The job of a personal trainer is vital in today’s society. Your job Is to assist others in accomplishing their health and fitness objectives. Those goals include losing weight, gaining muscle, or getting ready for an important race.

Accidents are inevitable throughout the training process; it doesn’t matter how cautious you are, and that’s good! If you have personal training liability insurance, dealing with incidents or claims may be simpler.

This article will discuss the typical cost of personal trainer insurance and provide you with all the information you need regarding personal trainers’ insurance.

- How much does personal trainer insurance cost?

- Average costs of different coverages for personal trainers

- Personal trainer insurance quotes

- Personal trainer insurance coverages and their costs

- What factors affect the cost of personal trainers’ insurance?

- How to buy affordable personal trainers’ insurance

- Best personal trainer insurance companies

How much does personal trainer insurance cost?

The average cost of a $1M professional liability insurance policy for personal trainers is $28 per month, or $336 per year. Most personal trainers pay from $11 to $69 per month for their professional liability insurance policy.

The cost varies significantly due to several reasons, one of which is the coverage included in the policy. It is common for some insurance companies to add other coverage and inclusions into a personal trainer professional liability insurance policy.

Personal trainers may need several coverages and they may cost more.

Average costs of different coverages for personal trainers

In addition to professional liability, personal trainers may need other coverages such as general liability, commercial auto, commercial property, and workers comp insurance. Below are the average costs of these coverages:

| Personal trainer insurance coverages | Average costs |

| Professional liability insurance | $28 per month |

| General liability insurance | $23 per month |

| Commercial property insurance | $38 per month |

| Commercial auto insurance | $89 per month |

| Workers comp insurance | $94 per month |

Keep in mind that these are just the averages. Your rates will be different. Be sure to shop around with a few companies or work with a digital broker to compare several quotes to find the cheapest one for you.

