Liability insurance is a type of insurance that businesses purchase to protect themselves from any legal action that may be taken against them. This type of insurance can help protect the business from any financial damages that may be awarded to the plaintiff in a lawsuit. There are a few different types of liability insurance that businesses can purchase, and each one offers different protections. Some of the most common types of liability insurance include product liability insurance, general liability insurance, and professional liability insurance.

These business liability insurance policies usually have $1M coverage limit. And they cost differently. In this article, we will examine how much each $1M policy costs.

- How much does $1M business liability insurance cost?

- How much does $1M professional liability insurance cost?

- How much does $1M product liability insurance cost?

- How much does $1M D&O insurance cost?

- How much does $1M commercial umbrella insurance cost?

- Factors that affect the cost of $1 Million business liability insurance

- How can you get cheap $1 million business liability insurance?

- What does business liability insurance cover?

How much does $1M business liability insurance cost?

Among the business liability coverage, general liability insurance is the most common one. In most cases, the word “business liability insurance” usually refers to business general liability insurance or commercial general liability insurance. If small businesses can only afford one policy, most insurance experts advise them to get a general liability policy.

On average, business owners spend between $20 to $300 a month, or $240 to $3,600 a year, for a $1M general liability insurance policy. This is a wide range, the reason is the cost of business liability insurance varies based on several factors that we are discussing in detail below.

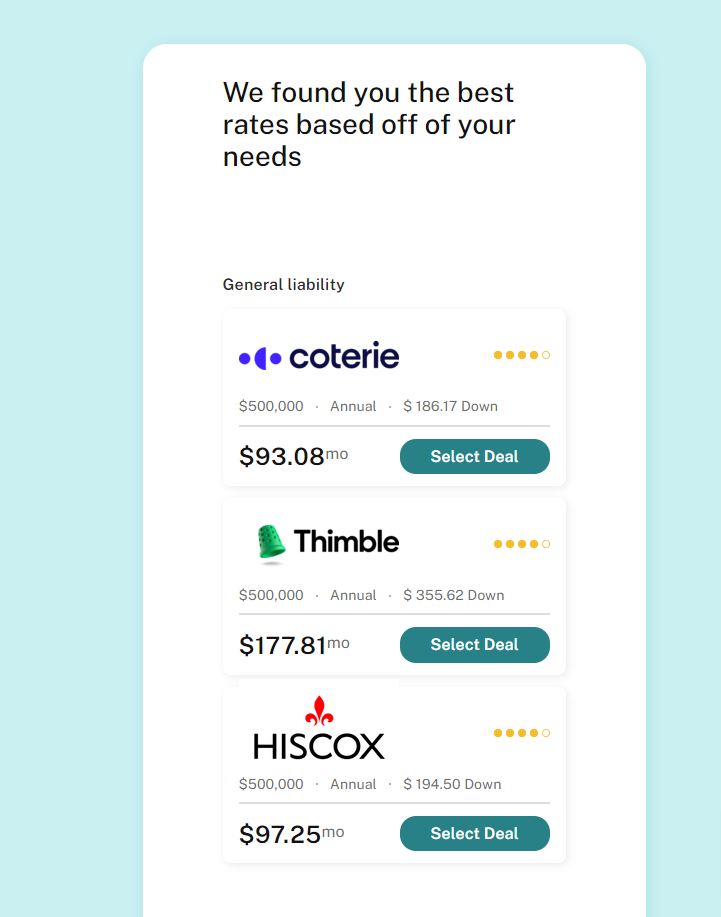

Below are some sample quotes we got from the three top providers of general liability insurance for small businesses:

- InsurePro, a broker specializing in providing affordable coverage with their on-demand short-term coverage. You can easily compare several quotes on InsurePro platform.

- NEXT: a digital carrier selling policies directly to small and micro businesses.

- CoverWallet: One of the best brokers if you want to compare several quotes online from top-rated carriers

- Simply Business: Best for finding low-cost coverage. Simply Business is a broker specializing in helping small businesses find low-cost coverage by working with several carriers with reasonable rates

How much does $1M professional liability insurance cost?

