Handyman services are essential to the lives of Californians and the economy. Handymen keep our stores, apartments, residences, and crucial equipment running efficiently.

While operating your handyman business can be gratifying, it carries significant risk. If a customer slips over your ladder and falls, for instance, you might be held legally liable for their medical expenses. Sometimes, these costs can exceed your annual income as a handyman.

This begs the question, how are you safeguarding yourself and your company against the possibility of lawsuits and losses? Handyman insurance is a cost-effective method of avoiding these risks, with affordable coverage options.

This article reviews five of the best and most popular handymen insurers in California. These companies offer the best policies regarding coverage, pricing, service, and more.

- 5 best handyman insurance companies in California

- What does handyman insurance cover?

- California handyman insurance requirements

- How much does handyman insurance cost in California?

- Factors impacting handyman insurance costs in California

- How to get cheap handyman insurance quotes in California?

5 best handyman insurance companies in California

We have done the research and here are the 5 best companies offering business insurance for handymen in California.

- CoverWallet: Best for comparing online quotes

- Simply Business: Best for finding low-cost coverage

- NEXT: Best digital experience

- InsurePro: Best for part-time handymen

- The Hartford: Best for extensive coverage options

CoverWallet: Best for comparing online quotes

CoverWallet is an insurance broker with an online quote generator that allows you to compare the prices and services of its partners. Four insurance choices are available from this firm.

You can simply choose general liability insurance with a $1 million maximum. Alternatively, you can buy general liability and commercial property insurance for more coverage.

If you’re searching for comprehensive insurance, CoverWallet provides a business owner’s policy with commercial auto coverage. If that is insufficient, CoverWallet may provide you with a bespoke insurance plan where you can choose and add the necessary insurance policies.

Pros

- An extensive array of accessible add-on policies

- Individual evaluation report to determine the best policy option

- Coverage is available online for all policies

- Compare handyman insurance quotes for free

- A dedicated agent is allocated to each quotation for around-the-clock phone service.

Cons

- Online chat response is slow

- Customers have to file a claim directly with the insurance company, not with CoverWallet

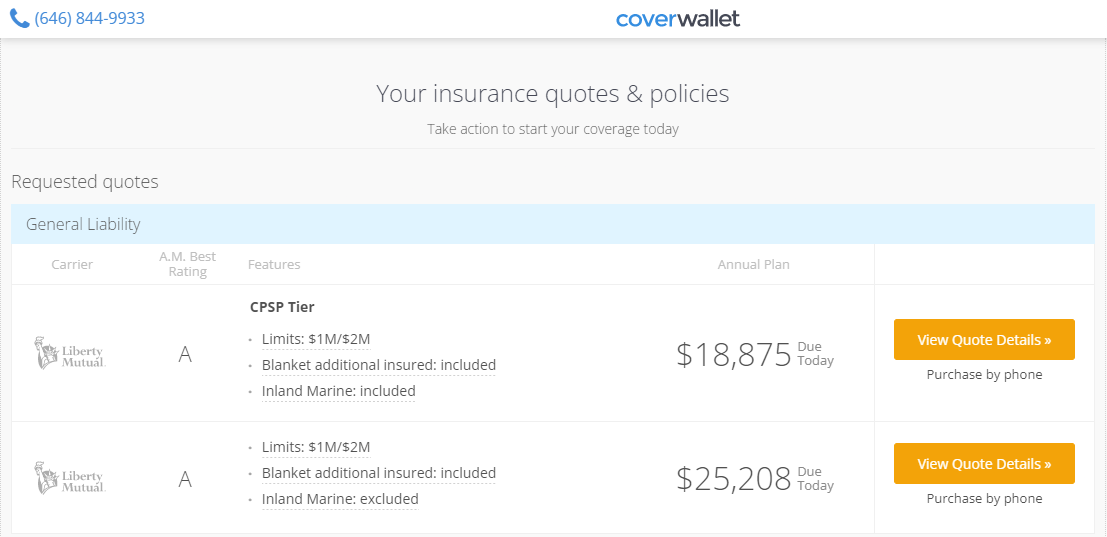

Below is a quote that we got from CoverWallet for a handyman located in San Jose, California

Simply Business: Best for finding low-cost coverage

Simply Business is an internet broker that offers rapid, low-cost, and affordable quotes, and the policy may be purchased online. This is the best choice if you’re a handyman who doesn’t want to search around and wants a one-stop shop to find the cheapest coverage.

