Business owners in New York are probably already familiar with New York’s workers’ compensation insurance requirements: if you have even one employee, you need workers’ compensation insurance. In New York, you can get insurance through a traditional insurance company, an insurtech company, a digital broker, the state fund, or you can self-insure.

Buy workers comp insurance in New York from traditional insurance companies

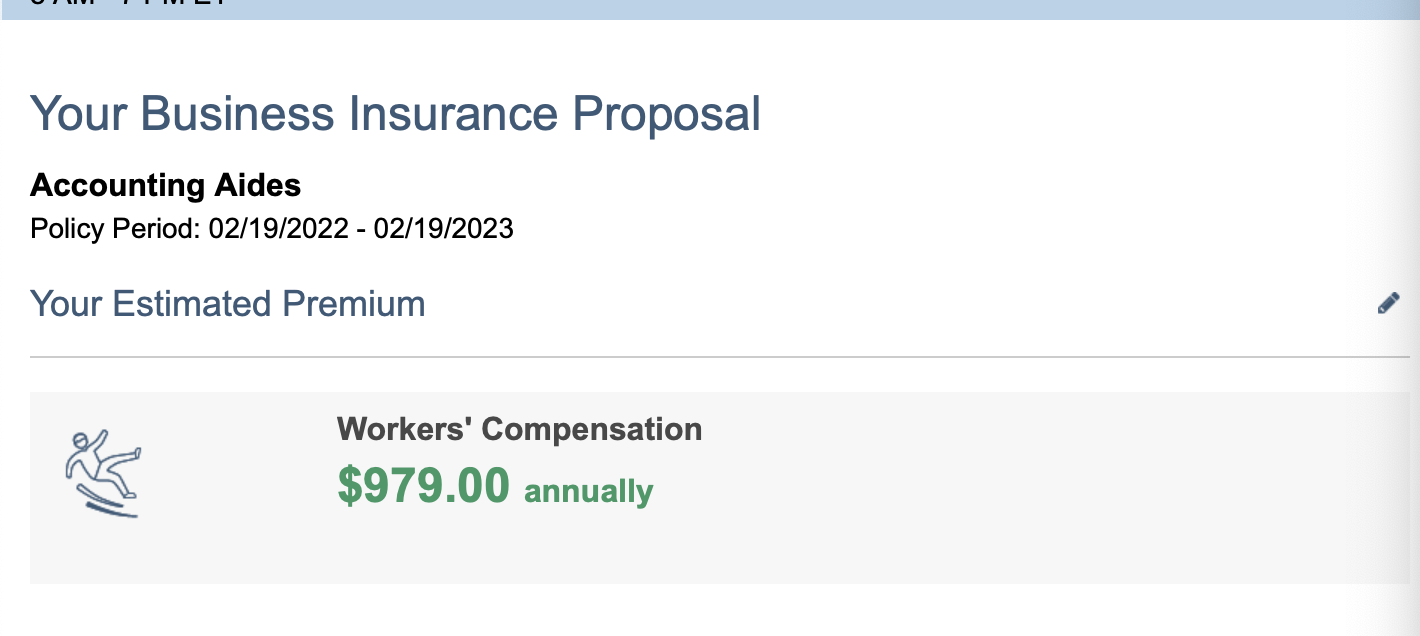

You can buy workers comp insurance in New York through many traditional insurance companies such as Chubb, Employers, AmTrust Financial, the Hartford, etc. Some traditional insurance carriers offer online quotes, and some don’t. Some, like The Hartford, will give you a quote online but to buy the insurance you have to call and talk to an agent. This quote is for an accounting firm in Staten Island with three full time employees, $350,000 in payroll and $500,000 in annual revenue.

Pros and cons of buying workers comp insurance from traditional insurance companies

| Pros | Cons |

| – Many traditional insurance companies have multiple types of policies, so you can all of your business insurance from the same company – Established companies with excellent financial strength – Most have a lot of experience with business insurance – Many offer multiple policy discounts | – It can be difficult to get an online quote from a traditional insurance company – Many require you to speak with an agent to purchase insurance |

Buy workers comp insurance from insuretech companies

The insurance industry has undergone a sea change when it comes to buying insurance online. Insurtech companies make it easy to get an online quote, purchase insurance, manage your policy, and file claims—all online. There are even insurtech companies that specialize in workers compensation insurance. Companies like Pie, Cerity, and Huckleberry all offer workers compensation insurance in New York.

