, you fail to complete a seasonal advertising campaign on time, your professional liability insurance could help pay for:

- Lawyer fees

- Court-ordered judgments

- Settlements

These expenses often put a small media company out of business.

Advertising injuries

Advertising injuries are generally covered under a general liability policy. However, they are typically excluded from general liability coverage for media and advertising professionals because of the nature of their work. Instead, media liability insurance provides coverage for issues like:

- Defamation, both libel (written) and slander (spoken)

- Copyright infringement.

Media companies put themselves at significant risk if they don’t have coverage for these severe and common errors.

Bad or incomplete advice

Imagine offering a client advice about a marketing campaign you project will significantly increase their sales. You launch the campaign and sales tank, causing your client to almost go out of business. They sue you because they feel you gave them bad advice that almost put them out of operation. Your professional liability insurance will pay legal and settlement costs, even if you settle out of court.

Be aware: When it comes to court settlements, there are typically two different clauses within a media liability policy that you must be mindful of:

- Consent-to-settle states that your insurer, once they’ve started the review process, will not settle unless the policyholder provides consent.

- The hammer clause states that if the policyholder doesn’t agree to a settlement acceptable to the insurer and claimant, a penalty will apply. The penalty results in the insurer paying less than the final settlement amount.

These two clauses seem contradictory. On the one hand, the insurer gives the policyholder the flexibility to accept a settlement offer or not. Conversely, if the policyholder disagrees with a settlement, they’re penalized. What’s important is to be aware that your policy may not pay all your settlement costs in some circumstances.

Who needs media liability insurance?

- Advertising agencies and marketing professionals

- Broadcasters and other media professionals

- Digital marketing agencies

- Graphic designers and other visual artists

- Media planners and buyers

- Public relations consultants and agencies

- Publishing companies

- Printers

- Social media consultants and companies

- Writers and authors.

This isn’t a complete list of professions and companies that could benefit from having media liability insurance, but it’s indicative of how broad the range can be.

What other types of insurance do businesses in the media industry get?

While media liability insurance covers many of the primary risks faced by media and advertising businesses, it doesn’t provide complete protection. Other coverages to consider include:

- General liability insurance covers expenses related to injuries that happen to non-employees on your business property, including medical bills and legal costs. It also pays for damage to other people’s property caused by you or the people who work for you while conducting business. Learn more at general liability insurance cost and the best general liability insurance companies

- Workers’ compensation insurance is required in most states for businesses with employees. It covers medical expenses and a portion of lost wages if an employee is injured or becomes ill for work-related reasons. Learn more at workers comp insurance cost and the best workers comp insurance companies

- Cyber liability insurance pays notification and communication costs, recovery, and other expenses related to data breaches. This policy is crucial for companies that store a lot of sensitive data, which many media businesses do. Learn more at cyber liability insurance cost and the best cyber liability insurance companies

This is only a partial list of the coverages that could be right for your media business. Speak with a business insurance agent or representative at an insurance company to figure out what coverage you need to protect the business you’ve worked so hard to build.

How much does media liability insurance cost?

Most smaller media and advertising businesses pay a median of $70 per month for media liability insurance, However, you could pay more or less depending on your business’s unique risks.

This is just the average rate that millions of small businesses pay for their media liability insurance policy. Your rates will be different. Be sure to shop around with a few companies or work with a top broker like CoverWallet and Simply Business to compare several quotes to choose the cheapest one for you.

Factors impacting media liability insurance cost

Liability insurance premium costs for media professionals are based on many factors, including:

- Advertising or media services offered

- Revenue

- Location

- Number of employees

- Employee experience

- Business processes and procedure

- Insurer

- And more.

How to find cheap media liability insurance?

Below are a few tips that can help you find cheaper media liability policy for your company:

Shop around to compare several quotes

You must get quotes from several insurers — or a broker or marketplace — to ensure you get the best professional liability insurance coverage at a reasonable cost for your media company.

Different insurance companies always give you different quotes because they assess risks differently. Don’t take the first quote , you will leave money on the table.

Manage your policy’s terms

The policy’s coverage limit and deductibles play a significant impact on the policy cost. Decreasing the policy’s coverage limit or increasing the policy’s deductibles will reduce the policy’s rates.

Make sure you select the right policy terms to reduce your cost.

Always ask for discounts

Insurance companies often provide different discount programs. You will be surprised to learn how much discount programs that you are eligible for. Even if you are not eligible now, knowing that it exists will help you prepare to be eligible for when you renew or need to shop again.