The quote procedure is fast and straightforward; it typically takes about 10 minutes. Simply Business offers you a personal account where you can manage your policy, add more insureds, and receive a certificate of insurance after purchasing a policy.

Pros

- Online quotes are available in 10 minutes

- Access to multiple insurers

- Insurance is purchased online

- With strong financial backing from Travelers

Cons

- You have to make claims with the third-party company that sold your policy

- Limited digital features

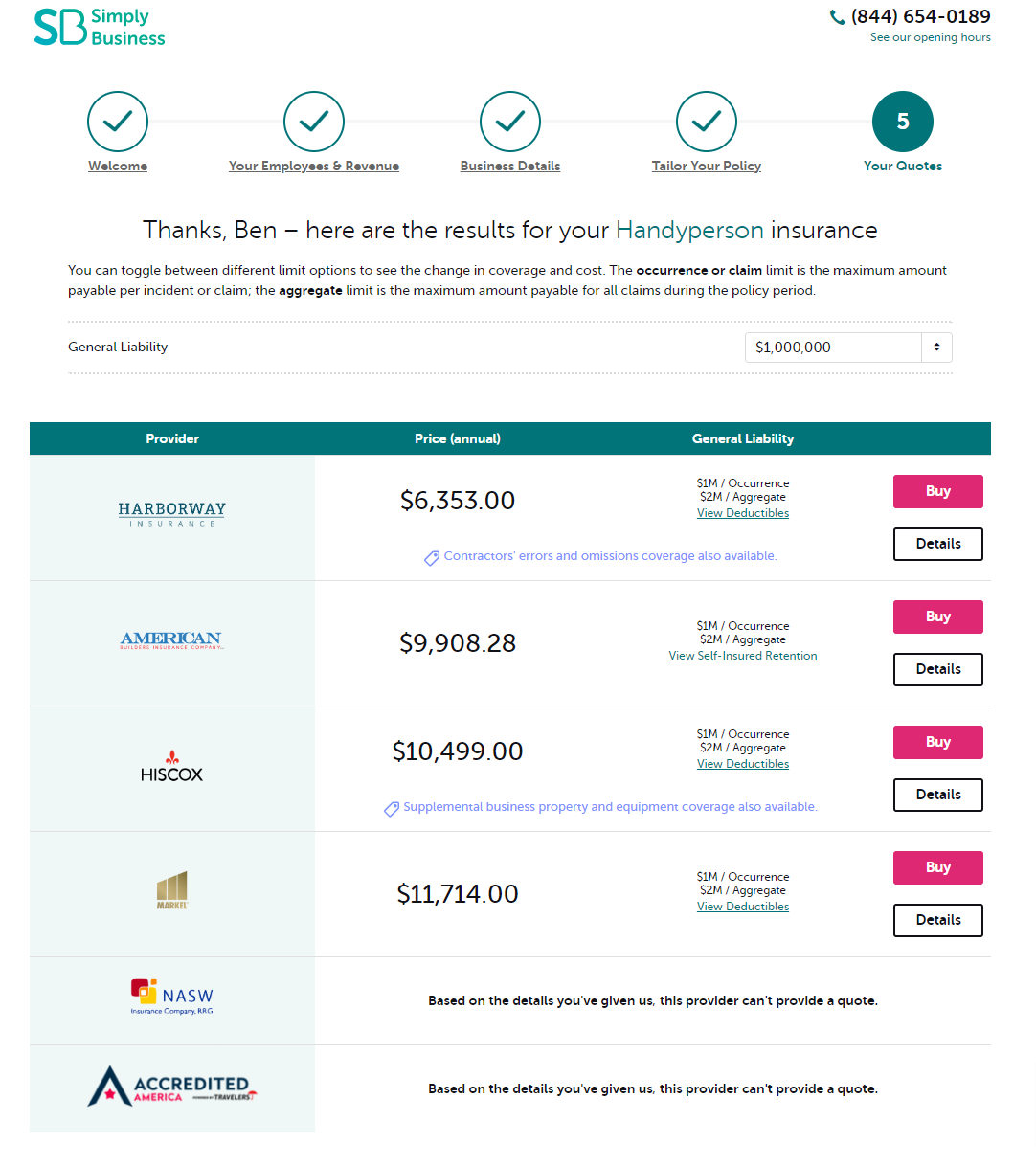

Below is the quote we got from Simply Business for a handyman based in Los Angeles California