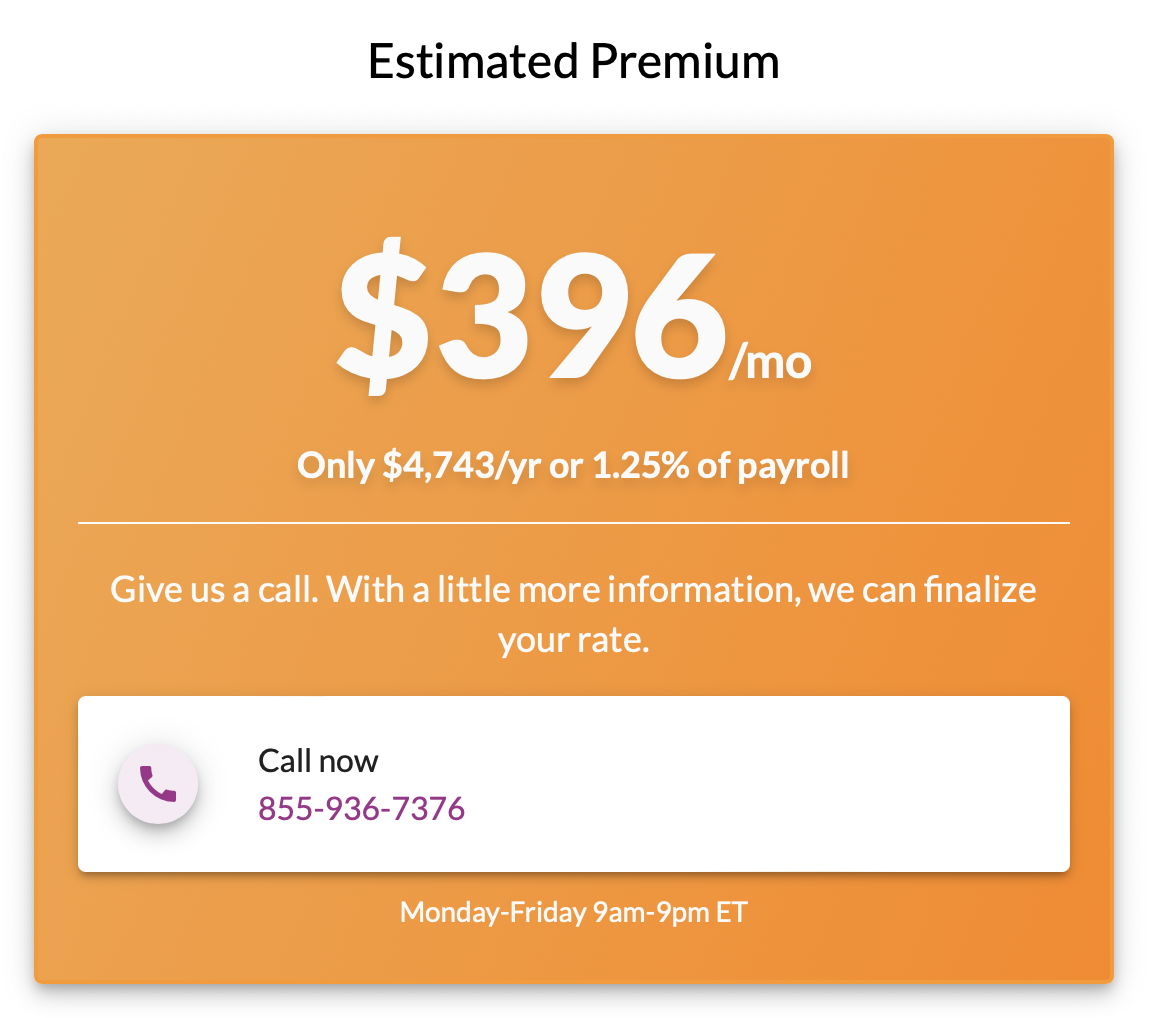

This is a quote for the same accounting firm as listed above.

