Hairdressers have to deal with unique risks not faced by other small businesses:

- Chemical burns to customers

- Injuries from slips and falls on wet and slippery floors

- Lawsuits from customers unhappy with their hairstyles.

The expenses associated with these things can be large enough to put even an established salon out of business.

The best way to protect your salon operation against these costs is to get adequate hairdressing business insurance. This article will reveal the 5 best hairdresser insurance companies and provide the information you need to get the right coverage for your salon.

- 5 best hairdresser insurance companies

- What is hairdresser insurance?

- What insurance coverages do hairdressers usually get?

- How much does hairdresser insurance cost?

- How do I get cheap hairdresser insurance?

- What information do I need to get a hairdresser insurance quote?

5 best hairdresser insurance companies

- CoverWallet: Best for comparing online quotes

- Simply Business: Best for an easy application process

- biBerk: Best for inexpensive hairdresser business insurance

- The Hartford: Best for hairdresser coverage from a top insurer

- Thimble: Best for highly flexible hairdresser insurance

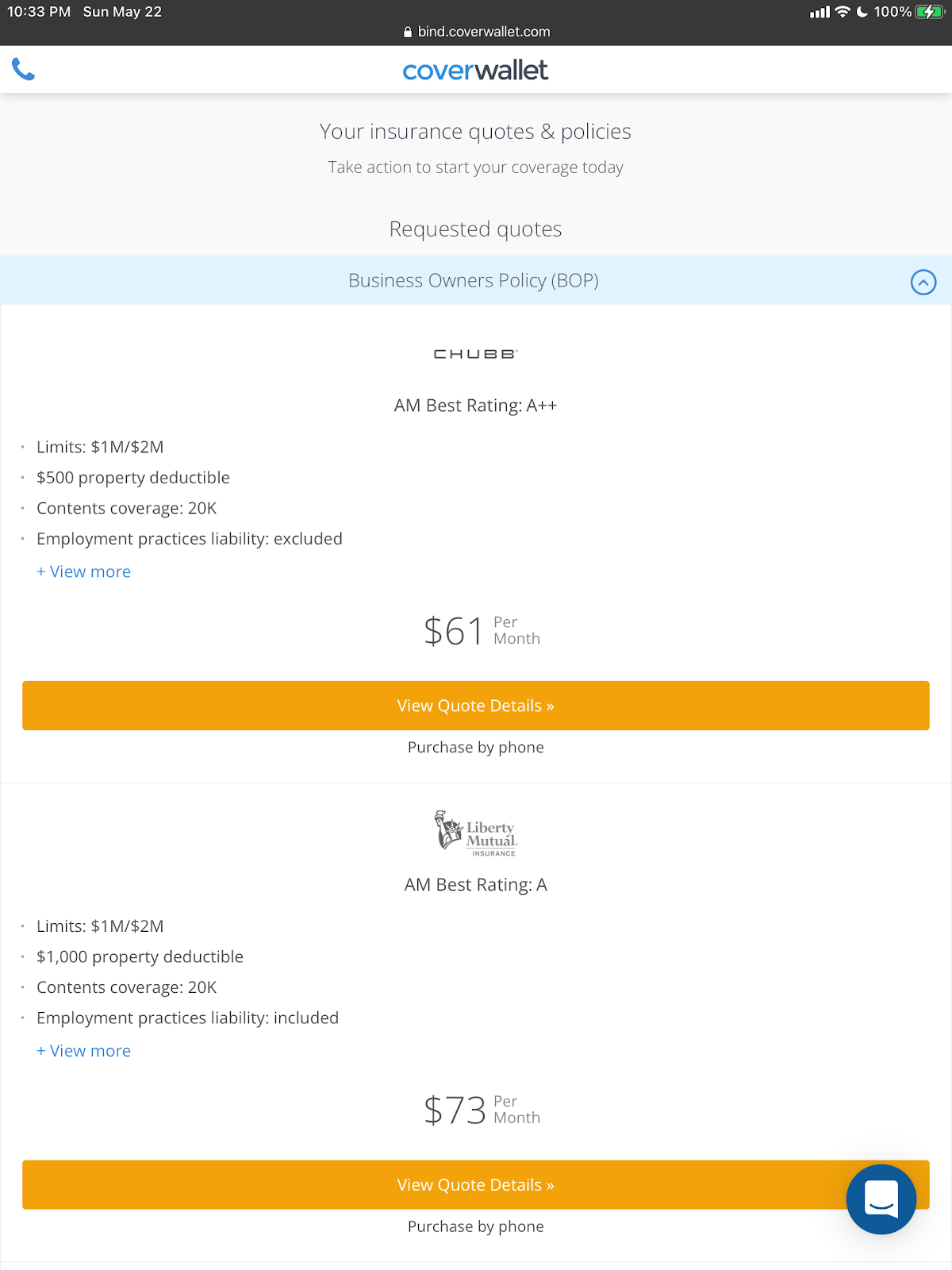

CoverWallet: Best for comparing online quotes

If you want to compare several quotes to find the most cost-effective one with the best level of coverage, CoverWallet could be a great option. CoverWallet is an online broker that partners with top business insurance companies. Once you provide CoverWallet with information about you and your salon, it will present you with several quotes. You can compare them and select the one that’s best for you.

After you buy your hairdresser insurance through CoverWallet, you can use its digital dashboard to manage all of your business insurance policies in one place. The dashboard also makes it easy to download a certificate of insurance, file a claim, and renew your policy.

Here is a quote for hairdresser insurance for a small home salon.