After general liability, professional liability insurance is the second most common policy among small businesses. Some may even argue it is the most popular policy for businesses that are selling their advice or services. It is also called E&O insurance.

The average cost of professional liability insurance for small businesses is $37 per month, or $444 per year. Most small businesses pay between $19 to $78 per month for their policy.

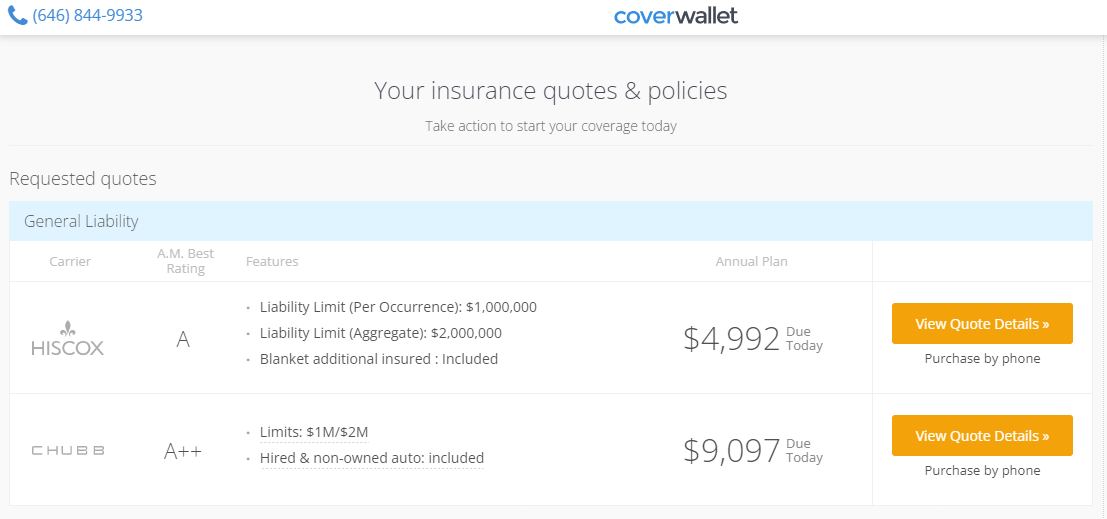

Below is a sample quote we got from Simply Business for a bundled policy: general liability and professional liability. CoverWallet is a small business insurance broker. They are one of the best brokers if you want to compare several quotes online to find the cheapest quotes. Their platform is optimized to find the cheapest coverage for your business.

Learn more about the cost of professional liability insurance

How much does $1M product liability insurance cost?

The third most popular business liability insurance policy small businesses need to have is product liability coverage.

Product liability insurance is a type of insurance that helps protect small businesses from the risks associated with manufacturing, selling, and distributing products. This type of insurance can help protect businesses from lawsuits that may arise due to product defects or injuries caused by products. Product liability insurance can also help protect businesses from the costs associated with recalls or product recalls.

This type of insurance is typically relatively affordable, and it can be a valuable tool for small businesses looking to protect themselves from the risks associated with product sales.

The average cost of a $1M product liability insurance policy is $45 per month or $540 per year. Most small businesses pay between $30 to $100 per month for their policy.

Many insurance companies offer bundled policies combining general liability and product liability coverage in one single policy. This will help you reduce the cost of these two coverage. Ask your agent or broker if their company offers bundled coverage.

Learn more at product liability insurance costs and the best product liability insurance companies

How much does $1M D&O insurance cost?

D&O insurance is considered a business liability coverage because it helps protect the company from financial losses that could occur if directors and officers of the organization are accused of wrongfully taking actions that have negative consequences for the business.

D&O insurance can help protect a business from losses related to wrongful actions by directors and officers, including allegations of fraud, securities violations, and other improper business practices. In addition, D&O insurance can help pay for the costs associated with defending against such allegations.