Pros and cons of buy workers comp insurance in New York from insuretech companies

| Pros | Cons |

| – Getting an online quote is easy – You can manage your policy, pay your bill, and file a claim online – Often have lower premiums than traditional companies | – Some insurtech companies don’t do their own underwriting – More limited selection of insurance types means you may have to go elsewhere to get everything you need |

Buy workers comp insurance in New York from digital brokers

Companies such as CoverWallet, Policy Sweet, Simply Business, and CoverHound aren’t insurance companies, but digital brokers. You enter your information, and they send it out to their partners to get you a quote for insurance.

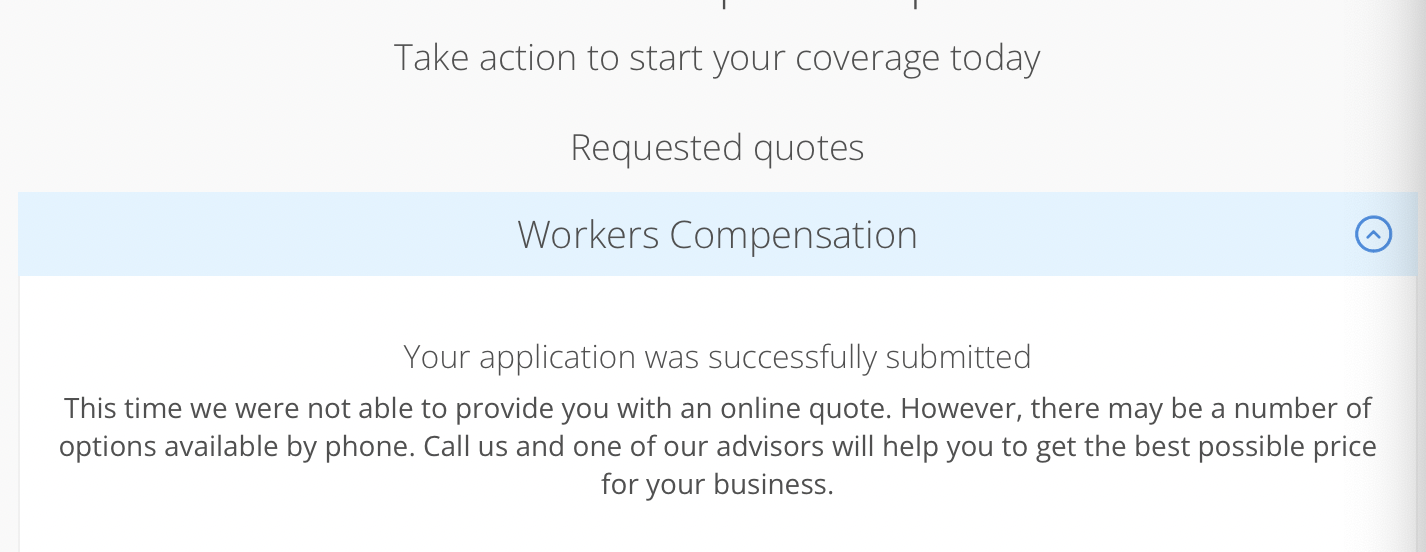

Usually, when we enter information into CoverWallet, it gives us at least one quote. Sometimes, though, they say they’ll get back to us, like they did here:

Pros and cons of buying workers comp insurance in New York from digital brokers

| Pros | Cons |

| – Gives you the opportunity to compare quotes, sometimes from companies don’t offer online quotes – Easy to get multiple types of insurance and manage them in the same “wallet” – Manage policies online, pay bills online, file claims—all online | – Quotes are not always instant – Don’t do their own underwriting – Don’t offer quotes from anyone they’re not partnered with |

Buy workers comp insurance from NY State Insurance Fund (NYSIF)

Some states offer a state fund to provide workers’ compensation insurance. New York state offers the state fund as an option: other states make it mandatory. The NYSIF will cover anyone, in any industry, unless you owe them money from a previous bill. But your industry, your safety record, and claims history will not prevent you from being offered insurance. The state fund is a not-for-profit business.

