Professional liability insurance is also called errors and omissions insurance, or sometimes malpractice insurance if you work in healthcare. Here are the top five companies we recommend for professional liability insurance in California.

- Top 6 Providers of Professional Liability Insurance in California

- What is Professional Liability Insurance?

- Why do I Need Professional Liability Insurance in California?

- How Much does Professional Liability Insurance Cost?

- What does Professional Liability Insurance Cover?

- What doesn’t Professional Liability Insurance Cover?

- How Much Professional Liability Insurance do You Need in California?

Top 6 Providers of Professional Liability Insurance in California

We researched 12 different companies providing professional liability insurance in California and here are our recommendations of the top 6 providers.

- CoverWallet – Best for comparing online quotes

- Hiscox – Best Overall

- CNA – Best for malpractice insurance

- Embroker – Best for legal companies

- Vouch – Best for startups

- Biberk – Best for small businesses

CoverWallet: Best for comparing online quotes

CoverWallet is a digital broker specializing in business insurance. They work with several leading business insurance companies such as Hiscox, Chubb, Liberty Mutual, etc. They are not an insurer. As a broker, they can provide you with several quotes from their partner companies.

After you fill in the lead form on their website, within a few minutes, they will be able to provide you with several quotes so that you can compare and select the best and the cheapest quote for your situation.

If you buy a professional liability insurance policy through them, you will be able to use their great digital dashboard, free, to manage all of your business insurance policies in one place conveniently.

Hiscox – Best Overall

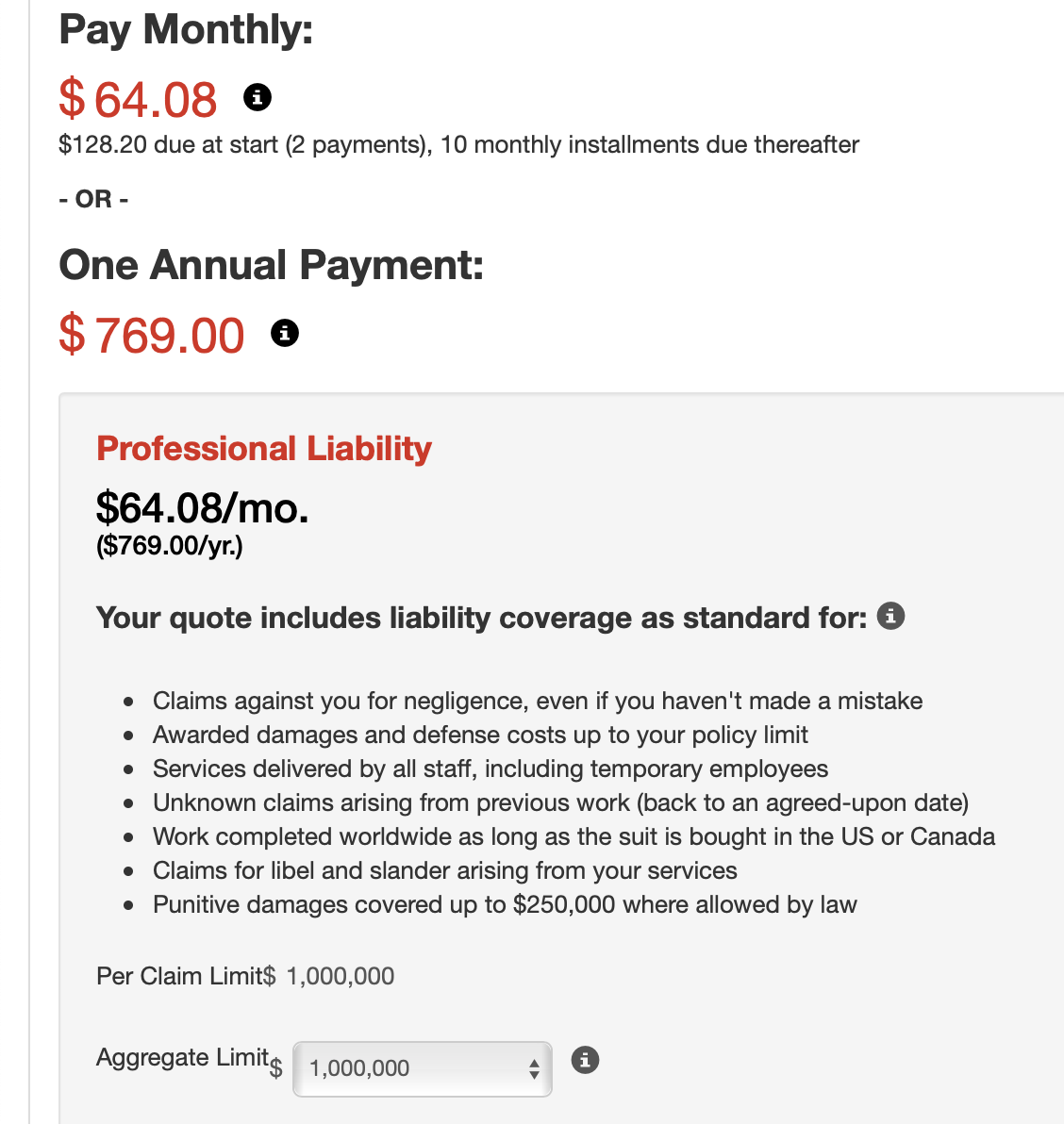

Hiscox features fast online quoting and flexible policies that can grow with your business. You can get covered almost immediately. They cover many different types of businesses, and they have excellent online reviews. Over 300,000 people have chosen to insure their business with Hiscox. You can get a discount for bundling, too. Online quoting is generally a breeze. For the quote below we said we were a business consulting firm with $150,000 in revenue.

