The one thing that Wisconsin small business owners have in common — whether medical professionals or pet groomers, boutique owners or contractors — is that they face risks doing business every day. The best way to control those risks is with adequate small business insurance.

This article will reveal the 7 best business insurance companies in Wisconsin for different reasons and the pros and cons of each, along with everything you need to know to get insurance coverage to protect your livelihood.

- 7 best business insurance companies in Wisconsin

- What is business insurance?

- Why do I need business insurance in Wisconsin?

- Which business insurance coverage is required in Wisconsin?

- The most popular business insurance policy in Wisconsin

- How much does small business insurance cost in Wisconsin?

- How can I find cheap business insurance in Wisconsin?

- Where to get business insurance quotes in Wisconsin

7 best business insurance companies in Wisconsin

Here are our choices for the best business insurers in Wisconsin for different reasons and the pros and cons of each:

- CoverWallet: Best for comparing quotes

- Simply Business: Best for low-cost coverage

- InsurePro: Best for on-demand and pay-per-day coverage

- Thimble: Best for general liability insurance for small businesses

- biBERK: Best for workers comp insurance

- Progressive: Best for commercial auto and commercial truck insurance

- Hiscox: Best for professional liability insurance

CoverWallet: Best for comparing quotes

CoverWallet makes it fast and easy for busy Wisconsin business owners to get several insurance quotes in one place. CoverWallet makes it possible for you to complete a single application, and it checks with its network of insurance providers to get quotes from them so you can compare them to find the best deal.

PROS:

- Insurance on-the-go.

- Fast and easy online application.

- Multiple quotes from reputable insurers all in one place.

CONS:

- May need to complete an online quote over the phone.

- Not as flexible or customizable as some other insurers.

- Some coverages a not available for all industries or in all locations.

Bottom line: If getting multiple quotes quickly is essential to you, it could be worth checking out CoverWallet.

Simply Business: Best for low-cost coverage

Simply Business was founded in 2005. It specializes in using technology to lower business insurance costs. It’s become an insurer trusted by more than 800,000 small business owners.

PROS:

- Easy to apply for coverage online or get help from a representative over the phone.

- Compare multiple quotes in one place and buy insurance in minutes.

- Expert claims support 24/7.

CONS:

- Relatively new business compared with many other insurers.

- Limited education content.

- Limited availability of niche coverages.

Bottom line: If you want high-quality, cost-effective coverage, it could be worth looking into Simply Business.