Pros and cons of buying workers comp insurance from the NYSIF

| Pros | Cons |

| – You are guaranteed coverage, no matter your industry or safety record – The state fund requires that premiums are the lowest they can offer and still remain solvent – You can get a quote online if you have payroll verification for the last four quarters or if you employ domestic workers, such as home health aides, cooks, housekeepers or nannies | – Customer service may be a little difficult to get a hold of |

Self-insured workers comp in New York

We should preface this by saying self-insurance is relatively rare, and you have to apply for the privilege. There are a lot of requirements you have to meet:

- Three years in business in a legally authorized entity

- Proof of current workers compensation insurance

- No outstanding procedural or compliance penalties

- A Moody rating of A3 or greater, or an S&P rating of A- or greater

- Tangible net worth must exceed seven times the greater of the three-year average premium paid

- Three years of certified, financially independently audited financial statements

- Safety program maintained by the employer to prevent accidents

If you meet all these criteria, you can apply to self-insure. The minimum security deposit for self-insurance (as of July 1, 2021) is $1,650,000.

Learn more at the best workers comp insurance in New York

Can you be exempt from workers compensation insurance in New York?

Probably not. The only way you can get away with not having workers’ compensation insurance is:

- You are a sole proprietor, and you are your only employee

- You have a partnership with one other person, and you have no other employees

- You are the owner of a corporation with no employees

In New York, both full-time and part-time employees are required to be covered by a workers’ compensation insurance policy. Even if you only employ your own family members, you still need workers’ comp insurance.

Do independent contractors in New York need workers comp insurance?

Many businesses try to get away with not paying workers’ compensation insurance (or other benefits) by calling their employees independent contractors. However, the IRS has strict rules about who is and who is not an employee. If you have a say in how someone spends their time, (as opposed to the employee just providing you with a product) they are an employee. If you supply someone with a steady paycheck, they’re probably an employee.

Some courts and federal agencies have developed “the economic realities test.” If a person gains most or all of their income from a business, they are probably an employee.

Learn more at the best workers comp insurance for independent contractors

What are the penalties for not having workers’ compensation insurance in New York?

More than the cost of workers’ compensation would have been in the first place. Businesses that fail to provide workers comp insurance can be fined $2,000 a day for every 10-day period of noncompliance. This does not include the money you will pay if someone becomes injured or sick, as you will also be on the hook for their medical bills, lost wages, and court costs when they sue you.

If you are found to be noncompliant with workers’ compensation insurance, the workers’ comp board can issue you a stop-work order, which is what it sounds like: all work will stop until you acquire workers comp insurance.

How much does workers’ compensation insurance cost in New York?

Workers’ compensation rates are $1.41 per $100 in payroll. You can figure out roughly how much you’ll pay by using this formula:

(Payroll/$100) x class code rate x experience modification rate = premium.

You can find a list of all the class codes here at the Numerical NCCI Code List. You can read more about how much workers’ compensation insurance costs.

Different insurance companies will give you different quotes. Be sure to shop around with a few companies or with a digital broker to compare several quotes to find the cheapest one for your company.

How to find cheap workers comp insurance in New York?

Workers compensation insurance is the most expensive in New York. It can be a significant cost to your business. Not having workers compensation insurance is not an option since it can result in even more costly consequences. Below are a few tips to help you get the cheapest workers comp insurance in New York.

- Shop around to compare several quotes: Make sure you shop around with a few insurance companies or a digital broker to compare several quotes to get the cheapest one for your business

- State programs: Check if there is any state savings program in New York that your business can be qualified for.

- Group insurance: if your company is a member of a larger association, you may be able to get a group rate on your company’s workers compensation insurance.

- Identify potential hazards and fix them. Once you fix them, make sure you notify your insurance agent (if you have one) or report it to your company. Continue improving the safety standard in your company’s workplace and ask for annual reviews when you need to renew your company’s workers comp insurance.

- Invest in safety education. According to Safety and Health, for every dollar you spend on injury prevention, you’ll earn a ROI of between $2 and $6 dollars. If you’re wondering how to start a safety program, OSHA (Occupational Safety and Health Administration) is a good place to start. After starting the program, you need to make sure to obtain the qualification certificate from the program administrator. Showing the certificate to your workers compensation insurance insurer or agent can help reduce the cost when you renew the policy.

- Check classification levels. Every employee type is assigned a classification level, and each level is assigned a rate that reflects the level of risk this type of job has. Obviously, a secretary is exposed to much less risk than a construction worker, even if they work at the same company. Make sure everyone is classified accurately and regularly update this as you are hiring new employees.

Learn more at the cheapest workers comp insurance companies.

Last thoughts

Workers’ compensation insurance is a non-negotiable part of doing business. Not only do you have to have it, but it protects your workers as well, making you a good employer to work for.