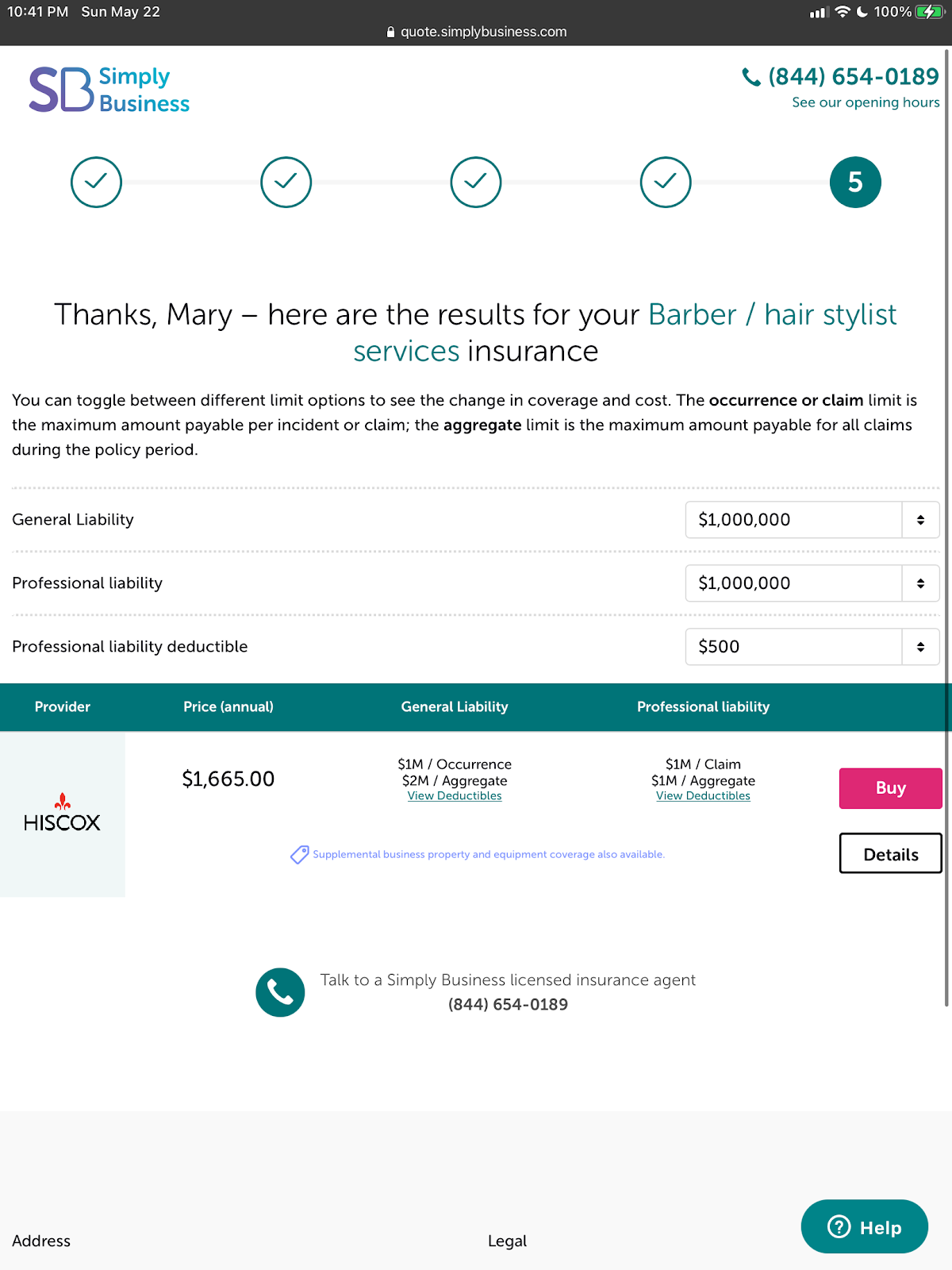

Simply Business: Best for an easy and fast buying process

Simply Business was founded almost twenty years ago. Despite its relative newness, it’s become an insurance company trusted by more than 800,000 small business owners.

Simply Business has become known for:

- Making it simple to apply for coverage through its website or get support from an experienced representative over the phone.

- Allowing you to compare multiple quotes and buy hairdressing insurance in minutes.

- Letting you get proof of insurance and other documents the day you purchase coverage.

- Expert claims support 24 hours a day, seven days a week.

- Being rated 4.7 out of 5.0 based on almost 40,000 reviews.

If you need hairdresser insurance fast and value a quick and easy application process, give Simply Business a look.

Here is a sample quote from Simple Business.

