If you run catering business, you know the catering business operations may run into different types of risks. Getting the right catering insurance coverage to protect your business is highly advisable. The question is where you can get and compare catering insurance quotes online to choose the best and the cheapest one for your business.

- 4 best companies where you can get online catering insurance quotes

- What is a catering insurance quote?

- Where to get catering insurance quotes: insurers or brokers?

- When does it make sense to get online catering insurance quotes from the insurer?

- When does it make sense to get online catering insurance quotes through a broker?

- Which information do you need to get catering insurance quotes online?

- How much does catering insurance cost?

- How to reduce your catering insurance cost?

4 best companies where you can get online catering insurance quotes

Several companies offer catering insurance. However, not many companies offer quotes online. Below are some companies offer catering insurance quotes online that we recommend you checking out.

- InsurePro: Best for pay-per-day catering insurance quotes

- Simply Business: Best for finding low-cost catering quotes

- CoverWallet: Best for comparing several quotes online

- Thimble: Best for catering businesses that hire part-time employees

InsurePro: Best for pay-per-day catering insurance quotes

InsurePro is one of the latest insurance companies in the industry. Like any other insurance company, they have policies covering caterers and their business with a little twist. Their company offers insurance with flexible terms such that you can buy insurance for single events or just a day. You might consider getting your quotes from InsurePro if you need flexible catering insurance options.

If your catering business only needs the coverage for a few days for whatever reason, getting pay-per-day coverage from InsurePro will save you a lot of money.

Besides offering online quotes, InsurePro also offers “chat to buy”, it is easy and convenient to provide some information about your catering business on chat and receive quotes back. You can also easily ask clarification questions and for additional details. Our experience of using their chat function is really good. Within 10 minutes, we have quotes, all questions answered and explained, and ready to buy, and download the certificate of insurance.

Simply Business: Best for finding low-cost catering quotes

Simply business is another insuretech broker specializing in small business insurance. The team claims they can help small businesses find cheap and affordable insurance policies. Using artificial intelligence and other state-of-the-art technology, the company helps its clients locate the best policies for them at the best price.

If your number #1 goal is to get the cheapest catering insurance policy, you may want to consider Simply Business. They utilize their technology to find the most affordable policy with the right coverage for your catering business. The quote they present to you is always the cheapest one that they could find for the right coverage.