The average cost of a $1M D&O insurance policy is $103 per month, or $1,236 per year. Most small businesses pay between $42 to $178 per month for their policy.

Learn more at D&O insurance costs and the best D&O insurance companies

How much does $1M commercial umbrella insurance cost?

Commercial umbrella insurance is a type of liability insurance that provides businesses with additional coverage above and beyond their existing liability policies. This coverage can help protect businesses from potential losses resulting from things like third-party lawsuits, property damage, and bodily injury.

Small businesses often need commercial umbrella insurance because their underlying policies may have relatively low limits. For example, a business’s general liability policy may have a limit of $1 million per occurrence, but a single lawsuit may cost $1.5 million in total. In that event, commercial umbrella insurance policy will help cover the $500,000 expense from the lawsuit. Without it, the business has to pay out large sums of money, which may put it in financial jeopardy.

The average cost of a $1M commercial umbrella insurance policy for small businesses is $1,500 per year. Most businesses pay from $900 to $2,700 per year for the coverage.

Learn more at commercial umbrella insurance costs and the best commercial umbrella insurance companies

How much does $1M cargo insurance cost?

If you are an owner of a small trucking business or an independent owner-operator trucker, you know that many shippers or brokers require you to have cargo insurance. Even if they don’t, you should still have it to protect yourself if something happens to the cargo that you are hauling.

When a broker requires you to have cargo insurance, they usually require a policy with $1M coverage limit, which is relatively expensive. Most cargo insurance policies have $50K to $250K coverage limits.

In our research, the average cost of a $1M cargo insurance policy is $410 per month or $4,920 per year. Most owner-operator truckers pay between $350 and $620 per month based on the cargo types that they haul and other factors.

Learn more at how much does $1M cargo insurance cost

Factors that affect the cost of $1 Million business liability insurance

This is how insurance coverage works: the greater the risk, the higher the premiums. To access risk, insurance companies work with some factors including the following:

Location

Insurance prices vary by state (and sometimes zip code). If you own a business in Los Angeles for instance, you will undoubtedly receive more foot traffic than if you operated a modest store in Orange County in Florida. As a result, the company in Los Angeles may pay more for its business liability insurance even though it’s still the same business as the one in Orange County in Florida and has the same $ 1 million limit.

Public interaction

The greater your business’ public interaction, the greater your premises’ liability exposure. It essentially suggests that there is a greater likelihood of individuals becoming injured at your place.

Construction companies, real estate agents, cleaning companies, and landscapers have some of the highest liability insurance premiums. This is because they perform a significant amount of work involving other people’s property.

Virtual client meetings completely eliminate the possibility of a premises liability claim. The likelihood of claims increases, however, if you hold in-person customer meetings at your office.

Your profession

The cost of commercial liability insurance is virtually usually influenced by occupation. What you do for a living will affect the amount of daily risk you confront. The greater your risk exposure, the more likely you are to file a claim.

For example, a retailer’s business liability costs will increase due to increased foot traffic. A freelancer who works from home, however, will have significantly less visibility and so their liability insurance premiums will be less expensive even though it’s the same $ 1 million limit.

Sales and revenue

Insurance companies use sales and revenue as risk measurement tools. This is because more sales likely mean your business has more customers. Since business liability insurance protects against claims for third-party personal injury and property damage, more claims result in a higher premium.

Deductibles

Your policy’s deductible is the amount of money you are willing to pay to cover an incident. Usually, the insurer collects this fee before paying your claims. The level of your policy’s deductible determines the cost of your company liability insurance. Selecting a lesser deductible would mean you would pay a higher premium.

Coverage details

You can add optional coverages to your business liability insurance policy. However, this will result in a higher insurance premium because your firm will be more protected.

Years of experience

The greater your business’s experience, the lower your business insurance premiums might be. There is a higher chance of liability claims among newer enterprises; hence their rates may be higher.

History of claims

The more claims you have had in the past, the more likely you will have high premiums. If you have not caused any customer injuries or property damage, your business liability insurance premium will likely be lower.

How can you get cheap $1 million business liability insurance?

