Professional advisors are constantly at risk of being accused of professional errors. Depending on the profession, minor errors can have far-reaching consequences like jail time, bankruptcy or even death.

When this happens, clients or customers may initiate a lawsuit against you if they believe you are responsible for their financial loss. If you have professional liability insurance, you might get cash assistance to defend your firm or correct the error.

Typical forms of professional liability insurance include coverages for accountants, consultants, and real estate specialists. Nonetheless, other firms that offer professional advice can purchase this form of business insurance.

The policy is vital as it may help you avoid customer conflicts and safeguard your brand if a customer feels you made a mistake, regardless of whether or not you did.

If you are at fault for a mistake or professional negligence, your coverage may help you pay for the associated costs. Additionally, it might assist pay for your defense if you are unfairly charged.

- Where to get professional liability insurance quotes online?

- What is a professional liability insurance quote?

- What factors affect your professional liability online quotes

- How to find cheap professional liability insurance quotes online?

- The average cost of professional liability insurance

- Professional liability insurance costs by profession

Where to get professional liability insurance quotes online?

There are two options to get quotes for your professional liability insurance. You can either contact insurers or use a digital insurance broker for quotes. In a broad sense, both options offer benefits and they work for different categories of people.

Getting professional liability insurance quotes online with digital brokers

Online brokers are companies that assist their clients in obtaining competitive quotations from insurers based on their needs. Insuretech companies work the same way; the only difference is that they use technological tools to find the best policies for their clients.

These companies operate online and do not issue insurance policies; instead, they point people toward the best policies.

These online brokers also act as advocates for the policyholders they serve. They’ll use their knowledge and expertise to assess your situation and choose the best insurance plan to cover your needs.

An insurance broker has extensive knowledge of the insurance market and is knowledgeable about the rates and options offered by several insurance providers.

A broker’s independence means they can shop around for the best deal and provide you coverage from many providers rather than just one.

The only problem with brokers might be that some of them may offer biased suggestions when they are provided high commissions. However, not every broker does this; some do a better job than others of recommending solid insurance plans. For this reason, you may want to compare several brokerages before settling on one.

Also, a broker can be an excellent way to start seeking quotes, especially if you are not so familiar with professional liability insurance.

Some insurance brokers/Insuretech companies you can use include the following:

- Simply Business

- Coverwallet

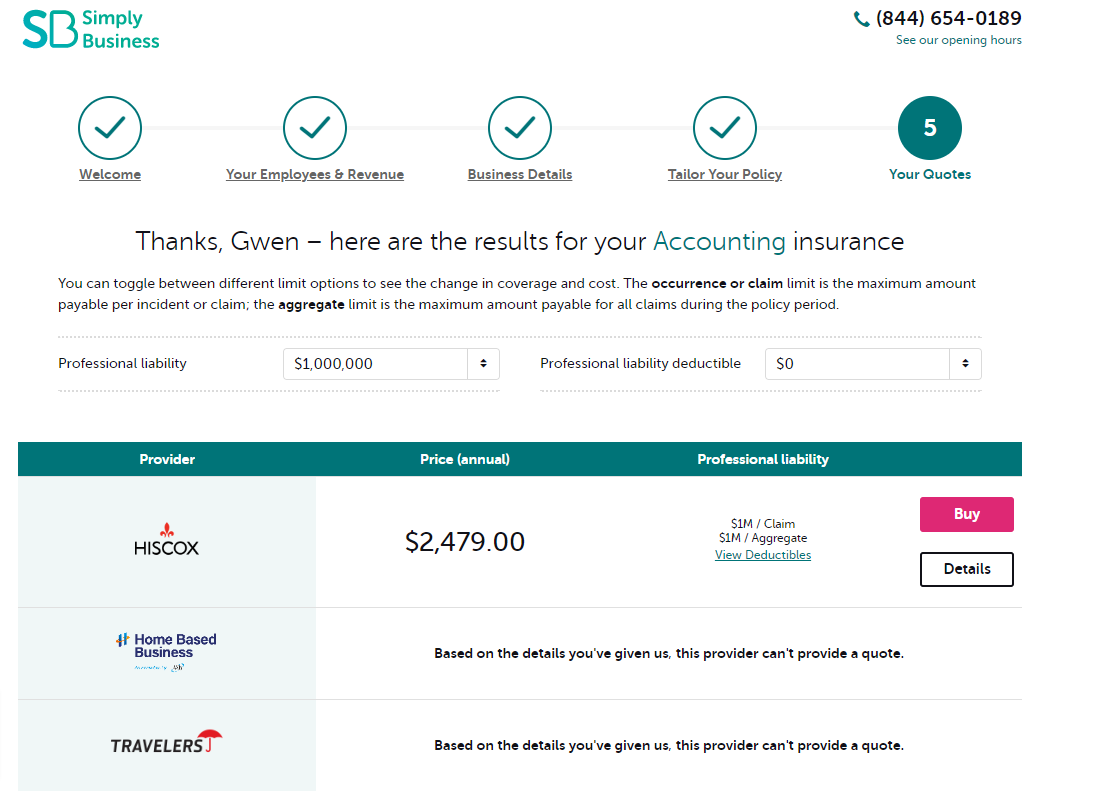

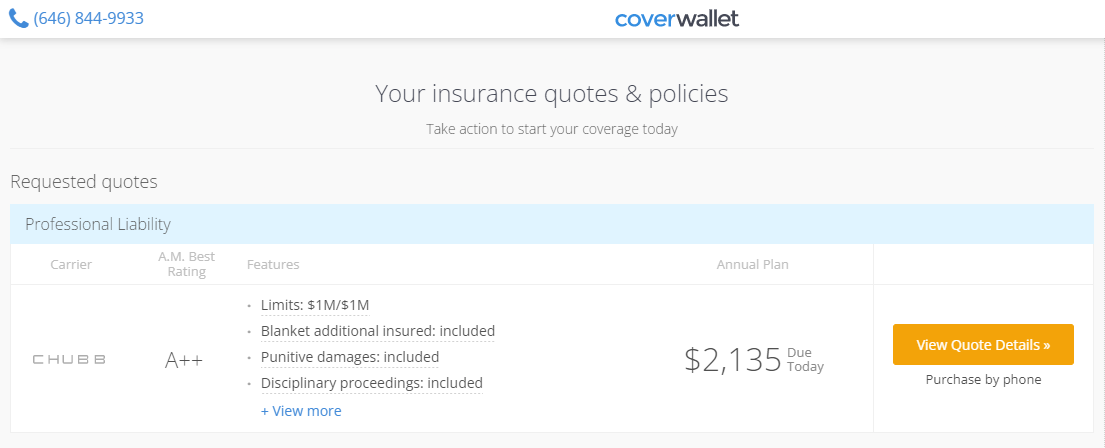

Below are online professional liability insurance quotes that we got from Simply Business and CoverWallet for an accounting firm.

Obtaining professional liability insurance quotes from insurers

Many insurers offer their quotes online through their website. Insurance firms can also use a mix of the two approaches in certain circumstances. This approach is best for people with a good idea of professional liability insurance and the company they want.

Avoiding intermediaries is the primary advantage of skipping the broker and going straight to the insurance company. However, the disadvantage of going through this route is that you are restricted to limited choices.

Your choice of insurer will be limited to how well you know insurance companies and how you can search the internet. In some cases, some insurers might offer better services at better prices that you did not see during your research.

Also, this strategy may not work for people unfamiliar with professional liability insurance.