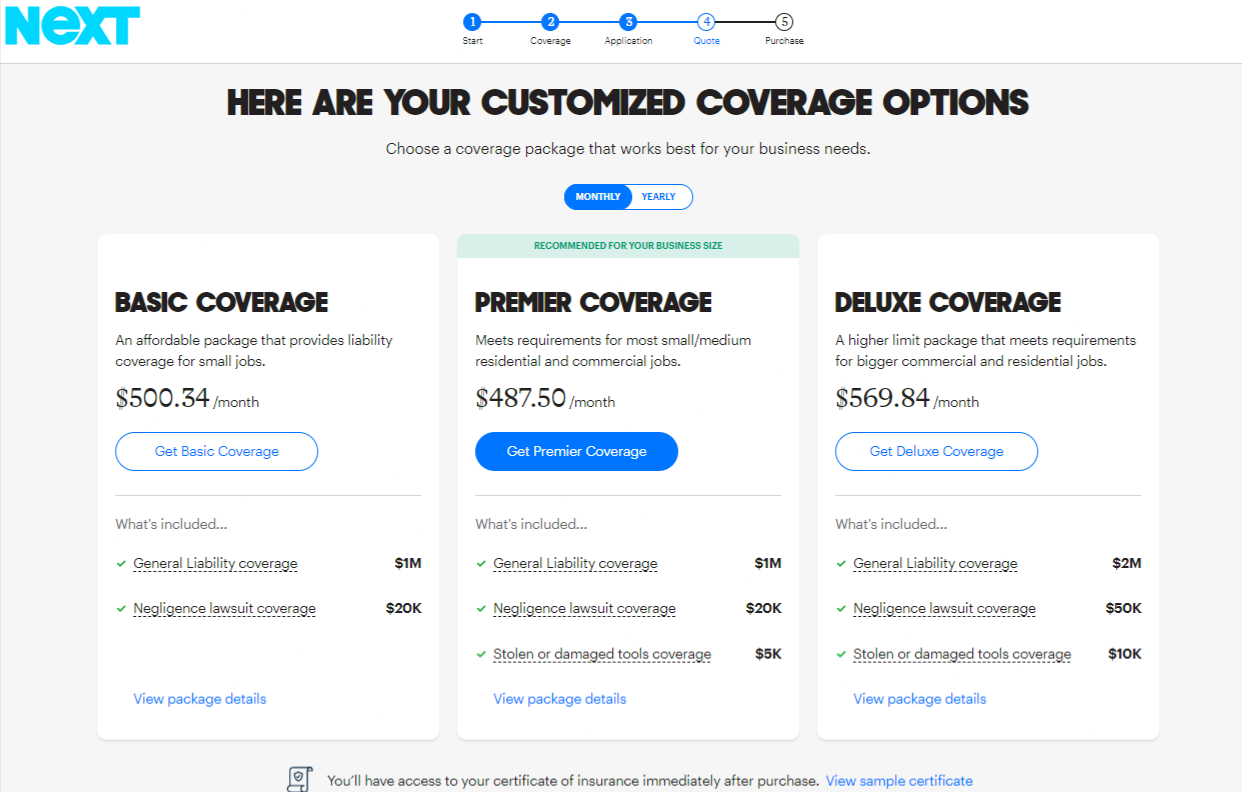

NEXT: Best digital experience

Next was created in 2016 and is relatively new to the insurance industry. NEXT Insurance focuses heavily on handyman insurance, offering a streamlined digital client experience, good customer service, and various bundling options that may reduce the cost of coverage for individual handymen.

Next can provide such reasonable insurance premiums because of the extensive usage of artificial intelligence in their claims procedure. This enables their customers to enjoy many discounts.

Pros

- 10% savings when different kinds of coverage are bundled.