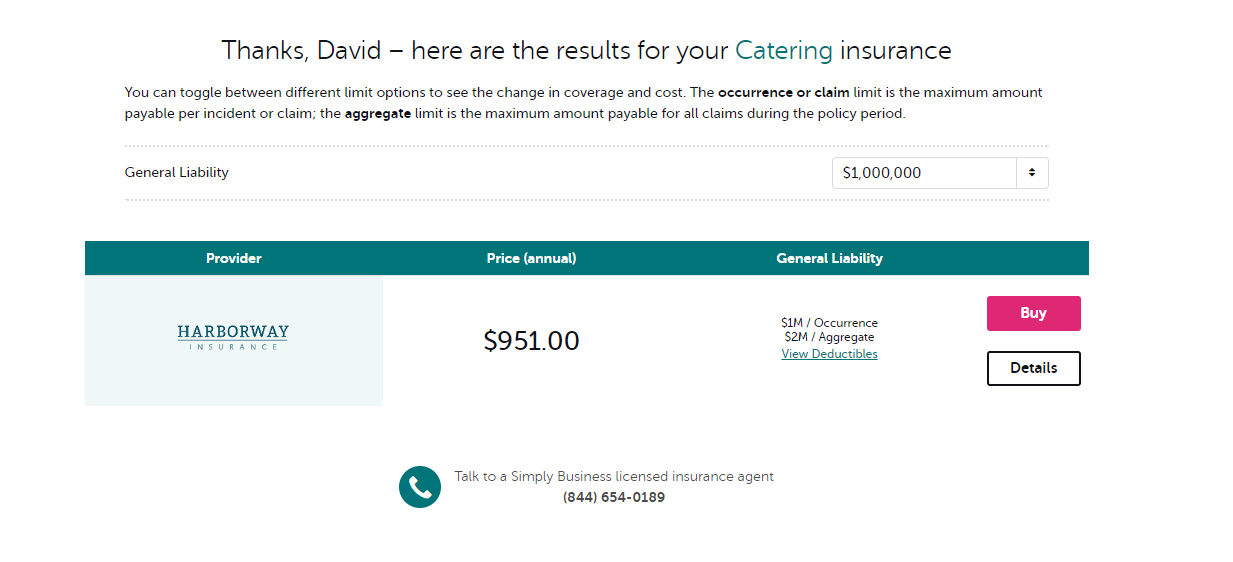

The following image is a sample quote for a small catering company located in Bakersfield, California, from Simply Business. Among all the quotes we have found for the same catering business in Bakersfield, CA, this is by far the cheapest one, at $79.25 per month.

CoverWallet: Best for comparing several quotes online

CoverWallet is an online broker that helps small businesses find the best insurance quotes. The company does not have any policy of its own. Instead, they work with several leading insurance companies and help small businesses like caterers find the best policy that suits their needs.

CoverWallet might be ideal for finding your catering if you have not bought catering insurance before. It might also be a good place if you are looking for better carriers that offer your current policies.

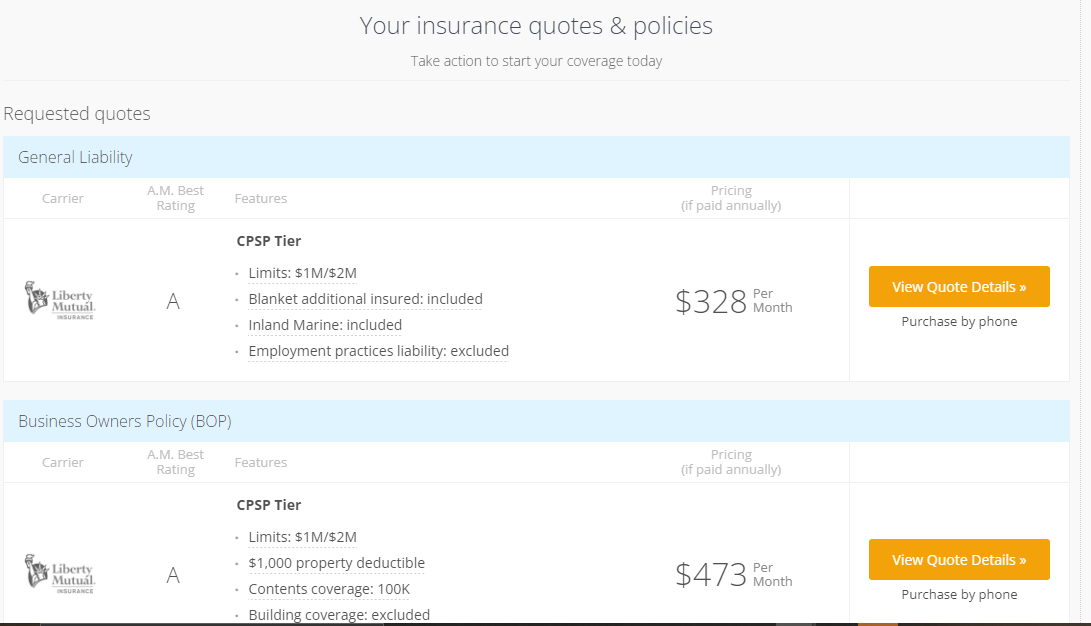

Here is a sample quote for a small catering company located in Bakersfield, California, from CoverWallet:

Thimble: Best for catering businesses hiring part-time employees

Thimble sells business insurance online. The company, however, depends on another insurer to underwrite its policies. So, if you have claims, you have to reach out to the insurer underwriting your policy. Similar to InsurePro, Thimble also provides temporary coverage for catering businesses and its employees. If your catering business often hire part-time employees for different events and need to add these part-time employees to your catering business insurance policy, you may want to get a quote from Thimble because their policies are made flexible to support that.