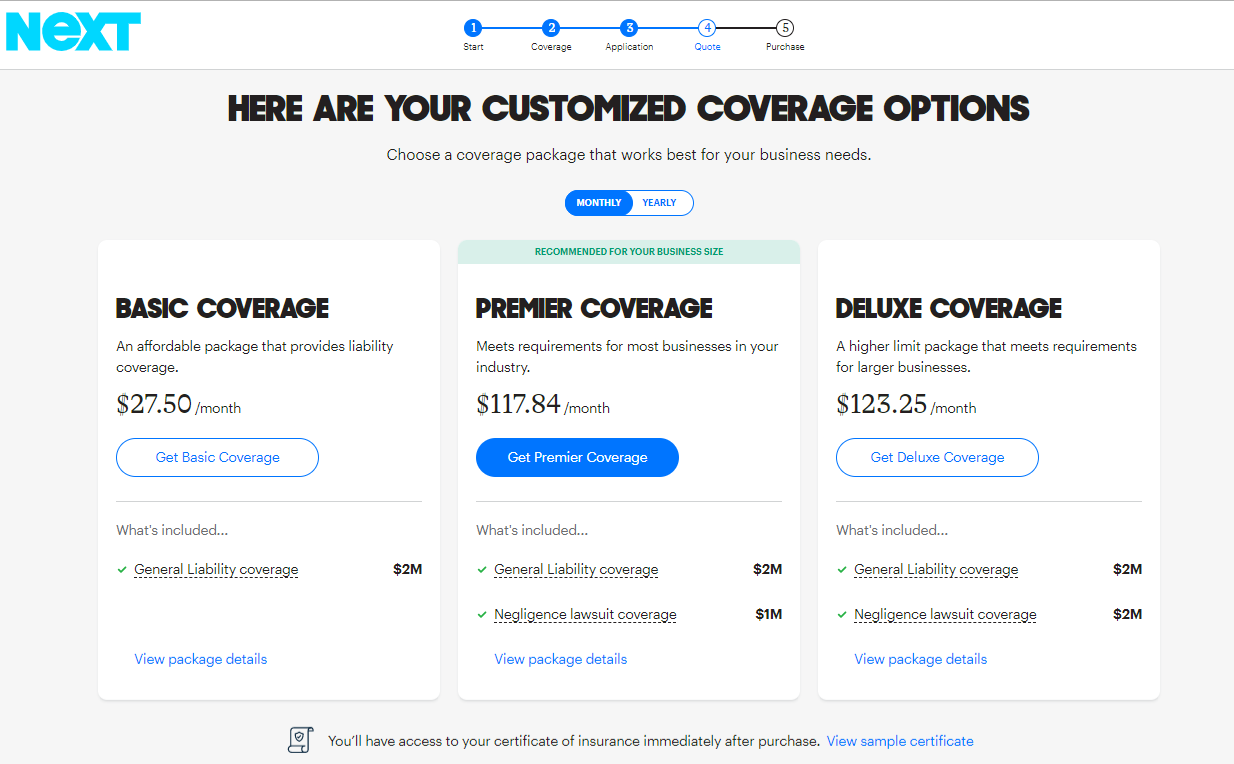

Examples of direct insurers that offer this policy include:

- Next

- The Hartford

- Hiscox

- biBERK

Learn more at the best professional liability insurance companies

What is a professional liability insurance quote?

A professional liability insurance quote refers to an estimate of the total amount your insurer demands monthly or annually in exchange for the coverage.

In most cases, insurance providers calculate your quotes by considering critical factors about your work, as well as other important risk factors such as the possibility that you would file a claim.

To arrive at the correct estimate, most insurers use quote systems that ask their prospects essential questions about their business. After calculating, your insurer will provide a quote that considers your business risks and the insurer’s expected profit.

Typically, online quotes are subject to change. The insurance company may opt to increase your premium during your policy term to compensate for the rising expenses of providing coverage.

What factors affect your professional liability online quotes?

The total cost of your professional liability insurance policy will be based on some criteria, including the following. When you receive a quotation for insurance, it is crucial to ensure that you offer the correct information about your company.

This will ensure that you have the appropriate coverage for you and that any claims are handled without delays.

The kind of work you do

The amount of risk in your work will affect the cost of your professional liability quotes. Insurance premiums tend to be much higher for professions that often include complaints of carelessness or mistakes in company operations.

Companies that offer professional advice also tend to pay more for their professional liability insurance.

For instance, a yoga teacher might pay less than a financial advisor. The reason is a simple miscalculation in financial advice from the financial advisor can lead to dangerous far-reaching consequences.

How many members of staff do you have?

The more consultants you have, the more the possibility of professional errors. Therefore, a company with five consultants might have a higher quote for professional liability insurance than a business with only one or two consultants.