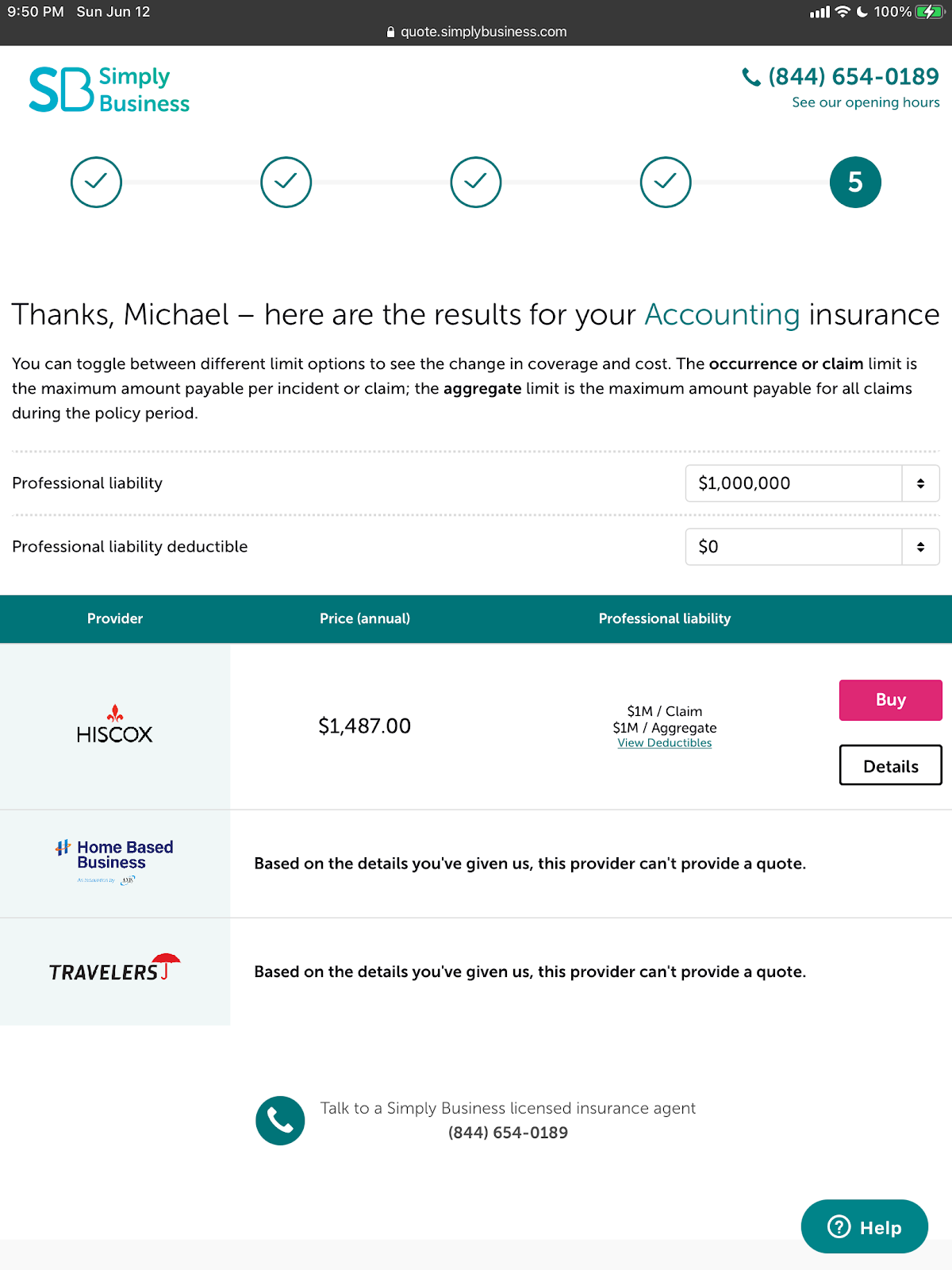

Here is a sample professional liability quote for a Madison accounting business from Simply Business.

InsurePro: Best for on-demand and pay-per-day coverage

InsurePro makes it possible for business owners to access on-demand and pay-per-day coverage.

PROS:

- One-stop insurance shop.

- Able to purchase coverage as needed.

- Complete end-to-end insurance buying experience usually takes less than 15 minutes.

CONS:

- Doesn’t offer as complete a line of coverages as other insurers.

- Relatively new company with a limited track record.

- Little advice and support are available for purchasing coverage.

Bottom line: Ideal for small business owners who don’t need continuous or full-year business coverage.

Thimble: Best for general liability insurance for small businesses

Thimble is an online insurance provider that sells coverage to people who need general liability and other business insurance fast. Thimble does not provide insurance direct. Instead, different insurance companies underwrite its general liability insurance and other coverage.

PROS:

- Good option for businesses that need coverage quickly or temporarily.

- Ideal insurer for business owners who hire contractors and require them to get insurance.

- Top-quality general liability insurance.

CONS:

- Thimble doesn’t underwrite its policies.

- If you need to make a claim, you must contact your insurer, not Thimble.

- Thimble customer service is only available online, which isn’t ideal if you like in-person help buying coverage.

Bottom line: If general liability coverage is critical, you should consider getting it through Thimble.

Unfortunately, when trying to get general liability insurance from Thimble, it’s not offered, so not sure what to do with this section because it’s not factual.

biBERK: Best for workers comp insurance

Do you have many workers you need to cover with workers’ compensation insurance? biBerk could be the ideal insurer for you. It’s a low-cost business insurance provider that specializes in the coverage.

PROS:

- Top-quality coverage at a reasonable price.

- Direct business insurance provider.

- May be able to save 20 percent on workers’ comp and other small business insurance.

CONS:

- Have to get quotes from multiple insurers to compare them.

- Not as flexible as many other small business insurance companies.

- May have to finish an online quote over the phone.

Bottom line: If you need workers’ comp coverage for several employees at a reasonable cost, biBerk could be the answer for you.

