The job of a landscaper comes with gratification but not immediately. You go through the rigors of working with mother nature to transform outdoor areas into lush havens. However, once the job is done, your expertise leaves behind beautiful sites valued by everyone, especially your client.

As interesting as the job is, there is always a chance that it could cause property damage or bodily harm to individuals. This is because landscapers constantly use dangerous tools like chainsaws, insecticides, and other potentially harmful items.

Because of this, the majority of landscapers require insurance. You must realize landscaping contractors might need several insurance coverages such as general liability, workers comp, commercial auto, and equipment and tool coverage. This makes landscaping insurance costs vary among different contractors.

In this article, we’ll discuss how much should you budget for landscaping business insurance; what exactly goes into the price; and we’ll discuss the costs and advantages of business insurance for landscapers.

- The average costs of landscaping insurance policies

- General liability insurance cost for landscaping contractors

- Commercial auto insurance cost for landscaping contractors

- Where to get landscaping insurance quotes online?

- How to get cheap landscaping insurance?

- Best landscaping insurance companies

The average costs of landscaping insurance policies

Landscaping insurance costs vary depending on the types of coverage you purchase, the level of coverage you select, and the services you provide.

For instance, a smaller company that does stump removal may incur annual charges of $500, but a larger one may incur costs of $1,000 for business property insurance.

Generally, the average cost of a comprehensive landscaping insurance policy, with all 4 coverages, is $445 per month, or $5,340 per year. Most landscaping businesses spend between $282 to $936 per month for general liability, commercial auto, business equipment coverage, and workers’ compensation. Below are the average costs for each coverage:

| Landscaping insurance coverage | Average costs |

| General liability insurance | $155 per month |

| Commercial auto insurance | $142 per month |

| Workers comp insurance | $136 per month |

| Equipment and tool insurance | $12 per month |

Since most landscapers only require these four main policies, we’ll focus on the cost of these four significant policies.

General liability insurance cost for landscaping contractors

Generally speaking, general liability insurance costs between $90 to $225 per month for landscapers.

The majority of commercial insurance programs for landscaping include landscaping general liability insurance as a primary component. Primary means you get this coverage as a basic plan, and you can choose to purchase additional insurance policies as add-ons to it later on.

The policy covers third-party human injury or property damage you unintentionally cause while doing landscaping services.

As such, the policy covers issues like the following:

- Payment for the medical bills of anyone injured due to your landscaping work.

- Refund the property’s value if your landscaping job caused damage to someone’s property.

- Payment for the cost of your legal defense. Mainly, general liability insurance will cover legal bills, administrative charges, settlements, and other relevant expenditures if your landscaping business gets sued.

Workers’ compensation insurance cost for landscaping businesses

In general, most landscaping contractors pay between $85 to $192 per month for a workers’ compensation insurance policy.

You must offer workers’ compensation to any landscapers employed by your business if they contract an illness or accident linked to their job. Buying worker’s compensation insurance is the best approach to avoid suffering losses when helping your sick or injured employees.

The state requires landscapers to carry workers’ compensation insurance. State regulations, except Texas, require this as soon as your landscaping business employs one or more contractors, part-time workers, or full-time staff. When an individual or group of employees suffers a work-related illness or injury, you can pay for the following by having this landscape insurance policy:

- Necessary payment for medication, ambulance bills, surgery, and treatment of work-related injuries for your landscape staff.

- Rehabilitation costs if an employee develops a permanent or temporary disability due to a work-related accident or illness.

- Weekly allowance for workers unable to work due to a job-related accident or illness. This is usually two-thirds of the average weekly pay or 67%.

- Death benefits in the form of burial costs and allowances to the decedent’s dependents.

Equipment and tools coverage cost for landscaping contractors

The average cost of equipment and tools coverage for landscapers is $12 per month. Most landscaping contractors usually pay between $6 and $18 monthly. This coverage protects your business equipment as you move them from one job site to another one.