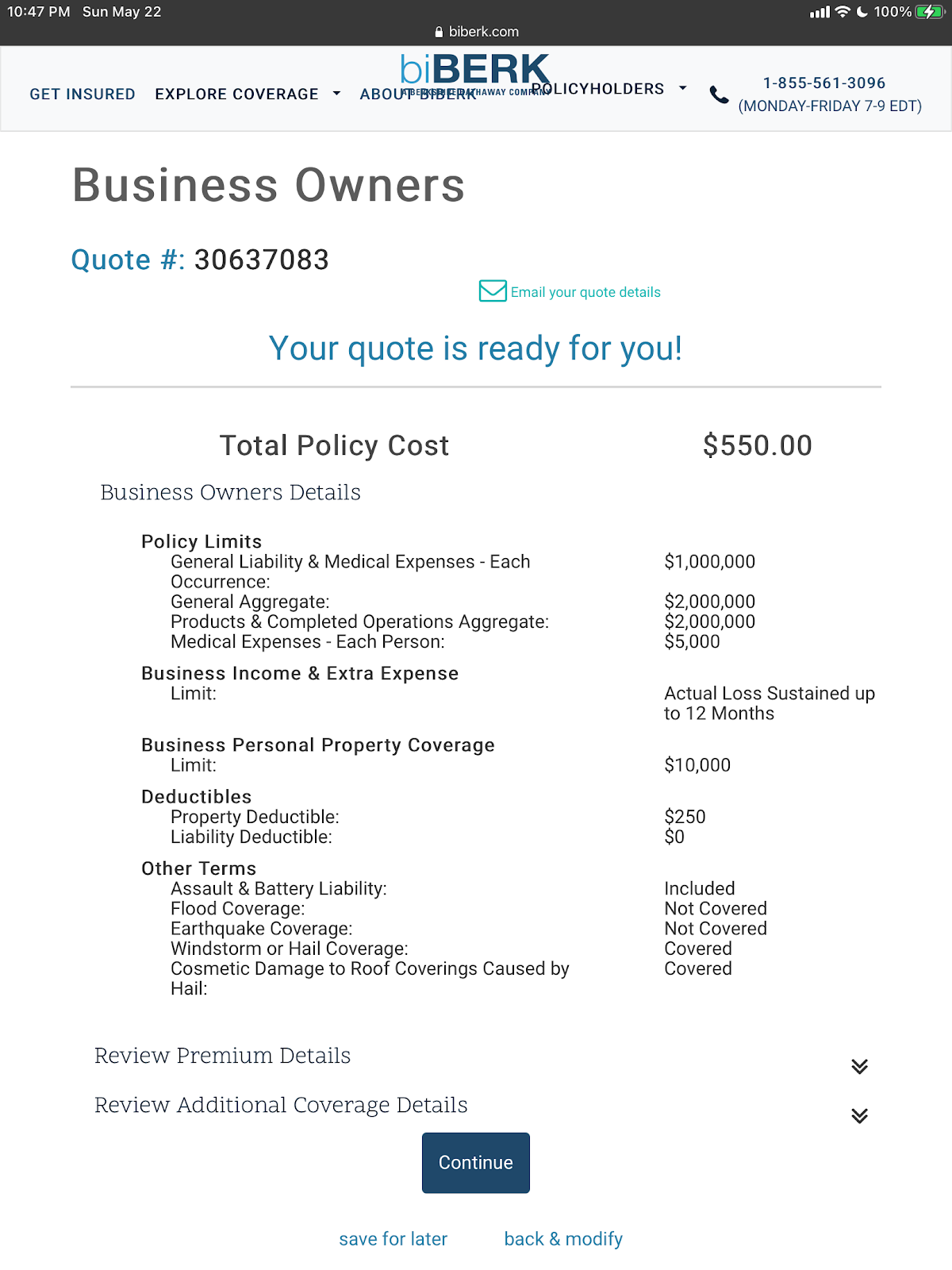

biBerk: Best for inexpensive hairdresser business insurance

After the last few years of extraordinary small business instability, few hairdressers have extra cash to spend on insurance. If that’s the case with your salon, biBerk could be a good insurance company for you.

biBerk is a low-cost business insurer. Even though you will save money on your hairdresser business coverage with biBerk, you can feel confident knowing you’re getting quality protection for the salon you’ve worked so hard to build. biBERK lowers insurance costs by almost 20 percent because it insures hairdressers and other small business owners directly, without the added cost of having to work through an intermediary or insurance broker.

biBerk is a division of Berkshire Hathaway, a company headed by Warren Buffett. It’s a firm with millions of satisfied customers that’s been insuring businesses for more than 75 years.

Here is a representative hairdresser insurance quote from biBerk.

The Hartford: Best for hairdresser coverage from a top insurer

The Hartford is a top salon insurance supplier. It can tailor a policy to the needs of any size of salon, including home-based businesses. In addition to bundling property and general liability coverage, The Hartford’s business owners policy has five optional insurance coverages salon owners can add to increase their protection, including coverage for professional errors, data breaches, and lost income because of off-premises utility service failures. It’s also easy to get workers’ compensation insurance through The Hartford. The Hartford offers online claim reporting and policy management available which is a big plus for busy hairdressers. Be aware that The Hartford doesn’t provide coverage in Alaska or Hawaii.

