According to the US Bureau of Labor Statistics, about 207 incidents of fatal injuries in Georgia in 2019. Unfortunately, private businesses recorded the highest number of casualties. These numbers prove to you that accidents are a normal part of business. Everyone makes mistakes once in a while, and sometimes, the results of those mistakes might be life-threatening.

The question, however, is, is your business prepared to face the risks that come with workplace injuries? The answer to that is to get workers’ comp insurance.

Asides from offering you the needed protection, the state laws demand most businesses in the state carry workers’ compensation insurance.

This guide will find all you need to know regarding Georgia workers’ compensation. And how to shop online to get workers comp insurance as low as $34/Month.

- Buy workers comp insurance in Georgia from digital brokers

- Buy workers’ comp insurance in Georgia from traditional insurance companies

- Apply for self-insurance status in Georgia

- Buy workers’ comp insurance in Georgia from insuretech companies

- What benefits do workers comp insurance provide in Georgia?

- Is workers’ compensation insurance required in Georgia?

- Workers’ comp exemptions in Georgia

- How much does workers’ compensation insurance cost in Georgia?

Buy workers comp insurance in Georgia from digital brokers

Digital brokers do not sell policies; instead, they provide workers’ comp from their partners to businesses. These companies have online platforms where business owners can quickly compare quotes from various companies.

You can buy the policy directly from their website when you’ve found the coverage you want. Also, you can monitor and manage your policies from their website.

Examples of digital brokers you can use in Georgia include:

- CoverWallet

- Policy Sweet

- Commercialinsurance.net

- SmartFinancial

The following is a sample quote generated for a small accounting firm from CoverWallet. The hypothetical firm has two workers, $500,000 annual revenue and $170,000 annual payroll.

Pros

- If you don’t know which insurance company to start with, this is a great place to start.

- It is easier to compare insurance quotes with digital brokers.

- With digital brokers, you may manage various insurance policies from different firms.

Cons

- Digital brokers might refer you to their offline representatives sometimes to get quotes.

- Digital brokers only suggest insurance policies from their partners.

Buy workers’ comp insurance in Georgia from traditional insurance companies

Companies that choose this route purchase their coverage from insurance firms and manage claims via them. Traditional insurance companies require businesses to pay a fixed premium either annually or monthly to secure coverage.

Traditional insurance firms that provide workers’ compensation in Georgia include:

- The Hartford

- Chubb

- Amtrust Financial

- Travelers

- CNA

- AmTrust Financial

- Employers, etc.

