If you have children, you’ve probably heard of Gerber Life Insurance. Their “Grow-up” plan is targeted to families with infants and small children. The odds are they mailed you information soon after your child was born.

But did you know they have other life insurance products as well? They have a full array of insurance products for your whole family. Let’s take a look at the company as a whole.

- Pros and Cons

- Products offered by Gerber Life Insurance: 60/100

- Financial Strength Rating of Gerber Life Insurance: 90/100

- Consumer Complaints of Gerber Life Insurance: 80/100

- Customer Satisfaction Rating of Gerber Life Insurance: 80/100

- Digital Experience Rating of Gerber Life Insurance: 70/100

Pros and Cons

| Pros | Cons |

| – Most people won’t need a medical exam – Easy to get a quote – Everyone is accepted – Limited underwriting – Easy online application process | – Because almost no one is required to have a medical exam, premiums are high – Cash value builds very slowly – Better ways to save for college – Children don’t need life insurance |

Products Offered by Gerber Life Insurance

Gerber is best known for the Grow-Up plan. This is a whole life insurance plan for children ages 2 weeks to 14 years. A big selling point is that coverage doubles at the age of 18—if you buy a $25,000 policy, it automatically becomes a $50,000 policy when the child turns 18. You can get life insurance for your child from $5,000 to $50,000. They also offer a whole life policy for teens ages 15-17, although it’s not as popular.

>>MORE: Life Insurance for Children: Is It Worth It?

Gerber also has:

- Guaranteed Issue Life insurance

- Term Life insurance

- Whole life insurance

- Accident Protection

- Gerber Life College Plan

Guaranteed-issue Life Insurance: Gerber Life also offers guaranteed-issue life insurance for older adults ages 50-80. Acceptance is guaranteed and your policy can’t be canceled as long as you pay the premiums. There are no medical exams required and everyone is accepted, which makes it an attractive option for people who can’t get life insurance any other way (for example; people with serious health issues).

This is a whole life policy, so it does build some cash value, but coverage amounts are low: from $5,000 to $25,000.

Term Life Insurance: You can buy term life insurance from Gerber Life in amounts up to $300,000. Terms are 10, 20, or 30 years. Most people who apply don’t have to take a medical exam, unless you’re over 51 and applying for more than $100,000 worth of coverage.

Whole life insurance: Whole life plans are available in amounts of $50,000 to $300,000. As with the term insurance, if you’re over 51 and applying for a policy more than $100,000 there is a required medical exam, but most people will not need one.

Accident Protection: This provides protection against accidental death or a listed disabling injury. Coverage is available in amounts from $20,000 to $100,000 and there is a cash benefit which can be used to cover out-of-pocket medical costs, lost wages, or other expenses. Approval is guaranteed for those 19 to 69 years old.

Gerber Life College Plan: Gerber markets this as a savings plan that also provides adult life insurance. It’s a whole life insurance policy that pays out at a certain date, or when the insured dies, whichever comes first. Many people choose the pay-out date to coincide with high school graduation. Coverage is available in amounts from $10,000 to $150,000.

If you borrow against any whole life insurance policy with Gerber, they charge you an interest rate of 8%, which is higher than many other companies.

Financial Strength Rating of Gerber Life Insurance

A.M. Best, which rates companies based on financial strength, gives Gerber Life insurance an A, or excellent. You can rest assured that Gerber won’t go bankrupt before paying your claim.

Consumer Complaints Rating of Gerber Life Insurance

The NAIC gives a ratio to every company based on how many consumer complaints are lodged against them. They come up with a ratio. A ratio of 1.0 means a company has exactly as many complaints as you would expect for a company of its size. A score of 2.0 would mean twice as many complaints. For individual life plans, Gerber earned a score of .54, which means they receive a comparatively low number of complaints.

Customer Satisfaction Rating of Gerber Life Insurance

J.D. Power does an insurance study every year, ranking all of the largest companies on parameters such as customer service, price, and product offerings. However, Gerber Life insurance is not on their list.