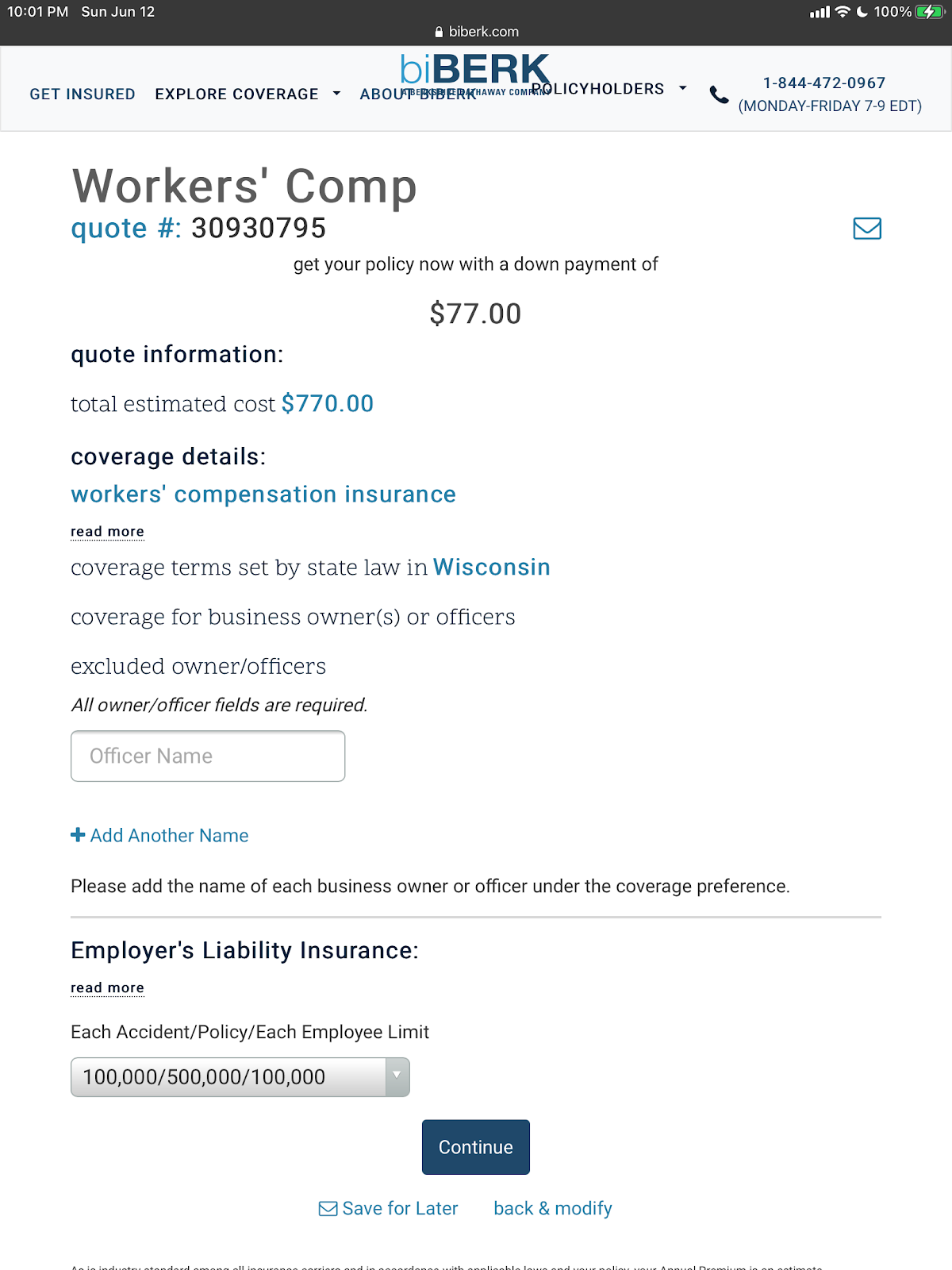

Here is a sample workers’ comp quote for a small accounting business in Madison from biBerk.

Progressive: Best for commercial auto and commercial truck insurance

Progressive has been in business since 1937, offering vehicle coverage beginning day one. It’s maintained its positioning as a leading auto insurer ever since.

PROS:

- Flexible coverage options.

- Great rates for insurance coverage.

- Highly responsive service.