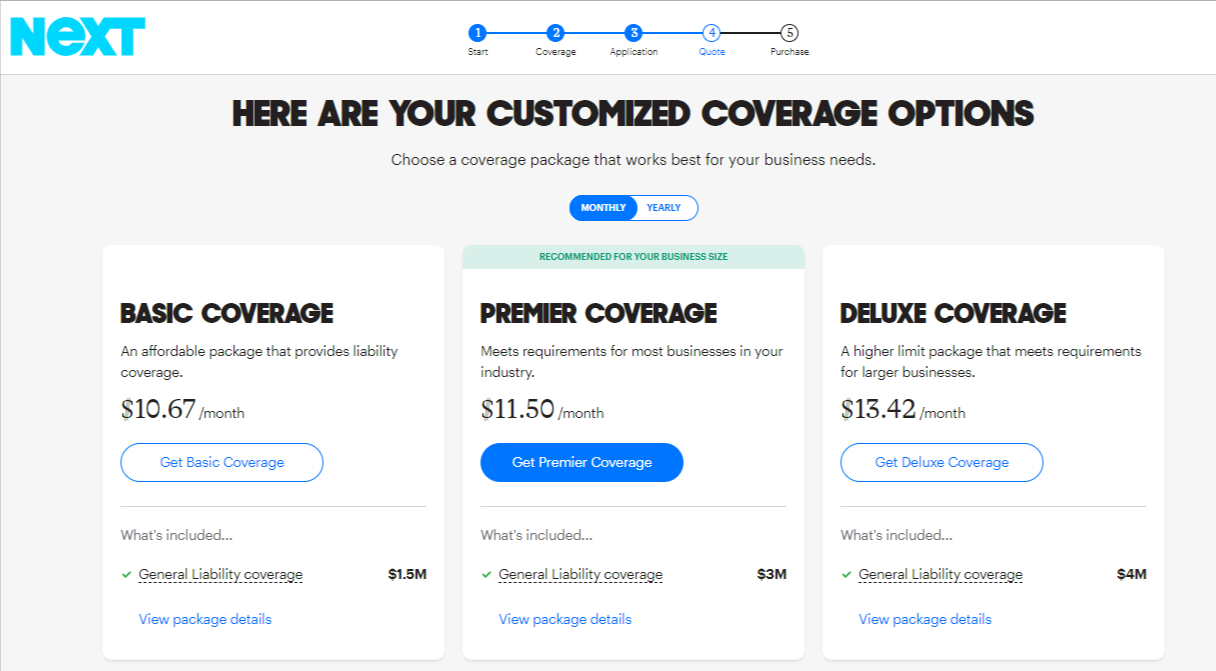

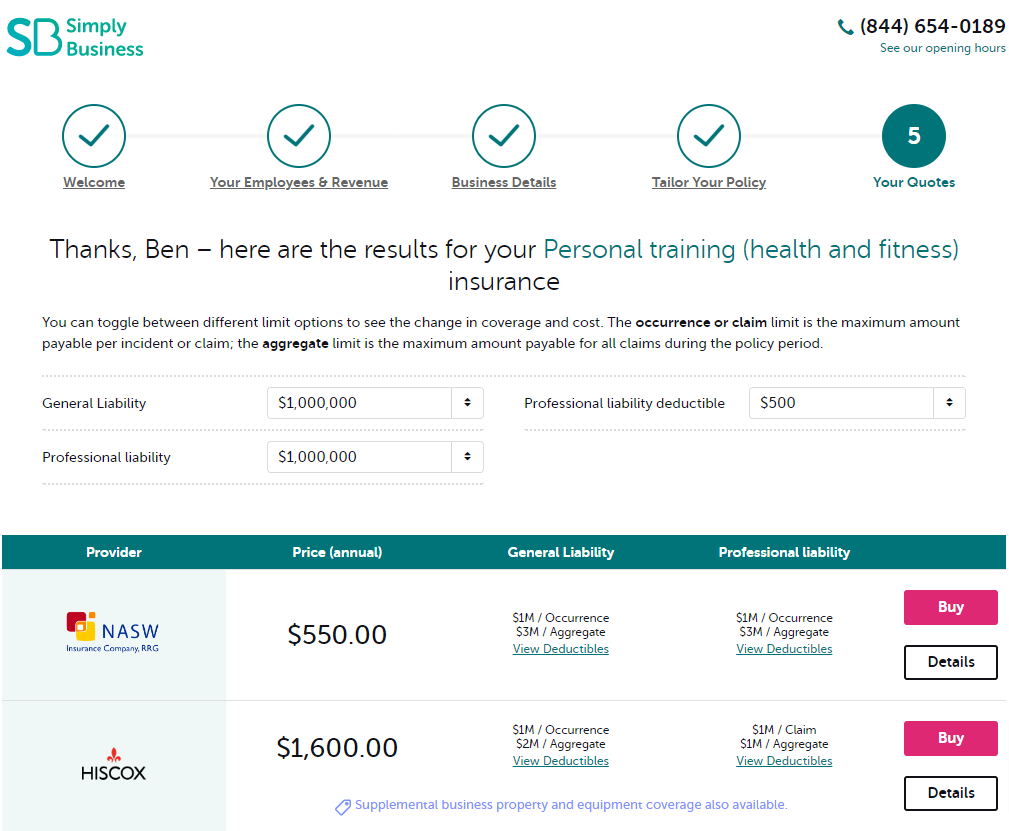

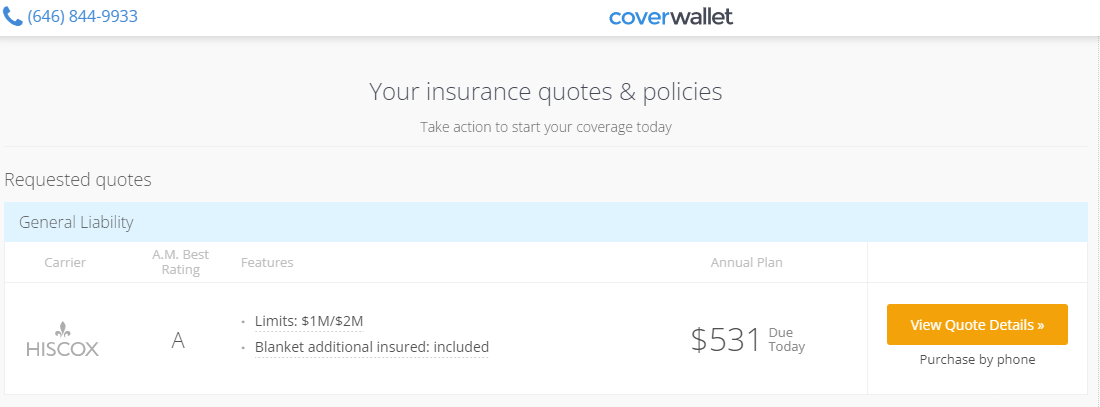

Personal trainer insurance quotes

The following are some sample quotes for fitness trainers’ insurance gotten NEXT, Simply Business, and CoverWallet. It only takes us a bit less than 10 minutes to get these quotes and if we want to buy the policy online, we can as well. It is fast and convenient to compare several quotes with them.

Personal trainer insurance coverages and their costs

The following are the most common coverages that personal trainers use. Ideally, if you want more coverage, you can speak with your insurer to see what additional coverage they have for you.

General liability insurance for personal trainers

Physical trainers pay a premium from $15 to $76 per month for general liability insurance.

This is usually the most common coverage for most personal trainers. You will probably get only this policy if you buy basic personal trainers’ policy. As a result, some insurers call it the personal trainers’ liability insurance policy.

This insurance policy covers third-party physical injury, property damage, and reputational harm. Every personal trainer should have this coverage since it protects against third-party claims, which are often the most significant source of financial loss for personal trainers.

The following are some instances that fall within the umbrella of general liability:

- Property damage: you accidentally break a window in a building you rent.

- Damage to your professional reputation: a performance rights group files a lawsuit against you after discovering that you have not paid royalties for the playlist you use in the classroom.

- Physical harm: a customer trips over a dumbbell in your fitness center and fractures their leg.

In the event of accidents such as these, general liability insurance may assist in paying for the repair costs, the injured person’s medical expenses, and your legal fees and the if the injured party chooses to file a lawsuit against you.

Learn more at the best general liability insurance companies

Commercial properties insurance coverage for personal trainers

Most personal trainers pay monthly premiums between $21 and $65 for commercial property insurance.

This policy usually covers you’re the housing unit of your business and the physical assets in it. This includes your studio and any of the equipment, furniture, or fixtures housed inside it.

If any of these are damaged due to a covered incident, such as fire, theft, or vandalism, the policies may pay to repair or replace them up to the insured value, less your deductible.