- Affordable insurance premiums

- Optional protection for tools and machinery

- Same-day coverage available

- Simple to get a quotation and register online

- Claims response in 48 hours

Cons

- Quotes cannot be obtained via phone.

- Relatively young insurer

InsurePro: Best for part-time handymen

InsurePro’s handyman insurance provides general liability insurance with coverage for products and performed operations. One of the advantages of getting insurance with InsurePro is that you will receive immediate evidence of coverage.

Also, you can buy flexible coverage for hours, days, weeks, or months. Handyman general liability insurance from InsurePro covers between $1 million and $2 million.

Pros

- Affordable coverage alternatives

- Convenient online quotes

- No deposit needed

- Policies available on demand by the hour, day, or month

Cons

- Only accessible during the week

- Most policies come with only two coverage limit options

The Hartford: Best for extensive coverage options

The Hartford is among the finest insurance providers for handymen. This is due to the company’s financial stability, countrywide availability, flexible policies designed for handymen, and excellent client feedback.

The Hartford attempts to create every client relationship on a solid foundation by examining potential customers’ insurance requirements to determine the best coverage and policy for their company.

New clients may simply limit their insurance selections from the beginning, thereby saving them time and money by preventing them from obtaining unnecessary coverage.

Pros

- Coverage offered per project

- Customized policies for handymen

- Numerous inexpensive policy packages

- One of the nation’s leading suppliers of workers’ compensation

- AM Excellent grade of A+

- 24/7 phone assistance with claims

Cons

- Outdated quotes generation platform

- Specific coverages offered only via an agent

What does handyman insurance cover?

Handymen insurance is a set of policies tailored by insurers to protect your small repair businesses against claims made due to liability or property damage. Depending on the size of your firm, you only need general liability.

Handyman general liability insurance

General liability insurance is the most typical form of coverage required for a handyman service. A general liability insurance policy covers most minor accidents that might occur during normal company operations, including bodily injury claims and property damage.

The policy will cover any legal bills incurred due to lawsuits brought against your company by consumers, other businesses and the general public.

For example, if a customer falls over your extension line and twists their ankle, or if you destroy their refrigerator by mistake, you could be held liable. If a claim is made, your handyman liability insurance coverage will pay attorney fees, other legal expenses, and settlements.

While most handymen and contractors will simply need general liability coverage, there are some additional forms of handyman insurance to consider. Therefore, if you want to add staff and expand your firm, you may need the following insurance policies.

Learn more at the best general liability insurance for handymen

Handyman workers’ comp insurance

Most states mandate workers’ compensation insurance for businesses with employees. It protects your workers (and you) in case of a workplace injury.

The policy typically compensates for missed earnings and medical costs to injured or sick workers. Workers’ compensation also shields you from any claims filed by injured workers.

For handymen with no workers, worker’s compensation is not necessary. However, you may choose to get coverage since it offers a financial cushion in the event of a work-related injury that prevents you from working for a time.

Learn more at the best workers comp insurance companies

Handyman commercial auto insurance

If you drive a business-owned car, you’ll require commercial auto insurance, as required by many state laws. In addition, it is essential to understand that your standard personal car insurance policy does not cover your vehicle for commercial purposes.

So, if you use your car for business purposes, you will need a commercial auto policy to protect you. Otherwise, you risk losing your vehicle if it gets damaged while using it for work.

Learn more at the best commercial auto insurance companies

Handyman commercial property insurance

Commercial property insurance is often required if your company is situated away from your residence or if you have a substantial inventory. It would cover you against theft and property loss resulting from fire, accidents, or natural disasters.

The policy may also protect your company tools and equipment, but only if they are placed on your premises. However, most insurers may not cover your tools and equipment if they are lost or destroyed while driving.

Most handymen do not need commercial property insurance since they operate out of their homes and have no inventory or business equipment.

But then, it’s crucial to analyze your individual scenario. If you have a big workshop at home with items worth tens of thousands of dollars, it may be prudent to get commercial property insurance.

Learn more at the best commercial property insurance companies

Handyman tools and equipment insurance

Unfortunately, general liability insurance does not cover stolen or damaged tools and equipment. Similarly, your commercial property insurance may not cover your tools adequately especially if you move them around.

