Guaranteed issue life insurance is life insurance with no medical exam. It’s called guaranteed issue because everyone is accepted—it’s guaranteed.

- Who is Guaranteed Issue Life Insurance For?

- Pros and Cons of Guaranteed Issue Life Insurance

- What is Graded Benefits in Guaranteed Issue Life Insurance?

- What to Look For in a Guaranteed Issue Life Insurance Policy?

- Alternatives to Guaranteed Issue Life Insurance

- Top Companies for Guaranteed Issue Life insurance

Who is Guaranteed Issue Life Insurance For?

The major selling point of guaranteed issue life insurance is that there is no medical exam. Anyone who is likely to be denied regular life insurance because of health issues, age, or drug use can qualify for a guaranteed issue life insurance policy. Of course, the insurance companies know this and charge a higher premium because of it.

A guaranteed life insurance plan provides essential benefits for those who may have a hard time getting approved the traditional way, such as adults with a chronic or fatal illness, those who have aged out of an existing plan, and veterans living with a disability.

It is also often a go-to life insurance products for individuals that are considered high risk due to possibly their lifestyle and hobbies, or their occupation, etc. In these cases, it is also referred to as high risk life insurance.

All guaranteed-issue life insurance policies are whole life insurance policies. They last your entire life, as long as you pay the premiums. Companies will usually sell this insurance to anyone under the age of 75.

Guaranteed issue life insurance usually offers a low amount of coverage— usually less than $25,000. As you can imagine, a whole life insurance policy and usually less than $25,000 coverage, people usually buy this type of policy for final expenses. Learn more about Final Expense Whole Life Insurance: Cost and Top 4 Providers

Pros and Cons of Guaranteed Issue Life Insurance

Pros:

- Everyone up to age 75 is accepted

- No medical exam

- Last option for those who don’t have access to life insurance

Cons:

- Because everyone is accepted, premiums are high

- Coverage is lower, so you’re paying more for less

- Age, gender, and where you live do affect your premiums

What is Graded Benefits in Guaranteed Issue Life Insurance?

Since insurance companies know that people with no other option are usually the ones purchasing guaranteed issue life insurance, they have what they call graded benefits. If you die within the first two years of the policy, you won’t get the death benefit and your premiums will be returned to your heirs. The one exception is if you suffer an accidental death. So, you need to be healthy enough to survive at least two years.

What to Look For in a Guaranteed Issue Life Insurance Policy?

Every company has different options when it comes to guaranteed issue life insurance. Shop around for the one that fits your needs best. You would do well to find one that:

- Increases your death benefit in case of accident

- Includes chronic illness and terminal illness riders

- Child rider (up to $2500 to cover the cost of the funeral)

Premiums are quite high for how much coverage you get—expect to pay up to $200 a month for $25,000 worth of coverage.

Alternatives to Guaranteed Issue Life Insurance

Term insurance: Even if you have significant health problems, as long as you are 60 years old or younger, you may qualify for a small term life insurance policy. This would be cheaper, and you wouldn’t have to worry about the graded benefit for the first two years. It’s worth it to shop around. Some companies are pretty forgiving about certain health conditions.

There will be a medical exam, so be prepared for that.

Final Expense Insurance: Final expense insurance offers higher amounts of coverage, up to $100,000. There’s no medical exam, but they will ask you some health questions.

Top Companies for Guaranteed Issue Life insurance

Vantis Life: Best for 30 Day Money-Back Guarantee

Vantis Life isn’t as well-known as the others on this list, but they’ve actually been around for 75 years. They recently merged with Penn Mutual life insurance.

They call their guaranteed issue life insurance “Guaranteed Golden.” A 55-year old male can get $10,000 worth of coverage for $46. You have 30 days to look over the policy, and if you decide against it, they’ll give your money back.

AIG: Best for Riders included

AIG includes chronic illness riders and a terminal illness rider at no additional cost. Once the graded benefit period is over, you can access 50% of the death benefit if you are diagnosed with a qualifying illness and/or are given less than 24 months to live.

You can only buy AIG life insurance through AIG—no brokers. Also, to get a quote you have to fill out a form and an agent will contact you.

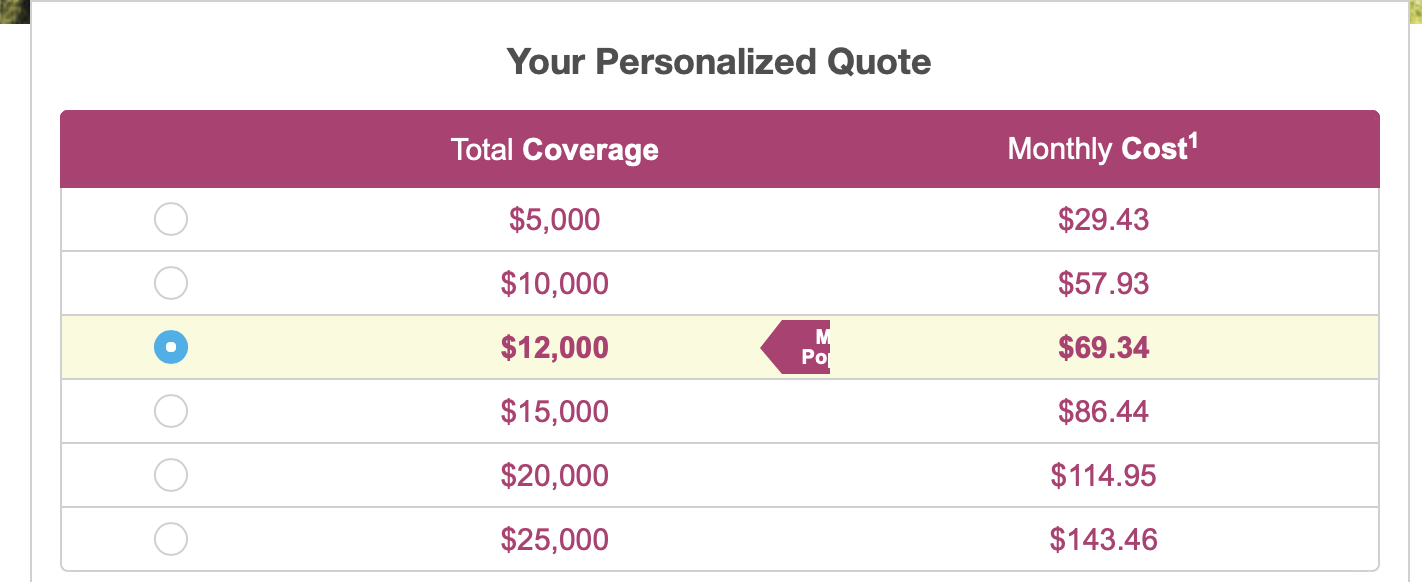

Gerber Life Insurance Company: Best for Up-front Pricing

Gerber isn’t just for their grow-up plan—they have guaranteed issue life insurance, too. They’ve been around since 1927.

For a 55-year old male, they gave us this quote selection:

Last Thoughts:

Guaranteed issue life insurance is like the court-of-last-resort for life insurance. If you can’t qualify for any other insurance, it might work for you. Consider all your options and shop around. If you can qualify for any other insurance, it would be cheaper. If a medical exam is impossible for you, guaranteed-issue life insurance gives you some protection.