This policy can cover your losses if your lawnmowers, drills, excavators, tractors, shovels, protective helmets, and other tools and equipment are destroyed or lost due to fire, theft, vandalism, or other insured dangers.

However, the amount you get from this insurance will only cover a percentage of the total value of your tools.

Commercial auto insurance cost for landscaping contractors

Generally speaking, commercial auto insurance for landscapers costs from $110 to $250 per month.

If you drive a vehicle for your business purposes, ie. driving from one customer’s house to another or driving to Home Depot to get additional supplies, you must have commercial auto insurance. Your personal auto insurance doesn’t cover your business driving. Learn more at why small businesses need to have commercial auto insurance

Commercial auto insurance provides similar coverages to personal auto policy such as liability (both bodily injury and property damage), collision, comprehensive, underinsured and uninsured, etc.

Commercial auto insurance for landscapers varies depending on several factors such as location, the type of car, your driving record, the nature of your landscaping business, years of experience, etc.

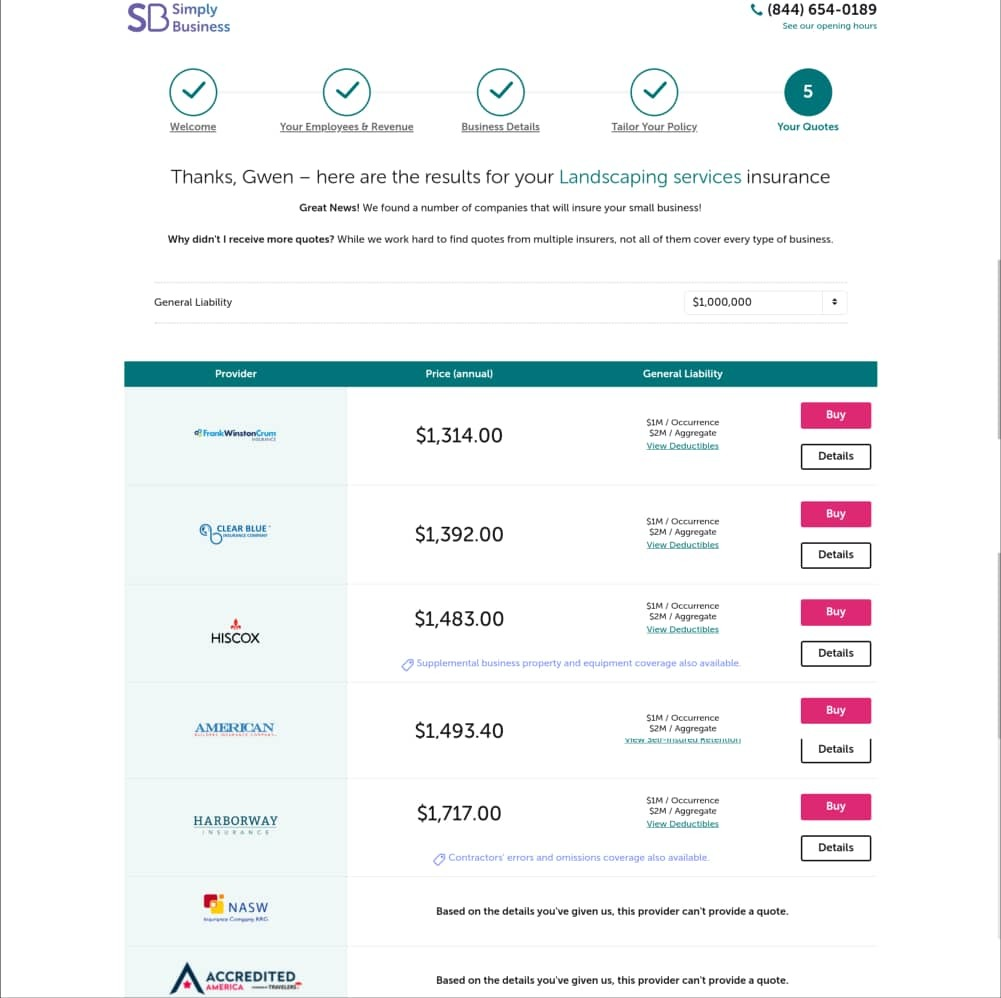

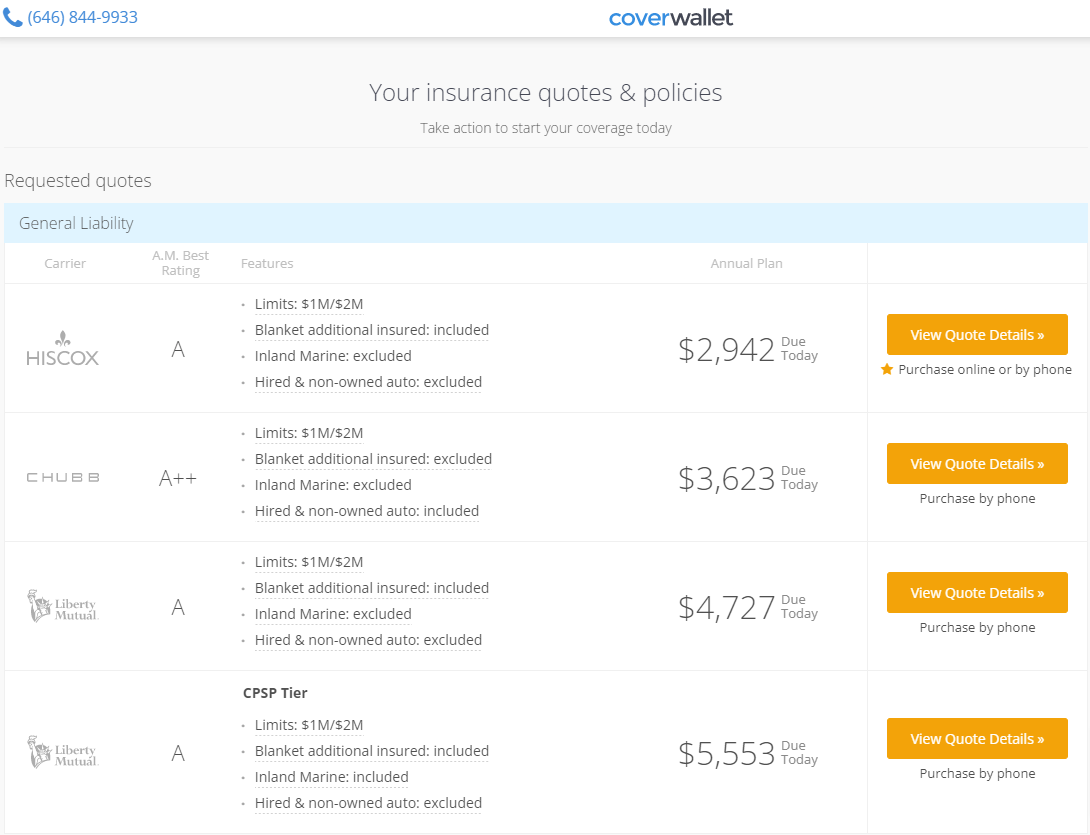

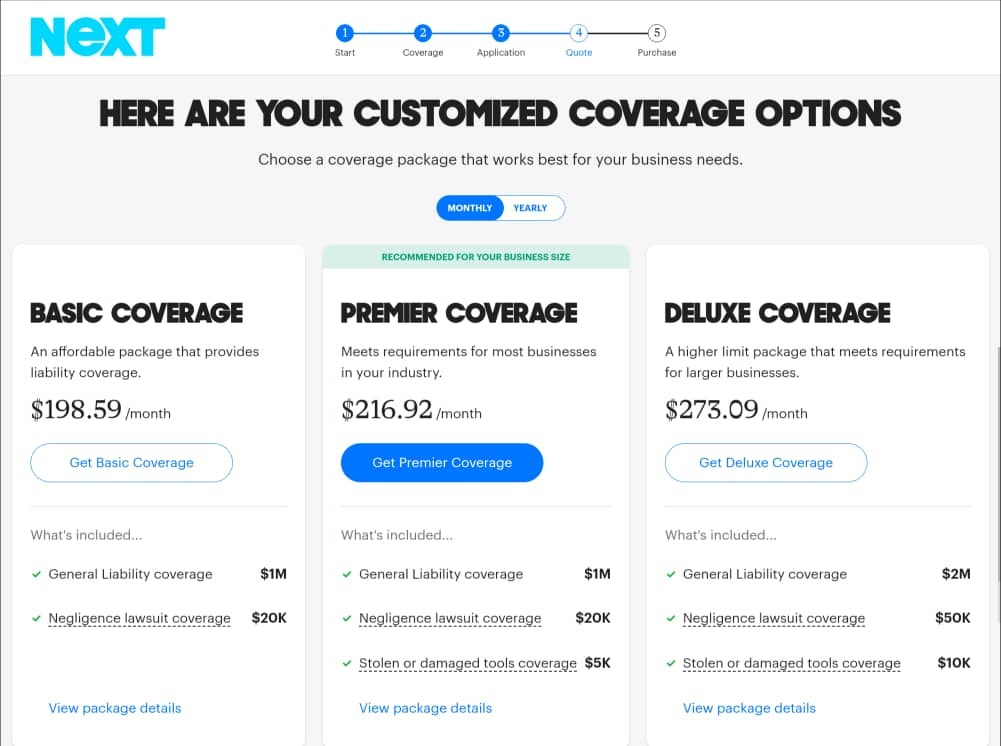

