As a food vendor, one of the most important things you can do to protect your business is to educate yourself on food vendor insurance and why it’s essential.

The reason is that without the appropriate food vendor insurance, your company is in danger of facing challenges it may not overcome. These challenges could result in the termination of your food vending operation. To avoid this, we have covered all there is to know about food vendors’ insurance in this comprehensive guide. But first, let’s show you the best companies where you can find this policy.

- 6 best food vendor insurance companies

- Who needs food vendor insurance?

- What does food vendor insurance cover?

- How much does food vendor insurance cost?

- How to find cheap food vendor insurance?

6 best food vendor insurance companies

Many insurance companies offer food vendor insurance. After intensive research, here are the top 6 providers that we recommend:

- Simply Business: Best for finding low-cost food vendor coverage

- Next Insurance: Best for fast and affordable quotes

- CoverWallet: Best for comparing online quotes from top carriers

- InsurePro: Best for short-term coverage

- Nationwide: Best comprehensive coverage for any food vending business

- Smart Financial: Best if you prefer working with an experienced agent

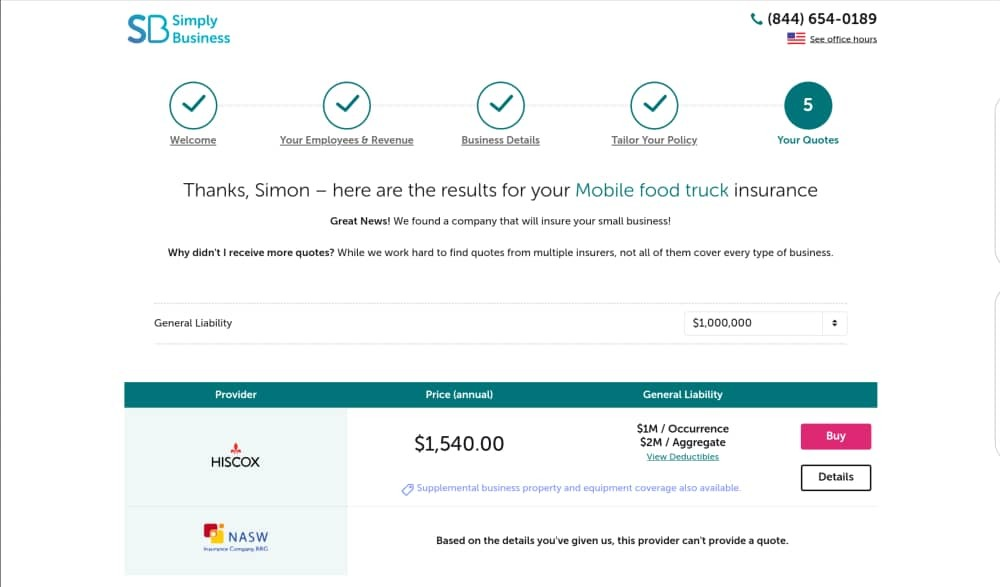

Simply Business: Best for finding low-cost food vendor coverage

Simply Business is a digital insurance marketplace where food vendors can find quotes from insurers. With Simply Business, food vendors can buy insurance online in ten minutes or less, according to their budget. You can also select which features you want in the policy, so they give you something close to your need. Getting a quote from them is simple, and the policy details are always immediately available.

Pros

- Compare quotes from over 20 companies

- Can help companies find discounts

- Easy-to-use platform

Cons

- Not all policy quotes are available online

- You can’t file a claim with Simply Business. You have to do that directly with the insurance company

Next Insurance: Best for fast and affordable quotes

Due to its speedy quote process, diverse coverage options, and affordable rates, Next is the best insurance provider for food cart merchants. If you are working a special event or selling on the street and require direct evidence of insurance, Next allows you to do so online or via its mobile app.

Pros

- Discounts are available

- Online quotes and buying a policy online take about 10 minutes

- The website saves your quotes for later

- A certificate of insurance is available

Cons

- Relatively young insurance provider

- All coverages that a food vendor need may not be available

CoverWallet: Best for comparing online quotes

As an online broker, CoverWallet helps you compare quotes from various insurance providers. The company does not sell its policies; instead, they sell policies from other companies. CoverWallet only partners with the top insurance companies and makes it easy for you to compare several quotes from them in one place