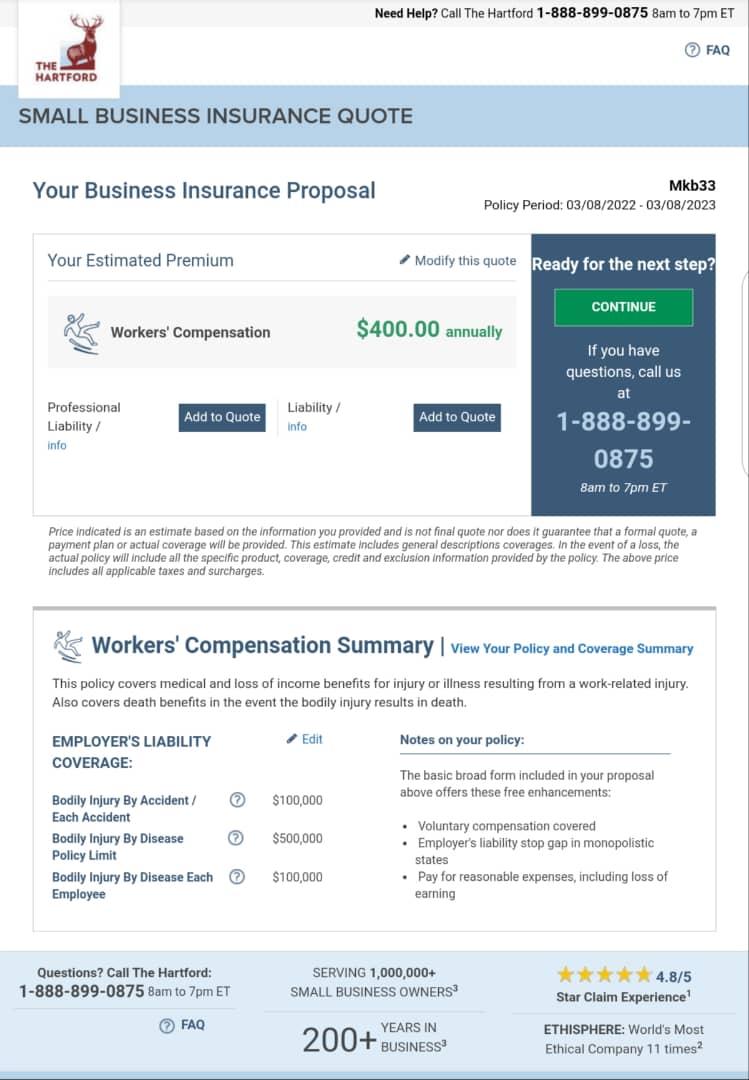

The following is a sample quote generated for a small accounting firm from The HartFord The hypothetical firm has 2 workers, $500,000 annual revenue and $170,000 annual payroll.

Pros

- These companies have extensive experience to offer workers’ comp to any business.

- Some traditional companies offer training to help your workers stay safe at work. This could lower your premiums in the future.

- Traditional insurance companies also offer discounts to companies.

Cons

- It can be pricey, depending on where you buy the coverage.

- There are too many alternatives, which may confuse new business owners.

Apply for self-insurance status in Georgia

You can also get your workers’ comp insurance in Georgia by applying for self-insurance. The term “self-insurance” refers to a situation in which the employer chooses to pay for the damages that might occur due to workers’ injuries and illnesses.

To be self-insured, you must be recognized as a member of the Georgia Self-Insurers Guaranty Trust Fund and certified by the State Board of Workers’ Compensation. Employers who want to do this must fill out an application and submit it to the Board, along with the relevant documentation and a $500 processing fee.

Pros

- Companies that self-insure avoid paying premiums that come with regular insurance companies.

- Companies that pay for their liabilities can monitor their risks and control accidents on their premises.

Cons

- Most small businesses do not have the resources to qualify for self-insurance.

- Risk assessment can be tricky. If not correctly done, the company might pay more in the event of injuries.

Buy workers’ comp insurance in Georgia from insuretech companies

Insuretech companies are tech companies that use technological tools to help companies find the right policies for their businesses. They work like digital brokers; however, they are relatively new companies compared with digital brokers. To buy policies from these companies, you have to visit the website of these companies and request quotes. The process usually takes about 5 minutes.

Pros

- Some of these companies claim they can help you find cheap quotes.

- These companies are focused on giving you the best user experience. Therefore, the quote generation process is faster than with other companies.

Cons

- These companies are relatively new players, and they might not have enough experience to offer policies for companies in risky industries like construction.