The Better Business Bureau (BBB) gives Gerber Life insurance an A+ rating, although it is not accredited by the BBB. What does this mean? It could mean a few different things:

- Gerber Life didn’t pay the BBB a fee in order to be accredited

- Gerber Life does not meet the standards set forth by the BBB

It’s hard to tell which of these is true. Let’s look at the complaints listed on the BBB’s website.

There are eleven negative reviews listed, 88 complaints closed in the last three years. Of those complaints that have text, several complain about communication from the company. Some thought the Gerber Grow Up plan and the Save for College plan were the same thing (they are not). A few people commented on the difficulty of cancelling a policy.

If you enter into a contract with any insurance company (or any contract at all) you need to read the policy carefully. Be sure you understand what you’re getting and don’t be afraid to ask questions. If you don’t like the answers the company gives, or if they fail to answer at all, shop around.

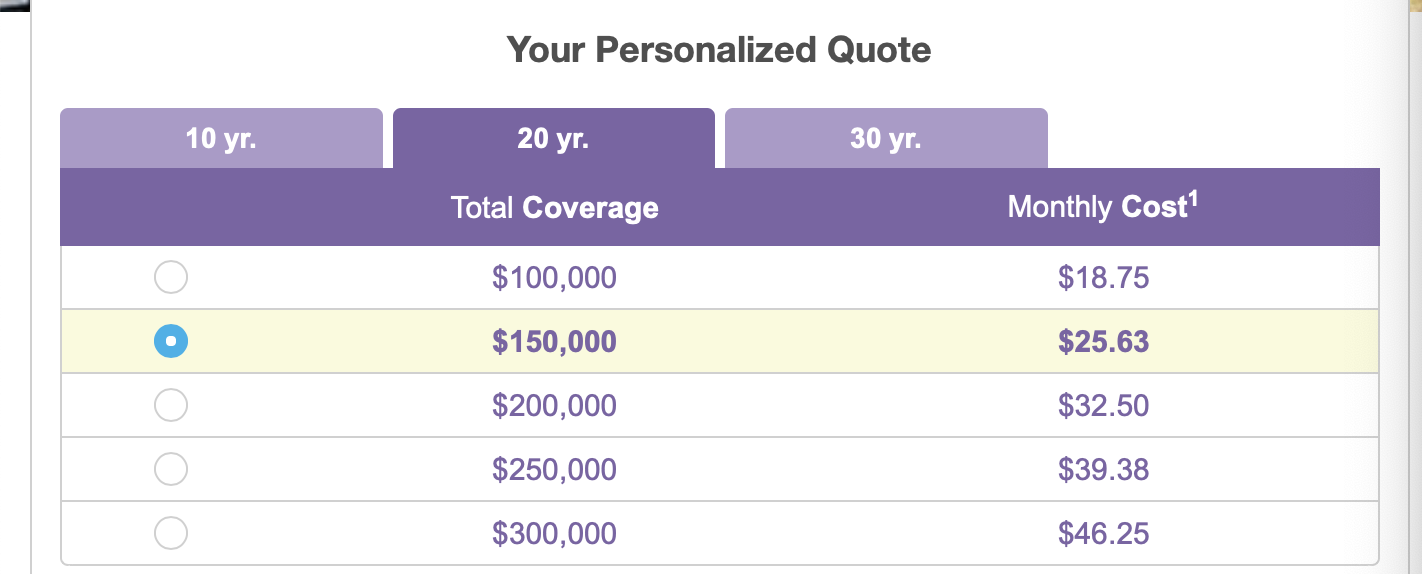

Digital Experience Rating of Gerber Life Insurance

It’s easy to get a quote from Gerber. Just enter a few basic details and your email address, and they will offer you some basic quotes. For term insurance on a 30-year old female who doesn’t smoke, Gerber gave us these quotes:

The downside is that since almost everyone is accepted by Gerber, premiums tend to be high.

You can see Gerber Life on every social media platform (Facebook, Twitter, Pintrest, Instagram, YouTube and LinkedIn) but there is no app.

Last Thoughts

If you really want a simple, no-exam insurance policy, you might be happy with Gerber Life. The application process is very easy. On the other hand, rates tend to be high for what you get. You might do better to shop around, especially if you’re in good health.