Depending on your insurer, covered perils can include:

- Fire

- Hail

- Theft

- Vandalism

- Windstorm

Personal trainers who rent space can purchase property insurance coverage that exclusively covers the equipment owned by the company, such as weight machines, Pilates apparatus, and kettlebells.

Professional liability insurance for personal trainers

Monthly premiums for professional liability insurance are estimated to fall between $11 to $69

Professional liability insurance sometimes referred to as errors and omissions (E&O) insurance, will pay for the costs of your legal defense and any settlements or judgments if a client alleges your training services were directly responsible for their injuries or financial losses. The following are some instances of occurrences that this policy might be helpful.

- Failing to deliver: You told a client you would help them reduce weight, but you missed a lot of classes, and they were not able to meet their goal.

- Errors: Telling a client to lift additional weights without considering that they are not physically able to do so.

- Omissions: providing advice on losing weight but neglecting to mention that the client needs to monitor their diet.

Even if the claims against you are completely without merit, personal trainer professional liability insurance will pay your legal expenditures.

Learn more at the best professional liability insurance companies for personal trainers

Business Owners’ Policy (BOP)

Monthly premiums for BOP can range anywhere from $45 to $92.

A BOP protects your personal training business against the most typical types of loss by bundling together general liability and commercial property policies. The combination is not only more convenient, but it is also more cost-effective.

Personal trainers who operate their studios should consider this policy. You can also add a business interruption coverage as an additional covered loss to this policy. The business interruption coverage will pay owners if their property sustains damage that prevents them from running their daily business.

Learn more at the best BOP insurance companies

Other insurance coverages that personal trainers may need

In addition to the four fundamental categories of coverage that we’ve discussed in the previous section, you may additionally need the following types of insurance:

Workers’ compensation insurance

You may be legally obligated to obtain workers’ compensation insurance if you have any employees. This policy will cover any injuries, illnesses, or disabilities your employees experience on the job.