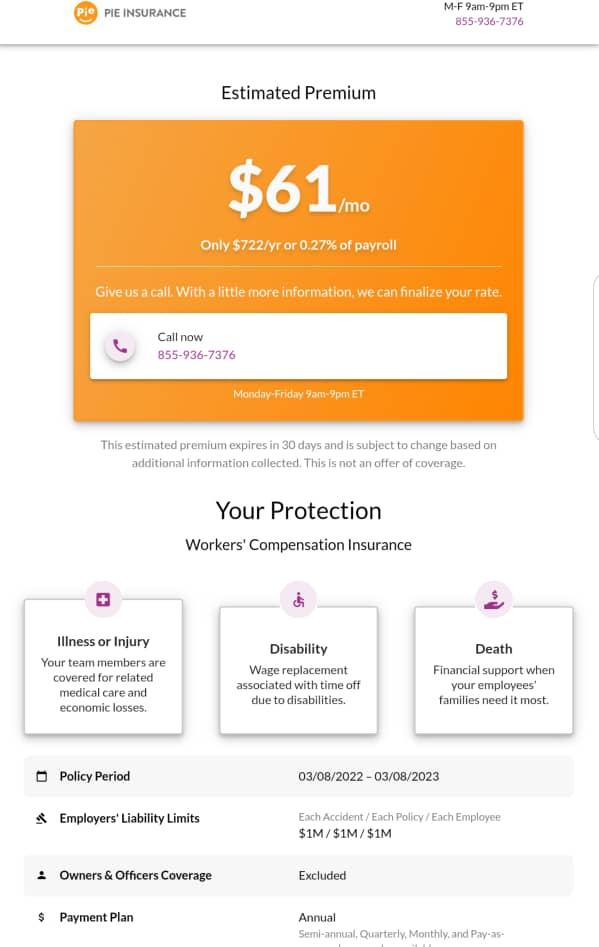

The following is a sample quote generated for a small accounting firm from Pie Insurance. The hypothetical firm has two workers, $500,000 annual revenue and $170,000 annual payroll.

Learn more at the best workers comp insurance companies in Georgia

How does workers comp function in Georgia?

The Georgia State Board of Workers’ Compensation (SBWC) oversees workers’ compensation cases. To arbitrate each workers’ compensation dispute, they choose an administrative law judge or a staff attorney.

According to Georgia’s workers’ compensation legislation, employers must offer workers compensation from the first day of work.

When an employee is injured, workers’ compensation insurance covers the cost of medical care supplied by an approved treating physician. This covers emergency care, hospitalization, medicines, and physical therapy.

Workers’ compensation insurance also covers temporary partial disability or temporary total disability benefits if an employee cannot work. It is usually two-thirds of their average weekly pay.

In some exceptional cases, like in the event of a partial or permanent disability, the injured employee receives monthly payments for a certain period.

A company’s liability insurance is typically included in policies, which can assist pay legal fees if an employee accuses their employer of an injury. However, the legislation that supports worker’s compensation ban employees from suing their employers if they take workers’ compensation payments.

What benefits do workers comp insurance provide in Georgia?

In terms of benefits, workers’ comp insurance has something for both employees and their employers.

Employees get to receive weekly income benefits and medical expenditures and provide death benefits in extreme instances. On the other hand, the insurance policy helps decrease employers’ responsibility for a work injury or illness.

Employers that do not have this coverage risk having their employees suing them to recover medical expenses and lost earnings due to a work-related accident or sickness.

The following are some examples of specific scenarios where workers’ compensation insurance can aid in Georgia:

- An employee develops carpal tunnel syndrome after working several years as an office secretary. Workers’ compensation may pay some of the costs of treating this repetitive strain injury.

- An employee sustains injuries to the back as he attempts to lift a heavy object. Workers’ compensation can assist in paying for their medical care, such as physical therapy or surgery.

- An employee that slips falls and breaks their wrist. Workers’ compensation might cover the cost of their emergency hospital visits as well as any follow-up consultations.

A worker’s compensation will cover all these and many other injuries, whether they are severe or not. Usually, the insurance policy will cover the following:

- Lost wages for the worker while they are receiving treatment.

- Medical expenditure in the form of medical care and supplies.

- Disability benefits in cases where the employee cannot use a body part due to the injury or illness.

- Physical therapy and other continuing care costs.

- Funeral expenses for extreme cases. This also includes compensation payments for the family of the deceased.

Is workers’ compensation insurance required in Georgia?

According to the Georgia State Board of Workers’ Compensation (SBWC), every firm in the state with three or more regular employees is required to have workers’ compensation insurance.

The term “regular” refers to someone who works for a company regularly, even if it is part-time, regardless of the employee’s average weekly income.