Pros

- Offers quotes for all food vendors

- Generate quotes in less than 10 minutes

- CoverWallet offers online quotes for almost all coverages

Cons

- Sometimes you need to call to get a quote

- Low-cost carriers may not available on the platform

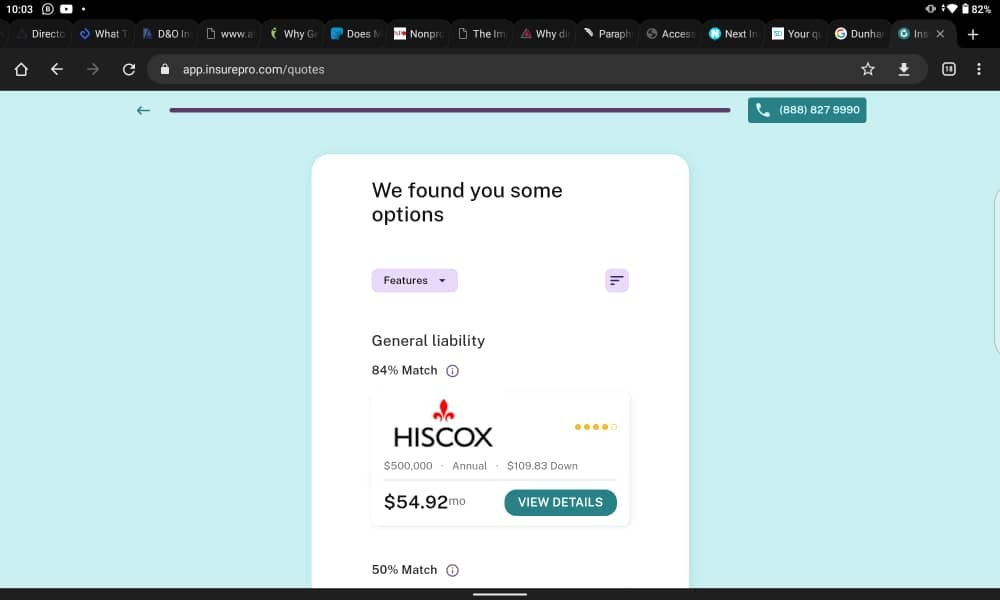

InsurePro: Best for short-term coverage

InsurePro is another digital broker specializing in serving small businesses, including food vendors. Their unique differentiator is short-term coverage, ie. you can buy coverage for just one day, a few days, or a few weeks. You don’t need to always buy an annual policy. They offer quotes comparison for food vendors needing various types of insurance, including general liability and commercial property insurance. Their insurance suits smaller vendors with less than $200,000 in annual sales.

Pros

- Short-term and pay-per-day coverage is available

- Very affordable rates if you don’t need traditional annual coverage

- Excellent digital experience, online quotes, buying a policy, and managing policies online

- Includes new online tools for finding discounts

Cons

- Does not sell their policies

- It is not available nationwide yet

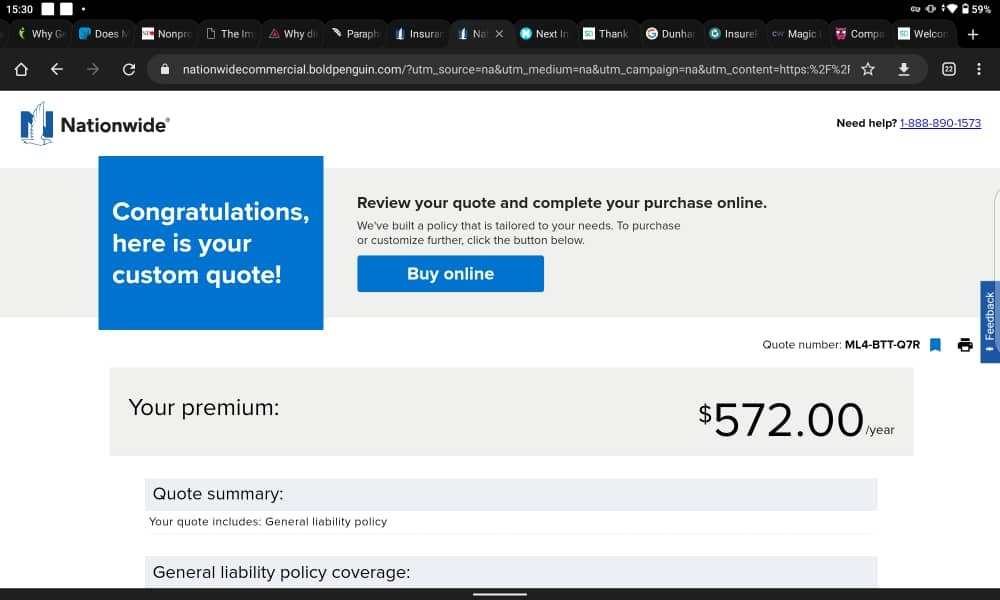

Nationwide: Best comprehensive coverage for any food vending business

Food vending businesses can get insurance coverage from Nationwide. Nationwide offers a wide range of coverages that any food vendor may need. They are an insurance company that has been around for almost a century with a great reputation and financial strength.