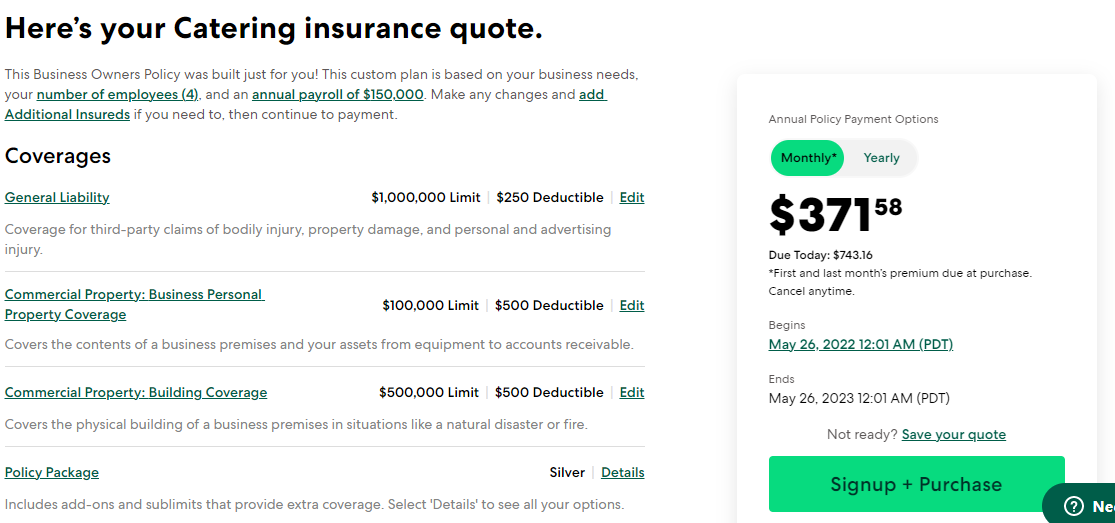

The following is a sample quote for a small catering company in Bakersfield, California, gotten from Thimble.

What is a catering insurance quote?

A catering insurance quote is simply an estimate you get from an insurer or a broker on how much your intended policy with its coverages and limits would cost you. It’s important to note that a quote is only an estimate, not the final price you will pay. In most cases, the difference between a quote and the final price is very minimal unless you provide some wrong information about yourself or your business in the quote application.

In some cases, insurance companies may increase or reduce your quotes if new information is available about your catering business. For instance, if you employ more staff after requesting a quote, your insurer reserves the right to adjust the quote to match the new information available to them.

However, to avoid disparities like this, insurance companies typically provide the final rate only when they are confident that you will purchase a policy. Usually, most companies will consider you have made up your mind when you accept to fill in your payment details, such as credit card information.

Just before you checkout, the company will likely run a final check on the data you provide and confirm your final rate only at that time.

Where to get catering insurance quotes: insurers or brokers?

You may obtain your catering insurance policy directly from an insurance company or through agents or brokers. Either way, the route you choose does not impact the price of your insurance in most cases.

Depending on the company and the insurance policy, you can obtain your quotes online or speak with a company agent. When getting quotes from the insurer, they will request your information and offer you a quote in about 10 minutes. The company may also call you to finalize the quotes if they need to clarify some things.

It works the same way for online brokers; the only difference is that they can help you get multiple quotes from different companies. When you use an online broker, they can give you suggestions on the best available and sometimes the cheapest options for your company. That makes comparing quotes easier.

If you like a carrier’s online quote, you can immediately buy and start your policy from the broker’s website. When you choose the best one for you, they will write you a policy.

When does it make sense to get online catering insurance quotes from the insurer?

If you are already familiar with insurance policies and know what you need, you should get your quotes directly from the company. Depending on the insurer you choose, quotes may be available online via their website, or you can use their agents. Companies that use agents usually have them in most states and areas to allow ease for their clients.

If you think you have done the needed research, feel free to pick the company that your research leads you to.

When does it make sense to get online catering insurance quotes through a broker?

If you are unsure what to get, an online broker would be a better option. Plus, brokers make it easy for caterers with complex or specific insurance needs. These companies will help you find the right policies at the best price. Generally speaking, you might need an online broker if you fall into these categories:

- You are not sure of what insurance policy to buy

- You are trying to cut costs by comparing quotes

- You do not understand what catering insurance is, the limits, deductibles, etc.