Corporate officials in corporations also count towards the “three or more workers” criteria. However, corporate officers can decide whether workers’ compensation coverage will cover them. But even if they are not covered, they will still count toward the total number of employees in the company.

One point of contention in Georgia at the moment is whether gig economy workers can count as employees or independent contractors. Individuals in this category include employment through apps like Uber, Lyft, or TaskRabbit.

Workers’ comp exemptions in Georgia

Georgia workers’ compensation rules have a few exclusions, but most employees who meet the conditions above are insured. It also makes no difference how long you have worked with the organization. You are protected from the first day of work.

Exceptions to the workers mentioned above’ compensation coverage requirements include (according to Georgia Code 34-9-2):

- Employees of US government agencies since they already carry federal worker’s comp insurance

- Railroad workers

- Farm laborers

- Domestic servants

- Employees of enterprises with less than three regular employees

Under Georgia law, if you are a sole proprietor or manage your firm as a partnership, you are regarded as an employer rather than an employee. As such, you are exempted from the coverage. However, if you desire the coverage, you can write to your insurance provider and request to be covered as an employee.

There are various circumstances in which workers’ compensation may not cover an injury, even if it happens at work. For instance, if an accident occurs while a worker is under the influence of drugs or alcohol, such worker forfeits their worker’s comp benefits.

Similarly, if an injury occurs during a workplace fight or due to horseplay at work, such injuries may not be covered. However, these sorts of scenarios are uncommon and do not account for the vast majority of work-related injuries.

What if I don’t have the required workers’ comp?

An employer who does not buy workers’ compensation in Georgia commits a criminal offense. Such businesses may face severe penalties for violating state workers’ compensation regulations.

This might result in both financial fines and legal ramifications, such as:

- Imprisonment for up to 12 months

- Lawsuits on behalf of injured workers

- Payment of attorney’s costs, civil fines, and an extra 10% compensation for the injured worker

- Penalties of up to $10,000

Suppose you do not have workers’ compensation insurance in Georgia. In that case, you might end up paying significantly more in penalties and settlement than you would have paid for the coverage in the first place. Furthermore, if you obtain coverage, your rates would most certainly be more significant than if you had maintained coverage without gaps.

How much does workers’ compensation insurance cost in Georgia?

Compared to the national average, the price of worker’s compensation in Georgia is relatively high. According to a 2018 assessment conducted by the Oregon Department of Consumer and Business Services, Georgia is rated sixth in the United States.

As a business owner in Georgia, you can expect to pay anything between $1.00 and $2.49 per $100 covered wages.

The National Council on Compensation Insurance (NCCI), which most states employ as their rating bureau, recommends Georgia workers’ compensation rates. NCCI gathers workplace injury data and provides rates based on classification code or industry categorization. Businesses are classified using class codes, and NCCI sets rates to each class code depending on the relative risk of disease or injury.

The insurance carrier calculates the ultimate premium cost based on the suggested rate from the NCCI, the company’s payroll, the Experience Modifier, and any additional credits or debits depending on workplace safety.

As you can see above, different insurance companies will provide you with different quotes. Be sure to shop around with a few companies to compare several quotes before making your final decision

>>MORE: How Much does Workers Comp Insurance Cost?

Who pays for workers’ compensation insurance in Georgia?

In Georgia, the payment for worker’s compensation is the employer’s responsibility. Therefore, it is wrong for employers to make deductions from their employees’ salaries to pay for this coverage. Employers that do this can be liable for prosecution.

How do I find cheap workers’ comp insurance in Georgia?

In some cases, insurance companies may offer discounts to their clients using an Experience modifier. The Experience modifier is a tool that companies calculate discounts based on your premium and safety score.

Your safety score refers to how the company perceives your business as risky. Using the tool, businesses that have not filed any claims in the past may be eligible for discounts.

Some other things you can do includes:

- Look around for the best prices.

- Consider cutting the size of your payroll.

- Commit to health and safety at your place of work.

Learn more at the cheapest workers comp insurance companies.