The online quote we got below is for general liability coverage for a food vending business located in Houston Texas.

Pros

- A well-established insurance provider with 95 years of expertise in the sector.

- Claim reporting is available through phone, web, and mobile app 24/7.

- Highly rated by A.M. Best and the Better Business Bureau.

- Solid financial security.

- There is coverage in 47 states.

Cons

- Few favorable consumer reviews

- You can get a quote online, but you have to call their agents to buy a policy

Smart Financial: Best if you prefer working with an experienced agent

Smart financial is an online company that provides food vendors with general liability, professional liability, and other insurance coverages that they may need.

Smart Financial works with hundreds of experienced agents who are very knowledgeable in any types of vending business. They will match you with the agent who is the most experienced in your business niche so that they can help you find the right coverages at the most reasonable price.

Whatever type of food vendor business insurance you need, Smart Financial offers it all.

Pros

- Best insurance agencies and companies

- Comprehensive insurance information

- Customized search for insurance policies

- Quick and accurate quotes for insurance policies

- Various insurance types are available

- 24/7 customer service is available

Cons

- You must deal directly with the insurer of your choosing

- You must work with an agent on the phone

- Limited digital capabilities

Who needs food vendor insurance?

Food vendor insurance is a type of insurance that is designed to protect businesses that sell food. Food vendors are businesses that sell food in unconventional places. These include mobile kitchens, food trucks, mobile chefs, party restaurants, caterers, ice cream trucks, hotdog carts, etc.

This type of insurance can help protect businesses from liability in the event that someone becomes sick after eating food that was sold by the business. Food vendor insurance can also help protect businesses from property damage claims in the event that something happens to the food that is being sold.

What does food vendor insurance cover?

Food vendor insurance is an umbrella term referring to insurance policies that protect food vendors from the risks emerging from their food vending operations. Different insurance coverage and policies protect food vendors from different risks and potential lawsuits. Below are the common coverages and policies that food vendors would need:

General liability insurance for food vending businesses

General liability insurance covers common risks, including food poisoning lawsuits and third-party property damage claims (usually to customers and the general public).

This policy is not usually mandatory by the government in most states of the United States. However, event organizers could require food vendors to carry this insurance.

General liability insurance typically protects you from the following:

- Slip and fall incidents around your business premises

- Damaged properties belonging to customers

- Libel and other damages from false advertising, copyright infringement, etc.

Product liability insurance for food vendors

Food vendors need product liability insurance because it covers any damages that may occur as a result of the food that they sell. This covers food vendors from lawsuits when someone gets sick after eating the food. Product liability insurance can help protect the vendor from any legal expenses that may arise as a result of any accidents or injuries that occur.

In many cases, general liability policies include product liability coverage as well. However, many don’t. If you are particularly interested in having product liability protection, you need. to make sure it is included in the general liability insurance policy. If not, you may want to buy a stand-alone policy for the coverage. Product liability insurance costs can be expensive, be sure to shop around to find the right policy.

Business owners’ policy (BOP) for food vendors

A business owner’s policy, sometimes known as a BOP, is an affordable solution for food vendors to combine their general liability and commercial property insurance policies.

Business owners’ insurance may cover you for issues such as the following:

- Physical injuries of customers

- Theft or destruction of food vending equipment

- Occurrences of business interruption

Workers’ compensation insurance for food vendors

Worker’s compensation insurance guards against expenditures associated with work-related accidents that health insurance may not cover. This insurance is vital since most states mandate workers’ compensation for food vendors with employees.

Worker’s compensation insurance typically covers the following:

- Employee health costs

- Disability compensation for employees

- Legal fees for workplace injuries in case of lawsuits

Commercial auto insurance for food vendors

Commercial auto insurance will pay the related expenses if a mobile food vendor’s vehicle is involved in an accident. It is essential since standard auto insurance might not cover your car if you use it for commercial purposes. Each state has its regulations for auto liability insurance. In most states, the policy is crucial for commercial vehicles.

Commercial auto insurance offers when:

- Your business automobile causes property damage

- Causes injuries to another person

- The business vehicle is stolen or vandalized.

Liquor liability insurance for food vendors

Liquor liability insurance covers the expense of property damage, personal harm, and legal costs incurred by an intoxicated customer.