If you feel your $ 1 Million business liability insurance is a bit expensive, the following ideas might help you cut costs:

Shop around to compare several quotes

The number one rule in getting cheap insurance is to shop around with a few companies or work with a broker to compare several quotes to find the cheapest one for you. Getting quotes from several companies can be time-consuming. Working with a broker such as InsurePro, Simply Business, and CoverWallet is an easy and convenient way to compare several quotes online.

Pay the complete premium upfront

The premium for your general liability policy can typically be paid monthly or annually. It may be tempting to choose a lower monthly premium, but you should consider paying the whole amount. Many insurers give discounts on annual premiums, allowing businesses to typically save money in this manner.

Bundle your insurance policies

When purchasing numerous policies from the same insurance provider, businesses might occasionally receive discounts. For instance, if your business is deemed low risk, you may be eligible for business owner’s insurance. A BOP combines general liability and business property insurance at a discounted rate.

Manage your business risks well

If your small business has a claim-free past, you might anticipate cheaper insurance premiums. Developing a comprehensive risk management plan is an efficient means to achieve this objective. For instance, you could:

- Compile guidelines for social media posting

- Create a comprehensive training program for employees.

- Develop procedural checklists and evaluations.

- Purchase a security system.

- Reduce dangers on your property

What is a $1 million business liability insurance?

Business liability insurance is also known as general liability insurance and commercial general liability insurance. This type of insurance can assist in shielding your company from legal action by third parties alleging that it was responsible for their bodily injury or property damage.

The $1 million refers to the limit of the policy, which is the maximum amount your insurer is willing to pay for covered perils. In this case, the maximum you can get for any claims under your $1 million business liability policy is $1 million.

Business liability lawsuits may arise while conducting your regular activities and result in significant financial losses. If you don’t have insurance, you’ll have to pay for your legal defense out of pocket.

What does business liability insurance cover?

Your business liability insurance policy may be able to assist in covering issues such as:

Property damage

If you accidentally damage a customer’s property, your general liability insurance will pay for the repairs or replacements. If a customer does sue you for damages, your policy may cover those damages and the legal fees whether the lawsuit is successful or not. It may also protect you if there is damage to your rented property that happened by accident or through a natural disaster like a lightning strike, a fire, or an explosion

Third-party accidents

This insurance shields the policyholder from liability for claims involving bodily injury, damage to property, and accidents to third parties. You are protected if a visitor to your property sustains an injury while they are there.

Third parties here refer to anyone asides from you and your staff. The policy will pay for medical expenses for anyone wounded due to your company’s actions.

For instance, someone slips and twists their ankle on your property due to wet floors. Of course, you could argue that if they were attentive enough, they could have spotted the wet floors.

However, the law in most states holds property owners responsible for making their environment safe enough. Such a person can therefore sue you for having a dangerous environment that caused their injury. Technically, you are liable for your actions.

If the injured party asks you to pay for their medical expenses, your insurance might cover their bills. Your business liability insurance will protect you in such instances when those injured by your company’s activities are not your staff.

Protection for tools and equipment

Adding contents coverage to your commercial general liability insurance policy may, in some instances, cover the expense of replacing or repairing items and equipment that have been stolen or lost.

Claims related to advertising or personal injuries

This coverage protects against things like slander, which may harm a business. This policy is vital for those just starting out in their respective industries. This coverage pays for injuries or errors in advertising, such as violations of copyright in your promotional materials. It may also offer protection if someone files a lawsuit against you for making defamatory or slanderous claims.

For instance, a competitor claims that your ad on Facebook passes the wrong information about their company. This policy will help you cover the needed legal bills

Product liability

Your business liability insurance can cover you if a customer discovers a defect in one of your products. Under the terms of this coverage, products are considered defective when they do not perform as promised by the manufacturer. For instance, you sell a freezer that claims to keep items frozen for 3 days after a power outage. However, your client claims your freezer only kept its goods frozen for 12 hours after a power outage. Your product liability insurance might cover you in such situations.