Where to get landscaping insurance quotes online?

Among the coverages that landscapers need, general liability insurance is the most important one. It is often the one policy that most landscaping contractors should have since most clients would require it.

Many companies offer this coverage for landscapers. However, only a few offers quotes online. Below are the three providers that offer landscaping general liability insurance quotes online. It shouldn’t take more than 10 minutes to obtain these quotes on their websites. They make it easy and convenient for you to compare several quotes online to choose the cheapest one for your landscaping business.

- Simply Business: Best for finding the cheapest landscaping general liability insurance coverage

- CoverWallet: Best for comparing several quotes from reputable companies

- NEXT: Best for a great digital experience and fast coverage

The following are some quotes for landscaping insurance from some insurers.

Factors influencing the cost of landscaping insurance

The cost of insurance for your landscaping business varies depending on the following variables:

What landscaping solutions do you provide?

Your insurance premium is impacted by the landscaping services you provide. If you provide simple lawn care and yard maintenance, insurers will rate your company as lower risk. As a result, you will pay less for a policy than, say, a major company that does excavation and tree removal.

Typically, a tree service business will spend $1,600 a year on general liability insurance. While a landscape architect might only pay $500.

Where is your business located?

The cost of your landscaping policy may be significantly impacted by your company’s location. You’ll pay more if you’re based in California than you would if you were in Ohio.

However, the price is influenced by more than just your state of residence. Another consideration is where you are in the state. You may discover that your insurance cost is higher if you operate your business in an area where real estate is pricey.

Your yearly business revenue

In general, the bigger the annual revenue of your landscaping company, the more expensive your coverage will be. Insurance companies believe companies with higher business revenue have higher potential exposure. That is, companies with higher revenue tend to pay more if sued, and so the insurer will charge more to insure them.

The cost of your machinery or property

The more expensive the equipment is to insure, the more you’ll pay. But resist the urge to underestimate your tools. If you undervalue your tools, you risk getting less than their value if an insured peril happens.