Learn more at the best workers comp insurance companies

Commercial auto insurance

If you own a car you use for your personal training business, it is important that you buy commercial auto insurance even if you only use your vehicle to travel to and from your scheduled workouts.

If your car is registered in your name, you may not need to worry about paying extra for a commercial auto policy. A personal car insurance policy should be enough to cover you for your daily movements as a trainer.

However, if you register your car with your business name, you may need a supplementary commercial insurance policy. The reason is most insurers might argue that personal insurance does not cover business purposes.

Always check with the company that provides your vehicle insurance to verify that you have enough coverage.

Learn more at the best commercial auto insurance companies

What factors affect the cost of personal trainers’ insurance?

When setting rates, insurance companies look at various factors related to your company in addition to the quantity of coverage and number of policies you have. The following are some of the most important of these factors that affect the price of your policy:

Location

In most cases, a company’s insurance premiums will be lower if it is situated in a region with a lower likelihood of crime or bad weather. Also, personal trainers that work in urban areas or places with a high cost of living will pay more for their premiums.

History of claims

If you have filed several claims in the past, your company may seem riskier to insurers. As a result, your rates may rise.

Annual business revenue

Personal trainers who make more money may pay a higher premium for their insurance. Firstly, customers tend to sue larger companies more than smaller businesses. If they are sued, verdicts against them may occasionally reflect the amount of money they make.

Staff

Employers are required to get workers’ compensation insurance in most jurisdictions. Usually, worker’s comp is calculated on an employee basis. Therefore, the more employees you have, the higher your worker’s comp insurance cost. More so, employing more employees raises the likelihood that your staff may accidentally harm customers or that customers may sue you for property damage. Plus, more staff increases the likelihood that they will steal from you.

Business property

Insurers take into consideration the total worth of your business property. They will also consider its dimensions, age, presence of safety systems, and many other variables.

Risk management

Certain insurance companies provide discounts to personal trainers with security systems and fire alarms installed in their businesses. These same companies may also cut a trainer’s rates if the trainer routinely utilizes written contracts and liability releases.

Duration of coverage

The cost of the insurance policy will vary depending on how long you want to be covered. Some companies offer coverage per job, per day, and per week as against monthly and annual plans. Usually, the more time your policy protects you, the more expensive it will be.

How to buy affordable personal trainers’ insurance

If you think your personal insurance policy is too expensive, you may be tempted to reduce your coverage limit or raise your deductible. While doing that may offer a momentary solution, it may cause more problems in the future. When an incident occurs, your insurance may not offer enough money to cover your damages.

Instead of doing that, the following are some ideas that may help you reduce the price of your premiums.

Identify your risks

As a personal trainer, you must know the risks associated with your business. Identifying these peculiar risks will help you stay away from possible dangers, which will likely reduce your premiums.

To ensure that you are aware of all possible dangers, you should analyze your personal training business in-depth. Ideally, you should pay close attention to your customers, procedures, and tools.

After that, choose the appropriate methods to mitigate these risks and then add all relevant coverages.

Consult with an independent agent

Independent agents have knowledge of the industry. They may be able to point you in the direction of insurance companies that have excellent expertise in dealing with your line of work.

Ask for discounts

The insurance industry is a competitive industry with companies trying their best to get customers’ attention. As a result, so many discounts are available to people who buy insurance policies. So, you may ask your insurer if they offer any discount and see if you qualify.

Check for the best prices

Insurers offer different prices for their policies. As a result, you may be able to get better offers if you are willing to check as many insurers as you can.

Purchase many policies from the same provider

This is a common practice among insurance providers. When you buy multiple policies from the same insurer, you get a discount on your total premium. One of the most ways to do this is to buy a business owner policy (BOP), which provides protection for both general liability and commercial property. Similarly, some insurers have special plans that contain all the coverages you need at discount prices.

Best personal trainer insurance companies

Many insurance companies offer personal trainer insurance. Different companies may have different policies and even for the same policies, they may have different coverages. We have done the research and here are our recommendations for the top providers of personal trainer insurance for your consideration.