Your location

As a general rule, companies in populated metropolitan areas tend to get higher quotes for their professional liability insurance.

So, for instance, if you operate a small company in San Francisco, you might pay more for insurance than if you worked in a tiny town like Montana. This is because of the higher cost of living in San Francisco.

Also, your higher premium can result from specific legislation in your state.

Your history of claims

Your history of claims and losses will have an effect on the price you pay for insurance. For instance, if you are an accountant and have had many prior claims due to poor services, insurers might increase your quotes when you opt for a renewal.

Coverage limits

Your coverage limit is the highest amount an insurer is willing to pay for covered perils.

You have the option of increasing the coverage limits on your insurance policy if you want protection against a more extensive range of losses. Your premium will increase as you increase your insurance coverage limits.

Professional liability insurance policies have two kinds of limits: a limit per claim and an aggregate limit for all claims (one year). After reaching your credit limit, you are responsible for paying any remaining balance.

For example, suppose you have a $1 million maximum on your professional liability coverage. You have a single claim with a cost of $1,200,000. This would need you to pay $200,000 out of pocket.

You’ll need more significant coverage limits on your insurance policy if you want to be protected against additional risks. Consequently, you will pay extra for this coverage.

Most professional liability policyholders choose coverage levels of at least $1 million.

The appropriate quantity of coverage for your company relies on your unique demands and level of comfort with financial risk exposure.

Your prior professional experience

The number of years that you have been running your company in your field also affects your insurance quotes.

Most insurers will offer you lesser quotes if you have operated your company for at least 2 years with no claims. Your years of experience in the industry are crucial as it shows your expertise and put you ahead of others.

For instance, if you have had a mechanic shop for eight years and have never had to file a claim, you may get a discount on your quote.

How to find cheap professional liability insurance quotes online?

You may use the following measures to minimize your insurance expenses and premium rates:

Check multiple insurers for quotes

The best policy offers quality protection at the most affordable price. So, before committing to an insurance policy, ensure you go through multiple companies. Working with a digital broker like Simply Business or CoverWallet is a good way to get several quotes in one place. Ensure that the policy you choose offers you the best protection at the best prices.

Keep your risk level low

A comprehensive awareness of the hazards in your company may assist in reducing the possibility of filing insurance claims and hence, reduce your premiums.

For instance, you could:

- Create process checklists and evaluations

- Develop a comprehensive training program for your employees

- Keep accurate notes and receipts about your work

- Only take work that you have the expertise to accomplish well

Learn from past claims

Analyze your prior claims and see what you may have done to prevent the risks involved.

For instance, if a customer filed a claim alleging that an employee missed critical facts, you might provide the employee with further training and improve your quality control procedures. That way, they won’t make such mistakes next time.

Choose the appropriate limits and deductible

Lower limits can save you money, but inadequate coverage will expose you to more significant dangers. Similarly, selecting a bigger deductible will result in lower premiums (a deductible is the amount of money you pay before your insurance policy kicks in). So, when choosing your policy, ensure you select the proper coverage limits and deductibles that you can afford and offer you good protection.

Bundle many policies.

Combining several types of insurance policies can help you get discounts. Depending on your insurer, you can get 10% and 20% discounts. So, if you want professional liability insurance, you may consider getting other policies like commercial auto coverage or a general liability policy to receive your discounts.

The average cost of professional liability insurance

As you can imagine, professional liability insurance costs vary significantly by profession. A doctor will pay more than a nurse for their professional liability insurance policies.

The average cost of professional liability insurance is $65 per month or $780 per year. Most small businesses pay between $500 to $1,200 for their policies.

Learn more at how much professional liability insurance costs

Professional liability insurance costs by profession

Below are the average costs of professional liability insurance for various professions for your reference.

| Professions | Average costs of professional liability insurance |

| Lawyers & Attorneys | $500 – $6,000 per year |

| Nurses, including nurse practitioners | $500 – $2,000 per year |

| Consultants | $720-$3,000 per year |

| Engineers & architects | $1,8000 per year |

| Teachers | $100 per year |

| Accountants and CPAs | $480 to $5,200 per year |