Number of employees

Most states require businesses to have workers’ compensation insurance so long as they have one employee. Usually, workers comp is calculated per employee payroll. The more employees you have, the higher your worker’s comp insurance. Additionally, the more workers you have, the more expensive your general liability insurance will be.

Your annual payroll

Insurers typically calculate workers’ compensation insurance using your annual payroll. Generally speaking, your worker’s comp insurance cost will increase with every $100 increase in payroll.

The deductible that you select

A deductible is the sum of money you consent to pay toward the expense of a claim. Generally speaking, your coverage premium will be lower if you pay higher deductibles. However, a higher deductible means you will pay more in the event of a claim. So you might want to reconsider the urge to pay a high deductible if you are not sure you can afford it in case of a claim.

Limits on coverage

The amount your insurance company will pay out on a claim depends on the policy limit you select. A policy with a high limit will cost more, but then it offers more protection and a higher payout for claims.

Two different kinds of policy limits exist:

- A per-occurrence limit, which is the most your insurance company will pay you for a single incident.

- An aggregate limit, which is the most your insurer will spend on claims made throughout your policy period, often a year.

Most small landscaping companies choose general liability insurance with a $2 million aggregate and $1 million per occurrence limit. However, when your company expands, you might want to consider raising your coverage limits.

Other insurance coverages landscapers should carry

The following are some policies that are not popular but may be beneficial for your landscaping business.

Commercial umbrella insurance

Commercial umbrella insurance is a special policy that offers protection over and above the liability limits of other primary insurance policies. Significant injuries or lawsuits may result in very high legal and medical costs that exceed the limit of your insurance policies.

For instance, if you have legal bills of about $1.8 million and your general liability insurance has a $ 1 million limit. An Umbrella can cover the extra $800 thousand bill.

Commercial umbrella insurance can help improve the liability gaps offered by general liability, commercial vehicle, and workers’ compensation insurance policies.

Generally speaking, this policy costs between $800 and $8000, depending on the insurance policy you are using it for.

Insurance for commercial property

This policy covers the commercial structure that houses your landscaping business, whether you own, rent, or lease it. Think about getting commercial property insurance to cover that.

By integrating this commercial insurance into your landscape insurance policy, you can recover losses if one of the following occurs:

- Your commercial building was harmed by fire, theft, vandalism, severe weather, or other covered risks.

- Your landscaping business’s commercial structure was destroyed by fire or severe weather.

Generally speaking, business property insurance for landscapers ranges from $500 to $1000 per year.

How to get cheap landscaping insurance?

To reduce the cost of your landscape insurance, the following are some ideas that might help:

Buy multiple policies

If you need more than one policy, consider buying them from the same insurer. Some insurers offer customized policies with coverage options tailored to your needs. When you buy these multiple policies at once, you may get discounts on each policy.

Pay your premiums in full

Most insurers appreciate customers that pay their premiums annually instead of monthly. So, when you pay in one lump sum, they might offer you up to a 10% discount or even more.

Make safety a priority

When you keep to the safety guidelines of landscaping, you reduce the number of claims you have. Usually, fewer claims mean lower prices.

Check multiple companies for quotes

Some insurers offer good protection at less expensive rates. However, you may not know if you do not search around. Therefore, do a little research before making your purchase. Ideally, you want to compare quotes from up to 3 companies before making your purchase decision.

Best landscaping insurance companies

Several companies offer business insurance for landscaping contractors. We have researched more than 30 companies and here are our recommendations for the top 6 providers:

- CoverWallet: Best for comparing online quotes

- Progressive: Best for commercial auto insurance

- NEXT Insurance: Best for fast quotes and instant coverage

- Hiscox: Best for mid-sized businesses who prefer a combination of online tools and agent advice

- Thimble: Best for landscaping businesses who only need insurance coverage for a few days

- The Hartford: Best if you prefer a reputable brand in the business insurance industry