- You don’t have all the time to do thorough research to find the right coverage and insurer for your catering business

Which information do you need to get catering insurance quotes online?

The information you need to provide depends on the policies you need, the insurance company, and government regulations. But in most cases, the following are some basic business info you must supply before getting a quote.

- The type of catering service you offer

- Number and types (part-time, full time or volunteers) of employees

- Location (zip code and address)

- Total payroll for all employees

- Claims history

- Business experience

- Annual sales and revenue

- Coverages and limits

- Business ownership details

- Value of your business property

- Employer identification number (EIN) or social security number (optional) – Most online quote providers don’t require this to get a quote, but they do before you buy the policy online.

How much does catering insurance cost?

The average catering insurance cost is $95 per month, or $1,180 per year. That is for a Business Owners Policy (BOP), the most popular insurance policy for small businesses, including catering business.

The catering insurance cost varies depending on several factors such as the business size, experience, the coverage that you get, the location, the policy terms such as coverage limits and deductibles, and the claim history, just to name a few important factors.

Different insurance companies will provide different quotes for a catering business. So make sure you shop around with a few companies to get and compare several quotes. We recommend to get quotes from InsurePro, Simply Business, CoverWallet, and Thimble to start with.

Learn more about the details of catering insurance cost here.

How to reduce your catering insurance cost?

Premiums for insurance can add up quickly for catering businesses. If you can find ways to cut those costs, the money leaving your company will decrease.

Besides, finding ways to lower your premiums can also help you identify ways to improve the efficiency of your catering company.

Here are seven options for lowering your catering insurance costs without compromising coverage.

Prioritize work safety

By training and educating your employees about proper workplace safety practices, you can avoid potential increases in workers’ compensation and general liability insurance rates. You can create your training or hire a third party to run a program or seminar for you.

As new procedures and technologies become available, you need to conduct research and plan to implement those that will benefit your catering company the most. Maintain consistency in your training and review your safety policies regularly to make necessary adjustments and updates.

Show that your company is running well

Insurers charge lower premiums for well-run businesses because they are less likely to have claims. To demonstrate that your catering business is doing well, you can do the following:

- Evaluate your business risks

- Have a working quality assurance process

- File your financial accounts on time

- Conduct financial audits

- Have professional accreditations and qualifications, training, and ongoing development for you and your employees

Buy comprehensive packages

Most insurers offer discounts on individual policies when you buy multiple policies. You might consider combining your essential business coverage into one package to save money on premiums. A good example is a Business Owners’ Policy.

Compare policies

Different companies have different standards for measuring risks. This is why the cost of catering insurance varies across insurers. To be sure you are getting the best deal on your policy, try to compare the quotes offered by other companies to see if you’d be better off switching providers.

Go over your employee classifications

Workers’ compensation class codes inform insurance companies about the work that each of your employees does. Using incorrect classifications and incorrectly classifying employees as having high-risk jobs may result in higher insurance premiums.

For instance, your servers do not have the same risks as the chefs in the kitchen. Chefs would naturally attract higher workers’ comp rates due to the nature of their job. However, if you put all your staff under the same classification code, you might pay the same high fees for chefs and servers.

When reviewing your insurance policies, reviewing employee classifications can help you spot costly mistakes that need to be corrected.

Misclassifying employees on purpose to save money is unethical, leaves employees without essential coverage, and can result in serious financial penalties.

Think about hiring an insurance broker

Catering Insurance can be a difficult product to purchase without professional assistance. A broker can guide you through the process and help you choose the right insurance coverage for you. The broker represents you and should conduct a market search to find the best insurer for you.

Compare insurance rates every year

Automatically renewing your insurance is not a good idea. Whether you have an established business or are just getting started, comparing the rates offered by various insurance companies each year can save you money.

To get a realistic idea of how much you can save by choosing one provider over another, compare similar or identical coverage, and contact the provider for clarification on any terms or restrictions you don’t understand.