CONS:

- You may not be able to reach a customer service rep immediately.

- You might have to double-check that you receive all the discounts you’re entitled to.

- Not all business coverages are underwritten by Progressive.

Bottom line: If you’re looking for commercial auto coverage, Progressive is worth checking out.

Hiscox: Best for professional liability insurance

Hiscox offers a complete array of business coverages but is known for its professional liability protection. If you work in a profession that provides advice and services, you should check it out.

PROS:

- Easy to purchase all types of business insurance, including professional liability, online or through an agent.

- Top-tier customer service.

- Quick claims processing.

CONS:

- Premium prices may be higher than other insurers.

- Online systems aren’t as up-to-date as other providers.

- May have to complete an online quote with a phone call.

Bottom line: If you’re looking for coverage to protect you against lawsuits related to the work you do, consider getting professional liability insurance and other coverage from Hiscox.

What is business insurance?

Business insurance, also known as commercial insurance, helps protect business owners from unexpected losses.

There are many types of business insurance options to help cover your operation for property damage, legal liability, and employee-related risks.

What is business insurance for?

Business insurance can help you control your company’s considerable risks. It provides you with financial protection against losses that occur while conducting business. When you have business insurance coverage, your insurer helps pay the costs of covered losses up to the limits of your policy. Without coverage, you might have to pay out of pocket.

Why do I need business insurance in Wisconsin?

The purpose of the insurance is to help protect your Wisconsin company from common risks most businesses face, along with industry-specific ones. It can protect the financial assets of your company, its physical property, employees, and intellectual property from:

- Lawsuits

- Property damage

- Theft

- Vandalism

- Income loss

- Employee injuries and illnesses

- And more.

Which business insurance coverage is required in Wisconsin?

Some business insurance coverage are required by law in Wisconsin, some are not. Below are the business insurance coverage legally required in Wisconsin:

Workers comp insurance is required in Wisconsin

You must have workers’ comp insurance as soon as your business hires a third employee or if you employ one or more full-time or part-time employees and you pay them combined gross wages of $500 or more in any calendar quarter for work done in Wisconsin.

This insurance provides benefits to your employees to help them recover from work-related injuries or illnesses. Some examples of these include:

- A clerk at your shop slips off a ladder and breaks her leg while stocking shelves. It makes her unable to do her job.

- An administrative assistant in your office has been working on a computer while sitting on a cheap old chair. It causes her to come down with carpal tunnel syndrome. She can no longer do her job because of the stiffness and discomfort.

- A carpenter at your kitchen cabinet manufacturing operation has been inhaling sawdust and chemical odors for years and comes down with lung disease. His doctor will not allow him to return to work.

Workers’ comp also pays funeral expenses and death benefits to immediate family members should an employee pass away because of a job-related incident. It also pays for job retraining when people can’t return to their usual duties because of a workplace injury or illness.

Learn more at workers comp insurance cost and the best workers comp insurance companies

Commercial auto insurance is required in Wisconsin

If you use a vehicle for business purposes, you need to have commercial auto insurance. Your personal auto insurance doesn’t cover it if you are driving for business reasons and involved in an accident.

Commercial auto liability insurance pays for damage to vehicles and the cost of medical care for others if you or an employee is involved in an accident while driving for business reasons. Similar to personal auto insurance, commercial auto insurance could also include other related coverage such as comprehensive, collision, underinsured and uninsured motorist, gap, etc.

Learn more at commercial auto insurance cost and the best commercial auto insurance companies

Other types of business insurance in Wisconsin

Some of the most common types of business insurance coverage small companies in Wisconsin purchase include:

- Commercial liability or general liability insurance helps protect your business from injuries that happen to non-employees in your workplace or property damage caused by your employees when doing their jobs. This includes customer injuries resulting from a slip and fall in your workplace or client property damage that occurs because of a work incident in a client’s home. Learn more at general liability insurance cost and the best general liability insurance companies

- Commercial property covers losses in your workplace resulting from things like weather damage, fire, theft, or vandalism. Learn more at commercial property insurance cost and the best commercial property insurance companies.

- Professional liability covers you and the people who work for you if a client sues you for giving them bad advice or not performing services that meet their expectations. Learn more at professional liability insurance cost and the best professional liability insurance companies

- Business income interruption helps replace some of your business income if your company cannot operate for reasons covered by your insurance.