So, if you carry costly tools and reside in an area where they are likely to be stolen, it may be worthwhile to pay an additional fee for your tools and equipment insurance.

Handyman professional liability insurance coverage

Professional liability insurance, also known as Errors and Omissions (E&O) Insurance, protects against carelessness claims.

This policy is commonly used by consultants, lawyers, architects, and other professionals that offer advice or licensed professional services.

E&O Insurance makes little sense for most handyman operations, but it is more helpful for contractors that offer their knowledge or supervise other subcontractors.

Handyman Business Owner’s Policy (BOP)

Business owners’ policies or BOPs are special plans that combine general liability, worker’s comp with commercial property liability at discount rates.

BOPs cover a large area of liabilities, including commercial property damage, personal property damage, loss of revenue due to covered work stoppages, general property liability, and general bodily injury to workers and others.

This coverage is suited for handymen with less than 100 employees and yearly sales below $5 million.

Learn more at the best BOP insurance companies

California handyman insurance requirements

To start a handyman business in California, you must first obtain a license. Without getting the handyman license, you cannot perform any project that exceeds a limit of $500, including labor and materials.

To undertake work that exceeds this limit, you must submit an application to the California Contractors State License Board for a general contractor’s license. The prerequisites include showing proof of insurance, a contractor’s bond of about $15,000 and more.

Also, workers’ compensation is compulsory in California as long as you have employees.

Even beyond government regulations, handyman insurance is still a good choice. This is because customers may inquire if you are insured by this coverage. If not, they may transfer the project to someone else with the policy.

How much does handyman insurance cost in California?

The average cost of handyman general liability insurance in California is $75 per month, or $900 per year. It is a bit more expensive than the national average of $65 per month.

As we learned above, handymen in California may need more insurance coverage than just a general liability insurance policy. Below are the average costs of other coverages for handymen in California:

| Handyman insurance coverages | Average costs |

| General liability insurance | $75 a month |

| Commercial auto insurance | $164 a month |

| Workers comp insurance | $332 a month |

| Contractor tools and equipment insurance | $18 a month |

These are just the averages. Your rates may be different. Be sure to shop around with a few companies or work with a broker like Simply Business or CoverWallet to compare several quotes to find the cheapest one for you.

Learn more at how much handyman insurance costs

Factors impacting handyman insurance costs in California

The price you pay for your handyman insurance may vary depending on the number of policies you choose and the kind of coverage you want.

The following variables may also impact the cost of your monthly and yearly premiums:

The city where you work in California

Handymen working in populated California like Los Angeles and San Diego have higher chances of getting sued than others in rural areas. Therefore, handyman insurance will likely be more expensive in populated areas of California.

The kind of repair work in which you specialize

Handymen that handle dangerous jobs or jobs that require expertise tend to have higher premiums. For instance, if you provide roof repairs, you’ll likely have to pay a little more since these services are more likely to result in an insurance claim.

Previously filed claims

Your previous claims are a sign that you will likely make more claims in future. Therefore, your insurer may charge you more if you have made several claims in the past.

Employee count

The more employees you have, the more the possibility of having issues with your clients. Therefore, your premiums increase with more employees.

Your yearly gross revenues or income

Companies with higher revenue tend to pay more when sued. Therefore, insurers will charge you more.

How to get cheap handyman insurance quotes in California?

In general, obtaining inexpensive general liability insurance for handymen is simple. However, the following are some ideas to help you get discounts on your quotes.

Compare insurance quotes

If you’re looking for a low-cost handyman insurance quotation, your best option is to compare handyman insurance rates online. Depending on your location in California, you may be able to take advantage of offers provided by local insurers.

Adjust your deductibles

The simplest technique to get a discount is to promise to pay a greater deductible. This implies that if you make a claim, you will pay more out of pocket. However, the trade-off is that your monthly premiums will be reduced.

Bundle plans

Bundling your plans is another excellent method for lowering your insurance expenses. Consider purchasing numerous insurance policies, such as general liability, commercial auto, and workers’ compensation. It is preferable to bundle them all via the same insurer and, if possible, on a BOP, as opposed to purchasing separate policies from several insurers.

By bundling your insurance, you effectively get discounts over individual policies, reducing the total cost of your premium.