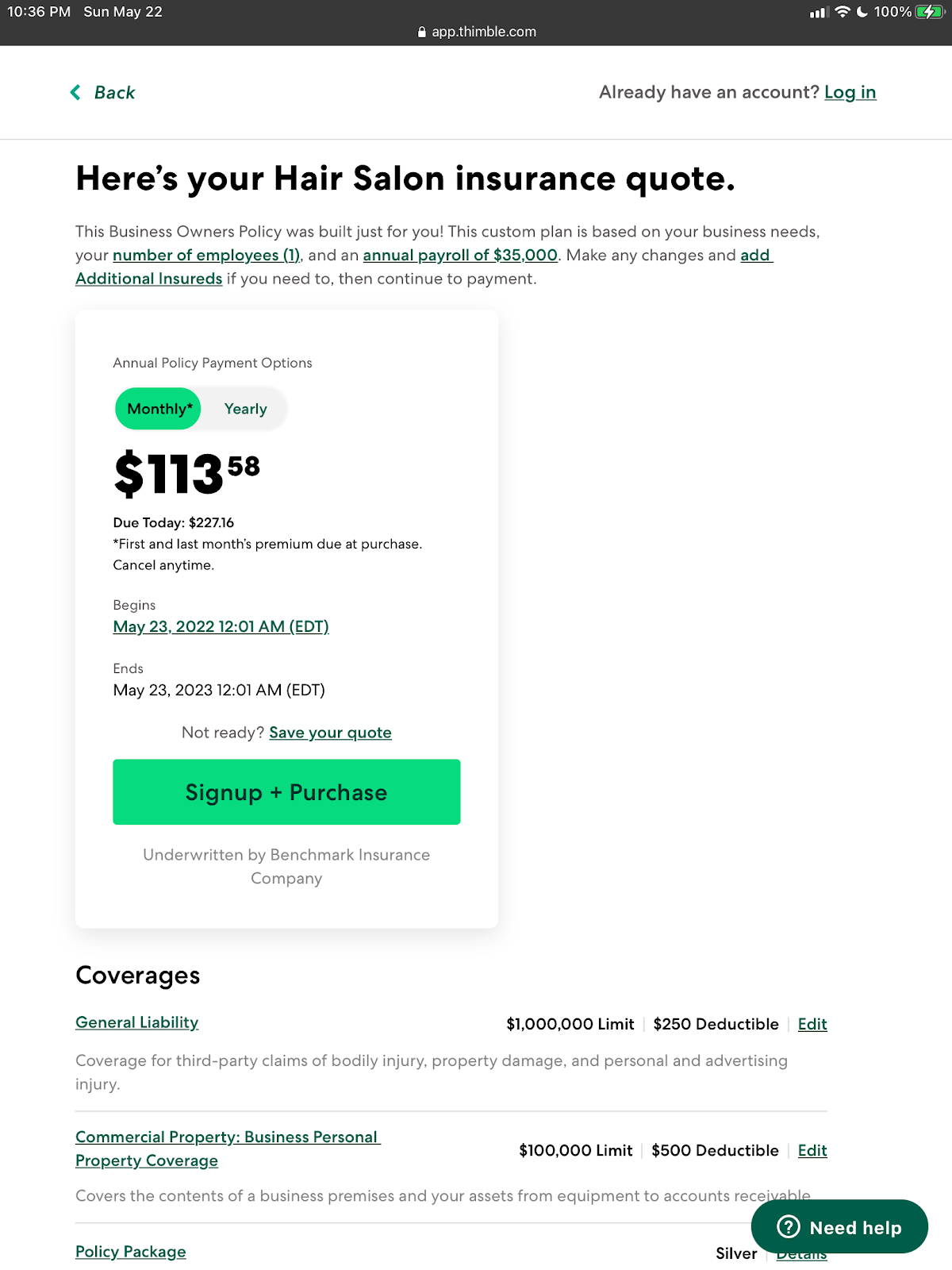

Thimble: Best for highly flexible hairdresser insurance

Thimble offers general, professional, and other types of business insurance for salons, other small businesses, and self-employed individuals. Thimble is a relative newcomer to the business insurance marketplace. However, it differentiates itself from other new insurers by offering policies with flexible terms.

Instead of forcing you to buy a policy for an entire year, Thimble lets you purchase one for as long as you need, whether a month, a day, or even as little as an hour. You can also extend, modify, or cancel your policy right from the Thimble app.

Here is a sample hairdresser insurance quote from Thimble.

What is hairdresser insurance?

Hairdresser insurance is coverage customized to fit the unique needs of hair salon owners. Choosing the right coverages is vital, as they can protect against costly losses from things like customer injuries and lawsuits resulting from them.

What insurance coverages do hairdressers usually get?

Basic insurance coverage for hair salon includes:

- General liability insurance protects against mishaps that can occur at your salon. For example, a customer slips on a wet floor in the salon and breaks her arm. General liability coverage could help pay for their medical expenses and your legal costs if you’re sued over the incident. Learn more at the general liability insurance cost and the best general liability insurance companies.

- Commercial property insurance is necessary coverage if you own your salon. It pays to repair the property or replace things damaged by fire, vandalism, weather events, and more. Commercial property insurance covers your business and its contents and the area surrounding it, including parking lots. You must get this coverage even if you run your salon out of your home because your homeowners insurance won’t pay for damage resulting from salon services. Learn more at commercial property insurance cost and the best commercial property insurance companies.

- Business owners policy (BOP) combines general liability coverage with commercial property insurance in a cost-effective policy. It’s easy to add additional coverages to a BOP like professional liability or rental equipment coverage. Learn more at BOP insurance cost and the best BOP insurance companies.

- Professional liability insurance, also known as errors and omissions (E&O) insurance, protects you from claims of negligence against your business related to providing hairdressing services. Learn more at E&O insurance cost and the best E&O insurance companies.

- Workers’ compensation insurance provides benefits, including medical care, disability, lost wages, and death benefits if an employee is injured, becomes ill, or dies because of work-related reasons. Most states require salon owners with employees to get this coverage. Learn more at workers comp insurance cost and the best workers comp insurance companies.

An insurance agent or company representative can advise you on the coverage you need for your salon.

What insurance coverage an independent hairdresser should get?

If you are an independent hairdresser or hairstylist, you may work independently or are a contractor at a hair salon, you are operating as an individual business owner, you’ll need insurance to protect yourself. The two insurance coverage you will need to protect yourself are:

- Professional liability insurance or E&O insurance: In fact, some hair salon require you to have this coverage before they hire you to work at the salon. Even if they do not require, you should have this in case your clients decide to sue you because they are injured or just simply not happy with the outcome and believe you make a mistake.