The insurance covers the following:

- Damage to property brought on by drunk customers

- Injuries brought on by drunk customers

- Legal costs for cases involving drunk driving by your customers

How much does food vendor insurance cost?

Food vendor insurance costs depend on the policies you select, the unique risks your business encounters, the value of your organization’s equipment, and several other crucial operational considerations.

The following are some of the average costs of some policies required by food vendors:

- On average, food vendors pay $32 per month or $378 per year for general liability insurance.

- On average, food vendors pay $62 per month or $727 per year for business owners’ coverage.

- On average, workers’ compensation insurance for food vendors costs approximately $100 per month or $1,210 per year.

These are just the averages. Your rates will be different. Be sure to shop around with a few companies to find the cheapest quotes for your food vending business. Working with a broker like Simply Business or CoverWallet is one of the best way to get and compare several quotes in one place.

What factors affect the cost of food vendor insurance?

Insurance providers determine premiums using a multitude of factors. However, of all the elements, the risk exposure your food vending business plays the most significant role.

To properly access your risks, the provider would likely ask questions like the following:

Claim history

Food vendors that have had too many claims in the past tend to have expensive quotes. In some cases, some insurers may not offer them insurance. The general idea is that they will likely have more claims in the future.

Company operations

The types of operations your company conducts will also affect the cost of your insurance. For instance, food vendors that use liquified petroleum gas regularly or have grills are at risk of fire accidents. Therefore, they might pay more for their insurance.

Your company location

The neighborhood where you do your food vending is also essential. If you are in an environment where lawsuits are common, or theft and vandalism are common, you might pay more to cover these risks.

Employee

The number of employees you have will also affect your premium rates. The more employees you have, your premiums will likely be higher. Also, if you employ people without background checks or you employ ex-convicts, you will probably pay more for your insurance.

Business property

The more valuable your business property and equipment are, the more you have to pay to insure them.

How to get cheap food vendor insurance

The following are some ideas that might help you get affordable food vendors’ insurance premiums:

Conduct a risk assessment program

Insurance policies typically cover the risk. Therefore, the first step to getting affordable insurance is considering your risk. After carefully considering the risk factors of your business, you can then match your risks with the required insurance policies.

Check for the best prices

Some insurers offer fantastic coverage options at low prices. If you feel the premium you got from a provider is too pricey, try to find quotes from other providers.

Ask for discounts

Almost all insurers have discounts for their customers. Sometimes it might make sense to ask your provider if they offer discounts. Some discounts you may qualify for include:

- New customer discount

- Discount for credit card payment

- Discount for paying your annual premium in full, etc.

Food business insurance

Food business insurance is a type of insurance policy designed specifically for businesses in the food industry. This insurance covers a wide range of risks that may be encountered in the course of operating a food business, such as damage or destruction to property, loss of inventory due to theft or spoilage, and liability claims.

The coverages that a food business needs may vary depending on their specific operations. Generally speaking, they will need some form of general liability insurance which provides coverage against third-party bodily injury or property damage claims resulting from their operations or products. Additionally, they may want to consider other forms of coverage such as product liability insurance which covers any damages caused by their products; property insurance to protect physical assets; automobile liability coverage if they are using vehicles for their operations; and workers’ compensation coverage for employee injuries.

What kind of insurance coverage does a restaurant need?

A restaurant is a typical food business. A comprehensive restaurant insurance policy usually protects against a variety of risks, including property damage, business interruption, general liability, product liability, workers compensation, liquor liability, and cyber liability. Property damage insurance would cover the physical building in case of an incident such as a fire or windstorm; business interruption provides coverage for lost income due to a covered event; general liability protects against third-party claims such as a customer slipping and falling on the premises; product liability covers against claims related to food-borne illnesses; workers compensation is required to cover employee injuries; liquor liability is necessary if the restaurant serves alcohol and cyber liability covers data breaches and other cyber threats.

Food liability insurance

Food liability insurance is a subset of food business insurance as mentioned above. It is a type of insurance that protects businesses involved in the sale or preparation of food from being held responsible for any illness, injury, or death resulting from the consumption of their food products. It covers medical expenses and damages associated with physical illness and injuries caused by a customer’s consumption of food prepared by the insured business. It can also cover legal costs associated with litigation over such issues.

Food businesses usually get a comprehensive general liability insurance policy customized for food businesses, which usually includes food-borne illnesses, contamination, and spoilage coverage. They can also get a general liability policy and a separate product liability policy as well. The latter option may be a bit more expensive but also more comprehensive.