CNA – Best for malpractice insurance

CNA has coverage limits of up to $5 million dollars and can cover almost any profession. You can pay your bill online, and they have excellent financial strength. You can pay a bill and report a claim online, but there is no online quoting. They are an excellent choice for malpractice insurance if you work in the health care field.

Embroker – Best for legal companies

Embroker has a tech startup package where you can get E&O, D&O (directors and officers), EPLI (Employment practices liability) and cyber insurance in the same bundle and save 20%. They also have legal professional liability insurance, which can be processed in less than ten minutes, which is unheard of for legal liability. Embroker has an office in San Francisco, so they understand your California business. You can get a quote online in about 60 seconds.

Vouch – Best for startups

Tech and other startups should look into Vouch. Everything is done entirely online, and you can get insurance in less than ten minutes, leaving you free to do other things. They offer ten different types of business insurance, so if you need more than E & O insurance, they can accommodate you. They have top-rated attorneys you can consult should a lawsuit be filed against you.

Biberk – Best for small businesses

Biberk offers small businesses cost-effective insurance. They have the amazing financial backing of Berkshire Hathaway, and they sell policies to you directly (no insurance brokers). This saves money—up to 20%. They’re available nationwide and insure a wide variety of industries. If you decide you need more than professional liability, they can offer you that, too.

What is Professional Liability Insurance?

Professional liability insurance covers you for any errors or mistakes you make that cause harm to a client. Sometimes it’s called errors and omissions insurance, and if you work in healthcare, its called malpractice insurance. Anyone who provides a professional service should get professional liability insurance, including:

- Lawyers – Top 5 Providers of Legal Malpractice Insurance & How Much It Costs

- Accountants – Professional Liability Insurance (E&O) for Consultants, Investment Advisors, and Other Financial Professionals

- Doctors – The 5 Best Providers of Medical Malpractice Insurance

- Consultants – Professional Liability Insurance (E&O) for Consultants, Investment Advisors, and Other Financial Professionals

- Real estate agents – Top 5 Providers of Real Estate E&O Insurance & Costs

- Insurance agents – E&O Insurance for Insurance Agents: Cost and Top 5 Providers

- Engineers – Top 5 Providers of Professional Liability Insurance for Architects and Engineers

- Marketing and advertising services

- Psychologists – Top 4 Providers of Malpractice Insurance for Psychologists and Counselors

- Nurses – The Best 4 Providers of Nursing Malpractice Insurance

- Dentists – Top 5 Providers of Dental Malpractice Insurance

- Physical Therapists – The 6 Best Malpractice Insurance Providers for Physical Therapists

- Chiropractors – 4 Best Choices for Cheap Chiropractic Malpractice Insurance

Basically, anyone who has special training and provides this special training to clients for a fee should look into professional liability insurance.

Why do I Need Professional Liability Insurance in California?

Professional liability lawsuits are expensive. Since anyone can make a mistake, it’s easy to see why you should get professional liability insurance. For example, if you’re an accountant and give a client poor advice that causes them to lose money, they could sue you.

And of course, you don’t actually have to have made any mistakes—your client could just be unhappy because something didn’t go their way. These lawsuits are expensive and troublesome. Professional liability insurance will take some of the worry off of your shoulders.

In California, so far malpractice insurance for lawyers is not required, but they keep batting around the idea. For now, if you do not have malpractice insurance you must disclose this fact to your clients in writing if your representation of them will be longer than four hours.

How Much does Professional Liability Insurance Cost?

According to Insureon, the average cost of professional liability insurance is about $59 a month. If you’re a doctor and need malpractice insurance, the average cost is about $8,274 a year, with obstetricians paying as much as $150,000.

Even for the same customer, different providers quote different prices. It is always a good idea to shop around with a few insurance companies or work with a digital broker like CoverWallet to compare several quotes to select the best one for your situation.

What does Professional Liability Insurance Cover?

Professional liability insurance covers:

- Alleged or actual negligence

- Defense costs

- Mistakes you make that cause someone to suffer financially

- Breach of contract

For example, say you are a tax accountant and make a mistake on your client’s account. Tax laws are extremely complex, and it’s easy to miss something. However, your mistake causes your client to file taxes incorrectly and they incur penalties. You would be sued for your error.

What doesn’t Professional Liability Insurance Cover?

Professional liability insurance doesn’t cover everything. It won’t cover:

- Bodily injury

- Malicious acts

- False advertising

- Illegal activities

- Defamation

Some of these things are covered by other types of insurance, such as bodily injury. Anything illegal or malicious is not covered by any type of insurance.

How Much Professional Liability Insurance do You Need in California?

It depends on a few factors, such as:

- Type of industry you work in

- Number of clients

- Number of employees

- Level of risk

If you have a small business, a $1 million occurrence limit/$1 million aggregate policy is very common. This means $1 million per occurrence and $1 for the lifetime of the policy, which is usually a year. Although this is a common policy, you may want to take to a financial advisor to discuss your specific needs.

California does not place caps on liability lawsuits, so businesses in California should especially seek out professional liability insurance. The sky is the limit when it comes to how much people can sue for—they may or may not get it, but its nerve racking all the same.

>>MORE: Top 6 Providers of General Liability Insurance in California

>>MORE: Top 6 Providers of Workers Compensation Insurance in California