- Product liability covers you if a product you manufacture or sell is faulty and doesn’t perform as intended, and you’re sued because of it. Learn more at product liability insurance cost and the best product liability insurance companies.

- Cyber insurance helps pay expenses related to the theft or loss of customer, employee, or business information. Learn more at cyber insurance cost and the best cyber insurance companies

- Directors and officers will help pay legal expenses and damages if a director or officer at your company is sued because of a business-related decision. Learn more at D&O insurance cost and the best D&O insurance companies

The most popular business insurance policy in Wisconsin

A Business Owners Policy (BOP), one of the most popular policies purchased by Wisconsin small business owners, will help protect your business property, income, and financial assets. A BOP typically includes three types of coverage:

- Business property coverage protects the buildings your business operates out of, whether you own or rent them, along with the equipment used to run your company housed in them. This includes your:

- Physical location

- Parking lots and outdoor spaces

- Computers

- Inventory

- Supplies

- Tools

- Desks, file cabinets, and other furniture

- And more.

- General liability insurance protects your business against legal claims related to:

- Injuries that happen to non-employees on your business properties

- Damage to other people’s property caused by you or your employees that occurs while working

- Reputational harm, such as libel and slander, caused by you or your workers.

- Business income insurance (often referred to as business interruption coverage) helps replace a portion of lost income if you can’t operate your business for a reason covered by your business policy. This includes damage from fire, wind, weather events, vandalism, and burglaries.

Depending on the specific needs of your business, you can work with your insurance agent or company rep to figure out what other coverages you may need.

How much does small business insurance cost in Wisconsin?

The average cost of a $1M general liability insurance policy for small businesses in Wisconsin is $76 per month, or $912 per year. Most small businesses in Wisconsin pay between $40 to $250 for a general liability insurance policy.

The average cost of $1M BOP policy for small businesses in Wisconsin is $126 per month, or $1,512 per year.

Different business insurance coverage has different rates for small businesses in Wisconsin. The more coverage you need, the more expensive your business insurance policy is.

These are just the averages. Your rates will be different. Be sure to shop around with several companies or work with a top broker like Simply Business, InsurePro, or CoverWallet to compare several quotes to find the cheapest one for your business.

Factors that impact small business insurance cost in Wisconsin

Premium costs can vary dramatically because they’re based on so many factors, including:

- The limits and coverage types you choose

- The age and value of your business property, along with its safety features

- The contents of your property, including equipment, inventory, and supplies

- Your business type and industry

- Whether or not you choose full or partial replacement cost

- Where in Wisconsin your business is located

- The insurer and how it calculates premium costs

- And more.

What’s important is that you get quotes from multiple providers to compare coverages and costs to get the best combination for your Wisconsin business.

How can I find cheap business insurance in Wisconsin?

Here are my top tips to help you find the insurance you need at an affordable price:

- Shop around. Get quotes from a few companies or compare the multiple quotes from an insurance marketplace or broker.

- Take advantage of discounts. If they’re not offered to you when getting a quote, ask about them, whether you’re buying online or through an agent.

- Choose the right coverage: The more coverage that you need for your business, the more expensive your business insurance policy is

- Choose the right policy details: Coverage limits and deductibles of your policy impact your policy’s premiums. Be sure to choose the right policy’s details to avoid overpaying.

- Safety-first operation: Make sure you follow all safety standards and protocols in your industry. Have regular machinery and factory maintenance and conduct safety training for your employees annually.

These steps will help ensure you’re not paying too much for your business coverage.

Where to get business insurance quotes in Wisconsin?

You can choose to get business insurance quotes online or through insurance agents or brokers in Wisconsin. If you prefer getting business insurance quotes online, below are some carriers and digital business insurance brokers that offer quotes online for different coverage:

- General liability insurance: CoverWallet, Simply Business, InsurePro, NEXT, Thimble

- Business Owners Policy (BOP): CoverWallet, Simply Business, and Thimble

- Commercial auto insurance: Progressive, biBERK, THREE, and InsurePro

- Workers comp insurance: CoverWallet, Simply Business, InsurePro, Pie, and Cerity

- Professional liability insurance: CoverWallet, Simply Business, NEXT, and Thimble