- Workers comp insurance: This coverage to protect yourself in case you get injured at work. Hair salon owners do not offer this coverage to independent contractors because they are not required. If you get injured at work without this coverage, you are completely on your own and that can bankrupt you. Learn more at the best workers comp insurance companies for independent contractors.

What insurance coverage for hairdressers renting a chair should get?

Similar to independent contractor hairdresser working for a hair salon, hairdressers renting a chair in a hair salon should get E&O insurance and workers comp insurance to protect themselves if their clients sue them or if they are injured at work. In addition, hairdressers renting a chair should also get property damage insurance just in case the booth or the chair they are renting gets damaged for whatever reasons, they don’t have to pay for it out of their pockets. In fact, the hair salon owners often require hairdressers renting a chair have at least E&O and property damage coverages before agreeing to rent a booth or a chair to them.

Learn more at the best insurance companies for hairdressers renting a chair.

How much does hairdresser insurance cost?

The average hairdresser insurance cost is $75 a month. However, this largely depends on the coverage you get and if you are a hairdresser owning a salon or an independent hairdresser. Below are some breakdowns for different scenarios:

| Hairdresser types | Insurance coverage | Average costs |

| Independent hairdressers | E&O insurance | $35 per month |

| Workers comp insurance | $80 per month | |

| Hairdressers and salon owners | BOP insurance | $75 per month |

| BOP insurance, with E&O coverage added | $95 per month | |

| Workers comp insurance | $90 per month |

Keep in mind that these are just the average costs. Your rates will be very different. Be sure to shop around with a few companies to compare quotes. Working with a top broker like CoverWallet and Simply Business to get and compare several quotes online is a good idea.

What factors affect hairdresser insurance cost?

The cost of hair and beauty salon insurance is based on many factors, from coverage needs and levels to the size and makeup of your staff. For example, a salon with two hairdressers will have a much lower cost to insure than a larger salon with thirty hairdressers.

Your experience also impact the cost of insurance. If you are new, you’ll pay a bit more than an experienced hairdresser.

Location of your salon, the policy terms (coverage limits and deductibles), and your insurance history are important factors in your insurance cost.

How do I get cheap hairdresser insurance?

When it comes to getting insurance, cost is always a factor. Your premium price must fit your budget. However, the cheapest hairdresser insurance may not cover everything you need. Work with your insurance agent or representative at an insurance company, broker, or marketplace to select the right coverages and limits to match your needs and fully protect your business at a price you can afford.

How can I get hairdresser business insurance?

Getting coverage is easier than you expect.

- Do your research. Learning about business insurance doesn’t have to be complicated or time-consuming. As little as 20 to 30 minutes of research or time spent with a business insurance professional could help you identify the coverage you need. You don’t need to become a salon insurance expert, but a basic understanding of the coverage will help you make better decisions with or without professional assistance.

- Evaluate your business risks. Every salon faces unique risks. Once you become familiar with business insurance coverages, figure out which ones will protect your business against the risks it faces.

- Get quotes. Complete applications for the coverages you need with an insurance agent, several online insurers, or an online insurance broker or marketplace.

- Review and purchase. Compare your quotes to find the best combination of coverage and price for your hairdressing business. Before purchasing your insurance, double-check that the provider is legitimate, has strong financial ratings, and positive reviews from its clients. Once you buy your coverage, you should be able to get proof of insurance immediately. You should be able to make changes to your policy when it’s in effect.

- Renewal. A lot can happen to your salon in a year. That’s why it’s essential to review your coverages and get several new quotes before you renew. You may find that you need different or more coverage or that you could get it at a better price.

What information do I need to get a hairdresser insurance quote?

To get an accurate business insurance quote, you’ll need:

- Business location

- Owner information and experience

- Details of business operations

- Gross annual sales

- Number of employees

- Annual payroll

- Subcontractor cost

- Tools and equipment specifics

- Number of claims in the past five years

- Date of claims

- Amount paid to settle each claim

- Age of building

- Salon square footage

- Building construction type

- Building safety features

- Names of other occupants

- Mortgage company information

- Additional insureds

- Lessors for equipment you lease or rent

- Lessor of space where you operate a business.

Having this information handy will help you get more accurate quotes quickly.